Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

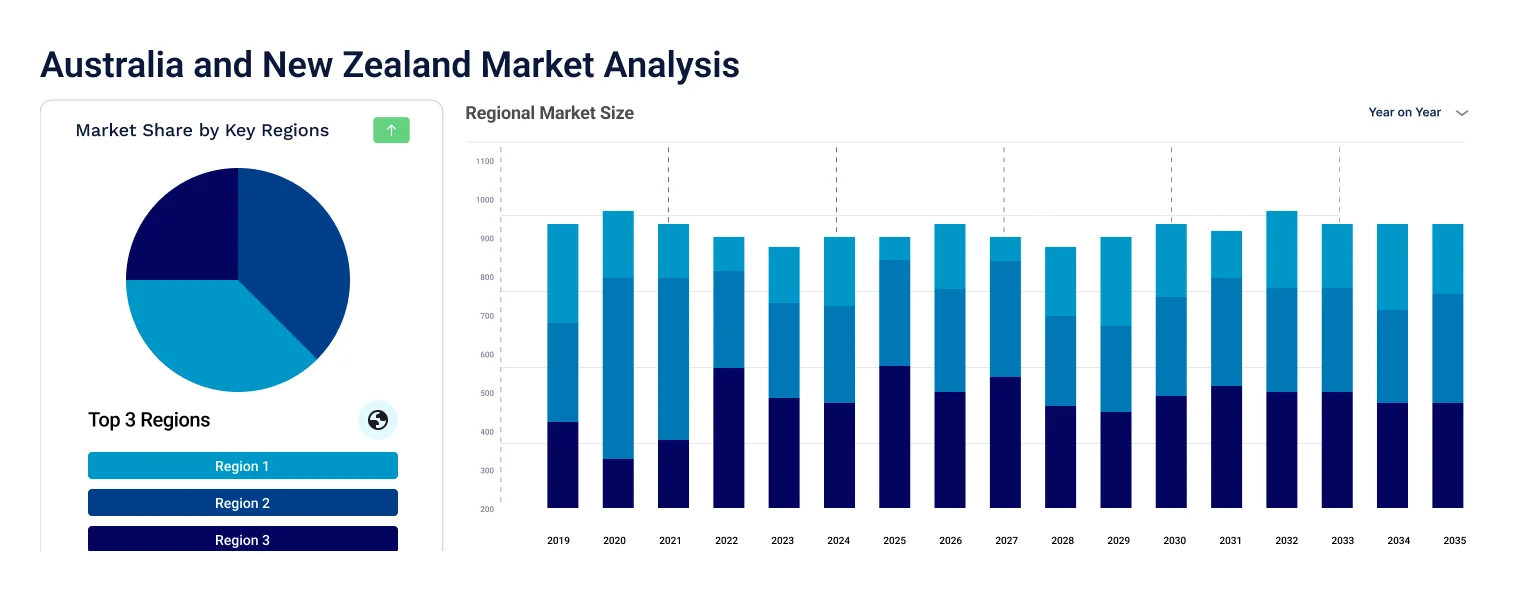

The Australia and New Zealand ultrasound devices market was valued at USD 380.47 Million in 2025 and is expected to grow at a CAGR of 6.07%, reaching USD 685.88 Million by 2035. Market growth is supported by increasing use in diagnostic imaging and prenatal care.

Compound Annual Growth Rate

6.07%

Value in USD Million

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The growth of the market is being driven by the advancements in medical technology and increasing healthcare awareness. This dynamic market is witnessing a rising demand for cutting-edge ultrasound devices, including portable and 3D/4D imaging systems. The regions’ healthcare infrastructure development, coupled with a growing elderly population, contributes to the expanding market. Additionally, the emphasis on early disease detection and prenatal care fuels the adoption of ultrasound technology. The Australia and New Zealand ultrasound devices market growth is also driven by the growing burden of chronic diseases, like cardiovascular diseases and cancer, along with increased healthcare investments and technological advancements.

According to According to the cancer data in Australia, there were approximately 3,830 new cases of thyroid cancer diagnosed in Australia, with 1,070 cases in males and 2,760 in females. The report also indicates that the likelihood of being diagnosed with thyroid cancer by the age of 85 is projected to be 1 in 83 (1.2%), with specific probabilities for males (1 in 145 or 0.69%) and females (1 in 58 or 1.7%). Ultrasound, being a convenient and widely available imaging modality that does not involve ionizing radiation, is considered ideal for detecting and evaluating thyroid nodules. Consequently, the increasing incidence of thyroid cancer in the country is expected to drive the Australia and New Zealand ultrasound devices market demand.

Increasing Funding by the Government Strengthens Imaging Services

The Australian Government's augmented financial support for enhancing imaging services is anticipated to fuel the market expansion. The government allocated additional funds for the expansion of the Heart of Australia Program in April 2022, amounting to approximately USD 12.0 million. This program extends mobile medical clinic services throughout northern Queensland, offering heart monitoring and various healthcare services. The government's commitment to cardiovascular care delivery is expected to boost the demand for ultrasound equipment, contributing to the Australia and New Zealand ultrasound devices market share.

Increasing Usage of High-intensity Focused Ultrasound Source

High-intensity focused ultrasound is increasingly employed in the treatment of both primary and metastatic tumors due to its precise tumor identification capabilities during ablation. In cases where patients exhibit substantial medical co-morbidities, rendering them high-risk candidates for surgery, or possess lower liver function restricting hepatectomy, high-intensity focused ultrasound emerges as a viable therapeutic option for addressing liver tumors. High-intensity focused ultrasound emerges as a promising and safe alternative for the minimally invasive treatment of localized prostate cancer.

Notably, recent research published by the Mayo Foundation in August underscores the growing interest in mitigating treatment-related side effects associated with prostate cancer by targeting a specific portion of the affected prostate. Focal therapy, utilizing high-intensity focused ultrasound (HIFU), proves effective in addressing this concern. HIFU precisely targets the most aggressive tumor, sparing the surrounding prostate structures. This approach is widely accepted in treating various cancers, including kidney cancers, where only the tumor is removed or ablated, leaving the rest of the organ intact. Consequently, the increased demand for HIFU systems may drive their adoption in Australian healthcare for minimally invasive prostate cancer treatment.

Australia and New Zealand Ultrasound Devices Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Market Breakup by Technology

Market Breakup by Applications

Market Breakup by Portability

Market Breakup by End User

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The ultrasound devices market in Australia and New Zealand exhibits a moderate level of competitiveness, with prominent players. Key market leaders include Mindray Medical International Limited, Siemens Healthineers AG, GE Healthcare, Fujifilm Holdings Corporation, and Koninklijke Philips NV, among others.

In November 2022, Caption Health disclosed the receipt of regulatory approvals from Health Canada's Medical Devices Directorate and Australia's Therapeutic Goods Administration to market its Caption AI technology platform. This innovative platform enables healthcare professionals in Australia and Canada, regardless of prior sonography experience, to conduct cardiac ultrasounds.

The key features of the Australia and New Zealand ultrasound devices market report includes patent analysis, grants analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players.

The major companies in the market are as follows:

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is anticipated to grow at a CAGR of 6.07% during the forecast period of 2026-2035.

The market demand is driven by the increasing burden of chronic diseases such as cardiovascular diseases and cancer, coupled with the rising healthcare investment in the country and technological advancements.

The current market trend involves the rising support from the government in the form of initiatives and investments in ultrasound devices.

It is commonly divided into stationary ultrasound and portable ultrasound.

Treatment types include advanced 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasoundand.

Major applications are anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, primary care, critical care, and emergency medicine.

The segments can be divided into handheld, compact, and cart/trolley.

Major end users include hospitals, imaging centres, and research centres.

The key players in the market include Canon Medical Systems Corporation, SonoScape Medical Corp, Fujifilm Holdings Corporation, GE Healthcare, Hologic Inc., Koninklijke Philips NV, Mindray Medical International Limited, Samsung Electronics Co. Ltd., Esaote SPA, Siemens Healthineers AG, ALPINION MEDICAL SYSTEMS Co., Ltd., CHISON Medical Technologies Co., Ltd., SAMSUNG HEALTHCARE, Analogic Corporation, and General Electric.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Technology |

|

| Breakup by Applications |

|

| Breakup by Portability |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.