Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

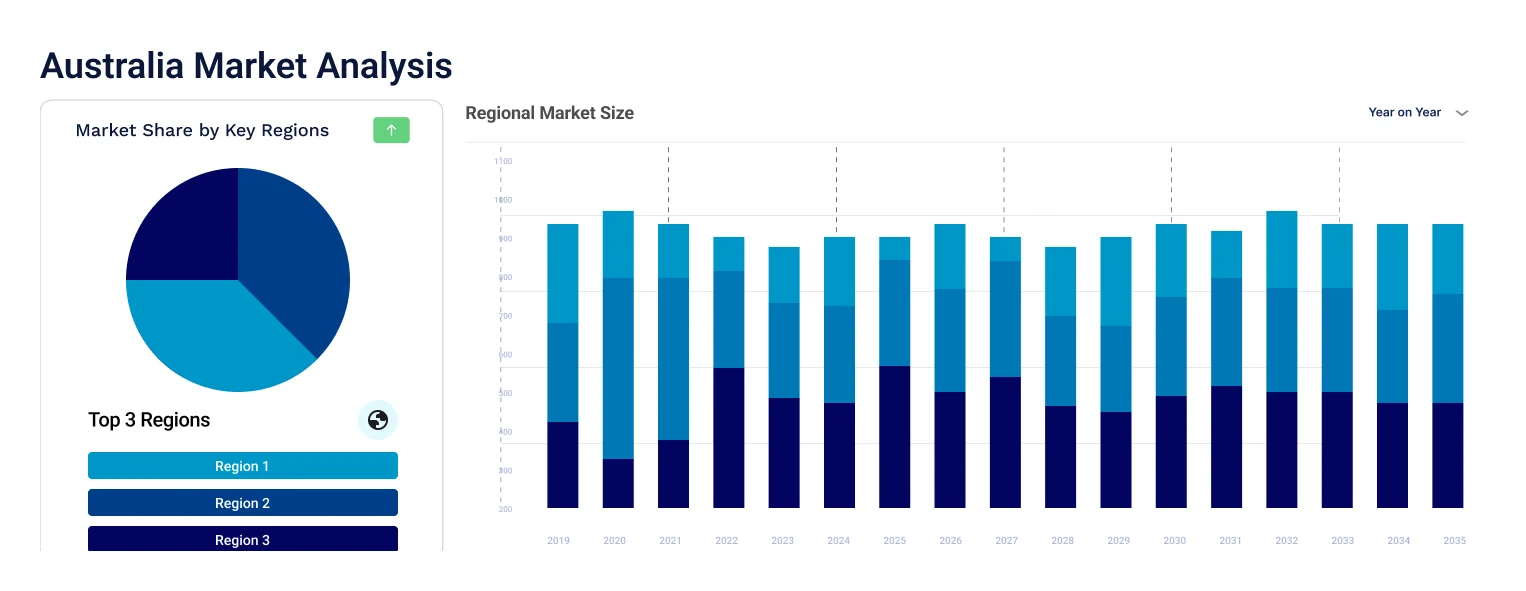

The Australia craft beer market size reached USD 1223.18 Million in 2025. The market is expected to grow at a CAGR of 17.50% between 2026 and 2035, reaching almost USD 6135.77 Million by 2035.

Compound Annual Growth Rate

17.5%

Value in USD Million

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Beer holds a significant place in Australian culture, from social gatherings to sporting events. While mainstream brands like Coopers, XXXX, and VB dominate consumption, there's a growing interest in craft beer, driven by a desire for unique flavours. However, there's a shift towards mid-strength and low-strength beers due to increased moderation and rising prices.

The craft beer market in Australia has experienced substantial growth, now representing around 5% of total beer sales, with approximately 350 brewers and microbreweries in Australia. Major beverage companies like Lion and SABMiller have capitalised on this trend by acquiring independent labels, such as Matilda Bay and Little Creatures.

Technological advancements, increasing consumer awareness, and government support for sustainability initiatives have fuelled the market's expansion, particularly in sectors like construction and automotive. As demand grows and environmental concerns persist, the future looks promising for the Australian craft beer market. With continuous innovations, regulatory support, and a focus on environmental sustainability, the industry is poised for sustained growth in the years ahead. The Australia craft beer market development has witnessed resilience and promise, with microbreweries carving out a niche in an otherwise dominated market.

Australia Craft Beer Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Market Breakup by Distribution Channel

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Key players in the craft beer in Australia brew, process and distribute products aiding the end-users for increased consumption.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The craft beer market reached a value of USD 1223.18 Million in 2025.

The market is projected to grow at a CAGR of 17.50% between 2026 and 2035

The revenue generated from the craft beer market is expected to reach USD 6135.77 Million in 2035.

The various types of craft beer include sour beer, ales beer, wheat beer, pilsners and pale lagers, and others.

The key market players Asahi Holdings (Australia) Pty Ltd., Emencee Pty Ltd. trading as Balter Brewing Company, Akasha Brewing Company Pty Ltd., BentSpoke Brewing Co., Boatrocker Brewers & Distillers, Bridge Road Brewers, Mountain Culture Beer Co., Fixation Brewing Co., Mountain Goat Beer, Lion Group (Lion Pty Ltd.), Wildflower Brewing & Blending, Bracket Brewing Company Pty Ltd., and others.

The market is driven by factors that include technological advancements, increasing consumer awareness, and government support for sustainability initiatives, among others.

The market is categorised according to its distribution channel, which includes on-trade and off-trade.

In 2022, the largest demographic of Australian craft beer enthusiasts fell between the ages of 30 and 39, comprising approximately 31% of the total. In contrast, younger consumers aged 18 to 29 made up only 13% of craft beer drinkers.

New South Wales and Victoria lead the craft beer scene in Australia, hosting the largest consumer bases and the highest number of breweries and retail outlets. The majority of craft beer enthusiasts fall within the 30 to 39 age group, with males comprising a notably larger proportion.

The Sail and Anchor Pub Brewery, established in 1984 in Western Australia, is widely recognized as Australia's pioneering craft brewery. Its success served as a catalyst, inspiring numerous other breweries to enter the craft beer market.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.