Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

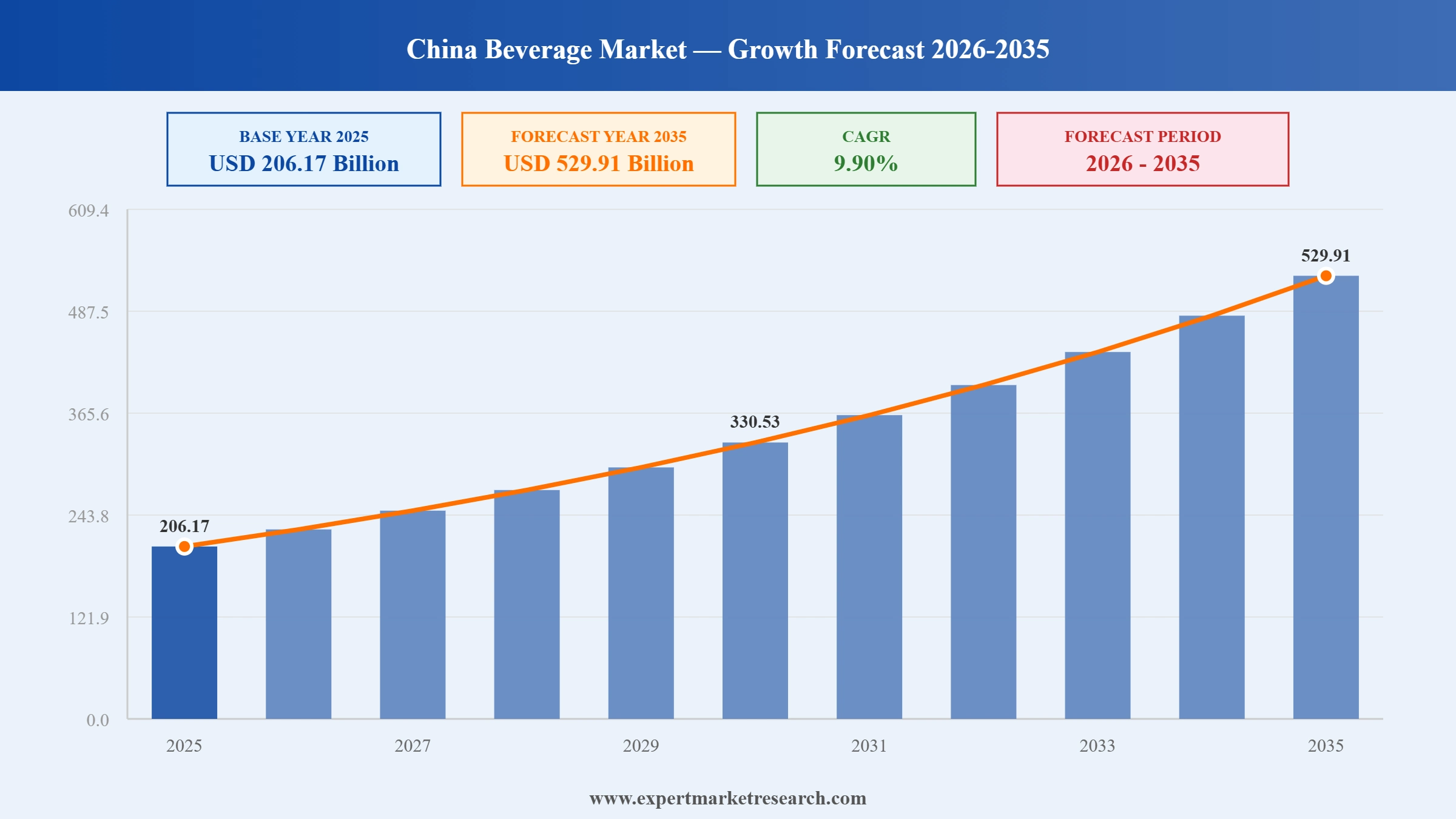

The China Beverage Market reached a value of USD 206.17 Billion at 2025 and is projected to expand at a CAGR of around 9.90% during the forecast period of 2026-2035. With growing demand for functional and health-focused beverages, the accelerating shift of younger consumers toward premium and craft products, rapid expansion of e-commerce and digital retail channels, and the integration of smart vending and AI-powered retail technology, the market is expected to reach USD 529.91 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

China Beverage Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

206.17 |

|

Market Size 2035 |

USD Billion |

529.91 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

9.90% |

|

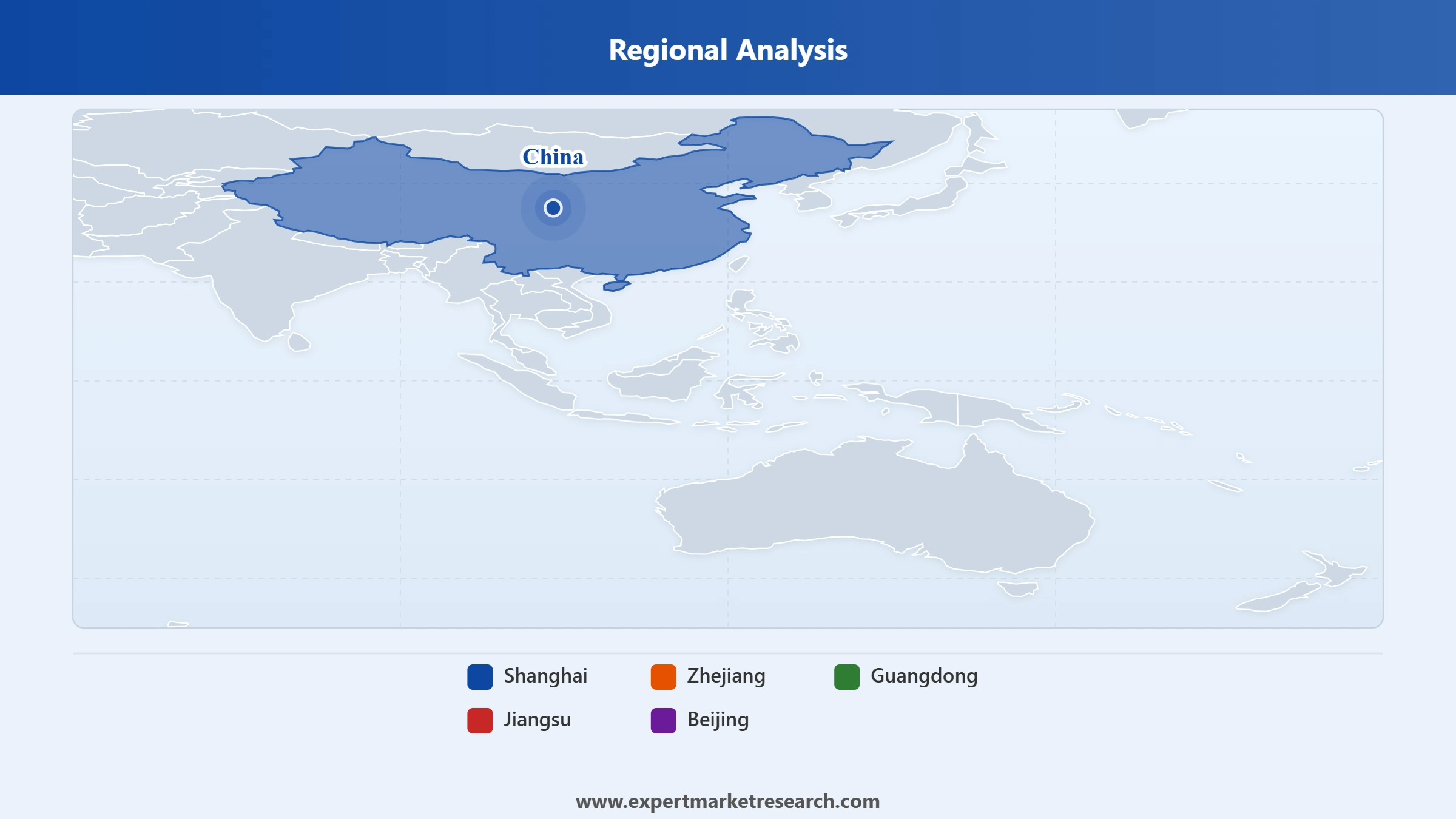

CAGR 2026-2035- Market by Region |

Zhejiang |

11.9% |

|

CAGR 2026-2035- Market by Product Type |

Non-Alcoholic Beverages |

10.9% |

|

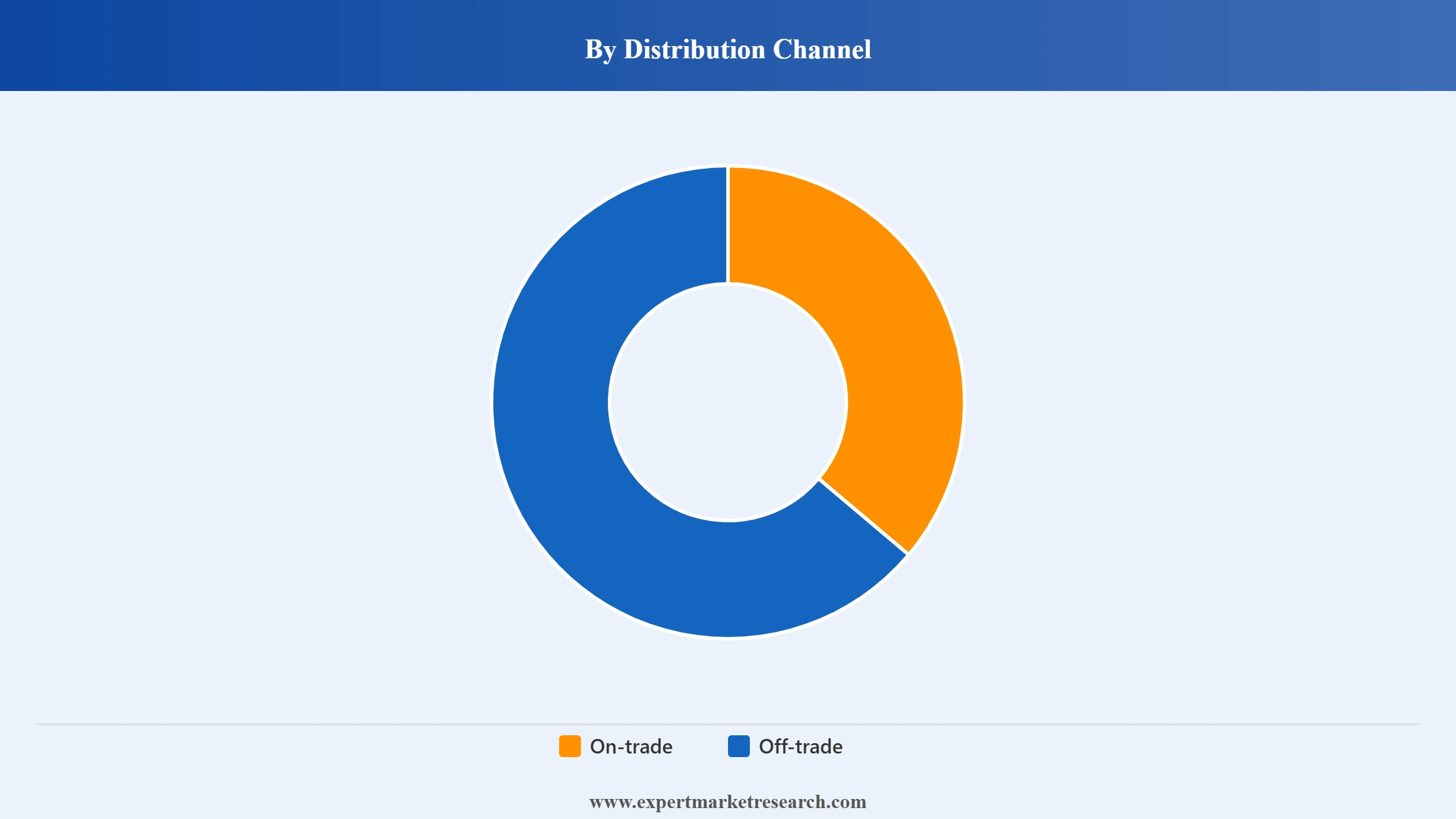

CAGR 2026-2035- Market by Distribution Channel |

Off-Trade |

11.1% |

The China Beverage Market is undergoing a structural shift shaped by health-conscious consumption, digital retail transformation, and premiumisation trends. Rising incomes, an increasingly aspirational middle class, and the influence of social media-driven product discovery are redefining what Chinese consumers want to drink, and how and where they buy it.

In November 2024, Budweiser APAC, the China-focused arm of Belgian beer giant Anheuser-Busch InBev, unveiled a portfolio of premium zero-sugar and alcohol-free products in the Chinese market. The release included Harbin IGD Zero Sugar, Budweiser Zero, and Corona Cero, directly targeting health-conscious younger consumers who are increasingly moderating or abstaining from alcohol. The move reflects AB InBev's strategic pivot toward the low-and-no alcohol category in China, as the company seeks to maintain revenue growth even as traditional beer volume consumption among the youth demographic faces headwinds.

In September 2025, PepsiCo introduced a range of plant-based functional beverages in China, aimed at the country's rapidly growing segment of health and vegan-oriented consumers. The move diversifies PepsiCo's China portfolio beyond traditional carbonated and energy drinks, entering a niche that has seen sustained growth in recent years as Chinese urban consumers increasingly seek cleaner-label, ingredient-transparent alternatives. The launch also positions PepsiCo to compete more directly with emerging Chinese domestic brands in the premium functional beverage space.

In August 2024, The Coca-Cola Company partnered with Oreo, the globally recognised snack brand owned by Mondelez International, to introduce a limited-edition Coca-Cola Oreo Zero Sugar beverage in the Chinese market. The product features a distinctive design combining Oreo cookie and Coca-Cola bottle imagery and delivers a cola-Oreo flavor fusion. This launch underscores Coca-Cola's strategy of using co-branding and cross-category collaboration to generate excitement in an increasingly competitive beverage landscape, while responding to China's growing preference for zero-sugar carbonated drinks.

In August 2024, Danone China introduced Mizone Electrolyte+, a grapefruit-flavored electrolyte drink targeting active urban consumers seeking functional hydration solutions. Built on a coconut water base, the product contains 455 mg of five essential electrolytes including potassium, calcium, sodium, magnesium, and chloride. The launch directly capitalises on surging Chinese consumer interest in sports and recovery beverages, positioning Danone competitively in a segment where international and domestic players are rapidly expanding their functional portfolio to meet a health-driven demand wave.

In July 2024, the China Beverage Industry Association (CBIA) officially endorsed and published a new group standard specifically governing the production, composition, and labelling of electrolyte beverages. This regulatory milestone is designed to bring uniformity, safety, and product quality benchmarks to a segment that has experienced explosive growth with limited formal oversight. For market participants, the standard creates both compliance obligations and a credibility-building opportunity, as brands meeting the specification can differentiate their products in an increasingly crowded functional beverage category.

Demand for beverages that deliver demonstrable health benefits, from electrolyte replenishment and gut health to cognitive enhancement, is reshaping the product innovation landscape in China. The trend is closely linked to rising health consciousness post-pandemic, urbanisation-driven lifestyle stress, and growing consumer willingness to pay premium prices for perceived wellness outcomes. In July 2024, the China Beverage Industry Association published a new group standard for electrolyte beverages, formalising the category and signalling regulatory recognition of functional drinks as a mainstream product segment within the broader China Beverage Market growth trajectory.

Chinese beer consumers, particularly those aged 18-35 in urban centres, are moving away from traditional standard lagers toward premium craft offerings and alcohol-moderation products. This shift has prompted global brewers to launch premium and zero-alcohol variants specifically for the China market. In November 2024, Budweiser APAC launched zero-sugar and alcohol-free variants including Harbin IGD Zero Sugar and Budweiser Zero in China, marking a significant acknowledgment from the world's largest brewer that Chinese consumption patterns are undergoing a genuine structural change rather than a temporary dip.

Offline channels continue to dominate Chinese beverage sales at roughly 90% of total volume, but online platforms are growing at a substantially faster pace, driven by livestreaming commerce, social media promotions, and same-day delivery infrastructure. Brands that effectively leverage platforms such as Douyin, Taobao, and JD.com are accessing consumers beyond the reach of traditional retail networks. In 2024, China's beverage-related livestreaming sales surged by over 65%, according to a United States Department of Agriculture Foreign Agricultural Service analysis of the Chinese beverage market, underscoring how dramatically digital channels are reshaping distribution for all beverage categories.

Global brands operating in China are learning that long-term success requires more than importing bestselling formats from other markets. Localised flavour innovation, heritage-inspired ingredients, and culturally resonant packaging are becoming essential differentiation tools. In 2024, Coca-Cola ranked at the top of the IMD China Company Transformation Indicator for the food and beverage sector, with analysts specifically crediting its ability to develop flavours tailored to the Chinese palate and deploy agile product pipelines that respond quickly to shifts in local consumer preference as the primary drivers of its competitive performance.

The Expert Market Research's report titled "China Beverage Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

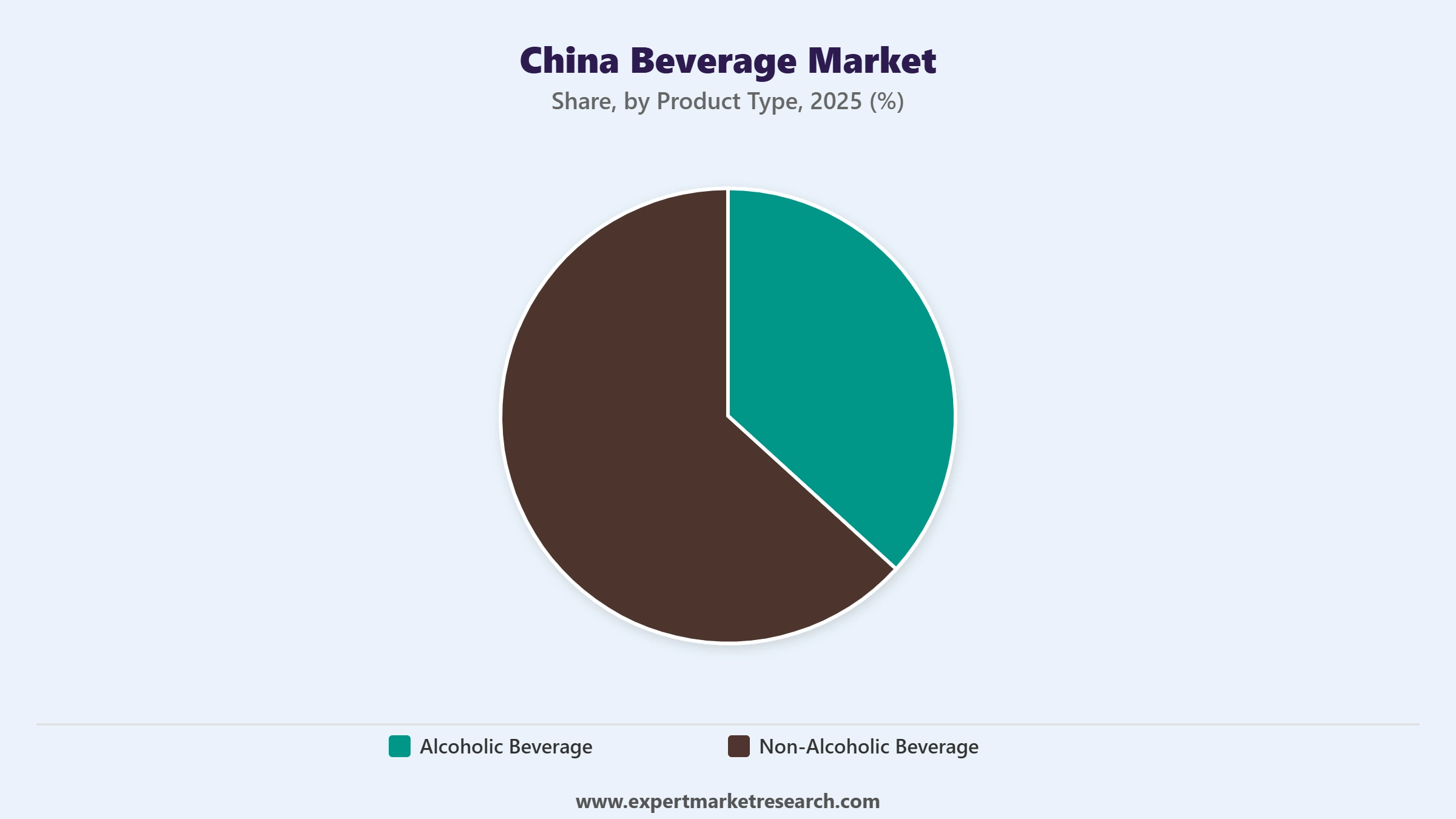

Key Insight: Non-Alcoholic Beverages hold the largest and fastest-growing share of the China beverage market, projected to expand at a CAGR of 10.9% through 2035. RTD teas and coffees have emerged as a particularly dynamic subcategory, with ready-to-drink tea surpassing carbonated soft drinks to become the second-largest subcategory by volume in China for the first time in 2024, according to USDA Foreign Agricultural Service data. Bottled water remains the category's anchor by volume. Within alcoholic beverages, spirits (notably baijiu) still generate the highest revenue, though beer premiumisation and the growth of low-and-no alcohol variants are driving category realignment. Brands including Wahaha, Nongfu Spring, Coca-Cola China, and PepsiCo are actively investing in portfolio diversification to capture this structural shift.

Market Breakup by Distribution Channel

Key Insight: The Off-Trade channel dominates China's beverage distribution and is set to grow at a CAGR of 11.1% over the forecast period, outpacing the On-Trade segment. Supermarkets and hypermarkets continue to anchor the off-trade segment given their wide geographic reach and product assortment. However, convenience stores have become increasingly important in urban tier-one and tier-two cities as consumers seek immediate purchase options. E-commerce within the "Others" off-trade subcategory is the most disruptive growth driver, with platforms leveraging livestreaming, influencer marketing, and rapid logistics to capture impulse and repeat purchases. Offline channels still account for roughly 90.6% of total beverage sales in China, but online is growing at multiples of the overall market rate.

Market Breakup by Region

Key Insight: Zhejiang is projected to be the fastest-growing regional market at an 11.9% CAGR, supported by its historically strong tea culture, a prosperous consumer base in Hangzhou and Ningbo, and a local preference for functional teas and herbal beverages. Shanghai serves as the market's premium and innovation hub, with demand for international brands, craft beverages, and specialty coffee concentrated among its affluent, cosmopolitan consumer base. Guangdong, with economic powerhouses Guangzhou and Shenzhen, is a strong contributor to RTD and energy drink volumes, given the region's young, fast-paced urban workforce. Jiangsu benefits from rising health consciousness and a growing middle class in Nanjing and Suzhou driving demand for low-sugar and premium packaged options. Beijing anchors the northern market with steady demand growth through digital food delivery and expanding workplace coffee culture.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Non-Alcoholic Beverages hold the dominant share of the China beverage market by product type, with bottled water and RTD tea together accounting for a substantial majority of volume. The structural advantage of the non-alcoholic segment lies in its versatility across age groups and occasions, its alignment with health and wellness trends, and its resilience to discretionary spending pressures. Companies including Wahaha, Nongfu Spring, and Coca-Cola China have built their China beverage dominance primarily on non-alcoholic product lines. Bottled water's growth has been sustained by urbanisation, food safety concerns, and the premiumisation of water as a functional or mineral-enriched product. RTD Tea and Coffee have surged as younger Chinese consumers shift away from sugary carbonates toward lighter, functional alternatives. Hangzhou Wahaha Group and Tingyi remain the most widely distributed domestic players in these subcategories.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the distribution channel segmentation, Off-Trade dominates with the vast majority of total beverage sales, and within it, Supermarkets and Hypermarkets hold the largest share due to breadth of assortment and nationwide footprint. However, convenience stores have experienced a notable share gain, particularly in tier-one city neighborhoods where rapid urban density and commuter-driven purchase occasions favor immediate-access formats. The on-trade channel, while smaller in volume share, commands premium pricing and is growing steadily as China's dining out, cafe, and hotel and restaurant industry spend recovers. For international players such as Nestle, PepsiCo, and Suntory, off-trade supermarket and convenience channel partnerships remain the primary revenue channel, while their on-trade foodservice relationships support brand positioning and trial generation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Shanghai stands as the most commercially sophisticated beverage market in China, characterised by some of the highest per-capita spending on premium beverages globally. The city's international population and globally mobile consumer base generate sustained demand for imported wines, specialty coffee, craft beers, and premium functional drinks. Domestic and international brands consistently use Shanghai as their China innovation laboratory, launching new products and formats here before rolling out nationally. The city's advanced e-commerce penetration and cafe culture have made it a critical battleground for brands competing in the RTD coffee, plant-based, and low-alcohol categories. Investment in cold chain logistics and modern trade infrastructure in the Shanghai metropolitan area has further strengthened off-trade distribution efficiency, reinforcing the region's role as a premium volume contributor.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Guangdong, encompassing Guangzhou and Shenzhen, is the largest provincial beverage consumption market by volume in China, owing to its population density, economic output, and young working-age demographic profile. The province's appetite for energy and sports drinks, high-end teas, and packaged fruit juices reflects both the health-oriented preferences of its young urban workforce and the region's deep cultural connection to tea. The Pearl River Delta's manufacturing and logistics infrastructure supports both production and rapid product distribution across southern China and beyond. The on-trade segment in Guangdong is particularly robust given the region's vibrant restaurant, hospitality, and nightlife ecosystem, making it a priority market for global brands including Anheuser-Busch InBev, Suntory, and Coca-Cola as they compete for share in both mainstream and premium tiers.Competitive Landscape

The China Beverage Market exhibits a highly competitive and fragmented structure, with global multinationals competing alongside powerful domestic incumbents and an expanding wave of digitally native challenger brands. Market competition centers on product innovation, digital marketing agility, cold chain and distribution reach, and the ability to localise offerings for regional Chinese tastes. Premium positioning, health and wellness credentials, and sustainability commitments have become increasingly important competitive differentiators, particularly among younger urban consumers.

Global players including Coca-Cola, PepsiCo, Nestle, and Anheuser-Busch InBev compete on brand equity, international product pipelines, and distribution scale, while domestic powerhouses such as Wahaha and Hainan Laizhi leverage deep local consumer trust, established distribution networks, and stronger adaptability to regional flavour preferences. The landscape is further animated by Suntory's growing China presence and Red Bull's commanding position in the energy drinks segment.

Founded in 1866 and headquartered in Vevey, Switzerland, Nestle operates a wide beverage portfolio in China spanning coffee (Nescafe), bottled water, and dairy-based drinks. The company's understanding of Chinese consumption occasions and its investment in localised product development have supported steady market share maintenance across several beverage categories. Nestle's coffee business has benefited from China's rapidly expanding cafe and at-home coffee culture, with the brand investing in both retail formats and foodservice channels.

Established in 1898 and headquartered in Purchase, New York, United States, PepsiCo operates a diversified beverage and snack portfolio in China. Beyond its flagship carbonated brands, PepsiCo has invested in tea, energy, and functional beverage lines to align with China's health trends. Its extensive bottling and distribution network across major Chinese cities, combined with digital marketing partnerships with leading platforms, positions the brand strongly in both on-trade and off-trade channels. The company's September 2025 plant-based functional beverage launch underscores its ambition to grow in the fast-moving health beverage space.

Founded in 1892 and headquartered in Atlanta, United States, Coca-Cola ranks as the leading foreign beverage brand in China by consumer recognition and distribution breadth. The company has invested heavily in localised flavour innovation, zero-sugar product lines, and cross-brand collaborations to sustain relevance among younger Chinese consumers. Coca-Cola topped the 2024 IMD China Company Transformation Indicator for the food and beverage sector, with its agile product pipeline and China Policy Power cited as key competitive strengths. Its portfolio spans carbonates, water, tea, coffee, and energy drinks.

Founded in 1977 and headquartered in Leuven, Belgium, AB InBev operates China's largest beer business through brands including Budweiser, Harbin, and Corona. The company has pivoted strategically toward premium, craft, and low-or-no alcohol variants to address evolving Chinese consumer preferences. In November 2024, it launched zero-sugar and alcohol-free variants for the China market, demonstrating its responsiveness to health-driven demand shifts. AB InBev's Budweiser APAC structure enables focused China-market decision-making and investment prioritisation.

Other key players in the market are Suntory Holdings Limited, Red Bull GmbH, Hainan Laizhi Industry Co., Ltd., Hangzhou Wahaha Group Co. Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Tap into the latest intelligence on the China Beverage Market 2026 with our comprehensive research report. Whether you are assessing entry into China's non-alcoholic drink space, evaluating premium beer brand strategy, or identifying the fastest-growing regional opportunities, this report gives you the data and insight to move with confidence. From functional drink trends to off-trade distribution dynamics, everything you need is here. Download your free sample today and explore the opportunities shaping China's thriving beverage industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China beverage market reached an approximate value of USD 206.17 Billion.

The market is projected to grow at a CAGR of 9.90% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 529.91 Billion by 2035.

Key strategies driving the market include focusing on digital-first launches, co-developing region-specific SKUs, piloting AI-driven retail formats, enhancing packaging sustainability, and partnering with TCM innovators.

The key challenges are fragmented regional tastes, complex regulatory landscape, volatile ingredient pricing, and short product lifecycles.

The major regions in the market are Shanghai, Zhejiang, Guangdong, Jiangsu, Beijing, and others.

The various product types considered in the market report are alcoholic beverages and non-alcoholic beverages.

The various distribution channels considered in the market report are on-trade and off-trade.

The major players in the market are Nestle S.A., PepsiCo Inc., Coca-Cola Co., Anheuser-Busch Inbev SA, Suntory Holdings Limited, Red Bull GmbH, Hainan Laizhi Industry Co., Ltd., and Hangzhou Wahaha Group Co. Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.