Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

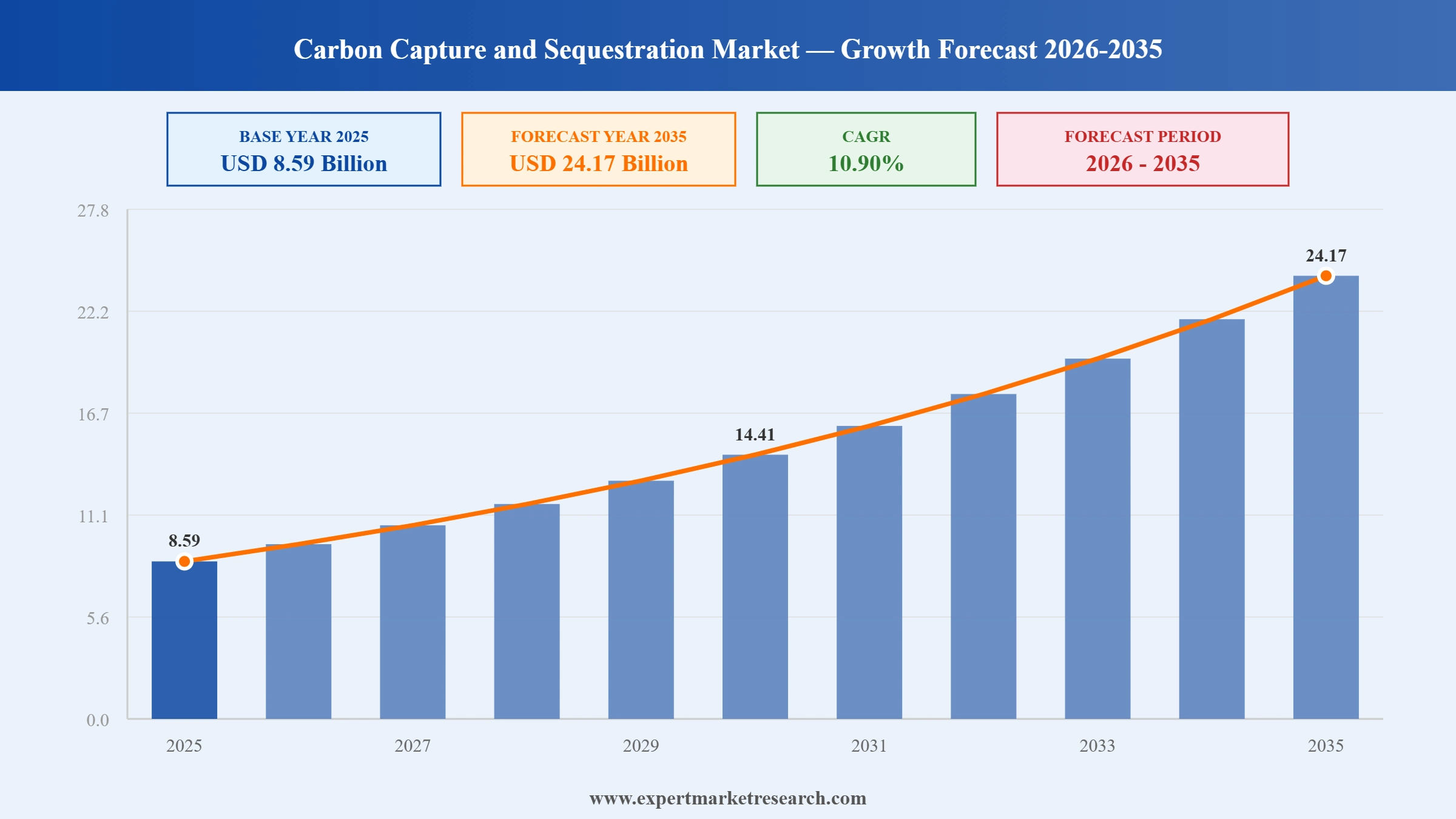

The global carbon capture and sequestration market reached USD 8.59 Billion in 2025 and is projected to grow at a compound annual growth rate CAGR of 10.90% during the forecast period of 2026 to 2035, reaching USD 24.17 Billion by 2035, according to Expert Market Research. This robust double-digit growth trajectory reflects the escalating urgency of industrial decarbonisation across the global economy, the progressive commercialisation of CCS technologies across power generation, cement, steel, chemicals, and oil and gas sectors, and the structural expansion of government policy frameworks including carbon pricing mechanisms, tax credits, and direct funding programmes that are transforming carbon capture and sequestration from an experimental technology into a commercially viable and increasingly mandatory component of national and corporate net-zero strategies.

The carbon capture and sequestration market encompasses the full value chain of technologies, services, and infrastructure required to capture carbon dioxide emissions at industrial point sources, compress and transport captured gas through pipeline or shipping networks, and inject it into geological formations including depleted oil and gas reservoirs, deep saline aquifer formations, and unmineable coal seams for permanent underground storage. The industry additionally encompasses the fast-growing direct air capture sub-sector, which removes CO2 directly from the atmosphere, and bioenergy with carbon capture and storage (BECCS), which combines biomass energy generation with CCS to produce net-negative emissions. CCS is recognised by the International Energy Agency and the Intergovernmental Panel on Climate Change as an essential technology pathway for achieving the Paris Agreement's 1.5°C target, given the structural difficulty of eliminating CO2 from hard-to-abate industrial sectors through electrification or fuel switching alone.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Carbon capture and sequestration (CCS) refers to the integrated set of technologies and infrastructure systems that capture CO2 emissions from industrial point sources or from the atmosphere, compress and transport the captured gas, and permanently store it in geological formations preventing atmospheric release and mitigating climate change. The three primary process stages capture, transport, and storage each encompass distinct technologies, engineering disciplines, regulatory requirements, and commercial models constituting the CCS value chain. Carbon capture utilisation and storage (CCUS) extends this framework by productively utilising captured CO2 in industrial processes including enhanced oil recovery (EOR), synthetic fuel production, and construction materials manufacturing before or instead of permanent geological storage.

Carbon capture technologies operate across four primary pathways. Post-combustion capture removes CO2 from flue gases after fossil fuel combustion, most commonly using chemical absorption with amine-based solvents such as monoethanolamine (MEA) and advanced proprietary amine blends. Pre-combustion capture converts fossil fuels to a CO2-hydrogen mixture before combustion, separating and capturing CO2 while utilising clean hydrogen as fuel the foundational technology for blue hydrogen and low-carbon ammonia production. Oxy-fuel combustion burns fuel in pure oxygen, producing a concentrated CO2 flue stream requiring less energy-intensive capture processing. Direct air capture (DAC) extracts CO2 from ambient air at atmospheric concentration. Bioenergy with carbon capture and storage (BECCS) combines biomass energy generation with CCS to produce net-negative emissions removing more CO2 from the atmosphere than the entire value chain generates. Carbon mineralisation permanently stores CO2 by converting it into solid carbonate minerals, offering inherently permanent storage without geological monitoring requirements. Storage options include deep saline aquifer formations, depleted oil and gas reservoirs utilised for EOR, and unmineable coal seams where CO2 adsorption is permanent.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Enhanced oil recovery injecting CO2 into mature oil reservoirs to increase pressure, mobilise residual crude, and simultaneously sequester CO2 is the largest and most commercially established CCS end-use, providing a revenue-generating CO2 outlet that materially improves project economics versus pure geological storage. EOR-CCS projects generate dual revenue: incremental oil production revenue and US 45Q tax credit income ($60/tonne for EOR storage, $85/tonne for geological sequestration). CF Industries' USD 4 billion Louisiana JV capturing 2.3 MtCO2/yr for EOR via Occidental's 1PointFive exemplifies integrated industrial CCS with EOR monetisation at commercial scale. The US Permian Basin, Williston Basin, and Gulf Coast are the primary EOR-CCS geographies, with deep saline aquifer formations increasingly substituting depleted reservoirs as CO2 storage sites where EOR is not economically viable.

Tightening greenhouse gas emission regulations and expanding carbon pricing mechanisms across major economies are creating structural compliance imperatives for CCS deployment in hard-to-abate industries. The European Union's Carbon Border Adjustment Mechanism (CBAM) imposes carbon costs on imports from countries without equivalent carbon pricing, incentivising European industrial operators to deploy CCS and reduce embedded carbon in production. The EU Net-Zero Industry Act's binding 50 MtCO2/yr geological storage target for 2030 is driving accelerated CCS infrastructure investment across Germany, Belgium, Norway, and Denmark. Carbon credit markets where verified CO2 sequestration generates tradeable credits under voluntary and compliance frameworks are creating additional revenue streams for CCS project developers, improving project financial models particularly for early-stage and smaller-scale deployments.

Government funding programmes and tax incentive structures in major economies have materially de-risked CCS project development. The US IIJA provided USD 8.2 billion for CCS programmes over 2022–2026, complemented by the enhanced 45Q tax credit ($85/tonne geological, $60/tonne EOR) and DOE's USD 1.3 billion Point-Source CCS and USD 1.7 billion Demonstration Projects programmes. Germany's €6 billion industrial decarbonisation initiative, Belgium's Flanders €2 billion package, and Norway's government-backed Northern Lights collectively represent a European public investment base mobilising significant private co-investment. These incentive frameworks are enabling projects that would be commercially unviable at current capture costs to reach final investment decisions, accelerating the technology cost reduction curve.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Public-private partnerships are proving essential to bridging the funding gap between CCS project costs and private sector return requirements, enabling a growing number of large-scale CCS projects to reach financial close. Government co-investment typically taking the form of grants, loan guarantees, concessional finance, and regulated revenue support reduces the equity risk for private CCS project developers, enabling institutional capital access at commercially viable terms. The Alberta government's 50% co-funding of CarbonQuest's February 2026 gas compressor CCS project illustrates the scalability of this public-private co-investment model from large central projects down to distributed smaller-scale CCS deployments. Northern Lights jointly developed by Equinor, Shell, and TotalEnergies with Norwegian government support demonstrates the hub-and-spoke public-private model where shared transport and storage infrastructure is co-funded to serve multiple industrial CO2 emitters across national borders.

The accelerating adoption of corporate net-zero commitments, science-based targets, and mandatory Scope 1, 2, and 3 emissions disclosure requirements is driving industrial operators to evaluate CCS as a necessary component of decarbonisation portfolios. Hard-to-abate process industries cement (60% of emissions from limestone decomposition), primary steel (blast furnace process CO2), and chemical manufacturing (process and energy emissions) have limited electrification alternatives, making CCS a strategic requirement for companies committed to net-zero aligned targets. BlackRock GIP's acquisition of a 49.99% stake in Eni's CCUS business demonstrates institutional investor confidence in CCS as infrastructure-grade revenue-generating assets aligned with net-zero investment mandates. Growing corporate demand for certified carbon removals to offset residual Scope 3 emissions after all feasible reduction measures are applied is additionally expanding the commercial market for DAC and BECCS.

Chemical absorption using amine-based solvents remains the dominant and most commercially mature capture method, accounting for the largest share of currently deployed CCS capacity through post-combustion applications at power plants, cement kilns, and gas processing facilities. However, the high energy penalty of conventional amine solvent regeneration which consumes 15 to 25% of a host facility's energy output is driving intense R&D investment in next-generation alternatives. Advanced solvent formulations with lower regeneration energy, phase-change solvents that selectively precipitate when loaded with CO2, ionic liquid solvents, and electrochemical CO2 capture that replaces thermal regeneration with energy-efficient electro-swing processes are all advancing toward commercial demonstration. Metal-organic framework (MOF) adsorbent materials as deployed in CarbonQuest's February 2026 Alberta project offer exceptional CO2 selectivity and cycle capacity with lower energy requirements than liquid solvents, positioning MOFs as a transformative capture material for the next generation of industrial CCS installations.

Membrane separation is the fastest-growing capture method in the global CCS market, leveraging selectively permeable polymer or inorganic membranes to separate CO2 from mixed gas streams based on differential permeability rates. Unlike chemical absorption, membrane separation systems have no solvent regeneration requirement, lower moving part complexity, modular scalability, and a smaller physical footprint advantages that make them particularly well-suited for retrofit applications on existing industrial facilities and for smaller-scale distributed CCS deployments where large chemical absorption plants are impractical. Advances in membrane material selectivity and permeance including mixed matrix membranes incorporating MOF or zeolite particles into polymer matrices are improving the CO2 purity achievable through single-stage membrane separation, expanding the range of industrial applications where membranes can substitute for solvent-based capture. Natural gas processing, hydrogen production, and cement manufacturing are the primary near-term membrane separation deployment contexts in the CCS market.

Bioenergy with carbon capture and storage (BECCS) combining biomass combustion or gasification for energy generation with CCS on the resulting CO2 stream is the most widely modelled negative emissions technology in global climate scenarios, producing net-negative emissions that can offset residual fossil fuel use in other sectors. Multiple BECCS projects are in development across the US, UK, and Scandinavia, targeting bioenergy power plants, ethanol refineries, and pulp and paper mills where biogenic CO2 streams are amenable to post-combustion capture. Carbon mineralisation permanently stores CO2 by reacting it with mineral silicates to form stable solid carbonates a storage form that is inherently permanent without the monitoring requirements of geological injection. Olivine Technologies, CemCycle, and other emerging mineralisation companies are developing reactor-based approaches that combine CO2 sequestration with production of useful mineral products, improving the commercial economics of mineralisation-based CCS relative to pure geological storage alternatives.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Deep saline aquifer formations porous geological strata saturated with saline water at depths typically exceeding 800 metres are the globally dominant long-term CO2 storage resource, with estimated storage capacity orders of magnitude larger than depleted oil and gas reservoirs alone. The commercial validation of offshore saline aquifer storage by Norway's Northern Lights project which issued its first verified CO2 storage certificates from the Aurora saline aquifer formation in 2026 and Denmark's Greensand project commencing operations in 2026 represents a critical market milestone that establishes the commercial precedent for cross-border contracted CO2 transport and injection into saline aquifer formations. The IEA estimates that global deep saline aquifer storage capacity is sufficient to store centuries of global CO2 emissions at projected capture rates, making aquifer storage site characterisation, permitting, and development the strategic long-term priority for the CCS industry's infrastructure build-out.

The carbon capture and sequestration market's trajectory beyond 2030 is defined by the progressive cost reduction of capture technologies toward the USD 50 to 100 per tonne range that would make CCS cost-competitive with other decarbonisation options across a broad range of industrial applications, the maturation of CO2 transport and storage infrastructure networks in Europe, North America, and Asia Pacific that will enable CCS to scale from isolated projects to integrated regional industrial decarbonisation systems, and the potential for DAC costs to decline toward USD 150 to 300 per tonne by the mid-2030s as manufacturing learning curves and energy cost reductions compound. The natural gas-fired power generation sector with CCS expected to grow significantly as AI data centre electricity demand accelerates represents one of the largest potential new market segments for CCS deployment in the 2027 to 2035 period. CCS experts at leading carbon management firms project multiple deals for natural gas power with CCS to power data centres as a defining trend of the late 2020s, creating a new commercial model where CCS-equipped gas plants provide firm low-carbon electricity to AI hyperscalers seeking to achieve their Scope 2 net-zero commitments.

The carbon capture and sequestration market faces significant technical, economic, and social challenges that constrain deployment velocity relative to the scale required for meeting global climate targets. The high energy penalty of current post-combustion chemical absorption systems reducing host facility net energy output by 15 to 25 percentage points materially increases the levelised cost of CCS-equipped facilities relative to alternative low-carbon options, creating an economic competitiveness challenge in electricity markets with rapidly falling renewable energy costs. Permitting timelines for CO2 pipeline infrastructure and geological storage site qualification have become critical project development bottlenecks: despite significant policy funding commitments, the lengthy regulatory approval processes for CO2 injection well Class VI permits and saline aquifer storage site certification in many jurisdictions are delaying project delivery and increasing financing uncertainty. Public acceptance challenges including local community concern about CO2 pipeline routing, underground saline aquifer storage safety, and the perceived risk of enabling continued fossil fuel use have contributed to project delays in several European and North American markets. Policy discontinuity risk remains real, as illustrated by the DOE's partial withdrawal of CCS programme funding that created investor uncertainty.

Several structural dynamics constrain the pace of CCS market expansion, limiting translation of policy ambition into deployed commercial capacity. The geographic mismatch between major industrial CO2 emission sources and optimal geological storage formations particularly in Europe where heavy industry is concentrated in the Rhine-Ruhr, Po Valley, and similar inland industrial clusters far from offshore saline aquifer storage creates CO2 transport infrastructure requirements that add significant capital cost and extend project timelines by years. Chemical absorption-based capture systems' high capital and operating cost relative to the current carbon price in many markets means projects require substantial policy support to achieve commercial returns support that is not uniformly available across geographies and that is subject to policy change risk over the 20 to 40 year operating lifetime of CCS infrastructure investments. The limited commercial availability of CO2 storage liability insurance and long-term storage performance warranty frameworks constrains institutional capital for storage projects where geological containment performance must be warranted across timescales beyond corporate planning horizons. The pausing of Heidelberg Materials' Swedish CCS project following loss of state backing illustrates that even technically advanced projects with high-purity biogenic CO2 streams remain vulnerable to public funding discontinuity.

The carbon capture and sequestration market presents exceptional commercial opportunities across the technology, geographic, and financing dimensions that support sustained above-10% growth through 2035. The expansion of the global CCS project pipeline from approximately 50 MtCO2/yr operational today to an announced pipeline target of 430 MtCO2/yr by 2030 a near-ninefold increase creates a multi-year demand surge for capture technology supply, engineering services, and infrastructure investment that significantly exceeds current industry supply capacity. The EU's binding 50 MtCO2/yr geological storage target for 2030, Germany's €6 billion programme, Belgium's Flanders €2 billion package, and Northern Lights Phase 2 expansion collectively position Europe as the world's most active near-term CCS deployment market. The natural gas power with CCS segment driven by AI data centre electricity demand from hyperscalers seeking firm low-carbon power supply represents an emerging and commercially significant new CCS end-use market for the late 2020s. The voluntary carbon credit market's growing demand for verified CO2 sequestration credits is creating an additional revenue stream for CCS and DAC project developers, improving financial models for projects in markets without mandatory carbon pricing. To access comprehensive opportunity sizing, capture method-specific growth forecasts, storage infrastructure investment analysis, and strategic entry frameworks across all five regional geographies and the full CCS value chain, explore Expert Market Research's complete Carbon Capture and Sequestration Market report.

Carbon capture and sequestration are technologies that capture carbon dioxide from industrial processes before it enters the atmosphere. The method includes transporting the compressed carbon dioxide and storing it in deep geological formations for centuries or millennia. These geological formations are covered with impermeable, non-porous rocks that trap carbon dioxide to prevent its release into the environment.

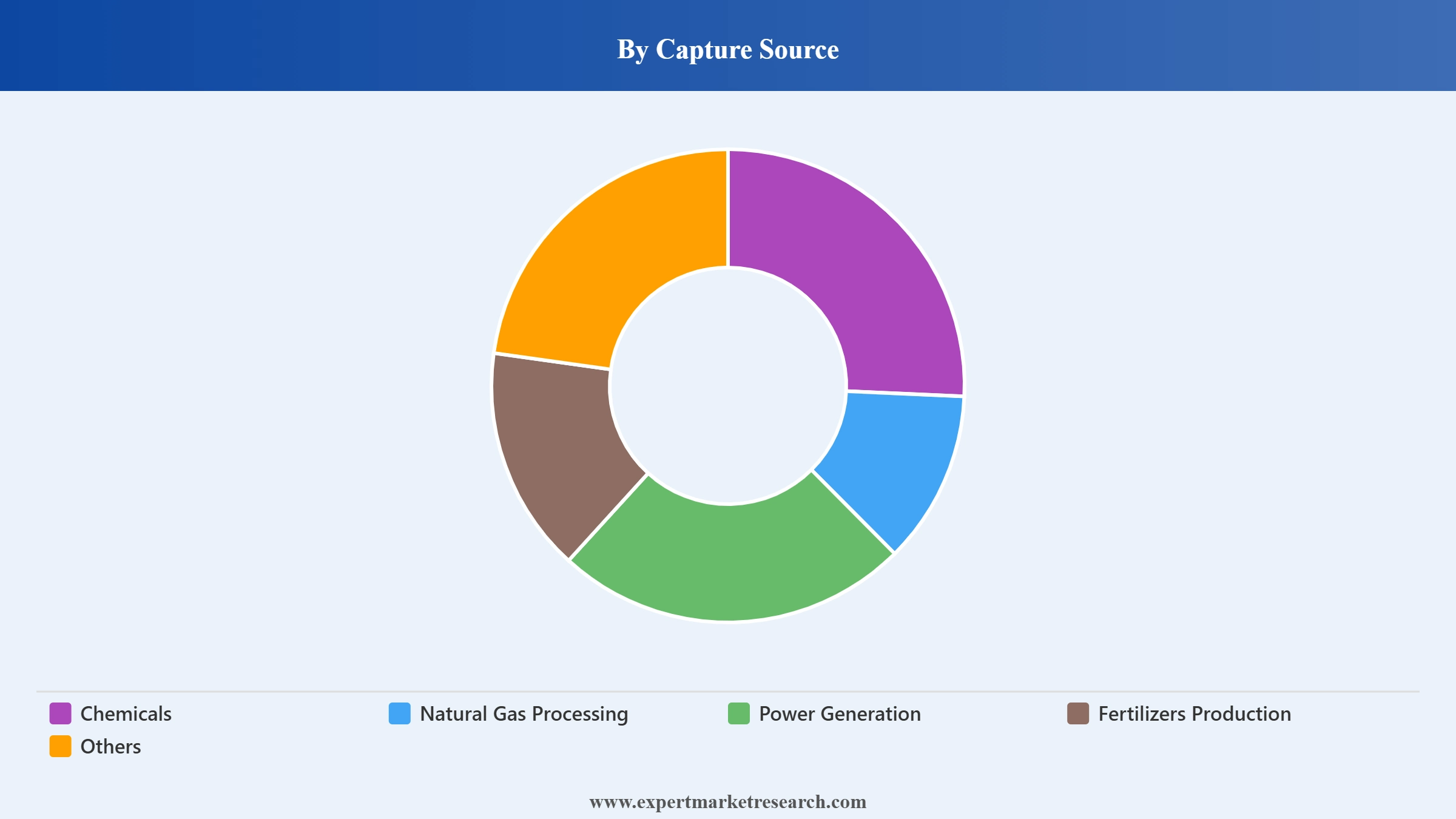

Market Breakup by Capture Source

Key Insights: The chemicals sector generates high-concentration CO2 streams from processes including methanol synthesis and steam methane reforming technically amenable to cost-effective capture due to their purity and pressure. Natural gas processing is the most commercially mature capture source, where CO2 is routinely separated from raw natural gas to meet pipeline quality specifications, making CCS integration a natural extension of existing gas treatment infrastructure. Power generation is a major target capture source for gas-fired and coal-fired plants, enabling continued low-carbon electricity generation from existing baseload assets. Fertilizers production particularly ammonia synthesis via steam methane reforming generates highly concentrated, low-cost CO2 streams; CF Industries' USD 4 billion Louisiana JV capturing 2.3 MtCO2/yr exemplifies this segment's commercial scale. Others include cement, iron and steel, and waste-to-energy facilities where hard-to-abate process emissions make CCS the primary available decarbonisation pathway.

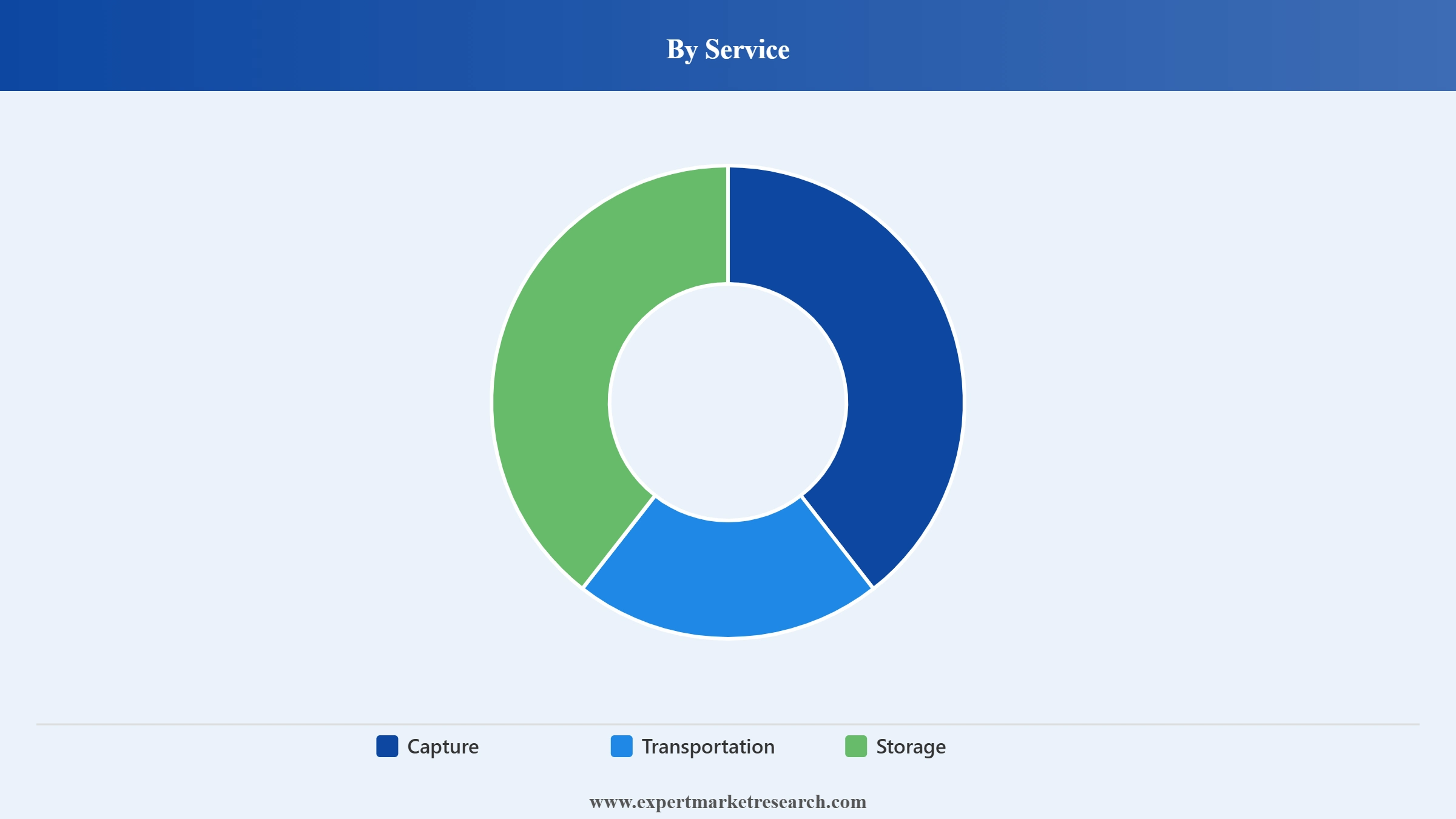

Market Breakup by Service

Key Insights: Capture is the largest service segment, encompassing engineering, procurement, and operation of CO2 capture systems across all industrial point sources. Post-combustion capture applying chemical absorption using amine-based solvents to flue gases is the dominant approach due to its retrofittability to existing assets. Pre-combustion capture converts fossil fuels into a hydrogen-CO2 mixture before combustion, separating CO2 prior to energy generation the foundational service for blue hydrogen and low-carbon ammonia. Oxy-fuel combustion burns fuel in pure oxygen, producing a concentrated CO2 stream that reduces the energy cost of downstream capture. Transportation services encompass CO2 pipeline networks, compression infrastructure, and ship-based CO2 transport for cross-border offshore delivery a growing segment as European offshore storage projects begin receiving continental CO2 volumes. Storage services geological injection into saline aquifers, depleted reservoirs, or coal seams alongside monitoring, measurement, and verification are fast-growing, with Northern Lights' first verified CO2 storage certificates establishing the commercial framework for contracted geological storage as a billable service.

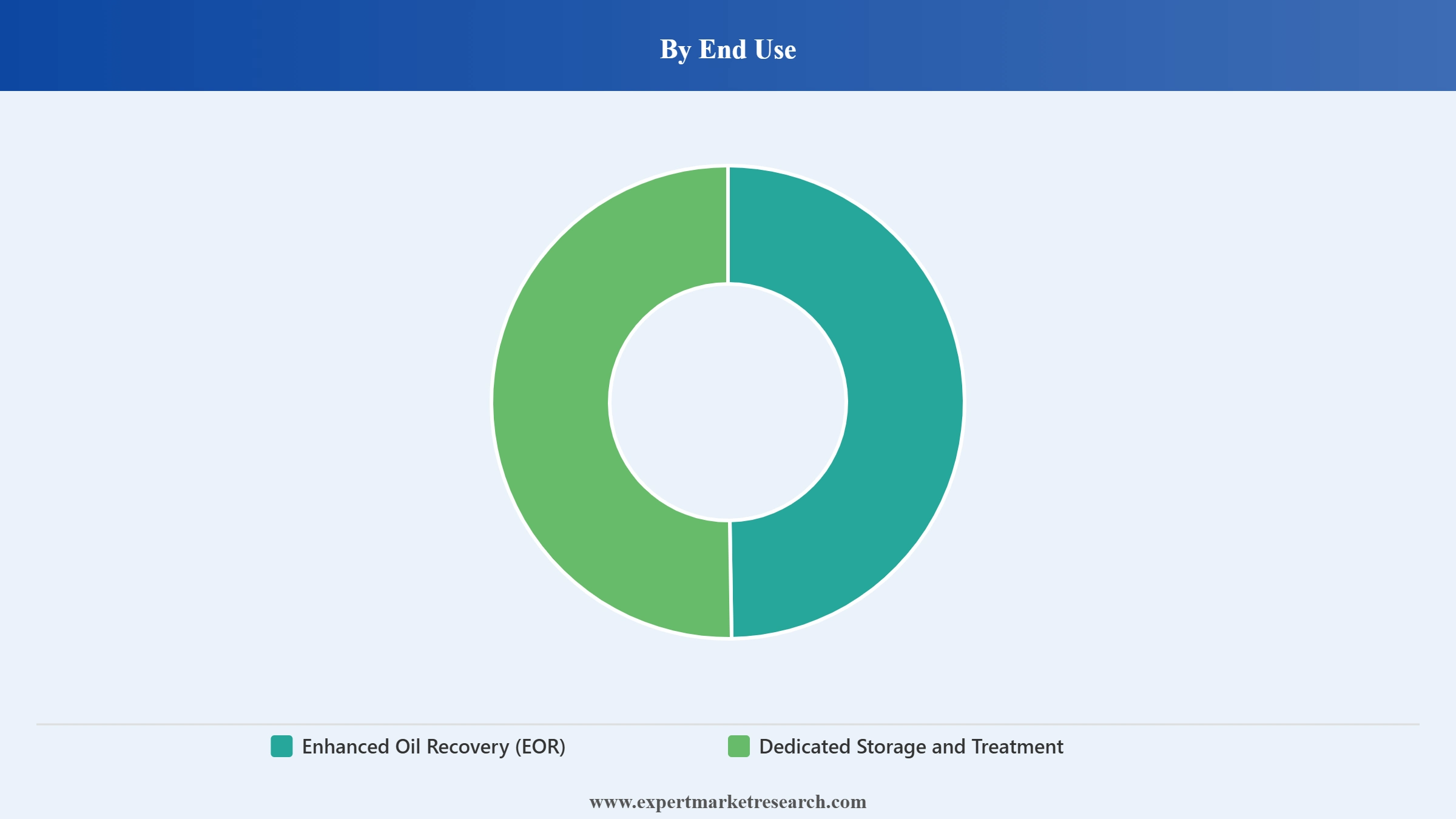

Market Breakup by End Use

Key Insights: EOR is the leading end-use segment injecting CO2 into mature oil reservoirs to restore pressure, mobilise residual crude, and simultaneously achieve permanent geological sequestration. The dual revenue model combining oil production income with the US Section 45Q tax credit ($60/tonne for EOR storage) makes EOR the most commercially self-sustaining CCS application, with the US Permian Basin, Williston Basin, and Gulf Coast as primary geographies. Dedicated Storage and Treatment permanently sequestering CO2 in deep saline aquifer formations or depleted reservoirs without EOR utilisation is the fastest-growing end-use, driven by the EU Net-Zero Industry Act's 50 MtCO2/yr storage target for 2030, Norway's Northern Lights commercial offshore storage service, Denmark's Greensand project, and growing European industrial operators contracting dedicated storage to meet net-zero compliance obligations.

Market Breakup by Regional

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the world's largest CCS market by operational capacity and policy investment, led by the United States which holds the world's most extensive CCS deployment history, the largest operational capacity, and the most comprehensive government funding framework. The US Section 45Q tax credit ($85/tonne geological sequestration, $60/tonne EOR) combined with the IIJA's USD 8.2 billion CCS programme appropriations through 2026, and DOE's USD 1.3 billion Point-Source CCS and USD 1.7 billion Demonstration Projects programmes, collectively create a policy environment enabling commercial-scale CCS across power, industrial, and DAC contexts.

The US CCS market is geographically concentrated in Texas (Permian Basin EOR, Occidental 1PointFive Stratos DAC), Louisiana (CF Industries USD 4B ammonia JV, industrial complex carbon capture), Wyoming (ExxonMobil LaBarge), and the Gulf Coast industrial corridor where petrochemical and refining complex CO2 streams are large, concentrated, and proximate to both pipeline infrastructure and geological storage. Multiple Class VI CO2 injection well permits are progressing through the US EPA permitting pipeline, addressing the primary regulatory bottleneck that has delayed commercial saline aquifer storage project development in the US. Canada's Alberta province is an active CCS hub, supported by the Quest CCS project (Shell), the CCUS incentive programme, and government co-funded frontier projects including the CarbonQuest-Tourmaline Alberta collaboration.

Europe is the most policy-active CCS development region in 2026, with Norway's Northern Lights (first commercial offshore CO2 storage service, Aurora saline aquifer, Phase 2 expanding to 5 MtCO2/yr), Denmark's Greensand commencing operations, Germany's €6 billion industrial decarbonisation programme, Belgium's Flanders €2 billion CCS investment, and the nine-country CCSA European CCUS National Associations Forum launched June 2026 collectively creating the world's most advanced CCS policy ecosystem. The EU Net-Zero Industry Act's binding 50 MtCO2/yr 2030 storage target is the defining regulatory driver for European CCS infrastructure investment. Heidelberg Materials leads cement sector CCS deployment across Norway, UK, and Bulgaria, establishing cement CCS as a replicable commercial model.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing regional CCS market, driven by Japan's comprehensive national CCS framework (offshore storage development, ship-transported CO2, government roadmap targeting hundreds of millions of tonnes annual storage by 2050), South Korea's industrial CCS commitments across steel and petrochemical sectors, Australia's Gorgon LNG CCS project (world's largest designed CCS capacity), and China's expanding industrial CCS portfolio including Sinopec Qilu and PetroChina Jilin EOR-CCS projects. The Asia-Pacific region's large coal and gas power fleet, extensive industrial base, and growing clean hydrogen ambitions collectively create the world's largest long-term potential CCS deployment market.

The Middle East and Africa region's CCS market is anchored by Abu Dhabi's Al Reyadah facility one of the world's first large-scale industrial CCS projects, capturing approximately 800,000 tonnes of CO2 annually from a steel mill for ADNOC EOR. Saudi Aramco is advancing CCS initiatives across refining and gas processing as part of Saudi Arabia's net-zero 2060 commitment. South Africa's Mpumalanga CCS initiative targets the world's densest concentration of coal-fired power plant emissions. Canada's support for ASEAN carbon capture development signals the growing international development finance role in building CCS capacity across developing economy markets.

Latin America's CCS market is in an early development stage, with Brazil and Colombia as the primary national markets. Brazil's Petrobras has operated sub-seabed CO2 injection in pre-salt Santos Basin deepwater reservoirs, providing a foundation of operational CCS experience. Colombia's oil and gas sector creates demand for upstream CCS decarbonisation. The Inter-American Development Bank and World Bank are providing financing for early-stage CCS feasibility studies and policy framework development, establishing institutional foundations for eventual commercial project development across the region.

Key carbon capture and sequestration market players are focusing on scaling capture technology efficiency, expanding CO2 transport and storage infrastructure, and securing long-term industrial offtake agreements. Leading CCS companies are forming strategic public-private partnerships and investing in integrated CCUS platforms to capitalise on growing regulatory and corporate demand for verified industrial decarbonisation solutions. The report gives a detailed analysis of the following key players in the global carbon capture and sequestration market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

ExxonMobil Corporation, headquartered in Spring, Texas, United States, is one of the world's largest energy companies and a major CCS market participant. The company operates the LaBarge CCS facility in Wyoming and the Shute Creek gas processing plant collectively among the largest operational CO2 capture installations in the US. Through its Low Carbon Solutions business, ExxonMobil is advancing large-scale CCS projects across the US Gulf Coast and pursuing blue hydrogen production with integrated CCS as a core energy transition strategy.

Carbon Engineering Ltd., headquartered in Squamish, British Columbia, Canada, is a leading direct air capture (DAC) technology developer, acquired by Occidental Petroleum in 2023. The company pioneered the liquid solvent DAC process that underpins Occidental's 1PointFive Stratos DAC facility in Texas one of the world's first commercial-scale direct air capture plants. Carbon Engineering's technology enables atmospheric CO2 removal independent of industrial point sources, making it a critical enabler of net-negative emissions solutions.

Fluor Corporation, headquartered in Irving, Texas, United States, is one of the world's largest engineering, procurement, and construction (EPC) companies with deep CCS project expertise. Fluor provides full-scope EPC services for carbon capture facilities and holds proprietary technology including the Econamine FG Plus post-combustion capture process, widely deployed at natural gas power plants and industrial facilities globally. The company has delivered major CCS projects across North America, Europe, and the Middle East.

Equinor ASA, headquartered in Stavanger, Norway, is the world's most experienced CCS operator, having pioneered offshore geological CO2 storage at the Sleipner project since 1996 the world's first commercial offshore CCS facility. Equinor leads the Northern Lights project the world's first commercial third-party CO2 transport and storage service which achieved first injection into the Aurora saline aquifer in August 2025 and issued the world's first verified CO2 storage certificates in December 2025. Northern Lights Phase 2 will expand capacity to a minimum of 5 MtCO2/yr with contracted clients across Europe.

Others include Dakota Gasification Company and Linde plc, among other emerging technology developers, EPC contractors, and specialised storage operators contributing to the global carbon capture and sequestration market's commercial and technological development. The comprehensive Expert Market Research report provides an in-depth assessment of the market based on the Porter's five forces model along with giving a SWOT analysis.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global carbon capture and sequestration market attained a value of nearly USD 8.59 Billion.

The market is assessed to grow at a CAGR of 10.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach almost USD 24.17 Billion by 2035.

The major market drivers include the expanding use of captured carbon in various end uses, increasing use of carbon capture and sequestration technologies to meet the growing demand for oil, developing enhanced oil recovery projects, and emerging need to reduce global warming.

The key trends guiding the growth of the market include the rising environmental consciousness, government initiatives, and investments by market players in carbon capture and sequestration technologies.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The significant capture sources of carbon capture and sequestration, include chemicals, natural gas processing, power generation, and fertilizers production, among others.

The various services of the market, include capture, transportation, and storage.

The major end uses of the market, include enhanced oil recovery (EOR) and dedicated storage and treatment.

The major players in the market are Exxon Mobil Corporation, Carbon Engineering Ltd., Fluor Corporation, Equinor ASA, Dakota Gasification Company, and Linde plc, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Capture Source |

|

| Breakup by Service |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.