Reports

Sale

Global Polyethylene Naphthalate (PEN) Market Share, Growth: By Type: Film, Fibre, Resin; By Application: Beverage Bottles, Food Packaging, Electronic Goods, Rubber Tyres, Textiles, Others; Regional Analysis; Market Dynamics: SWOT Analysis, Porter’s Five Forces Analysis, Key Indicators for Demand; Competitive Landscape; 2024-2032

Global Polyethylene Naphthalate (PEN) Market Outlook

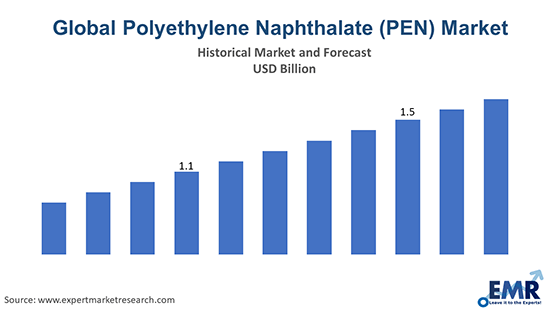

The global polyethylene naphthalate (PEN) market size reached a value of nearly USD 303.36 million in 2023. The market is projected to grow at a CAGR of 11.2% between 2024 and 2032 and reach around USD 787.77 million by 2032.

Key Takeaways

- In the food packaging sector, PEN is rising in popularity as a packaging material as it reduces the permeability of gases, flavour, and vapour in or out of containers.

- Indorama Ventures Public Company Limited, Kolon Plastics Inc., and DuPont Teijin Films Ltd. are some major companies in the market.

- The polyethylene naphthalate (PEN) market is driven by the rising demand for electronic goods.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

PEN offers oxygen permeability, improved hydrolysis resistance, high heat, temperature resistance, enhanced tensile strength and service temperature, and lower elongation and shrinkage due to its higher glass transition temperature. As a result, PEN outperforms PET in demanding electronics applications, such as electrical insulation, flexible printed circuits, and capacitors in the electronics sector.

Some of the factors driving the polyethylene naphthalate (PEN) market growth are the growing adoption of renewable energy resources and the robust growth of the food packaging sector. PEN-based back sheets for solar panels have high transparency, excellent thermal resistance, long lifetime, high chemical resistance, and good mechanical strength compared to PET. As a result, they find use in solar panel back sheets. In 2022, the global solar power generation increased by a record 270 TWh, a 26% year-on-year surge. Further, solar PV accounted for 4.5% of total global electricity generation.

Regulations for PEN Use in Food Packaging Applications in the USA

- If a manufacturer wants FDA to consider the use of recycled plastic for a food-contact application, they should provide a complete description of the recycling process and steps that are taken to ensure that the recyclable plastic is not contaminated.

- Surrogate contaminant testing is not needed to demonstrate that PCR polyethylene terephthalate (PET) or PEN produced by a tertiary recycling process is suitable for food-contact use. This is because the FDA has determined that tertiary recycling processes produce PCR-PEN or PET with suitable purity for food-contact use.

- Further, they need to provide a description of the proposed conditions of plastic use. For instance, information on the intended temperature of use, the food the plastic will come in contact with, the duration of the contract, and whether the plastic will be for repeated or single-use applications.

Key Trends and Developments

Excellent properties of PEN; the thriving electronics sector; growing demand for solar energy; and rising applications of PEN in electric vehicles are favouring the polyethylene naphthalate (PEN) market expansion

August 2021

DuPont Teijin Films announced the re-introduction of Kaladex® polyethylene naphthalate (PEN) high-performance polyester films, which were originally produced at its facility in Dumfries, the United Kingdom.

June 2021

Indorama Ventures Xylenes & PTA, LLC (IVXP) added a new PNDA (Purified 2,6-Naphthalene Dicarboxylic Acid) production line, at IVXP’s integrated manufacturing site in Decatur, Alabama, the United States.

The superior performance of PEN than PET

PEN films offer a higher glass transition temperature, long-term ageing performance at elevated temperatures and better dimensional stability, boosting their demand as an alternative to PET in different applications in sectors like electronics and automotive.

Downstream demand for PEN from the electronics sector

Capacitors are rising in prominence owing to the growing demand for consumer goods, such as smartphones, laptops, tablets, smart TVs, wearable technology, and IoT products, driving the market expansion.

Growing demand for PEN from the food packaging sector

PEN films are widely used for flexible food packaging as they add durability and strength to food and beverage packages.

Growing demand for solar energy

When compared to PET, PEN-based back sheets have superior mechanical strength, high chemical resistance, extended lifetime, and excellent transparency. As a result, they are used in solar panel back sheets.

Rising adoption of EV

PEN is increasingly being used to manufacture lightweight automotive components for improved fuel efficiency. The expanding demand for EVs necessitates the need for PEN.

Global Polyethylene Naphthalate (PEN) Market Trends

Many notable consumer-packaged-goods companies such as Nestlé S.A. and The Kraft Heinz Company are committed to reducing their packaging waste and increasing recyclability in packaging. This key trend favours the demand for esters such as PEN in the packaging sector due to their property of recyclability.

Furthermore, the PEN demand from the automotive sector is surging due to expanding EV demand. In 2022, the global electric car market witnessed exponential growth, with sales exceeding 10 million. In March 2023, the EU adopted new CO2 standards for cars and vans calling for a 55% and 50% reduction in emissions of new cars and vans by 2030 as compared to 2021, and 100% for both vehicles by 2035. Such regulations are expected to favour the polyethylene naphthalate (PEN) market expansion in the coming years.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market Segmentation

Global Polyethylene Naphthalate (PEN) Market Report and Forecast 2024-2032 offers a detailed analysis of the market based on the following segments:

Market Breakup by Type:

- Film

- Fibre

- Resin

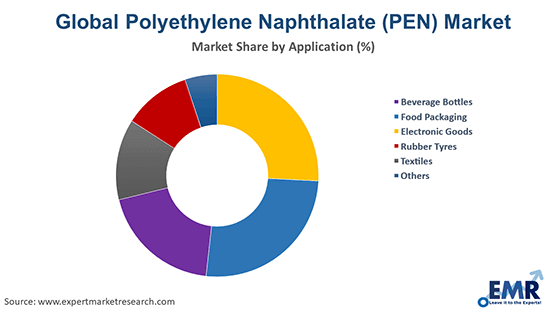

Market Breakup by Application:

- Beverage Bottles

- Food Packaging

- Electronic Goods

- Rubber Tyres

- Textiles

- Others

Market Breakup by Region:

- North America

- Europe

- Asia Pacific

- Rest of the World

PEN film is expected to dominate the polyethylene naphthalate (PEN) share due to its increased use in isolation transformers and magnetic tapes.

PEN film offers high rigidity, dimensional stability, and electrical insulation. As a result, there is a rising demand for PEN film in various applications, including flexible printed circuits, solar and photovoltaic cells, automotive, flexible heaters, electronic components like capacitors and electrical insulation, batteries, and optical applications.

Besides, PEN fibres exhibit greater initial stiffness, making them an appealing alternative for various applications, including mooring ropes and more.

Meanwhile, PEN resins are crystallised, making it easier to shape transparent moulded products. As a result, these are widely used in bottles. They offer advantages like moisture barrier, gas barrier, heat resistance, and UV ray absorption, and are particularly suitable for components demanding transparency, heat resistance, or chemical resistance. As a result, they find applications in cosmetic packaging, tableware, medical product containers, and additives to enhance the performance of PET.

Competitive Landscape

Major players in the polyethylene naphthalate (PEN) market are increasing their collaboration, partnership, and research and development activities to gain a competitive edge

Indorama Ventures Public Company Limited

Indorama Ventures, headquartered in Thailand and founded in 1994, offers products, including PEN, NDC, PNDA, PENCo, PBN and PTN, among others.

DuPont Teijin Films Ltd. (Toyobo Co. Ltd.)

DuPont Teijin, headquartered in the United States and founded in 2000, is a global market leader in the chemical sector. The company provides PEN polyester films, including Kaladex® polyester films, for electrical applications such as capacitors, wires, cables, and motors.

Kolon Plastics Inc.

Kolon Plastics Inc., headquartered in South Korea and founded in 1996, offers polyethylene naphthalate products under the brand NOPLA®-PEN-PET, a transparent material commercialised as PEN-PET copolyester.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Global Polyethylene Naphthalate (PEN) Market Analysis by Region

The Asia Pacific accounts for a major market share due to government initiatives aimed at promoting the expansion of the chemical sector. Initiatives such as the 14th Five Year Plan in China for the development of the chemical fibre sector support the production and adoption of PEN. China is the largest producer and consumer of ethylene glycol, globally which is a key raw material for PEN production.

The Europe polyethylene naphthalate (PEN) market is driven by the growing need for sturdy packaging. The packaging sector accounts for about 40% of Europe's plastic production. PEN's attributes like shrinkage resistance, dimensional stability, superior barrier qualities, and heat resilience make it a favoured barrier material.

Meanwhile, North America holds a growing PEN market share, driven by the rapid growth of the food packaging sector. Due to its lightweight nature and recyclability, as well as the ability to reduce oxidation of food, PEN is witnessing a rise in popularity as a favoured material for food and beverage packaging.

Key Highlights of the Report

| REPORT FEATURES | DETAILS |

| Base Year | 2023 |

| Historical Period | 2018-2023 |

| Forecast Period | 2024-2032 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

1 Preface

2 Report Coverage – Key Segmentation and Scope

3 Report Description

3.1 Market Definition and Outlook

3.2 Properties and Applications

3.3 Market Analysis

3.4 Key Players

4 Key Assumptions

5 Executive Summary

5.1 Overview

5.2 Key Drivers

5.3 Key Developments

5.4 Competitive Structure

5.5 Key Industrial Trends

6 Market Snapshot

6.1 Global

6.2 Regional

7 Opportunities and Challenges in the Market

8 Global Polyethylene Naphthalate (PEN) Market Analysis

8.1 Key Industry Highlights

8.2 Global Polyethylene Naphthalate (PEN) Historical Market (2018-2023)

8.3 Global Polyethylene Naphthalate (PEN) Market Forecast (2024-2032)

8.4 Global Polyethylene Naphthalate (PEN) Market by Type

8.4.1 Film

8.4.1.1 Historical Trend (2018-2023)

8.4.1.2 Forecast Trend (2024-2032)

8.4.2 Fibre

8.4.2.1 Historical Trend (2018-2023)

8.4.2.2 Forecast Trend (2024-2032)

8.4.3 Resin

8.4.3.1 Historical Trend (2018-2023)

8.4.3.2 Forecast Trend (2024-2032)

8.5 Global Polyethylene Naphthalate (PEN) Market by Application

8.5.1 Beverage Bottles

8.5.1.1 Historical Trend (2018-2023)

8.5.1.2 Forecast Trend (2024-2032)

8.5.2 Food Packaging

8.5.2.1 Historical Trend (2018-2023)

8.5.2.2 Forecast Trend (2024-2032)

8.5.3 Electronic Goods

8.5.3.1 Historical Trend (2018-2023)

8.5.3.2 Forecast Trend (2024-2032)

8.5.4 Rubber Tyres

8.5.4.1 Historical Trend (2018-2023)

8.5.4.2 Forecast Trend (2024-2032)

8.5.5 Textiles

8.5.5.1 Historical Trend (2018-2023)

8.5.5.2 Forecast Trend (2024-2032)

8.5.6 Others

8.6 Global Polyethylene Naphthalate (PEN) Market by Region

8.6.1 North America

8.6.1.1 Historical Trend (2018-2023)

8.6.1.2 Forecast Trend (2024-2032)

8.6.2 Europe

8.6.2.1 Historical Trend (2018-2023)

8.6.2.2 Forecast Trend (2024-2032)

8.6.3 Asia Pacific

8.6.3.1 Historical Trend (2018-2023)

8.6.3.2 Forecast Trend (2024-2032)

8.6.4 Rest of the World

9 North America Polyethylene Naphthalate (PEN) Market Analysis

9.1 United States of America

9.1.1 Historical Trend (2018-2023)

9.1.2 Forecast Trend (2024-2032)

9.2 Canada

9.2.1 Historical Trend (2018-2023)

9.2.2 Forecast Trend (2024-2032)

10 Europe Polyethylene Naphthalate (PEN) Market Analysis

10.1 Spain

10.1.1 Historical Trend (2018-2023)

10.1.2 Forecast Trend (2024-2032)

10.2 Germany

10.2.1 Historical Trend (2018-2023)

10.2.2 Forecast Trend (2024-2032)

10.3 France

10.3.1 Historical Trend (2018-2023)

10.3.2 Forecast Trend (2024-2032)

10.4 Belgium

10.4.1 Historical Trend (2018-2023)

10.4.2 Forecast Trend (2024-2032)

10.5 Others

11 Asia Pacific Polyethylene Naphthalate (PEN) Market Analysis

11.1 China

11.1.1 Historical Trend (2018-2023)

11.1.2 Forecast Trend (2024-2032)

11.2 Japan

11.2.1 Historical Trend (2018-2023)

11.2.2 Forecast Trend (2024-2032)

11.3 India

11.3.1 Historical Trend (2018-2023)

11.3.2 Forecast Trend (2024-2032)

11.4 Vietnam

11.4.1 Historical Trend (2018-2023)

11.4.2 Forecast Trend (2024-2032)

11.5 Others

12 Market Dynamics

12.1 SWOT Analysis

12.1.1 Strengths

12.1.2 Weaknesses

12.1.3 Opportunities

12.1.4 Threats

12.2. Porter’s Five Forces Analysis

12.2.1 Supplier’s Power

12.2.2 Buyer’s Power

12.2.3 Threat of New Entrants

12.2.4 Degree of Rivalry

12.2.5 Threat of Substitutes

12.3 Key Indicators for Demand

12.4 Key Indicators for Price

13 Price Analysis

14 Manufacturing Process

14.1 Overview

14.2 Detailed Process Flow

14.3 Unit Operations Involved

15 Competitive Landscape

15.1 Market Structure

15.2 Global Polyethylene Naphthalate (PEN) Raw Material Manufacturers

15.3 Production Capacity of Leading Global Polyethylene Naphthalate (PEN) Manufacturers

15.4 Company Profiles

15.4.1 Indorama Ventures Public Company Limited

15.4.1.1 Company Overview

15.4.1.2 Product Portfolio

15.4.1.3 Demographic Reach and Achievements

15.4.1.4 Certifications

15.4.2 DuPont Teijin Films Ltd. (Toyobo Co. Ltd.)

15.4.2.1 Company Overview

15.4.2.2 Product Portfolio

15.4.2.3 Demographic Reach and Achievements

15.4.2.4 Certifications

15.4.3 Kolon Plastics Inc.

15.4.3.1 Company Overview

15.4.3.2 Product Portfolio

15.4.3.3 Demographic Reach and Achievements

15.4.3.4 Certifications

15.4.4 Others

16 Key Trends and Developments in the Market

Additional Customisations Available

1 Project Requirement and Cost Analysis

1.1 Land, Location, and Site Development

1.2 Construction

1.3 Plant Machinery

1.4 Cost of Raw Material

1.5 Packaging

1.6 Transportation

1.7 Utilities

1.8 Manpower

1.9 Other Capital Investment

List of Key Figures and Tables

1. Global Polyethylene Naphthalate (PEN) Market: Key Industry Highlights, 2018 and 2032

2. Global Polyethylene Naphthalate (PEN) Historical Market: Breakup by Type (USD Billion), 2018-2023

3. Global Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Type (USD Billion), 2024-2032

4. Global Polyethylene Naphthalate (PEN) Historical Market: Breakup by Application (USD Billion), 2018-2023

5. Global Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Application (USD Billion), 2024-2032

6. Global Polyethylene Naphthalate (PEN) Historical Market: Breakup by Region (USD Billion), 2018-2023

7. Global Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Region (USD Billion), 2024-2032

8. North America Polyethylene Naphthalate (PEN) Historical Market: Breakup by Country (USD Billion), 2018-2023

9. North America Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Country (USD Billion), 2024-2032

10. Europe Polyethylene Naphthalate (PEN) Historical Market: Breakup by Country (USD Billion), 2018-2023

11. Europe Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Country (USD Billion), 2024-2032

12. Asia Pacific Polyethylene Naphthalate (PEN) Historical Market: Breakup by Country (USD Billion), 2018-2023

13. Asia Pacific Polyethylene Naphthalate (PEN) Market Forecast: Breakup by Country (USD Billion), 2024-2032

14. Global Polyethylene Naphthalate (PEN) Market Structure

Key Questions Answered in the Report

In 2023, the market value was nearly USD 303.36 Million.

The market is projected to grow at a CAGR of 11.2% between 2024 and 2032.

The market is estimated to witness a healthy growth in the forecast period of 2024-2032 to reach USD 787.77 million by 2032.

The major drivers include the superior performance of PEN over PET and downstream demand for PEN from the electronics, automotive and food packaging sectors.

The key trends include the growing adoption of solar energy systems and the growing application of PEN in EV production.

The different types of PEN include film, fibre, and resin.

The major applications of polyethylene naphthalate (PEN) include beverage bottles, food packaging, electronic goods, rubber tyres, and textiles, among others.

The major players in the market include Indorama Ventures Public Company Limited, DuPont Teijin Films Ltd. (Toyobo Co. Ltd.), and Kolon Plastics Inc.

Purchase Options 10% off

Call us

Purchase Full Report

Mini Report

$ 2969

$2699

-

Selected Sections, One User

-

Printing Not Allowed

-

Email Delivery in PDF

-

Free Limited Customisation -

Post Sales Analyst Support -

50% Discount on Next Update

Single User License

$ 4399

$3999

-

All Sections, One User

-

One Print Allowed

-

Email Delivery in PDF

-

Free Limited Customisation -

Post Sales Analyst Support -

50% Discount on Next Update

Five User License

$ 5499

$4999

-

All Sections, Five Users

-

Five Prints Allowed

-

Email Delivery in PDF

-

Free Limited Customisation

-

Post Sales Analyst Support

-

50% Discount on Next Update

Corporate License

$ 6599

$5999

-

All Sections, Unlimited Users

-

Unlimited Prints Allowed

-

Email Delivery in PDF + Excel

-

Free Limited Customisation

-

Post Sales Analyst Support

-

50% Discount on Next Update

Any Question? Speak With An Analyst

View A Sample

Did You Miss Anything, Ask Now

Why Expert Market Research?

Right People

We are technically excellent, strategic, practical, experienced and efficient; our analysts are hand-picked based on having the right attributes to work successfully and execute projects based on your expectations.

Right Methodology

We leverage our cutting-edge technology, our access to trusted databases, and our knowledge of the current models used in the market to deliver you research solutions that are tailored to your needs and put you ahead of the curve.

Right Price

We deliver in-depth and superior quality research in prices that are reasonable, unmatchable, and shows our understanding of your resource structure. We, additionally, offer attractive discounts on our upcoming reports.

Right Support

Our team of expert analysts are at your beck and call to deliver you optimum results that are customised to meet your precise needs within the specified timeframe and help you form a better understanding of the industry.

NEWSLETTER