Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

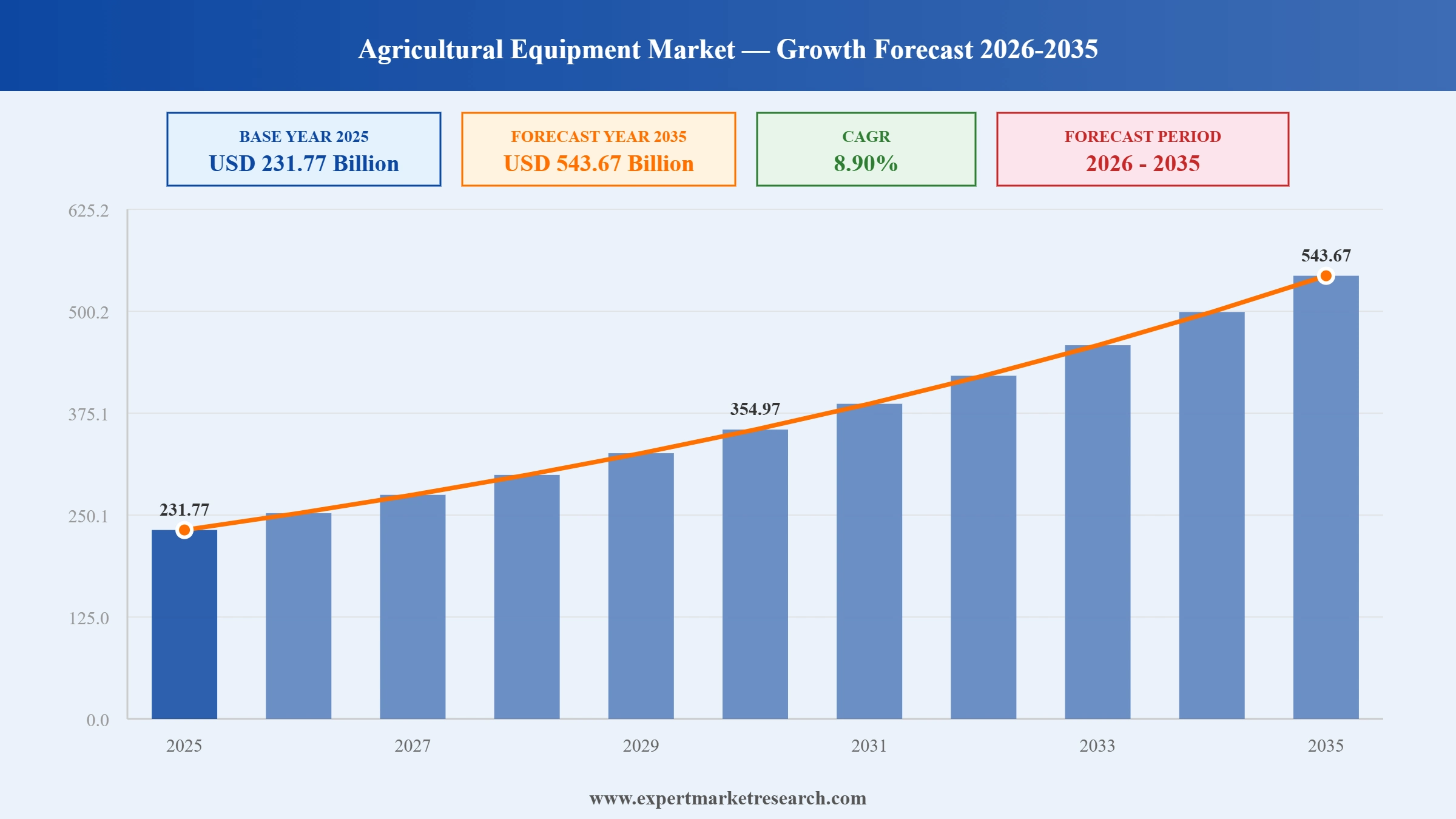

The global agricultural equipment market reached USD 231.77 Billion in 2025 and is projected to grow at a compound annual growth rate CAGR of 8.90% during the forecast period of 2026 to 2035, reaching USD 543.67 Billion by 2035, according to Expert Market Research. This sustained growth trajectory reflects the structural shift toward mechanised and technology-enabled farming practices as global agriculture confronts rising labour shortages, expanding food demand from a growing world population, and increasing pressure to improve land productivity and resource efficiency across both developed and emerging farming economies.

The agricultural equipment market encompasses the full range of machinery used across the crop production cycle, including tractors, harvesting equipment, planting and seeding machinery, tillage equipment, irrigation systems, and haying and forage equipment, alongside the precision agriculture technologies, telematics platforms, and autonomous systems that are increasingly integrated into modern farm machinery. The industry serves a global customer base spanning large-scale commercial farming operations, mid-sized family farms, and smallholder agricultural producers, with equipment specifications and price points varying substantially across mature mechanised markets and developing regions where farm mechanisation remains in earlier stages of adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Agricultural Equipment Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 231.77 |

| Market Size 2035 | USD Billion | 543.67 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 8.90% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 9.8% |

| CAGR 2026-2035 - Market by Country | India | 10.0% |

| CAGR 2026-2035 - Market by Country | China | 9.7% |

| CAGR 2026-2035 - Market by Product | Harvesters | 10.2% |

| CAGR 2026-2035 - Market by Application | Harvesting and Threshing | 10.1% |

| Market Share by Country 2025 | Australia | 2.0% |

The agricultural equipment market refers to the global commercial ecosystem encompassing the design, manufacture, distribution, and sale of machinery used in crop production, ranging from soil preparation and planting through crop maintenance, harvesting, and post-harvest handling. The market spans a broad equipment portfolio including tractors, power tillers, ploughs, rotavators, seed drills, balers, threshers and dehuskers, combine harvesters, and specialised implements for spraying, irrigation, and haying and forage operations, each engineered to address specific stages of the agricultural production cycle across diverse crop types and farming systems.

Agricultural equipment is broadly classified into powered equipment including tractors, combine harvesters, and self-propelled sprayers that incorporate their own engine and propulsion system and non-powered implements, such as ploughs, harrows, and certain seed drills, that are towed or mounted on a powered unit to perform their function. The industry is undergoing a substantial technology transformation, with precision agriculture systems including GPS guidance, variable-rate application technology, telematics, and increasingly autonomous and semi-autonomous operation capabilities becoming standard or available features across premium equipment tiers from leading global manufacturers, fundamentally reshaping how farm operations are planned, executed, and monitored.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Government subsidy programmes, farm mechanisation incentives, and agricultural credit schemes across major farming economies are providing substantial structural support for agricultural equipment market growth, particularly in emerging markets where mechanisation levels remain below those of developed agricultural economies. National agricultural policy frameworks in India, China, Brazil, and across Sub-Saharan Africa increasingly prioritise farm mechanisation as a strategic lever for improving food security, rural income, and agricultural productivity, translating into direct equipment purchase subsidies, low-interest agricultural financing programmes, and custom hiring centre initiatives that expand smallholder farmer access to modern machinery without requiring full upfront capital investment.

Structural labour shortages across major agricultural economies driven by rural-to-urban migration, an ageing farming workforce, and declining interest in agricultural careers among younger generations are creating powerful demand for labour-saving and autonomous agricultural equipment. With millions of farm jobs going unfilled annually in major markets including the United States, equipment manufacturers are responding with autonomous tractor platforms, automated harvesting systems, and remote equipment monitoring tools that allow a single operator to manage multiple machines or supervise operations remotely, directly addressing the operational capacity constraints that labour scarcity imposes on modern farming operations.

The accelerating integration of precision agriculture technology including GPS-guided steering, variable-rate input application, machine vision-based weed and crop detection, and increasingly autonomous vehicle operation is transforming agricultural equipment from mechanical tools into data-driven, intelligent systems that materially improve farming efficiency and resource utilisation. Modern equipment platforms increasingly offer satellite connectivity for real-time data transmission from remote fields, AI-driven automation features for tasks including tillage, spraying, and harvest settings adjustment, and centralised fleet management software that allows farm operators to monitor multiple machines simultaneously, collectively driving the premiumisation and value growth of the global agricultural equipment market alongside underlying unit volume trends.

The combination of global population growth, changing dietary patterns favouring higher-protein and processed food consumption, and a finite or declining amount of arable land per capita is creating sustained pressure on farming operations to improve yield and land productivity, directly driving demand for advanced agricultural equipment capable of optimising input use and maximising output per cultivated hectare. Equipment innovations including variable-rate seeding and fertiliser application, precision spraying systems that reduce input waste while improving crop protection efficacy, and harvest automation technologies that minimise crop loss during collection are collectively positioned as essential tools for farming operations seeking to meet rising food demand within fixed or shrinking land resource constraints.

The growing availability of agricultural equipment rental, leasing, and custom hiring service models is expanding market access among smallholder and resource-constrained farming operations that cannot justify the capital expenditure of outright equipment ownership, particularly for high-value machinery including combine harvesters and large tractors used for limited periods during the agricultural season. Custom hiring centres and equipment-sharing platforms, increasingly supported by government policy in emerging agricultural markets, are enabling a broader base of farmers to access modern mechanised equipment, expanding the addressable market for equipment manufacturers and dealers beyond traditional ownership-based sales models.

Full-vehicle autonomous agricultural equipment is transitioning from pilot demonstrations to commercial-scale deployment in 2026, with major manufacturers confirming nationwide rollout plans for autonomous tractor fleets across multiple farming regions. Leading autonomy platforms now integrate advanced sensor fusion combining GPS, LiDAR, radar, and machine vision systems that enable equipment to identify and navigate around obstacles, operate safely in challenging conditions including rain, fog, dust, and low light, and execute complex field operations including tillage, spraying, and harvesting with minimal human supervision. The retrofittable nature of many autonomy upgrade kits designed for installation on existing tractor models from recent model years is additionally lowering the adoption barrier for farmers seeking to integrate autonomous capability into already-owned equipment rather than requiring entirely new machine purchases.

Battery-electric agricultural equipment is advancing beyond early prototype stages toward targeted commercial deployment, particularly in orchard, vineyard, and other specialised farming applications where the operational profile favours electric drivetrains over diesel power. Battery-electric autonomous tractor platforms unveiled in early 2026 are specifically engineered for a full day's operation in orchard and vineyard environments, combining electric propulsion with autonomous perception systems to extend automation into lower-emission farming operations. Alternative powertrain development extends beyond battery-electric systems, with hydrogen-powered engine technology also progressing toward commercial regulatory approval for agricultural and adjacent equipment applications, reflecting the industry's broader exploration of decarbonisation pathways alongside continued diesel engine efficiency improvements.

Artificial intelligence-powered precision spraying technology is delivering substantial input cost savings and environmental benefits by enabling targeted herbicide, fungicide, and fertiliser application based on real-time crop and weed detection rather than blanket field treatment. Advanced precision spraying systems can identify individual weeds versus crop plants using computer vision and apply herbicide only where needed, with leading systems demonstrating herbicide input savings of up to 80% relative to conventional blanket spraying approaches. This precision input application capability is extending to variable-rate fungicide and desiccant application for late-season crop protection, combine automation features for harvest settings, and integrated weed detection sensing that is becoming a standard expectation across premium sprayer and combine equipment tiers.

The agricultural equipment industry is addressing a long-standing technology fragmentation challenge through new interoperability frameworks that enable secure data exchange between proprietary equipment platforms from different manufacturers. New industry-wide interoperability networks, developed collaboratively by major equipment manufacturer associations, are enabling cloud-to-cloud exchange of machine data, work orders, and prescription maps across different brands' farm management software platforms, allowing farmers and custom operators to continue using their preferred software tools without compatibility constraints while maintaining data control and regulatory compliance. This interoperability advancement addresses a critical barrier to precision agriculture adoption, as farms increasingly operate mixed-brand equipment fleets that previously required separate, incompatible software ecosystems for each manufacturer's machines.

Expanding satellite connectivity integration is addressing one of precision agriculture's most persistent infrastructure challenges: reliable data transmission from farm fields in rural areas with limited or no cellular network coverage. New satellite connectivity modules, leveraging low-earth-orbit satellite networks, are being integrated into premium tractor and combine platforms to maintain continuous data connectivity during field operations regardless of terrestrial network availability, enabling real-time machine health monitoring, remote diagnostics, and operations centre data synchronisation even in the most remote farming locations. This connectivity expansion is a critical enabler for the broader autonomous and precision agriculture technology stack, as autonomous operation, fleet management, and AI-driven field optimisation all depend on consistent, reliable data transmission between field equipment and centralised farm management systems.

The global agricultural equipment market faces significant cyclical and structural challenges that constrain near-term growth velocity across specific equipment categories and regional markets. High financing costs and tightening agricultural credit conditions have compressed farmer purchasing power in several major markets, with elevated interest rates increasing the cost of equipment financing and prompting many farming operations to defer new equipment purchases in favour of repairing and extending the operational life of existing machinery. The capital intensity of modern precision and autonomous agricultural equipment creates an affordability barrier that is particularly acute for smallholder and resource-constrained farming operations, even as these technologies offer the greatest potential productivity benefits for operations facing the most severe labour and resource constraints. Equipment manufacturers are additionally navigating substantial research and development investment requirements to maintain technology leadership in autonomy, electrification, and precision agriculture, requiring sustained capital allocation toward innovation even during periods of cyclical sales softness across the broader equipment market.

Several structural dynamics restrain the pace of agricultural equipment market expansion in specific segments and geographies. The agricultural equipment industry remains structurally exposed to commodity price cycles and farm income volatility, as farmer equipment purchasing decisions are closely tied to crop and livestock commodity prices that determine farm profitability and available capital for capital expenditure in any given season. Fragmented landholding patterns across major emerging agricultural markets, particularly in South Asia and parts of Africa, constrain the economic viability of large-scale mechanised equipment on individual smallholder farms, limiting market penetration to equipment-sharing, rental, and custom hiring models rather than direct ownership-based sales in these geographies. The technical complexity of integrating autonomous and precision agriculture technology across mixed-brand equipment fleets has historically created interoperability challenges that complicate technology adoption for farms operating equipment from multiple manufacturers, though emerging industry-wide data standardisation initiatives are beginning to address this constraint.

The global agricultural equipment market presents substantial and well-documented commercial opportunities across technology innovation, geographic expansion, and business model dimensions that support sustained above-market growth through 2035. The accelerating commercial scale-up of autonomous agricultural equipment represents the single largest near-term value creation opportunity in the industry, as nationwide autonomous tractor deployment plans and expanding retrofit autonomy kit availability create substantial new revenue streams for equipment manufacturers beyond traditional machine sales, including software subscriptions, data services, and fleet management platforms. Emerging agricultural markets across Asia Pacific, Latin America, and Africa offer the largest untapped mechanisation opportunity, as government-supported mechanisation programmes and expanding equipment rental and custom hiring infrastructure progressively bring modern agricultural equipment within reach of smallholder farming populations that have historically relied on manual or animal-powered cultivation methods. The convergence of electrification, AI-driven precision input application, and satellite connectivity is creating a premium technology tier within the agricultural equipment market that commands substantially higher margins than conventional mechanical equipment, offering manufacturers a structural pathway to revenue and profitability growth even during periods of cyclical softness in core equipment unit sales. To access comprehensive opportunity sizing, equipment category-specific growth forecasts, regional mechanisation investment analysis, and strategic market entry frameworks across all major geographies, explore Expert Market Research's complete Agricultural Equipment Market report.

Agricultural equipment refers to tools and machinery deployed in agricultural practices to aid in farming. This equipment can be motor-based, like tractors or tools for purposes like ploughing and sowing.

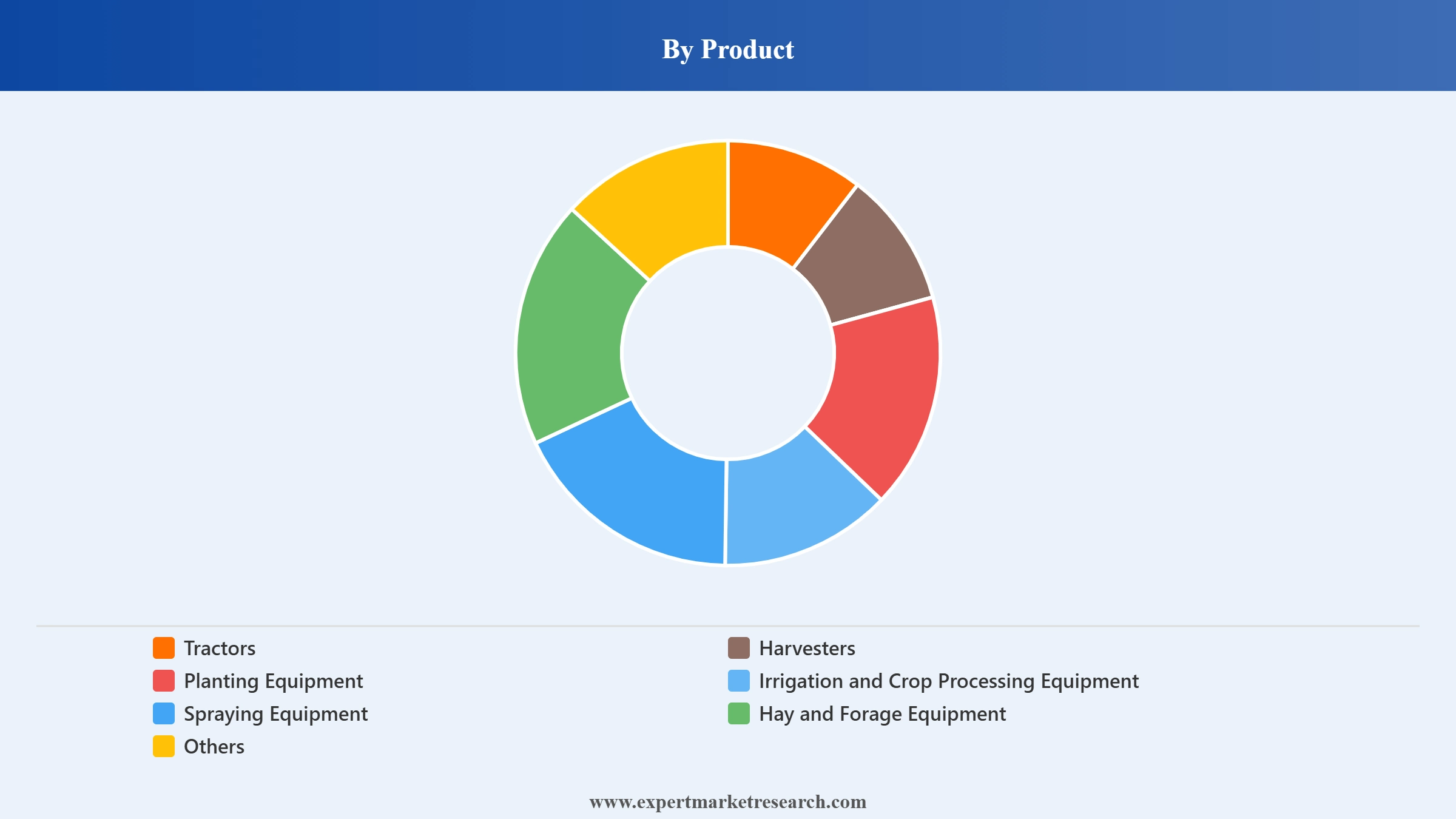

Market Breakup by Product

Key Insighs: Tractors represent the largest product segment by revenue and unit volume, serving as the foundational power source for most mechanised farm operations across all farm sizes. Harvesters constitute a high-value segment given the substantial capital cost and crop-specific engineering of modern harvest machinery, with automated harvest settings driving premiumisation. Planting equipment, including seed drills and precision planters, is benefiting from variable-rate seeding technology that optimises plant population based on real-time field data. Irrigation and crop processing equipment is seeing rising demand as water-use efficiency becomes a growing agricultural priority. Spraying equipment is undergoing rapid transformation through AI-driven precision systems that significantly reduce herbicide and pesticide costs. Hay and forage equipment serves the livestock feed production segment, while Others includes specialised tillage implements, ploughs, and rotavators used in land preparation.

Market Breakup by Application

Key Insights: Harvesting and threshing is one of the largest application segments by value, given the time-critical nature of harvest operations and the yield loss risk tied to equipment downtime. Land development and seed bed preparation remains a foundational, high-volume application across virtually all cultivated farmland. Sowing and planting applications are benefiting from precision agriculture integration that improves seed placement, germination rates, and crop uniformity. Weed cultivation is the fastest-growing application by technology investment, driven by AI-powered precision spraying and mechanical weeding systems. Plant protection covers the broader range of pest and disease management equipment that safeguards yield through the growing season. Post-harvest and agro-processing equipment supports the handling and drying operations that follow harvest, helping preserve crop quality and reduce losses.

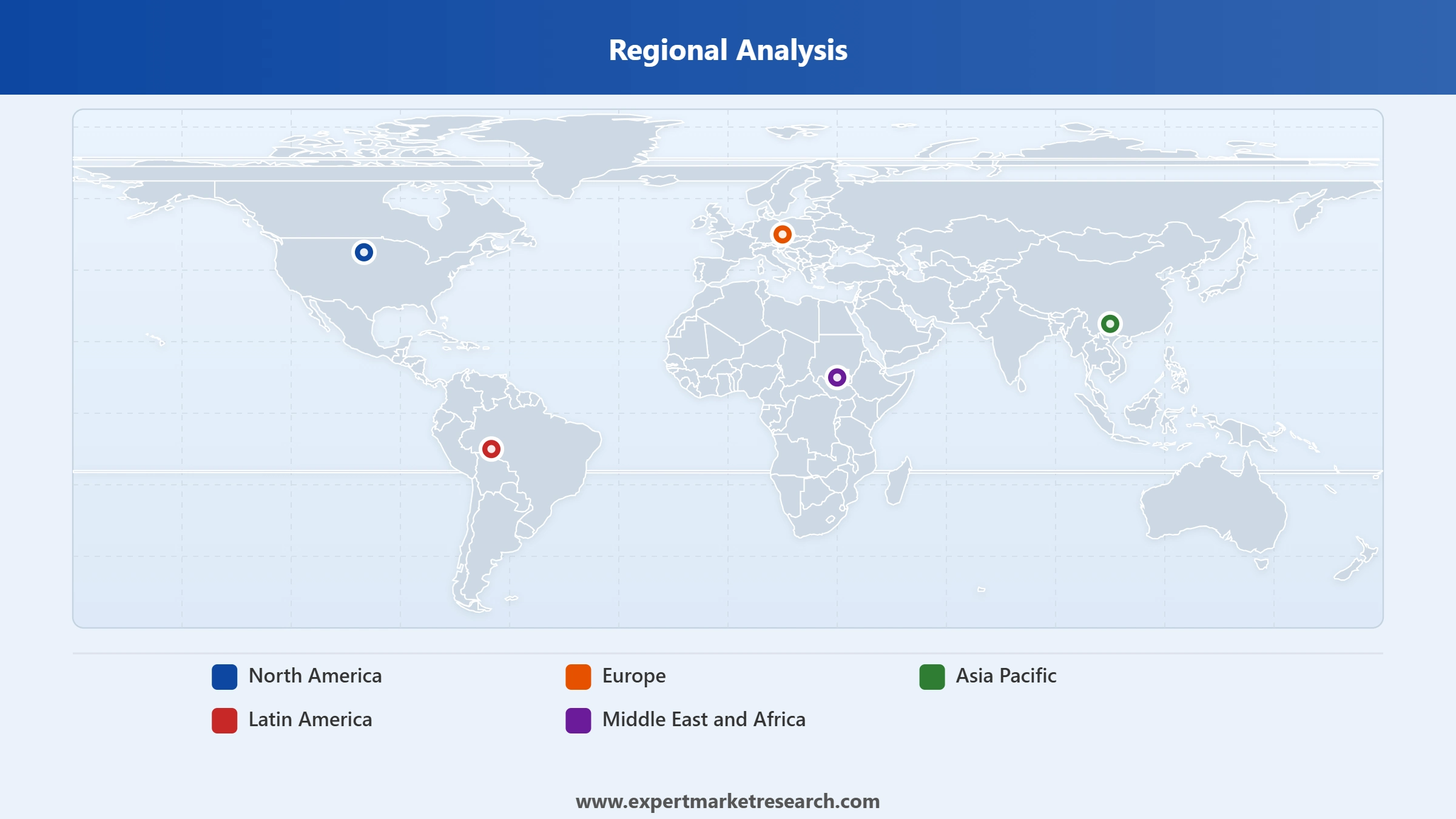

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the largest regional agricultural equipment market, anchored by China and India's massive farming populations and substantial government-supported mechanisation programmes aimed at improving agricultural productivity and rural incomes. China's agricultural equipment market benefits from sustained government subsidy programmes for farm machinery purchases and a manufacturing base capable of serving both domestic mechanisation demand and growing export markets. India's agricultural equipment sector is characterised by strong demand for tractors and power tillers suited to the country's predominantly smallholder farming structure, with growing adoption of custom hiring centres and equipment rental models expanding mechanisation access among resource-constrained farmers. Japan and South Korea represent technologically advanced but mature agricultural equipment markets, with strong adoption of precision agriculture and automation technology reflecting both farm labour scarcity and high farmer technology adoption rates. Southeast Asian markets, including Indonesia, Vietnam, and Thailand, are experiencing accelerating mechanisation as rural labour migration to urban centres increases the economic case for farm equipment investment.

North America's agricultural equipment market is characterised by high mechanisation levels, large average farm sizes that support substantial equipment capital investment, and global leadership in precision agriculture and autonomous equipment technology development. The United States hosts the world's leading agricultural equipment manufacturers and represents the most advanced commercial deployment market for autonomous tractor technology, with confirmed nationwide rollout plans spanning multiple states. The 2026 Commodity Classic showcase of new high-horsepower tractor platforms with autonomy-ready factory configuration and satellite connectivity reflects the region's position at the technology frontier of agricultural equipment innovation. Canada's agricultural equipment market, serving the country's substantial grain and oilseed farming sector, closely parallels US market dynamics given the integrated nature of North American agricultural equipment supply chains and similar farm size and mechanisation profiles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe's agricultural equipment market is shaped by the region's diverse farming structures, ranging from large-scale mechanised operations in France and Germany to smaller family farms across Southern and Eastern Europe, alongside increasingly stringent environmental and emissions regulations that are accelerating equipment electrification and alternative fuel adoption. Germany and France are the primary European agricultural equipment manufacturing and consumption markets, hosting major equipment manufacturers and trade events that showcase the industry's latest autonomy, electrification, and precision agriculture innovations. The region's agricultural labour shortage, comparable to North America's, is driving strong demand for autonomous and semi-autonomous equipment, while European Union sustainability and emissions regulations are creating regulatory tailwinds for electric and hydrogen-powered equipment development.

Latin America's agricultural equipment market is anchored by Brazil and Argentina, two of the world's largest grain and oilseed producing nations with substantial mechanised farming operations serving major export markets. Brazil's large-scale commercial agriculture sector, particularly in soybean and corn production, drives strong demand for high-horsepower tractors, combine harvesters, and precision agriculture technology comparable to North American equipment specifications. Argentina's agricultural equipment market similarly serves a substantial commercial grain farming sector, with both countries representing significant export markets for global equipment manufacturers. Mexico's agricultural equipment demand spans both commercial export-oriented agriculture and smaller-scale domestic food production, creating a diverse equipment demand profile across the country's varied farming regions.

The Middle East and Africa region represents an agricultural equipment market characterised by sharply contrasting sub-regional dynamics. Gulf Cooperation Council states, including Saudi Arabia, are investing in agricultural equipment as part of broader food security and agricultural self-sufficiency programmes, despite the region's challenging arid farming conditions that require specialised irrigation and water-efficient equipment. Sub-Saharan Africa represents the region's largest long-term mechanisation opportunity, with the majority of farming operations still reliant on manual or animal-powered cultivation methods, creating substantial latent demand for basic mechanisation as government programmes, development finance institutions, and equipment rental models progressively expand access to tractors and essential farm machinery across the continent's smallholder-dominated agricultural sector.

The report presents a detailed analysis of the following key players in the global agricultural equipment market, looking into their capacity, market share, and latest developments like capacity expansions, plant turnabouts and mergers and acquisitions.

Deere & Company, headquartered in Moline, Illinois, United States, is a leading manufacturer of agricultural, construction, and forestry machinery. Founded in 1837, the company's popular brands include John Deere tractors, combines, and precision agriculture technology, among others. Its products are distributed globally through an extensive network of authorised dealers and direct OEM channels.

CNH Industrial N.V., headquartered in Basildon, United Kingdom, is a leading manufacturer of agricultural and construction equipment. Founded in 1842, the company's portfolio includes Case IH, New Holland, and STEYR agricultural brands, among others. Its products are distributed across North America, Europe, the Middle East, Africa, South America, and Asia Pacific through dealer networks and financial services support.

AGCO Corporation, headquartered in Duluth, Georgia, United States, is a leading manufacturer of agricultural machinery and precision agriculture technology. Founded in 1990, the company's popular brands include Fendt, Massey Ferguson, Valtra, and PTx, among others. Its products are distributed globally through a network of farmer-focused dealers and retrofit technology partners.

Mahindra & Mahindra Ltd., headquartered in Mumbai, India, is the world's largest tractor manufacturer by volume. Founded in 1945, the company's popular brands include Mahindra, Swaraj, and OJA tractors, among others. Its products are distributed across India and over 50 global markets through an extensive dealer network.

Others include Kubota Corporation and ISEKI & CO., LTD., among other established manufacturers contributing to the global agricultural equipment market's technological and commercial development.

The comprehensive EMR report provides an in-depth assessment of the market based on the Porter's Five Forces Model along with a detailed SWOT analysis, offering valuable insights into the micro and macro factors shaping the industry's competitive landscape and long-term growth trajectory.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global agricultural equipment market attained a value of nearly USD 231.77 Billion in 2025.

The market is projected to grow at a CAGR of 8.90% in the forecast period of 2026-2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach about USD 543.67 Billion by 2035.

The market is being driven by mechanisation of agricultural tools to boost productivity and reduce human labour, and incentives and subsidies by various governments for farmers to adopt advanced agricultural equipment.

The key trends of the market for include the integration of digital technologies like the Internet of Things (IoT) and artificial intelligence (AI) in precision farming and increased focus on farm mechanisation.

The major regional markets for agricultural equipment are North America, Latin America, the Asia Pacific, Europe, and the Middle East and Africa.

The different products of agricultural equipment are tractors, harvesters, planting equipment, irrigation and crop processing equipment, spraying equipment, and hay and forage equipment, among others.

The major applications of agricultural equipment include land development and seed bed preparation, sowing and planting, weed cultivation, plant protection, harvesting and threshing, and post-harvest and agro processing.

The key players in the global agricultural equipment market are Deere & Company, CNH Industrial N.V., AGCO Corporation, Mahindra & Mahindra Ltd., Kubota Corporation, and ISEKI & CO., LTD., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.