Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

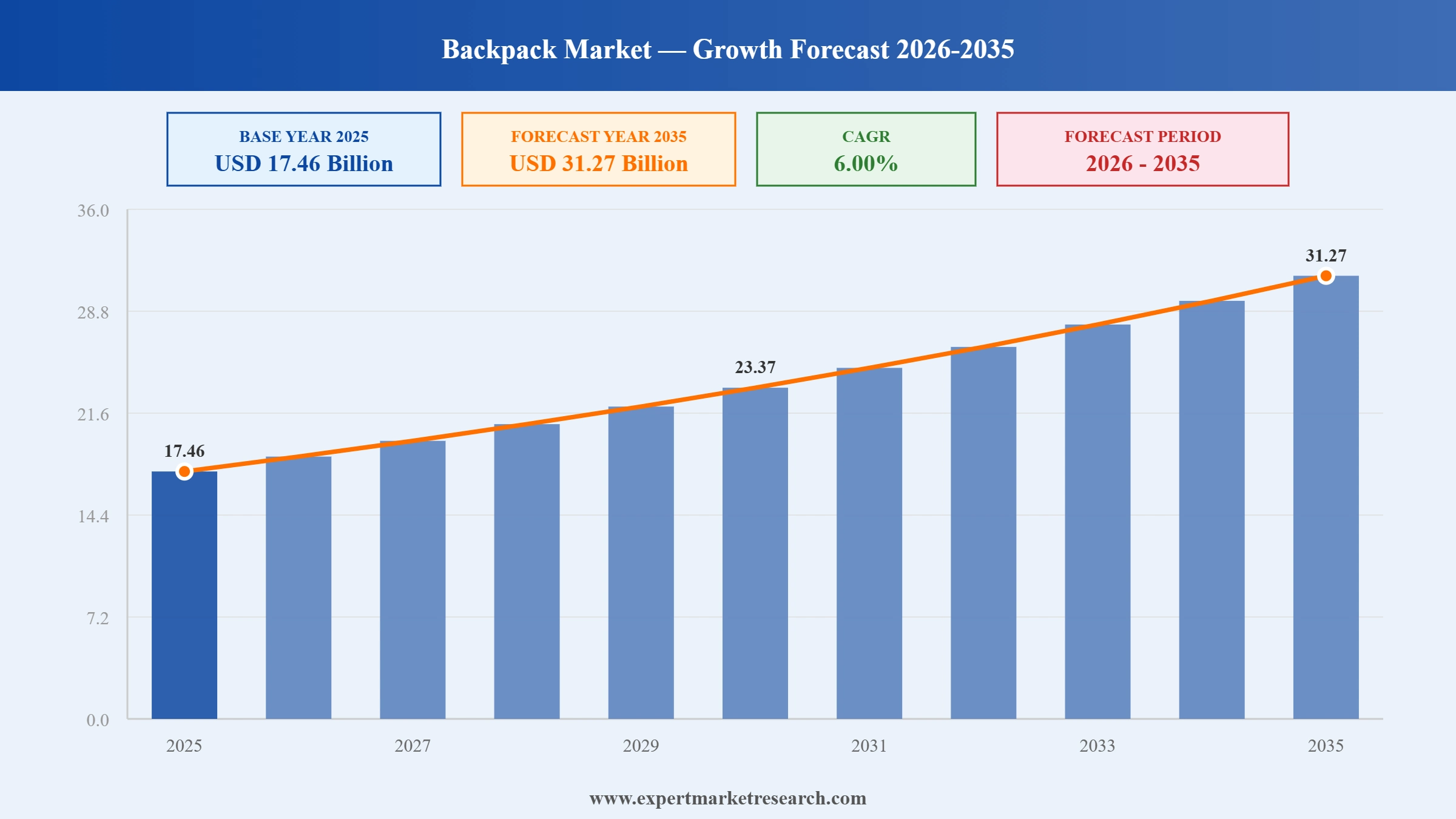

The global backpack market reached a value of USD 17.46 Billion at 2025 and is projected to expand at a CAGR of around 6.00% during the forecast period of 2026-2035. With a rising culture of travel and adventure tourism, growing demand for ergonomic and tech-integrated designs, rapid expansion of e-commerce retail channels, and increasing urbanisation driving commuter backpack adoption, the market is expected to reach USD 31.27 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Backpack Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 17.46 |

| Market Size 2035 | USD Billion | 31.27 |

| CAGR 2019-2025 | USD Billion | XX% |

| CAGR 2026-2035 | USD Billion | 6.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 7.8% |

| CAGR 2026-2035 - Market by Country | India | 8.9% |

| CAGR 2026-2035 - Market by Country | Canada | 7.2% |

| CAGR 2026-2035 - Market by Distribution Channel | Online Channel | 6.7% |

| CAGR 2026-2035 - Market by End User | Women | 6.7% |

| Market Share by Country 2025 | China | 16.9% |

The global backpack market is advancing beyond its traditional school-and-travel roots into a broader lifestyle and performance category. Sustainability mandates, smart tech integration, and the digital nomad movement are reshaping product development, while online platforms and direct-to-consumer launches are accelerating trial and repeat purchase. Major brands and specialists alike compete on ergonomics, materials innovation, and channel agility to capture a widening consumer base.

In February 2026, Nike relaunched its All Conditions Gear line, opening a flagship store in Beijing while showcasing Team USA kits during the Olympics. The relaunch merged technical outdoor performance with lifestyle fashion, bridging the trail-to-street gap and positioning ACG packs at the intersection of urban commuting and outdoor performance, expanding the addressable premium backpack segment within the global backpack market.

In February 2025, JanSport announced a strategic partnership with L2 Brands to extend its collegiate presence across American universities. The collaboration widened JanSport's branded apparel and accessories range for students, deepening shelf presence in campus retail and reinforcing the brand's status as the go-to option for the student segment of the global backpack market.

In November 2024, Nike introduced the Elite EasyOn backpack, originally engineered for the Paris 2024 Paralympic Games. The design features a full clamshell opening, oversized U-shaped zippers, and modular straps to assist athletes with reduced dexterity, demonstrating how inclusivity-led product innovation is opening new user segments within the global backpack market.

In January 2024, Yeti acquired Mystery Ranch, a specialist producer of high-performance backpacks and gear used by military personnel, wildland firefighters, and backcountry athletes. The acquisition gave Yeti a credible route into load-bearing technical packs and expanded its outdoor lifestyle ecosystem, accelerating consolidation within the premium tier of the global backpack market.

Consumer and regulatory pressure is making eco-friendly materials a baseline expectation rather than a premium differentiator. Deuter plans to incorporate recycled polyester into 90% of its 2025 lineup, and brands such as EVERKI have reported over 40% year-on-year growth in recycled backpack sales. A 2024 Deloitte survey found that 64% of Gen Z consumers are willing to pay a premium for sustainable products, sustaining innovation investment across the global backpack market.

USB charging ports, RFID-blocking pockets, solar panels, and GPS-enabled anti-theft designs are shifting backpacks from passive carry solutions to active utility devices. This appeals to digital nomads, frequent flyers, and tech professionals who demand device-ready carry, broadening the addressable market beyond traditional students and hikers and supporting sustained value-per-unit growth within the global backpack market.

E-commerce platforms and direct-to-consumer launches are compressing the gap between product release and consumer purchase. Peak Design's online-first product launches and Cotopaxi's limited-edition drop model generate social proof and urgency that physical retail struggles to replicate. Online is the fastest-growing distribution channel, supported by virtual fitting tools, influencer marketing, and subscription replenishment features in the global backpack market.

The proliferation of remote and hybrid work has normalised the digital nomad lifestyle, generating consistent demand for laptop-protective, carry-on-compliant, and multi-day travel backpacks. Brands are responding with work-to-weekend hybrid packs that serve the same consumer across commuting, co-working, and weekend travel occasions, effectively doubling usage frequency per unit in the global backpack market.

The Outdoor Industry Association recorded a 4.1% rise in US outdoor participation to an all-time high of 175.8 million participants in 2024. This underpins structural demand for 31-50 litre technical packs suited to day hikes, backpacking trips, and multi-sport use. Premium brands including Osprey, Deuter, and Patagonia are capturing this cohort through performance claims, lifetime warranties, and sustainability credentials within the global backpack market.

The report by Expert Market Research, titled "Global Backpack Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

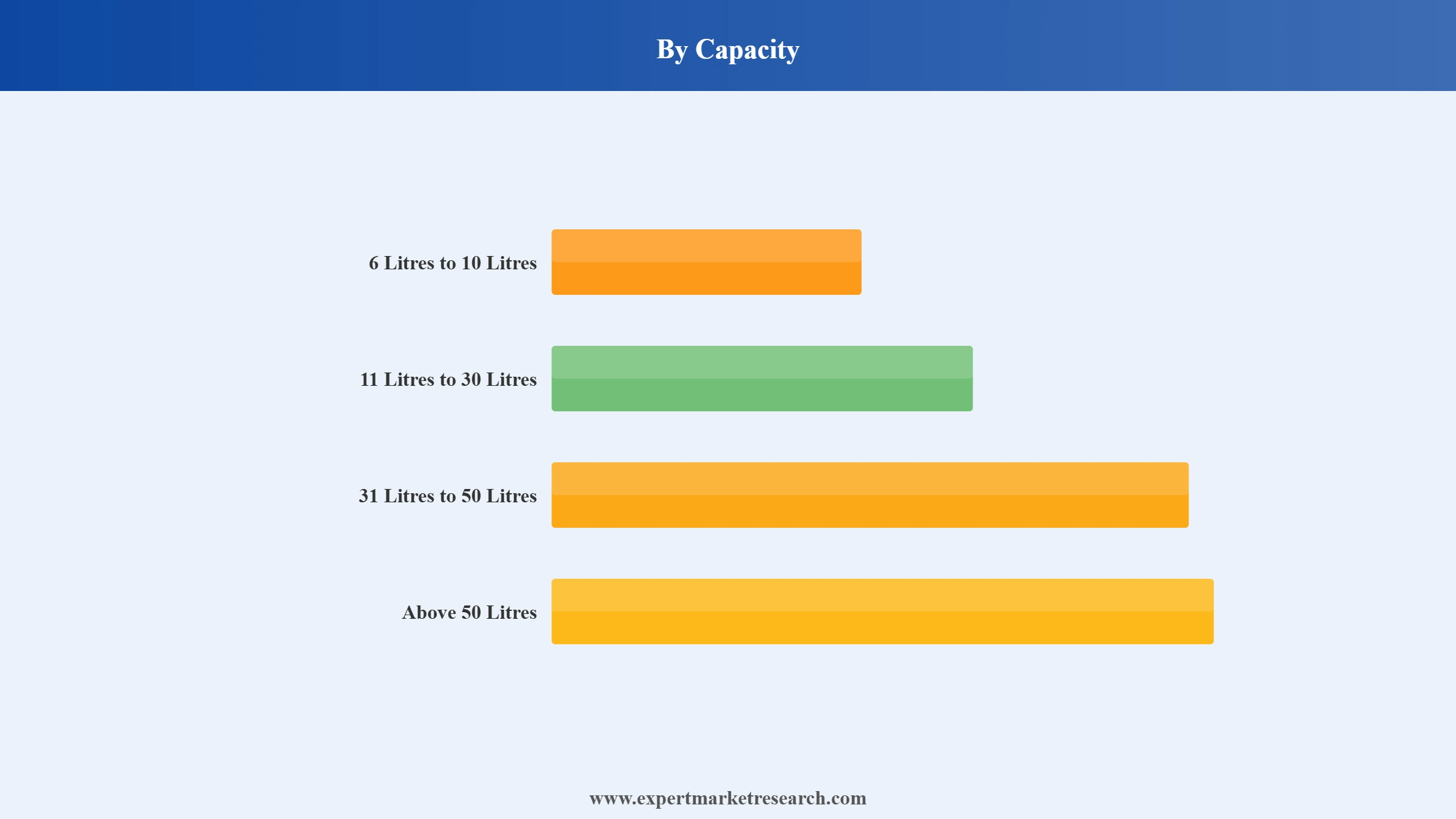

Market Breakup by Capacity

Key Insight: The 31 litres to 50 litres segment leads the global backpack market by volume, serving the broadest range of use cases from day hiking and weekend travel to student campus carry. Smaller 6-10 litre packs are gaining traction among urban commuters and cyclists seeking lightweight, minimalist options, while above 50 litre models serve expedition trekkers. Rising outdoor participation and adventure tourism continue to drive demand across mid-to-large capacity tiers in the global backpack market.

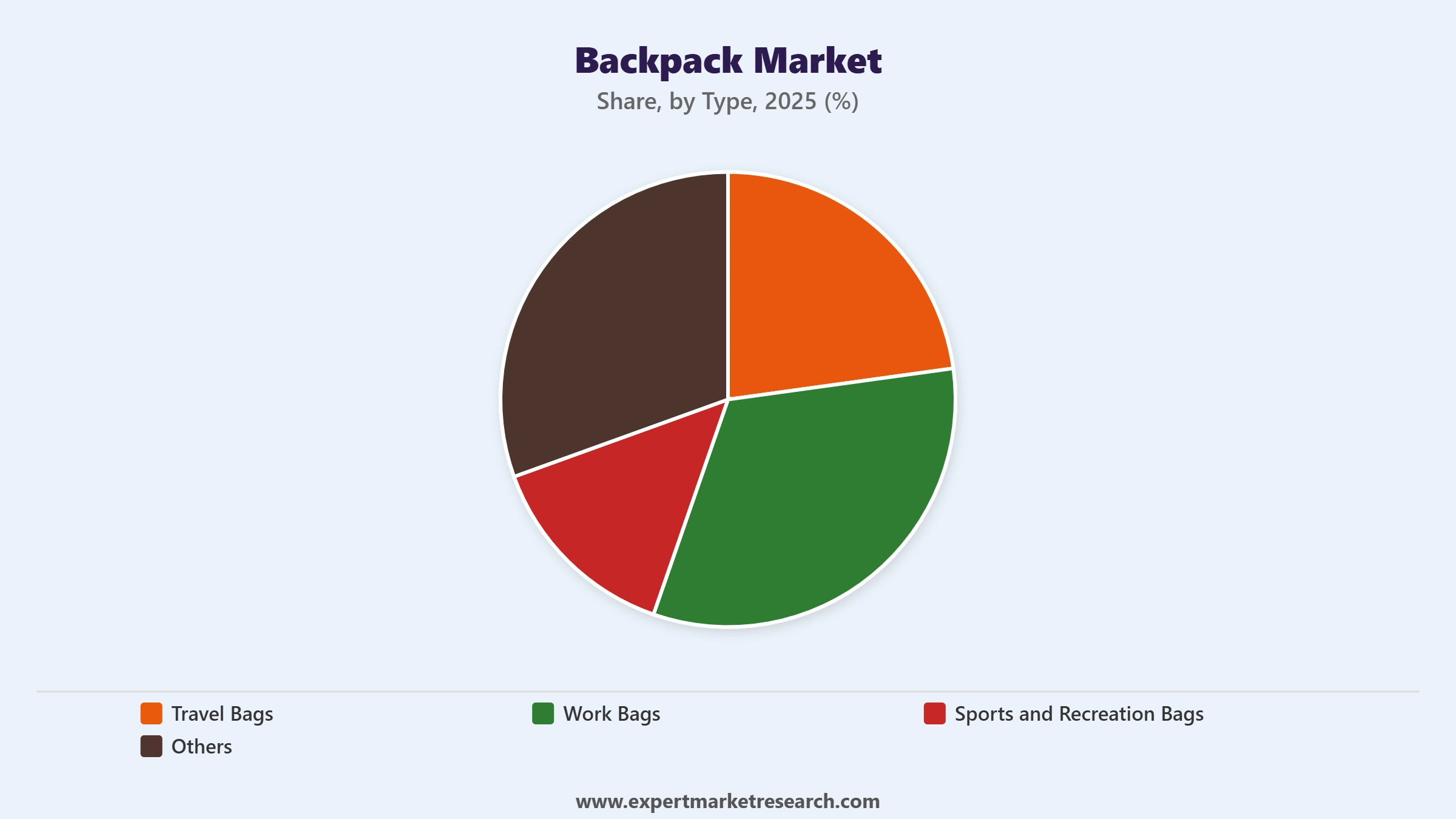

Market Breakup by Type

Key Insight: Travel bags hold the largest share of the global backpack market by type, benefitting from the post-pandemic resurgence in tourism and the rise of carry-on only travel. Work and laptop bags rank second, driven by hybrid work culture and growing laptop penetration. Sports and recreation bags are expanding on the back of fitness culture and growing outdoor activity participation. Brands are increasingly blurring category lines by launching hybrid work-travel packs, widening the addressable market and supporting sustained revenue growth in the global backpack market.

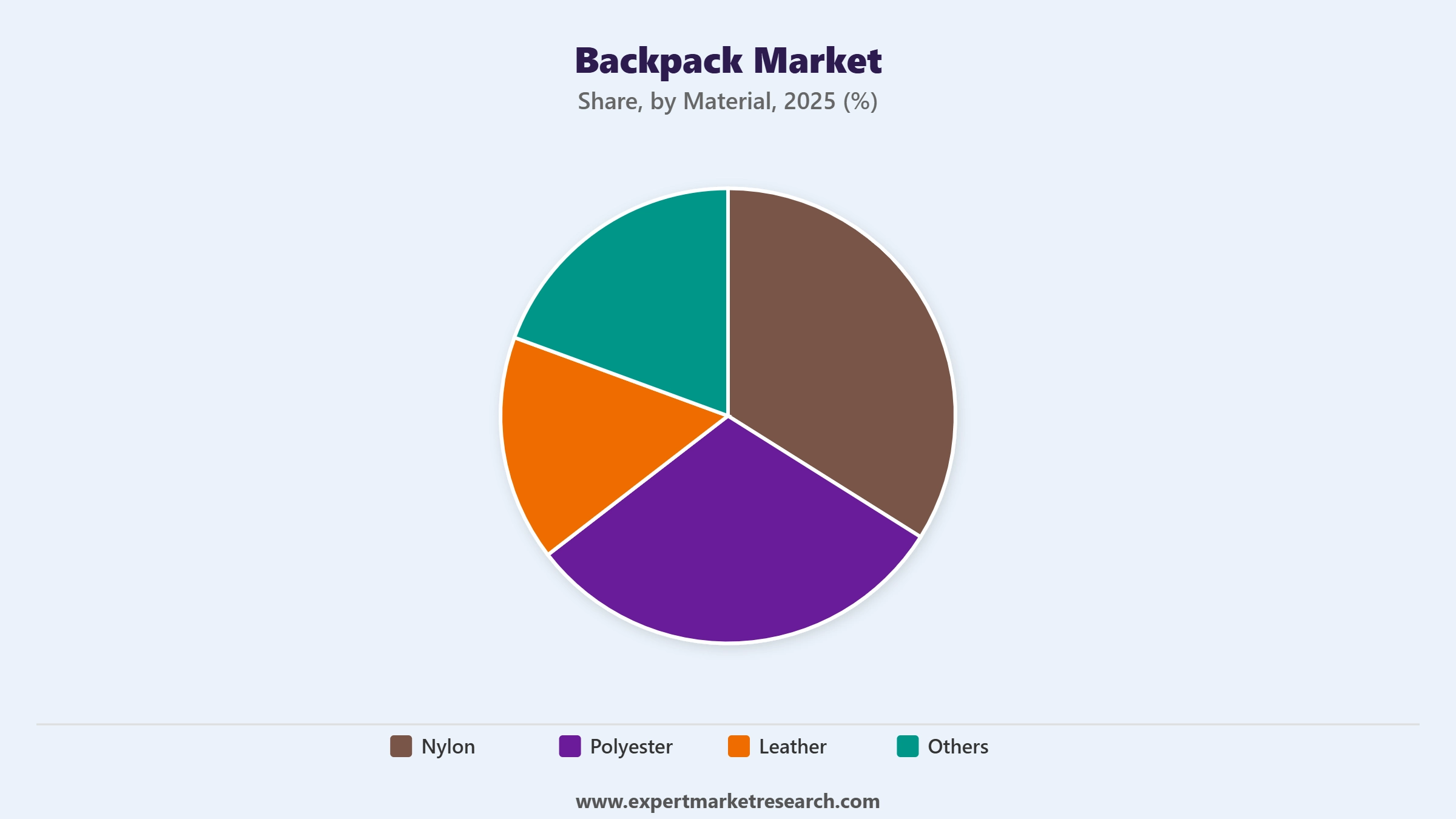

Market Breakup by Material

Key Insight: Nylon dominates backpack material choice due to its superior abrasion resistance, water repellency, and durability, making it the preferred choice for outdoor, travel, and performance applications. Polyester is the second most popular material, widely used for affordably priced everyday and student backpacks. Leather carries a premium positioning appealing to business commuters and fashion-oriented buyers. Recycled nylon and polyester variants are gaining ground rapidly as sustainability moves from a marketing claim to a product prerequisite in the global backpack market.

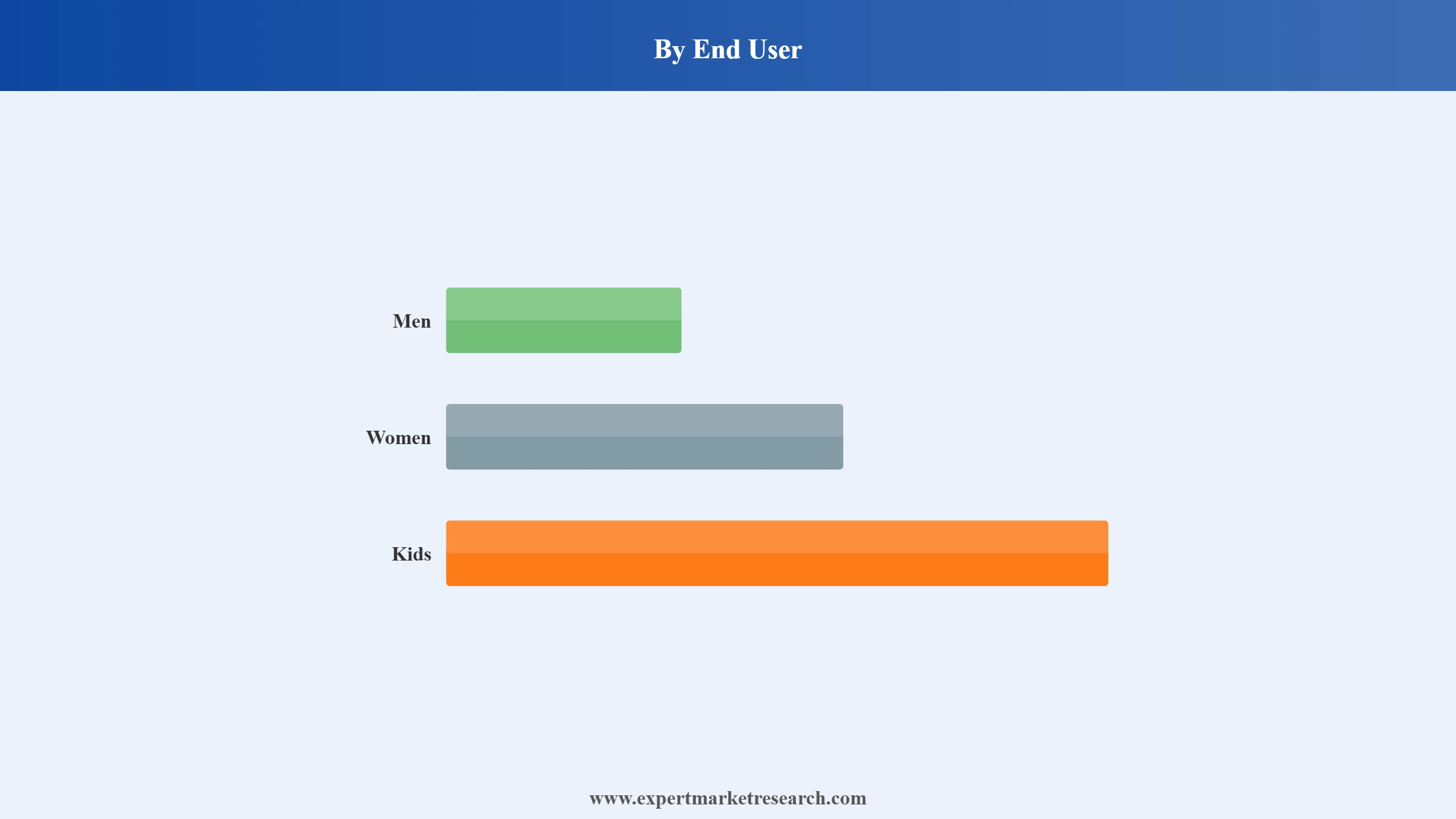

Market Breakup by End User

Key Insight: Men account for the largest end-user share in the global backpack market, as backpacks serve as their primary carry solution for commuting and travel. Women represent a fast-growing cohort as brands expand ergonomic, fashion-forward, and multifunctional designs tailored to female proportions. The kids segment benefits from consistent global school enrolment, with parents prioritising ergonomic support, safety features, and branded designs when purchasing school backpacks across retail and online channels in the global backpack market.

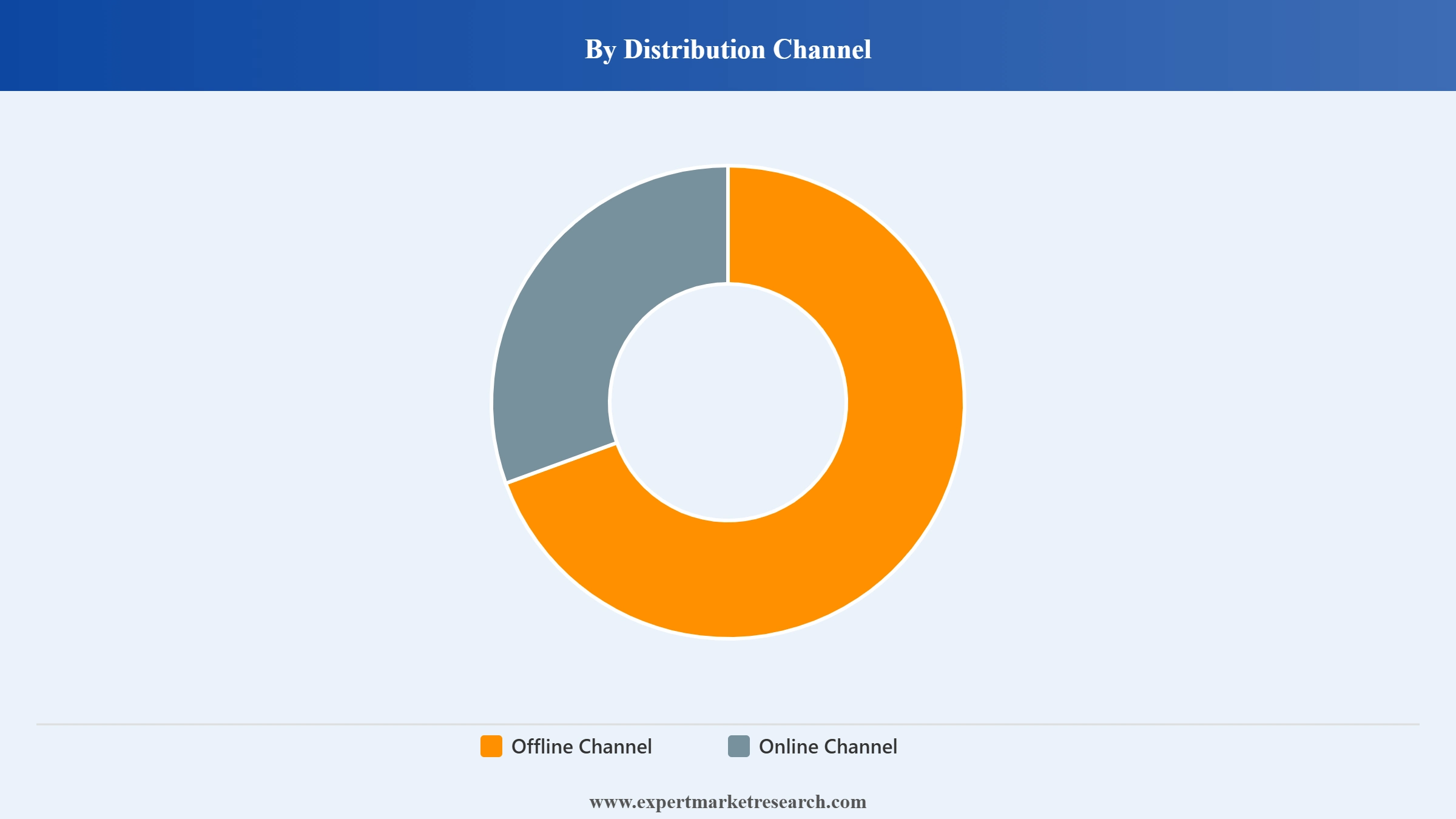

Market Breakup by Distribution Channel

Key Insight: Offline retail holds the larger absolute share, driven by in-store ergonomic testing, tactile quality assessment, and the importance of fit evaluation for high-value and technical backpacks. Online is the fastest-growing channel, supported by expanding e-commerce reach, direct-to-consumer brand launches, influencer-led discovery, and the convenience of home delivery. Specialty outdoor retailers remain important for premium performance packs, while marketplaces accelerate sales of everyday and student backpacks across the global backpack market.

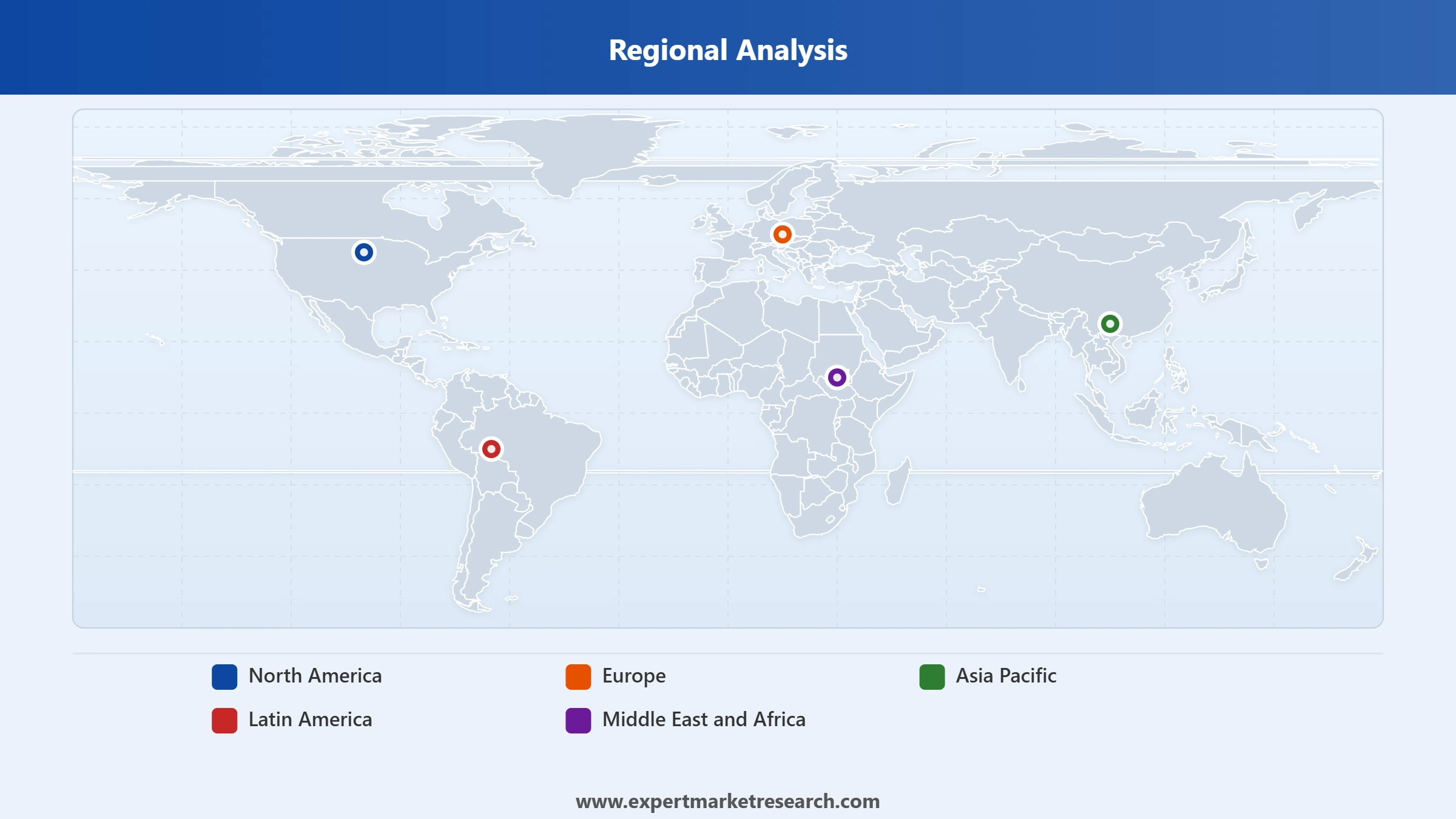

Market Breakup by Region

Key Insight: North America leads the global backpack market by value, underpinned by high disposable incomes, strong outdoor recreation culture, and premium product demand. Europe ranks second, driven by established outdoor heritage brands and sustainability-conscious consumers. Asia Pacific is the fastest-growing region, propelled by rising urbanisation, expanding student populations, and rapid e-commerce penetration. Latin America and the Middle East and Africa represent emerging opportunity markets with rising youth populations and increasing adventure tourism activity driving the global backpack market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By capacity, 31 litres to 50 litres leads the backpack market due to its versatility across outdoor, travel, and campus carry use cases

The 31 litres to 50 litres capacity segment holds the dominant share of the global backpack market, serving the widest range of everyday occasions from multi-day trekking and weekend travel to student campus carry. Its balance of storage volume and portability makes it the default choice across consumer demographics, combining large enough capacity for overnight and short-trip packing with manageable carry weight for daily use. Brands including Osprey, Deuter, and The North Face have built flagship product lines around this capacity range.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The 11 litres to 30 litres range is the fastest-growing capacity segment, driven by urban commuters, gym users, and casual outdoor participants who prioritise lightweight carry with sufficient everyday storage. The 6 to 10 litre micro-pack segment is gaining traction among festival-goers, cyclists, and minimalist travellers seeking hands-free portability for day trips. Above 50 litre expedition packs serve a smaller but commercially valuable segment of serious mountaineers and through-hikers, sustaining premium price positioning for specialist brands within the global backpack market.

By type, travel bags hold the largest share driven by travel recovery and demand for versatile multi-use carry solutions

Travel bags lead the global backpack market by type, as post-pandemic international travel recovery and the rise of carry-on only travel have sustained high unit demand. Consumers seek packs that meet airline cabin size restrictions while offering laptop protection, organisational compartments, and weather resistance. In February 2026, Nike's ACG relaunch demonstrated how athletic brands are pushing performance credibility into the travel backpack segment, intensifying competition and raising product standards across this dominant type category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Work and laptop bags are the second-largest type segment, growing steadily on the back of hybrid work adoption and rising laptop penetration in offices, universities, and schools. Sports and recreation bags are expanding on the back of fitness culture growth and growing outdoor activity participation. Nike's November 2024 Elite EasyOn backpack demonstrated how large sportswear brands are raising the ergonomic and accessibility bar for work-oriented backpacks, driving innovation and intensifying competition within the global backpack market across type segments.

By material, nylon leads the backpack market for its durability and water resistance across outdoor and travel applications

Nylon dominates the global backpack market by material, valued for its superior tear resistance, lightweight profile, and water-repellent properties that make it the standard choice for performance, travel, and outdoor backpacks. Technical nylon variants such as Cordura are used by premium brands including Osprey and Deuter to offer long-lasting durability, while standard nylon grades serve everyday and student segments at competitive price points. Recycled nylon is growing rapidly as brands respond to sustainability pressure without compromising the performance attributes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Polyester holds the second-largest material share, serving the mass-market and student segments where cost efficiency is prioritised. Recycled polyester adoption is accelerating, with Deuter committing to incorporate it into 90% of its 2025 lineup. Leather maintains premium positioning, appealing to fashion-conscious consumers and business commuters seeking a refined aesthetic. Others including canvas and biodegradable plant-based fibres are emerging at the sustainability-focused premium end of the global backpack market, supporting continued material diversity and price-tier segmentation.

By end user, men hold the dominant share while women represent the fastest-growing consumer segment

Men account for the largest end-user share of the global backpack market, as backpacks represent their primary carry solution for commuting, travel, and outdoor activities, with fewer competing bag format alternatives available compared to women. Men's backpacks span a wider range of technical and performance applications, from laptop commuter packs to expedition-grade outdoor packs, sustaining high per-category unit values and strong brand investment in the men's backpack segment globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Women are the fastest-growing end-user segment in the global backpack market, supported by brands' investment in women's specific ergonomic design, lighter colourways, and multifunctional aesthetics that serve both professional and leisure occasions. Brands such as Patagonia, Cotopaxi, and Osprey have developed dedicated women's backpack lines engineered to female body dimensions and carrying preferences. The kids segment benefits from consistent global school enrolment, with parents prioritising certified ergonomic designs and safety features for school-going children.

By distribution channel, offline retail holds the larger share while online is the fastest-growing channel

Offline retail holds the larger absolute share of the global backpack market, as in-store fit evaluation, ergonomic testing, and specialist staff advice remain critically important particularly for technical and high-value backpack purchases. Specialty outdoor retailers including REI in the United States and Globetrotter in Germany provide the premium trial environment that supports the conversion of high-consideration backpack purchases across the market's most valuable consumer segments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online is the fastest-growing distribution channel, supported by expanding e-commerce reach, direct-to-consumer brand launches, influencer-led discovery, and the convenience of home delivery. JanSport's February 2025 collegiate partnership and Nike's February 2026 ACG relaunch both incorporated strong digital components, reflecting how major backpack brands are prioritising online channel investment. Virtual fitting tools and hassle-free return policies are reducing purchase risk and accelerating digital conversion rates in the global backpack market.

North America dominates the global backpack market due to high disposable income, mature outdoor culture, and dense specialty retail

North America commands the largest revenue share of the global backpack market, anchored by the United States where high disposable incomes, an established outdoor recreation culture, and strong travel activity sustain consistent demand for premium and performance backpacks. A dense network of specialty outdoor retailers and direct-to-consumer e-commerce platforms gives brands efficient access to the market's most commercially valuable consumer segments. Nike's February 2026 All Conditions Gear relaunch, which opened a flagship store in Beijing, illustrated how brands are also leveraging this regional strength to expand globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing region in the global backpack market, propelled by rising urbanisation, expanding student populations, and surging e-commerce penetration across China, India, and Southeast Asia. Yeti's January 2024 acquisition of Mystery Ranch signalled growing investment in premium pack performance across the region, while adventure tourism expansion and a rapidly growing outdoor recreation participant base continue to build structural demand momentum within the global backpack market.

The global backpack market is moderately fragmented, with large athletic conglomerates, specialist outdoor brands, premium lifestyle players, and value-oriented mass-market manufacturers competing for share. Top brands including Nike, Adidas, VF Corporation (via The North Face), Samsonite, and Patagonia compete on global distribution, brand equity, and product innovation, while specialists such as Osprey and Deuter hold loyal followings in the technical outdoor segment. Sustainability, tech integration, and direct-to-consumer channel development are the primary competitive battlegrounds.

Market leadership increasingly depends on the ability to serve multiple end-use occasions through a coherent brand identity. Brands combining performance credibility with sustainable materials and an engaging digital presence are best positioned to capture the growing lifestyle and adventure-oriented consumer cohorts driving long-term growth in the global backpack market.

Founded in 1968 and headquartered in Denver, Colorado, VF Outdoor LLC operates The North Face, one of the world's most recognised outdoor performance brands. The North Face backpack range spans everyday commuter packs, technical climbing packs, and premium travel designs. Its Borealis and Surge lines are among the best-selling styles globally, supported by broad distribution across specialty retail, department stores, and e-commerce platforms. Sustainability commitments include increasing recycled material use across its product lines globally.

Founded in 1974 and headquartered in Cortez, Colorado, Osprey Packs is a specialist backpack brand celebrated for its technical outdoor packs. The company's all-mighty guarantee offers lifetime repair or replacement, building exceptional brand loyalty among trekkers, hikers, and travellers. Acquired by Helen of Troy in 2021, Osprey gained broader distribution and marketing resources. Its Atmos, Talon, and Farpoint ranges cover everything from ultralight day hiking to extended expedition carry.

Founded in 1910 and headquartered in Luxembourg, Samsonite is the world's largest luggage and travel gear company. Its backpack portfolio spans business, travel, and lifestyle categories under the Samsonite, American Tourister, and Tumi brands. The company leverages its extensive global retail and e-commerce distribution to compete across price tiers. Samsonite's focus on ergonomic design, anti-theft features, and laptop-protective compartments keeps its backpack range commercially relevant for professional and frequent travel segments.

Founded in 1898 and headquartered in Kaufbeuren, Germany, Deuter is one of Europe's most respected technical backpack manufacturers, known for its Aircomfort ventilation systems and ergonomic fit systems. Deuter serves trekking, hiking, ski touring, and urban cycling segments, with a strong presence in German-speaking countries and growing distribution across North America and Asia Pacific. Its commitment to recycling 90% of its 2025 lineup into sustainable materials underlines its leadership in responsible manufacturing in the global backpack market.

Other key players in the market are Adidas AG, Nike Inc., Patagonia Inc., L.L. Bean Inc., Lululemon Athletica Inc., Herschel Supply Company, Under Armour Inc., Puma SE, Global Uprising PBC, Nordace Limited, Dakine IP Holdings LP, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the complete picture of the global backpack market with our latest report. Explore how sustainability trends, smart tech integration, and the adventure tourism boom are reshaping the category, and identify where the next growth opportunities lie across capacity, type, material, and region. Whether you are a manufacturer, retailer, brand investor, or e-commerce operator, this report gives you the data and clarity to move confidently. Download your free sample today and uncover the key trends and opportunities defining the future of backpacks globally.

United Kingdom Backpack Market

North America Backpack Market

Asia Pacific Backpack Market

Mexico Backpack Market

Europe Backpack Market

India Backpack Market

Upto 15% Off

USD

$2999 $2699

$4839 $4355

$5999 $5099

$7259 $6170

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 17.46 Billion.

The market is assessed to grow at a CAGR of 6.00% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach almost USD 31.27 Billion by 2035.

The major market drivers include increasing working population, changing lifestyles, rapid urbanisation, and innovative marketing strategies by market players.

The key trends guiding the growth of the market include the growing travel and tourism industry, evolving technology, and the launch of diversified backpacks by market players.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The various capacities that are available in the market include 6 litres to 10 litres, 11 litres to 30 litres, 31 litres to 50 litres, and above 50 litres.

The different types of backpacks include travel bags, work/laptop bags, and sports and recreation bags, among others.

The different materials used for backpacks are nylon, polyester, and leather, among others.

The major end users in the market are men, women, and kids.

The major players in the market are VF Outdoor, LLC, L.L. Bean Inc, Adidas AG, Patagonia, Inc., Lululemon Athletica Inc., Nike, Inc., Osprey Packs, Inc., Deuter Sport GmbH, Global Uprising, PBC, Nordace Limited, Herschel Supply Company, Under Armour, Inc., Puma SE, Samsonite IP Holdings S.A.R.L, and Dakine IP Holdings LP, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Capacity |

|

| Breakup by Type |

|

| Breakup by Material |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,839

USD 4,355

tax inclusive*

Five User License

Five User

USD 5,999

USD 5,099

tax inclusive*

Corporate License

Unlimited Users

USD 7,259

USD 6,170

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.