Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

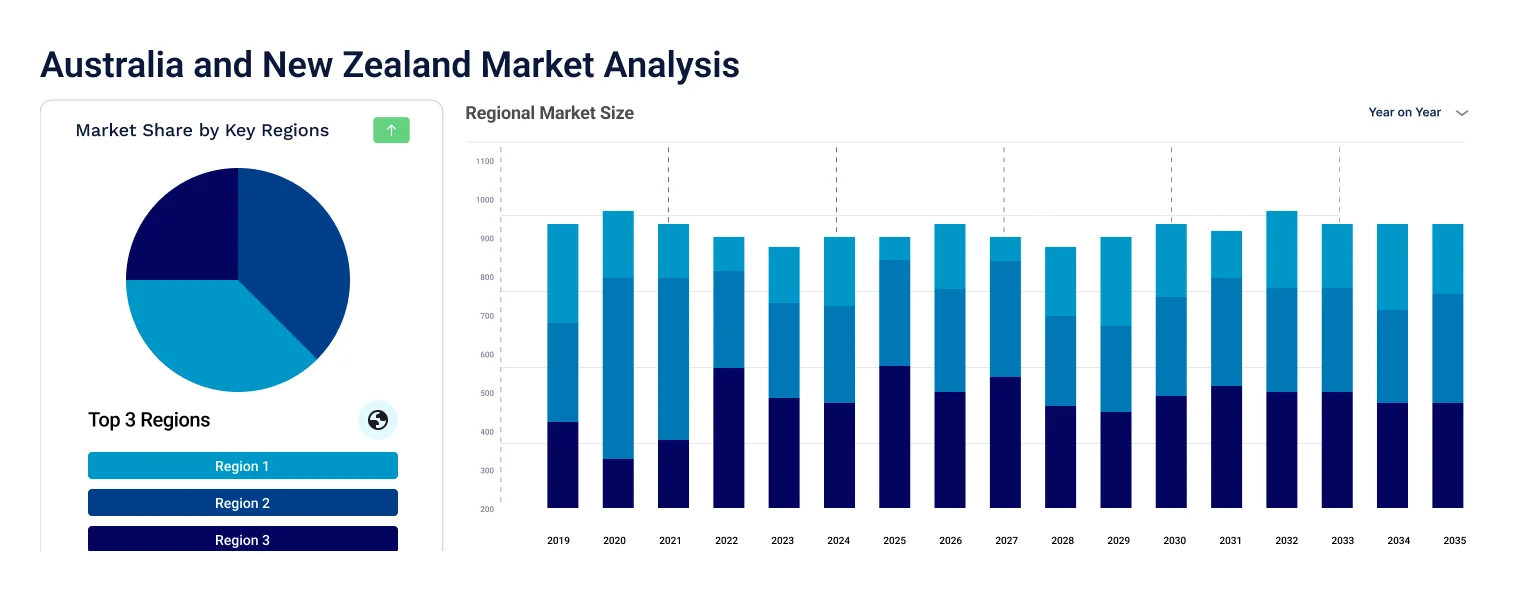

The Australia and New Zealand diagnostic imaging services market was valued at USD 1041.08 Million in 2025 and is expected to grow at a CAGR of 6.20%, reaching USD 1899.89 Million by 2035. The market is experiencing growth due to rising demand for non-invasive imaging procedures and technological advancements in imaging equipment.

Compound Annual Growth Rate

6.2%

Value in USD Million

2026-2035

Read more about this report - Request a Free Sample

The growth of the market is being driven by the growing ageing population and increased prevalence of chronic diseases. This has led to an increase in healthcare expenditure and has significantly contributed to expanding diagnostic imaging services in the region. The growth of the Australia and New Zealand diagnostic imaging services market value is also driven by the growing burden of chronic diseases, like cardiovascular diseases and cancer, along with increased healthcare investments and technological advancements.

Continuous technological advancements in imaging technologies, coupled with a growing awareness among the population about the importance of early diagnosis, has further fueled the demand for diagnostic imaging services in Australia and New Zealand. In April 2021, Koninklijke Philips N.V. installed its most advanced digital diagnostic and interventional neurovascular imaging solutions at Westmead Hospital Australia, leading to the expansion of the diagnostic imaging services in the region.

Government initiatives aimed at improving healthcare infrastructure, reducing waiting times, and enhancing accessibility to healthcare services, have also been contributing to the rising Australia and New Zealand diagnostic imaging services market] share . Additionally, strategic collaborations among diagnostic imaging service providers, healthcare facilities, and technology companies, along with adopting telemedicine and teleradiology services, have positively impacted the market dynamics.

The regulatory support for maintaining high standards in diagnostic imaging services also ensures the reliability of diagnostic results, further fostering market growth. According to the Australian Institute of Health and Welfare, in Australia and New Zealand, chronic diseases together caused 85% of the total burden of disease, which is a similar figure to chronic diseases accounting for 90% of the burden due to deaths alone.

The Australia and New Zealand diagnostic imaging services market growth is being driven by advancements in medical technology and increasing healthcare awareness. This dynamic market is witnessing a rising demand for cutting-edge ultrasound devices, including portable and 3D/4D imaging systems. The regions’ healthcare infrastructure development, coupled with a growing elderly population, also contributes to the expanding market. Additionally, the emphasis on early disease detection and prenatal care fuels the adoption of ultrasound technology.

Increasing Disease Burden to Drive the Growth

The growing incidence of diseases, such as cancer and cardiovascular disorders, is aiding the rising demand for diagnostic imaging services, as early detection and accurate diagnosis are crucial for effective treatment. According to the Australian Prevention Partnership Centre statistics, in Australia, chronic diseases cause 9 out of every 10 preventable deaths 2 and account for 85% of years lost due to ill health or early death. This has facilitated the research and developmental activities and henceforth in the discovery of novel diagnostic imaging services in the market.

Rising Initiatives by the State Governments to Aid the Market

The state governments have formulated initiatives to improve healthcare infrastructure, enhance diagnostic capabilities, and ensure better accessibility to healthcare services playing a pivotal role in the Australia and New Zealand diagnostic imaging services market growth. Government investments in healthcare infrastructure projects and policies aimed at reducing waiting times for diagnostic procedures are notable in both countries. In May 2023, the Australian Government provided USD 8.3 million to improve training opportunities for specialist doctors in regional Australia through round two of the Flexible Approach to Training in Expanded Settings (FATES) program.

Rapid Technological Advancements to Benefit the Market

Continuous innovations in diagnostic imaging technologies, including MRI, CT, and ultrasound, are accelerating the market growth, as healthcare providers invest in advanced equipment to enhance diagnostic capabilities. The adoption of 3D mammography and the integration of artificial intelligence (AI) in diagnostic imaging is anticipated to boost the Australia and New Zealand diagnostic imaging services market size in the forthcoming years.

In June 2023, the Hospital for Special Surgery (HSS), the world's leading academic medical centre specialized in musculoskeletal health, and New Zealand-based medical device and technology company MARS Bioimaging Limited (MARS) collaborated for the MARS’s photon-counting spectral CT imaging technology. Through the HSS Innovation Institute, HSS and MARS will advance musculoskeletal imaging and diagnosis, including evaluation of specific aspects of the MARS 5x120 Extremity Scanner and potential co-development of new scanning technologies and systems.

Read more about this report - Request a Free Sample

Australia and New Zealand Diagnostic Imaging Services Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Modality

Market Breakup by Application

Market Breakup by End User

Market Breakup by Country

Read more about this report - Request a Free Sample

The diagnostic imaging market in Australia and New Zealand exhibits a moderate level of competitiveness, with prominent players. Key market leaders include Mindray Medical International Limited, Siemens Healthineers AG, GE Healthcare, Fujifilm Holdings Corporation, and Koninklijke Philips NV, among others.

In December 2023, Lunit, a leading provider of AI-powered solutions for cancer diagnostics and therapeutics, proposed an acquisition offer to Volpara Health Technologies Ltd., a global leader in AI-enabled software for the early detection and prevention of cancer. This strategic move comes as a result of an exhaustive evaluation of potential avenues for growth and innovation by Lunit.

The key features of the Australia and New Zealand diagnostic imaging services market report include patent analysis, grants analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players.

The major companies in the market are as follows:

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is anticipated to grow at a CAGR of 6.20% during the forecast period of 2026-2035.

The market demand is driven by the increasing burden of chronic diseases such as cardiovascular diseases and cancer, coupled with the rising healthcare investment in the country and technological advancements.

The current market trend involves rising support from the government in the form of initiatives and investments in ultrasound devices.

It is commonly divided into MRI, computed tomography, ultrasound, X-ray, nuclear imaging, fluoroscopy, mammography, and other modalities.

Major applications are cardiology, oncology, neurology, orthopedics, gastroenterology, and gynaecology, among other applications.

Major end users include hospitals and diagnostic centres, among others.

The key players in the market include Siemens Healthineers, GE Healthcare, Philips Healthcare, Fujifilm Holdings Corporation, Hologic, Inc., Hitachi Medical Corporation, Shimadzu Corporation, Carestream Health, Inc., Canon Medical Systems Corporation, Toshiba Medical Systems Corporation, Agfa-Gevaert Group, Samsung Medison Co., Ltd., Aurora Imaging Technology, Inc., Esaote S.p.A., and Mindray Medical International Limited.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Modality |

|

| Breakup by Application |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.