Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

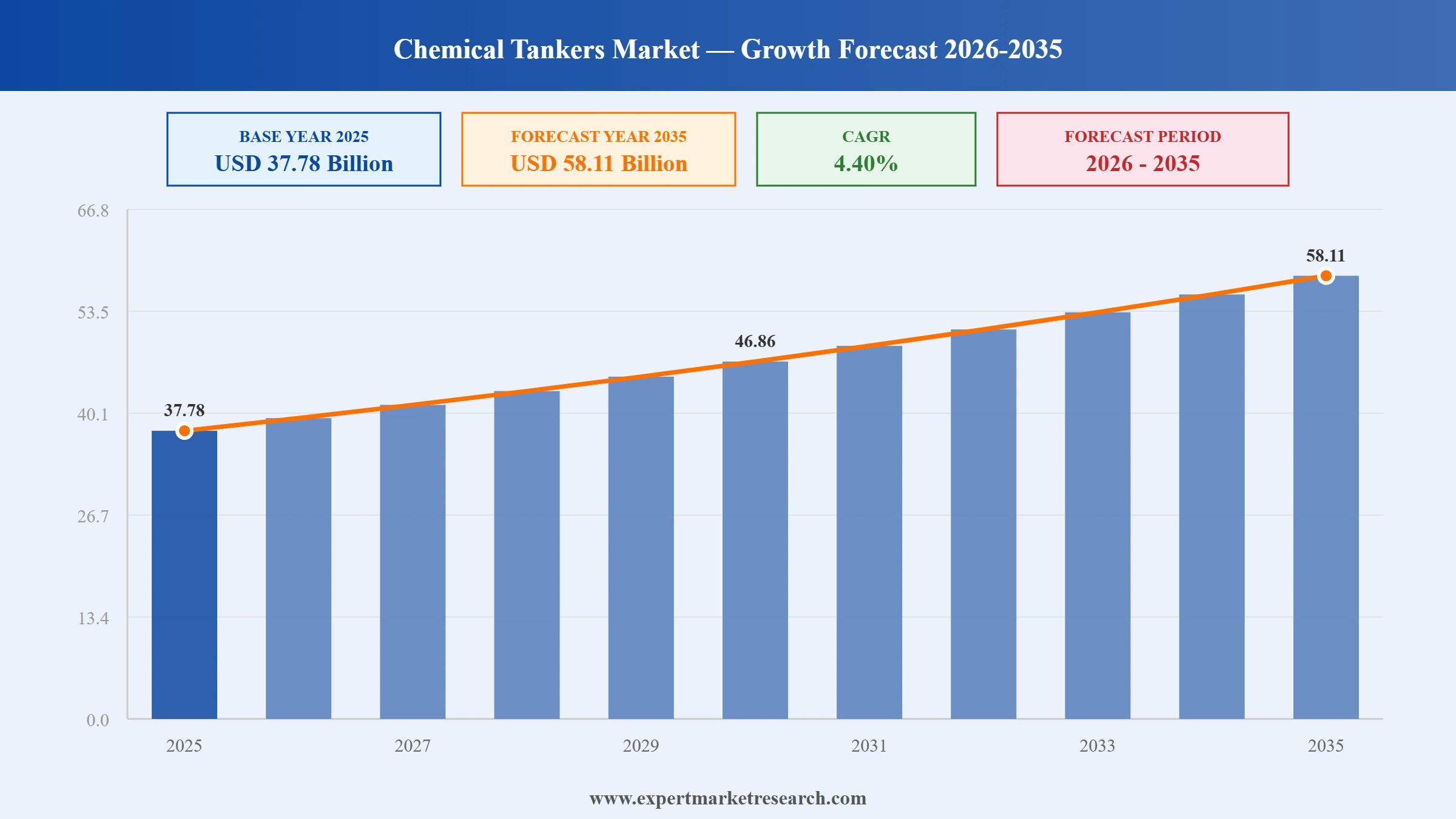

The chemical tankers market reached a value of USD 37.78 Billion at 2025 and is projected to expand at a CAGR of around 4.40% during the forecast period of 2026-2035. With growing global petrochemical trade volumes, rising demand for vegetable oil transportation, increasing adoption of eco-compliant stainless steel and coated tankers, and expanding deep-sea chemical logistics networks, the market is expected to reach USD 58.11 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The chemical tankers market is navigating a transition from an exceptional 2023-2025 earnings cycle toward a more normalised but structurally well-supported growth phase. Key themes include fleet renewal driven by IMO environmental regulations, consolidation among major parcel tanker operators, growing demand for biofuel feedstock logistics, and the integration of digital fleet management platforms. Operators are balancing capital allocation for eco-vessel investment against continued demand from the petrochemical, specialty chemical, and food-grade liquid sectors.

In March 2025, MOL Chemical Tankers announced the acquisition of Fairfield Chemical Carriers, a US-based stainless steel chemical tanker operator with an established position in North American and trans-Pacific trade lanes. The acquisition materially strengthened MOL's presence in the US Gulf Coast petrochemical export market and expanded its parcel tanker fleet by several stainless steel vessels.

In November 2025, Odfjell and Japan’s Nissen Kaiun established Odfjell Hakata Maritime, a Bergen-based joint venture initially comprising ten stainless steel chemical tankers. Odfjell Tankers acts as commercial manager. The venture projects a 12% increase in commercial trading days in 2026 versus 2025, reflecting growing demand for premium stainless steel parcel tanker capacity.

In November 2025, Odfjell’s chemical tanker Bow Olympus completed a transatlantic voyage combining wind-assisted propulsion with certified sustainable 100% biofuel, achieving near-zero GHG emissions. Real-time data confirmed the dual-propulsion approach met the 2050 FuelEU Maritime GHG intensity targets, marking a significant milestone in chemical tanker decarbonisation.

From January 2025, tightening IMO Energy Efficiency Existing Ship Index and Carbon Intensity Indicator requirements accelerated fleet renewal investment among chemical tanker operators. Stolt-Nielsen, Odfjell, and MOL committed capital to engine upgrades, hull optimisations, and new vessel orders to maintain regulatory compliance and operational competitiveness across global chemical trade routes.

Rising global petrochemical output, especially from the Middle East and the US Gulf Coast, sustains structural demand for chemical tankers. US shale feedstock advantages have expanded Gulf Coast exports significantly, fuelling chemical tankers market growth through consistent cargo volumes in organic chemical and specialty solvent trade lanes.

Global vegetable and palm oil trade is expanding rapidly, with India remaining the world's largest edible oil importer. Food-grade liquid cargo logistics require stainless steel and coated tankers meeting strict hygiene standards, supporting chemical tankers market growth through dedicated vegetable oil and fats vessel deployment on Asia-Middle East trade routes.

SAF mandates in Europe and the US require massive volumes of bio-feedstocks including used cooking oil and tallow. Transporting these feedstocks over long distances creates new cargo flows for chemical tankers, adding a structurally growing bioenergy logistics dimension that supplements traditional petrochemical and specialty chemical trade in the chemical tankers market.

Stainless steel chemical tankers earn premium freight rates by handling reactive, corrosive, or high-purity specialty chemicals requiring segregated, contamination-free tank systems. Growing pharmaceutical, fine chemical, and food-grade liquid cargo flows are increasing the commercial premium attached to stainless steel capacity within the chemical tankers market globally.

Chemical tanker operators including Stolt-Nielsen and Odfjell are deploying digital fleet management platforms covering route optimisation, predictive maintenance, and cargo documentation. Real-time vessel performance monitoring reduces fuel consumption and port turnaround times, improving cost efficiency and customer service standards in a competitive chemical tankers market.

The Expert Market Research's report titled “Chemical Tankers Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

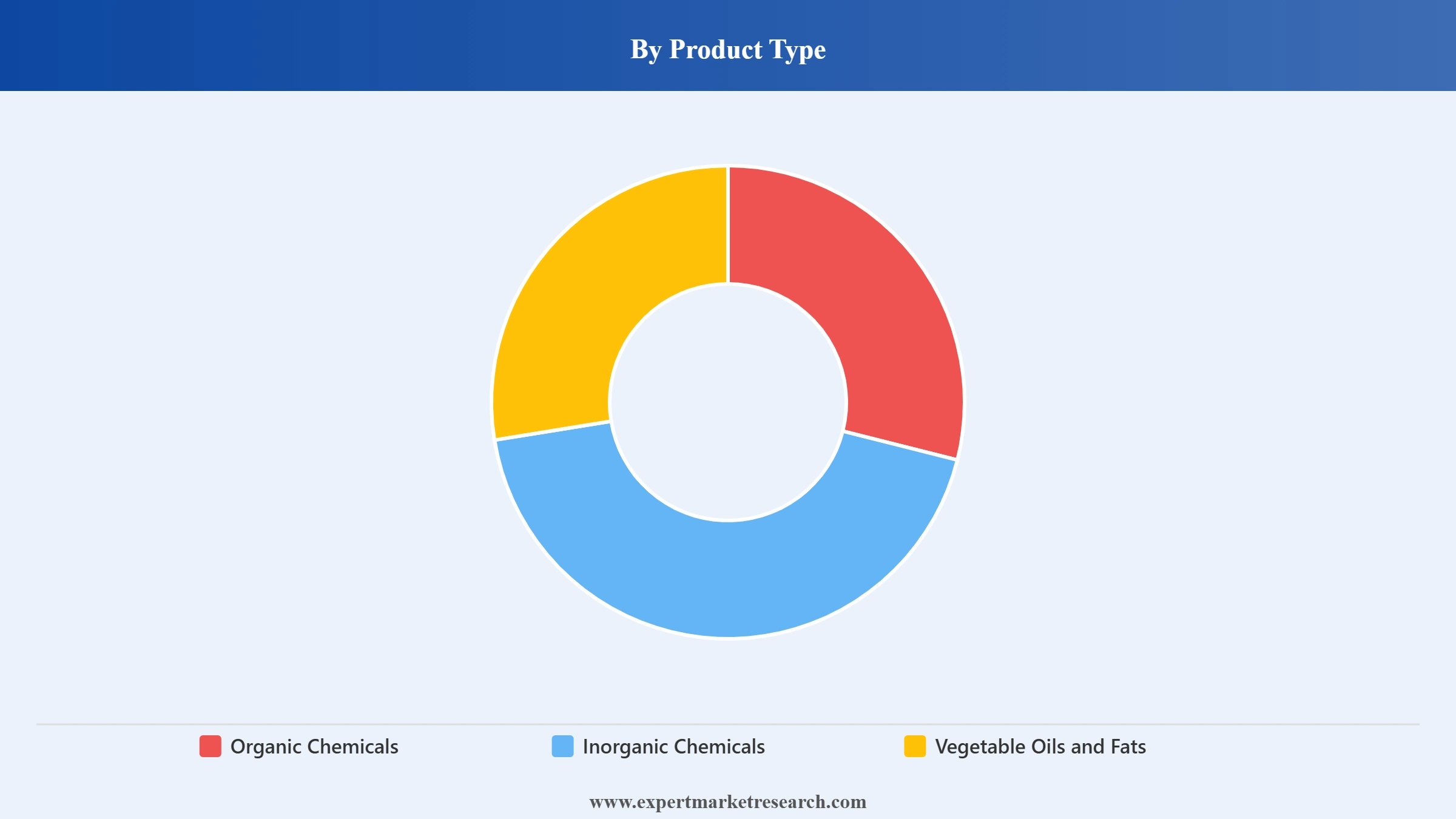

Breakup by Product Type

Key Insight: Organic chemicals dominate the chemical tankers market by cargo volume, encompassing a broad range of petrochemical intermediates, solvents, alcohols, and specialty organics transported between major chemical production hubs. Inorganic chemicals including acids and alkalis represent a smaller but technically demanding segment, requiring high-specification tank coatings. Vegetable oils and fats are the fastest-growing product type, driven by expanding global food and biofuel trade, with stainless steel and food-grade coated vessels becoming essential assets for operators serving Asia and Africa.

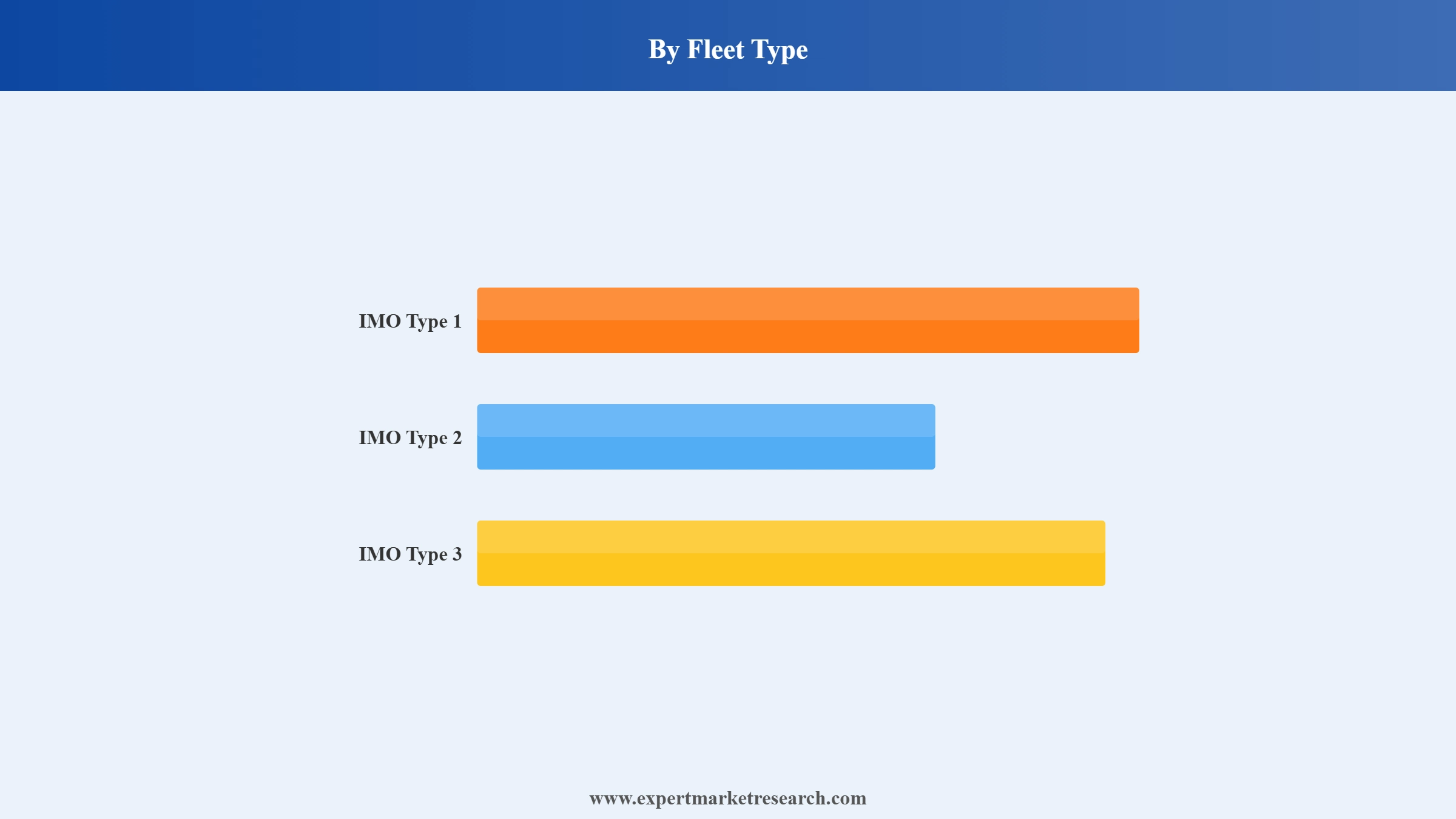

Breakup by Fleet Type

Key Insight: IMO Type 2 vessels hold the dominant fleet share in the chemical tankers market, accounting for approximately half of the global fleet by cargo-carrying capacity. Type 2 tankers carry a wide range of hazardous, toxic, and reactive chemicals in segregated tanks with high-specification coating or stainless steel lining, serving the broadest cross-section of cargo types. IMO Type 1, the most specialised category, commands premium freight rates for the most toxic cargoes. IMO Type 3 vessels serve the largest volume of less hazardous commodity chemicals and clean petroleum products.

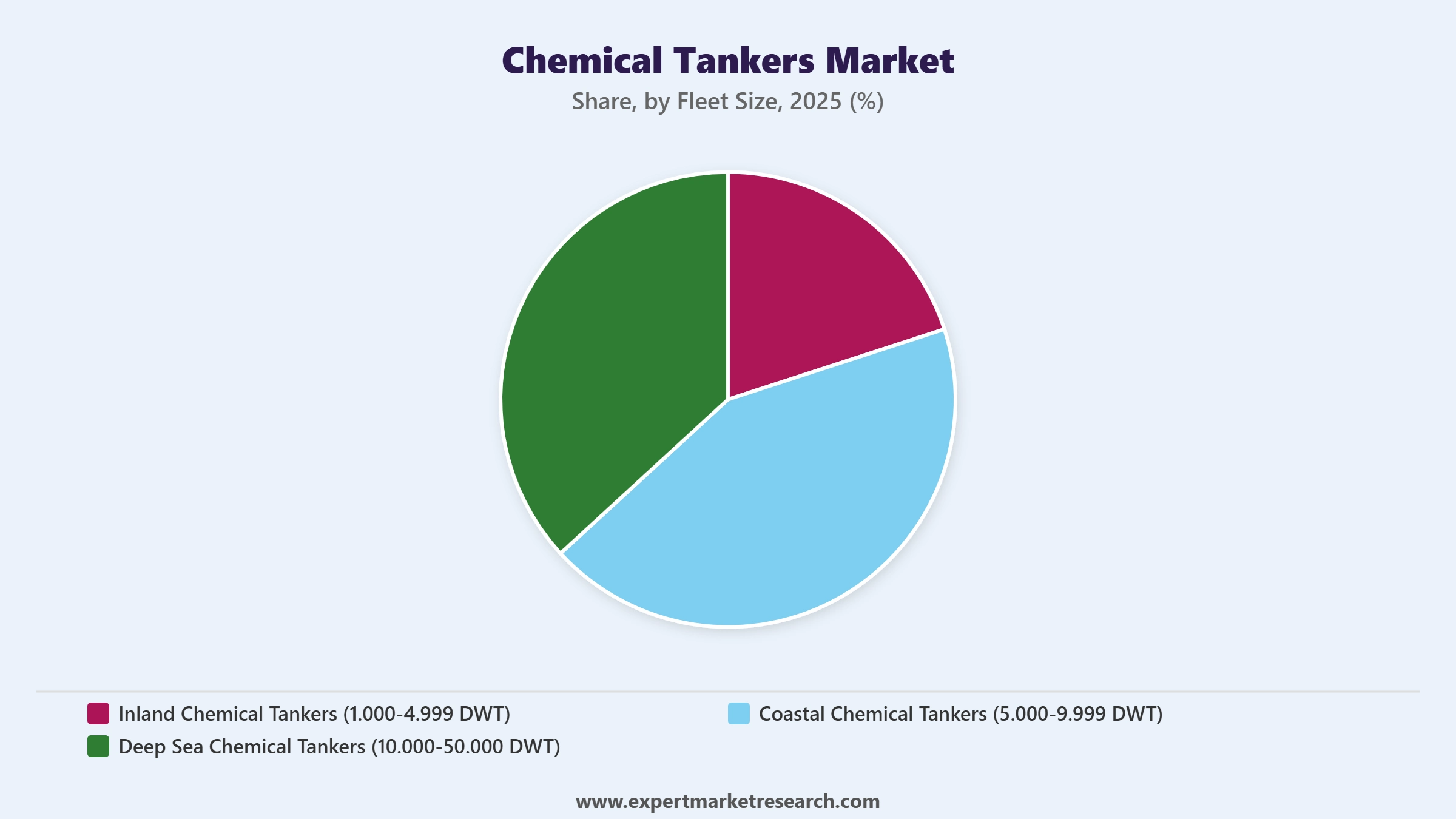

Breakup by Fleet Size

Key Insight: Deep-sea chemical tankers dominate by value in the chemical tankers market, serving long-haul intercontinental trade lanes connecting the US Gulf Coast, Europe, the Middle East, and Asia Pacific. These vessels offer the highest cargo flexibility, with multiple segregated tanks enabling parcel loading of different chemicals for different consignees on a single voyage. Coastal and inland tankers serve regional distribution networks and short-sea routes, with the coastal segment growing in Europe and Asia as chemical production clusters expand near coastal industrial zones.

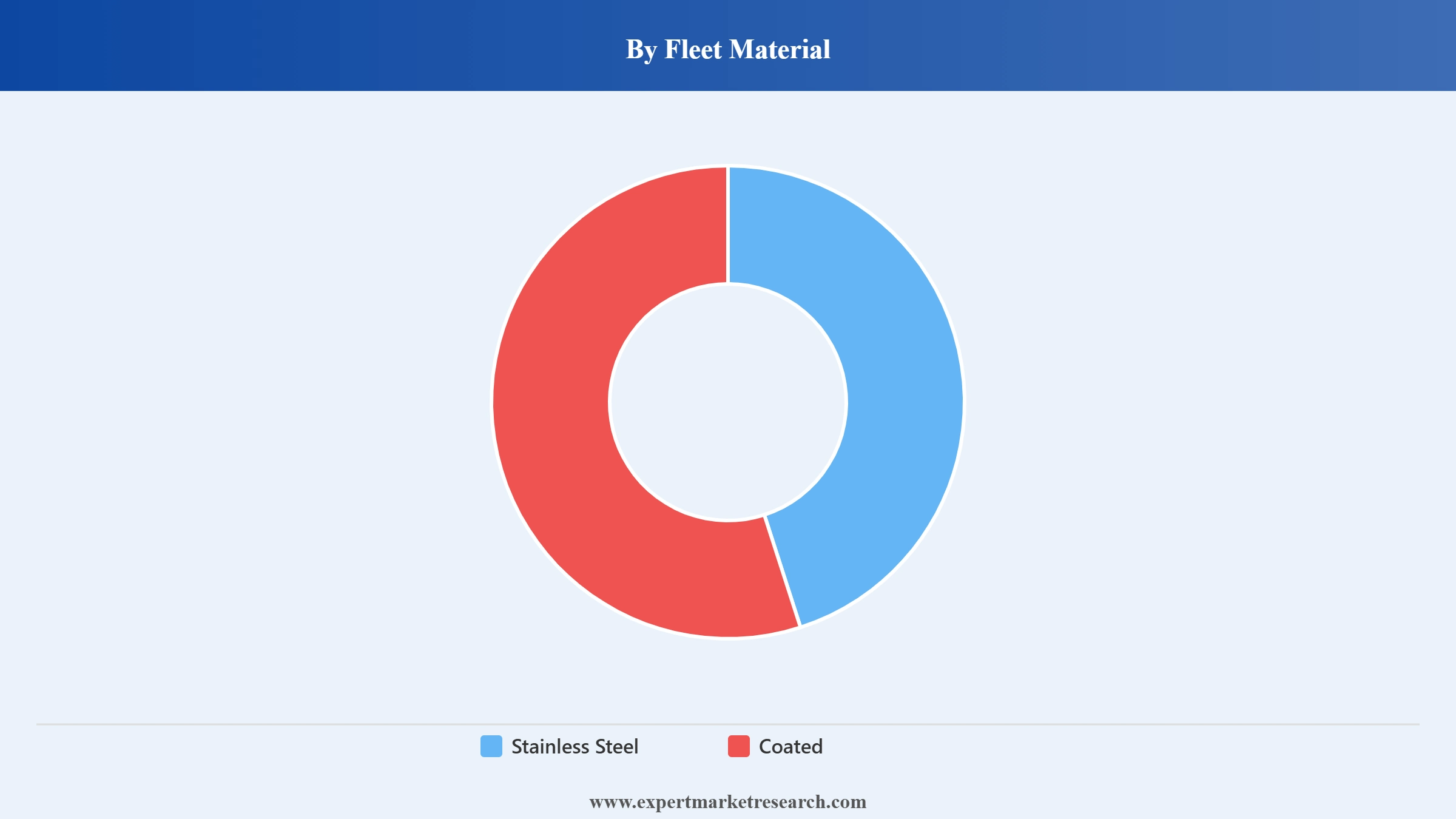

Breakup by Fleet Material

Key Insight: Stainless steel tanks command the premium segment of the chemical tankers market, enabling transport of the broadest range of high-value, reactive, and food-grade liquid cargoes without contamination risk. Their high cost is offset by higher freight rates and longer operational lifespans. Coated tankers serve a larger volume of commodity chemical cargoes at lower freight rates, supported by advances in epoxy and zinc silicate coatings that extend operational life and cargo compatibility. Both tank types are under regulatory pressure to improve energy efficiency and emissions performance.

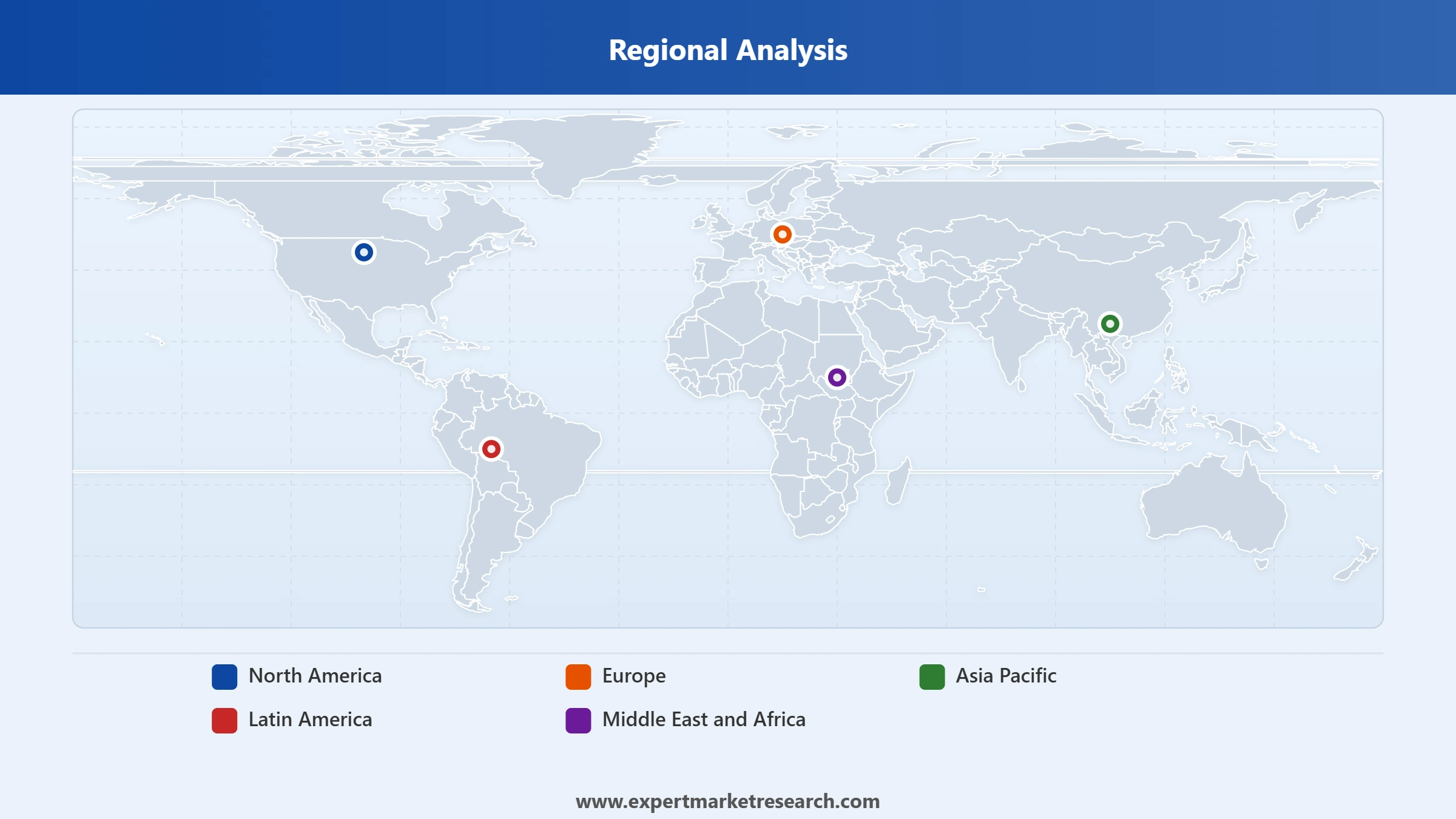

Breakup by Region

Key Insight: Asia Pacific is the largest and fastest-growing regional market in the chemical tankers market, driven by China's dominant position as both a petrochemical producer and importer, Japan's advanced chemical industry, and Southeast Asia's growing industrial chemical demand. North America benefits from US Gulf Coast petrochemical export expansion fuelled by shale-derived feedstock cost advantages. Europe maintains a mature fleet and a sophisticated chemical trade network. The Middle East is a key cargo origin for petrochemicals, while Latin America and Africa are growing destinations for chemical imports.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, organic chemicals dominate the market due to high-volume global petrochemical trade flows

Organic chemicals lead the chemical tankers market by cargo volume because they encompass the broadest range of liquid chemical products traded globally, from basic petrochemical feedstocks including benzene, toluene, and xylene to alcohols, acids, and specialty solvents. Growing chemical manufacturing output in the US, the Middle East, and China generates high and consistent cargo volumes requiring specialised tanker capacity with segregated tank systems and appropriate cargo-handling equipment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vegetable oils and fats represent the fastest-growing product segment as expanding global edible oil trade, biofuel feedstock demand, and processed food manufacturing drive cargo growth. India, the world's largest edible oil importer, generates significant bilateral trade flows that require food-grade stainless steel tank capacity. In November 2025, Odfjell's near carbon-neutral transatlantic voyage using biofuel highlighted how vegetable-derived fuels are also creating new logistics demand within the chemical tankers market.

By fleet type, IMO Type 2 accounts for the dominant share of the market due to broad cargo compatibility

IMO Type 2 vessels account for the largest fleet share in the chemical tankers market because their operational flexibility across a wide range of hazardous and non-hazardous liquid chemical cargoes makes them the most commercially versatile chemical tanker type. Their stainless steel or high-specification coated tank systems allow operators to load multiple different chemicals in segregated parcels, maximising vessel utilisation across diverse trade lanes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

IMO Type 1 tankers, while a smaller segment, command the highest freight premiums because they are the only type certified to carry the most toxic and environmentally hazardous liquid chemicals. Demand for Type 1 capacity is driven by specialty chemical producers requiring secure, compliant transport for highly toxic cargoes. Fleet renewal and regulatory compliance investment are central competitive drivers for operators maintaining Type 1-certified vessels in the chemical tankers market.

By fleet size, deep-sea chemical tankers dominate the market due to high-value intercontinental parcel trade routes

Deep-sea chemical tankers in the 10,000-50,000 DWT range lead the chemical tankers market by revenue value because they serve the highest-value long-haul trade lanes connecting the US Gulf Coast, Europe, the Middle East, and Asia Pacific. Their multiple segregated tanks enable parcel loading of different chemicals for different consignees on a single voyage, delivering the cargo flexibility that commands premium freight rates from specialty chemical shippers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Coastal and inland chemical tankers serve regional distribution networks and short-sea routes at lower freight rates, but play a critical role in connecting production hubs to consumption centres within regions. Coastal tankers are a growing segment in Europe and Asia as chemical production clusters expand near coastal industrial zones, reducing the need for deep-sea transfers and shortening supply chains in the chemical tankers market.

By fleet material, stainless steel holds a dominant premium position due to cargo versatility and hygiene standards

Stainless steel chemical tankers hold the premium commercial position in the chemical tankers market because they offer the broadest cargo compatibility, including food-grade liquids, pharmaceutical-grade solvents, and highly reactive chemicals that would corrode or contaminate epoxy-coated alternatives. Their higher construction cost is justified by superior freight rates, longer service lives, and the ability to serve high-value specialty chemical and vegetable oil cargo segments without tank cleaning restrictions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Coated tankers dominate by fleet count because their lower build cost makes them accessible to a broader range of operators serving commodity chemical and clean petroleum product trade routes. Advances in high-performance epoxy coatings have expanded cargo compatibility and reduced cleaning turnaround times, improving the commercial competitiveness of coated vessels. In March 2025, MOL Chemical Tankers' acquisition of Fairfield Chemical Carriers added stainless steel vessels to its fleet, reflecting the strategic value of premium tank material in the chemical tankers market.

Asia Pacific dominates the market due to China's petrochemical output scale and regional chemical import demand

Asia Pacific leads the chemical tankers market by shipping volume because China is simultaneously the world's largest petrochemical producer and a significant importer of specialty and commodity chemicals, generating high-density cargo flows on intra-regional and intercontinental routes. Japan's advanced chemical industry, South Korea's petrochemical exports, and Southeast Asia's growing industrial chemical imports further consolidate the region's dominant position in global chemical tanker demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is a structurally important growth market, with US Gulf Coast petrochemical export volumes expanding significantly as shale-derived ethane and natural gas feedstock cost advantages support new chemical plant capacity. In March 2025, MOL Chemical Tankers strengthened its North American position through the Fairfield Chemical Carriers acquisition, reflecting the region's growing strategic importance. Middle East export flows from Saudi Arabia and the UAE are also expanding within the chemical tankers market as new petrochemical megaprojects come online.

The chemical tankers market is moderately concentrated in the premium parcel tanker segment, with Stolt-Nielsen, Odfjell, and MOL Chemical Tankers commanding the highest-value specialty cargoes through their stainless steel fleets. The broader market is more fragmented, with regional operators serving coastal and commodity chemical routes. Competition turns on fleet quality, cargo handling expertise, route network breadth, and the ability to meet tightening IMO environmental standards.

Consolidation through joint ventures and acquisitions is reshaping the competitive structure, as demonstrated by MOL's Fairfield acquisition and the Odfjell-Nissen Kaiun joint venture. Technology adoption, digital fleet management, and decarbonisation investment are becoming differentiating factors for operators competing for high-value cargo contracts.

Saudi Arabian national shipping company founded in 1979 and headquartered in Riyadh. Bahri operates one of the world's largest chemical tanker fleets, with a diversified portfolio covering chemicals, crude oil, and bulk cargo. Its strategic alignment with Saudi Aramco and SABIC gives it privileged access to Saudi petrochemical export volumes, anchoring its commercial position in the chemical tankers market.

Norwegian-American specialty tanker operator founded in 1959, headquartered in London. Stolt-Nielsen operates the world's largest parcel tanker fleet, specialising in stainless steel chemical tankers that carry the broadest range of specialty liquid cargoes. Its integrated tank terminal and chemical logistics network differentiates it from pure fleet operators, offering end-to-end liquid chemical supply chain services globally.

Singapore-based subsidiary of Japan's Mitsui O.S.K. Lines, one of the world's largest shipping companies. MOL Chemical Tankers operates a fleet of stainless steel and coated parcel tankers serving Asia-Pacific, Middle East, and North American chemical trade routes. Its March 2025 acquisition of Fairfield Chemical Carriers significantly expanded its US Gulf Coast presence.

Norwegian chemical tanker operator founded in 1916 and headquartered in Bergen. Odfjell operates a fleet of deep-sea and regional chemical tankers alongside a network of tank terminals in key chemical hubs. Its November 2025 joint venture with Nissen Kaiun added ten stainless steel vessels, and its biofuel-powered transatlantic voyage demonstrated leadership in chemical tanker decarbonisation.

Other key players in the market are Iino Kaiun Kaisha, Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain the strategic intelligence you need to stay ahead in the global chemical tankers market with our comprehensive report for 2026. Understand the cargo type growth trajectories, fleet renewal cycles, IMO regulatory requirements, and competitive dynamics that will define the next decade. Whether you operate vessels, charter capacity, invest in maritime assets, or supply the sector, this report gives you the clarity to act decisively. Download your free sample today and explore the key opportunities in chemical tankers.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 37.78 Billion.

The market is projected to grow at a CAGR of 4.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 58.11 Billion by 2035.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Key strategies driving the market include fleet modernization with eco-friendly vessels, expanding capacity through newbuilds, focusing on specialized tankers for diverse chemicals, adopting digital technologies for operational efficiency, strengthening safety and environmental compliance, and forming strategic partnerships to access emerging markets and optimize global trade routes.

The growing research and development activities by the major manufacturers aimed towards designing superior quality tankers complying with the cleaning standards of the government are likely to be the key trends in the market.

Organic chemicals, inorganic chemicals, and vegetable oils and fats, among others, are the different product types of chemical tankers.

IMO type 1, IMO type 2, and IMO type 3 are the major fleet types of chemical tankers.

Inland chemical tankers (1,000-4,999 DWT), coastal chemical tankers (5,000-9,999 DWT), and deep sea chemical tankers (10,000-50,000 DWT) are the significant fleet sizes of chemical tankers.

Stainless steel and coated are the significant fleet materials based on which the market has been bifurcated.

The key players in the market report include Bahri, Stolt-Nielsen Limited (SNL), Mol Chemical Tankers Pte. Ltd., Odfjell SE, and Iino Kaiun Kaisha, Ltd., among others.

Asia Pacific is the most dominating segment in the market, driven by rapid industrialization, urbanization, and growing demand for chemicals in manufacturing, pharmaceuticals, and agriculture.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Fleet Type |

|

| Breakup by Fleet Size |

|

| Breakup by Fleet Material |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.