Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The China Used Car Market reached a value of USD 250.29 Billion at 2025 and is projected to expand at a CAGR of around 7.60% during the forecast period of 2026-2035. With accelerating urbanization driving replacement vehicle demand, government-backed trade-in subsidy schemes injecting newer inventory into the market, rapid growth of online transaction platforms, and formalization of the sector through organized dealerships and certified pre-owned programs, the market is expected to reach USD 520.67 Billion by 2035.

Compound Annual Growth Rate

7.6%

Value in USD Billion

2026-2035

| China Used Car Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 250.29 |

| Market Size 2035 | USD Billion | 520.67 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.60% |

| CAGR 2026-2035 - Market by Region | Southwestern China | 8.7% |

| CAGR 2026-2035 - Market by Region | Northwestern China | 8.1% |

| CAGR 2026-2035 - Market by Vendor Type | Organized | 8.4% |

| CAGR 2026-2035 - Market by Sales Channel | Online | 10.3% |

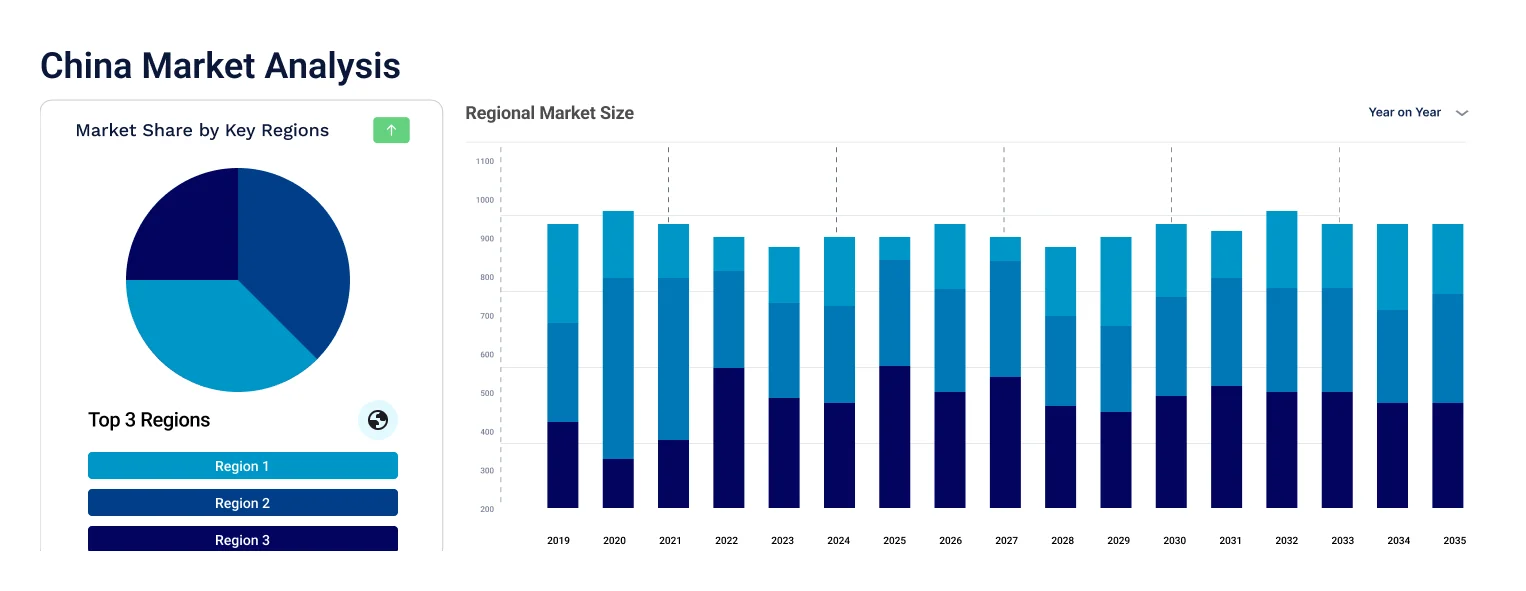

| 2025 Market Share by Region | Southwestern China | 12.2% |

China's used car market is undergoing a fundamental structural transformation, with government incentive programs, digital platform dominance, the rising volume of nearly-new electric vehicles, and the formalization of organized dealerships collectively reshaping how pre-owned vehicles are bought and sold across the country.

Data from the China Automobile Dealers Association (CADA) released in January 2026 showed that second-hand vehicle transactions across China reached 18.24 million units from January to November 2025, growing 2.95% year on year. The total transaction value for the period reached CNY 1.17 trillion. The data revealed that cars aged three to six years accounted for the largest share of transactions, reflecting the impact of trade-in incentives and shorter replacement cycles among urban consumers. Digital platforms and short-video commerce emerged as the leading information channels for younger buyers in this period.

In the second quarter of 2025, Uxin Ltd. reported retail revenues of approximately RMB 607.6 million (around USD 84.8 million), representing an 87% increase compared to the same period in 2024. The company's omnichannel superstore model, which blends physical showrooms with app-based transactions, drove this growth by providing buyers with a combination of vehicle inspection experiences and digital convenience. Uxin's performance demonstrates the commercial effectiveness of the hybrid online-offline retail format, which is becoming the dominant transaction model in China's organized used car segment

In 2025, Haier, a major Chinese consumer electronics and appliances conglomerate, acquired a stake in Autohome Inc., one of China's leading automotive information and transaction platforms. The move signals a broader strategic convergence between smart home technology and automobile data ecosystems, with Haier positioning itself to harvest valuable automotive purchase behavior data from Autohome's established user base. For China's used car market, this development underlines the increasing role of data-driven platforms in shaping consumer decision-making and dealer inventory management, a trend expected to intensify through the forecast period.

In April 2024, the Chinese government announced the operational details of its used car trade-in program, offering consumers subsidies of up to USD 1,380 when exchanging older vehicles for newer or more efficient alternatives. The scheme was designed to remain active through end of 2025 and has had a dual effect on the market: stimulating transaction volume by incentivizing upgrades, and simultaneously releasing a wave of newer pre-owned vehicles into the supply chain. This policy-driven inventory expansion is improving the quality composition of China's used car stock, attracting buyers who were previously hesitant about second-hand vehicle condition.

In 2024, Wang Xiaoyu, co-founder of Guazi (China's leading C2C used car marketplace), publicly called for the establishment of unified inspection and evaluation standards across China's used car platforms, alongside stronger service guarantees for buyers. Operating in over 200 cities nationwide, Guazi's advocacy reflects the sector's maturation challenge: growing transaction volumes are running ahead of standardized quality assurance frameworks, creating buyer uncertainty, particularly in online-first markets. This push for standardization is expected to reshape competitive positioning among platforms, where transparency and warranty offerings are becoming critical trust differentiators.

China's government trade-in scheme, announced in April 2024 with subsidies of up to USD 1,380 per qualifying exchange, has simultaneously stimulated buyer demand and injected newer inventory into the used car supply chain. Consumers upgrading to newer vehicles are releasing earlier-generation cars into the pre-owned market at an accelerated pace, improving stock quality and reducing the average age of vehicles available for resale. This policy has been particularly effective in urban markets, where shorter replacement cycles and higher affordability create faster inventory turnover that supports overall China used car market growth.

Online used car platforms have crossed a structural threshold in China, becoming the primary transaction channel for a growing majority of buyers, especially those under 35. From January to November 2025, transaction data confirmed that digital channels are dominating both information search and final purchase processes. Approximately 72% of buyers sourced vehicle information through automotive apps, while 64% relied on short-form video platforms before making purchasing decisions. Models that combine online browsing and ordering with offline test drives and seven-day return policies have resolved the trust barriers that previously limited digital adoption in vehicle transactions.

The formalization of China's used car market is accelerating. Organized vendors held approximately 63% of market share in 2025 and are growing at over 10% annually, widening the gap over fragmented, independent dealers. Scale advantages in inventory financing, AI-based vehicle appraisals, and extended warranty programs allow organized platforms to deliver a noticeably superior customer experience. Government crackdowns on odometer fraud and incomplete ownership documentation are disproportionately burdening unorganized operators, compressing their margins and pushing smaller dealers toward peripheral markets or forced consolidation.

A notable structural shift is under way as nearly-new electric and hybrid vehicles begin entering China's used car market in meaningful numbers for the first time. As replacement cycles shorten, early NEV adopters are trading in their first-generation electric vehicles, creating a supply of relatively young, technology-equipped used EVs. Battery health certification programs and standardized residual-value frameworks are emerging to support buyer confidence in this segment. Fintech solutions embedding EV-specific loan structures are also reducing financing barriers, unlocking a new wave of younger urban buyers who see nearly-new EVs as accessible and technologically relevant alternatives to new car purchases.

The EMR’s report titled “China Used Car Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Vehicle Type

Key Insight: SUVs represent the dominant vehicle type in China's used car market, reflecting the broader popularity of the segment in China's overall automotive market where consumer preferences have shifted decisively toward utility vehicles over the past decade. As new SUV ownership has grown, a corresponding inventory of used SUVs has entered the secondary market, providing buyers with greater choice across a range of budgets and specifications. Sedans maintain the second-largest share, supported by their prevalence in older vehicle cohorts and strong demand from price-sensitive buyers in Tier 3 and 4 cities. Hatchbacks appeal primarily to urban first-time buyers who prioritize maneuverability and fuel efficiency at lower price points.

Market Breakup by Vendor Type

Key Insight: Organized vendors held approximately 63% of China's used car market in 2025 and are growing at a CAGR exceeding 10% per year, driven by advantages in digital integration, inventory financing, and certified pre-owned service offerings. Their ability to deploy AI-based vehicle appraisals, provide extended warranties, and integrate financing options gives them a compelling advantage over independent dealers who rely on localized buyer relationships and lower overhead models. Unorganized vendors, while still present, are losing share as government fraud-prevention regulations and growing consumer preference for certification-backed purchases erode the trust advantages that proximity and price flexibility once provided.Organized vendors held approximately 63% of China's used car market in 2025 and are growing at a CAGR exceeding 10% per year, driven by advantages in digital integration, inventory financing, and certified pre-owned service offerings. Their ability to deploy AI-based vehicle appraisals, provide extended warranties, and integrate financing options gives them a compelling advantage over independent dealers who rely on localized buyer relationships and lower overhead models. Unorganized vendors, while still present, are losing share as government fraud-prevention regulations and growing consumer preference for certification-backed purchases erode the trust advantages that proximity and price flexibility once provided.

Market Breakup by Fuel Type

Key Insight: Gasoline-powered used vehicles continue to dominate China's second-hand market by volume, reflecting the large base of internal combustion engine cars that entered the market over the past two decades. Petrol variants maintain significant share given their affordability and widespread service infrastructure. The Hybrid/Electric segment is the fastest-growing fuel type, supported by shortening replacement cycles among early NEV adopters and government battery health certification programs that are building consumer confidence in second-hand electric vehicles. Diesel used vehicles serve primarily commercial and logistics buyers, maintaining stable demand in Northeast and North China where heavy-duty use cases persist.

Market Breakup by Sales Channel

Key Insight: Offline channels, including organized dealerships, auction houses, and physical superstore formats, retained a 32.18% share of transactions in 2025, underpinned by consumers who value direct vehicle inspection, test drives, and face-to-face negotiation. However, online channels are expanding rapidly, with platforms like Guazi, Uxin, and Autohome using AI-driven pricing, verified ownership histories, and hybrid purchase models to capture growing buyer confidence. The online CAGR of approximately 10.3% through the forecast period significantly outpaces offline growth, pointing to a progressive rebalancing of transaction volume toward digital-first or omnichannel formats.

Market Breakup by Region

Key Insight: East China is the clear regional leader, accounting for 33.29% of the total used car market in 2025, driven by its large urban population, high vehicle ownership rates, and well-developed dealer ecosystem across cities including Shanghai, Hangzhou, and Nanjing. Southcentral China follows, supported by major manufacturing and commerce centers where rising incomes are accelerating vehicle replacement cycles. Southwestern China is emerging as a high-growth region, with urbanization momentum and government infrastructure investment driving consumer purchasing power and vehicle demand. North China and Northeast China, historically strong in industrial vehicle use, are contributing stable volumes as gasoline and diesel used commercial vehicles retain relevance in those markets.

| CAGR 2026-2035 - Market by | Region |

| Southwestern China | 8.7% |

| Northwestern China | 8.1% |

| North China | 7.2% |

| East China | XX% |

| Southcentral China | XX% |

| Northeast China | XX% |

By Vehicle Type: SUVs account for the largest share of China's used car market by vehicle type, a reflection of the dominant position utility vehicles have carved out in the country's overall automotive consumption over the past decade. A large proportion of the used SUV inventory available today consists of vehicles aged three to six years, representing trade-ins from first-time new car buyers upgrading their original purchases. Platforms such as Guazi and Uxin report high search and transaction volumes for this category, particularly in Tier 1 and Tier 2 cities. Sedans hold the second-largest share, supported by continued demand from price-conscious buyers and the substantial volume of older sedans available at sub-USD 10,000 price points in smaller Chinese cities.

By Sales Channel: Offline channels retain a meaningful share of China's used car transactions, primarily serving buyers who require physical inspection and test drives before committing to a purchase. Organized dealers with physical showrooms, particularly those operating superstore formats, benefit from higher conversion rates among customers who value the experiential aspects of vehicle selection. Online channels are outgrowing offline in both transaction volume and revenue pace, with platforms combining digital browsing, AI valuations, and blockchain vehicle histories increasingly handling the full transaction cycle. The convergence of digital and physical retail through hybrid models, where buying begins online and finalizes offline, is becoming the standard commercial format as consumer comfort with digital vehicle commerce grows.

East China holds the commanding position in China's used car market, accounting for nearly a third of total national transaction value in 2025. The region's commercial centers, particularly Shanghai, Zhejiang, and Jiangsu, have among the highest per-capita vehicle ownership rates in the country, creating a continuous flow of trade-in supply that keeps used vehicle inventory fresh and diverse. Digital platform penetration is also highest in East China, where buyers are most comfortable transacting online and where organized dealer infrastructure is most mature. The concentration of new car dealerships in this region simultaneously generates a steady flow of certified pre-owned inventory as manufacturers execute vehicle exchange programs with their existing customer bases.

Southcentral China is establishing itself as the second most significant regional market, driven by a combination of manufacturing activity, growing service sector employment, and escalating urban incomes in cities including Wuhan, Guangzhou, and Changsha. Consumer appetite for vehicles in this region has been rising steadily as middle-class households move through first-time ownership toward replacement purchase decisions. Government road improvement programs in Southcentral provinces have also made vehicle ownership more practical outside major city centers, expanding the active buyer base for both new and used vehicles. Organized used car platforms are expanding coverage in this region, recognizing it as the most commercially attractive growth frontier over the coming decade.

China's used car market is fragmented but consolidating, characterized by a mix of large national digital platforms, omnichannel organized dealers, and thousands of smaller independent operators. National players such as Guazi and Uxin dominate through technology investment, brand recognition, and geographic breadth across hundreds of cities. Autohome Inc., while originally an automotive information portal, has evolved into a transaction and financing gateway. CAR Inc. and Souche serve distinct niches within fleet and dealer enablement respectively.

The competitive edge in China's used car market is shifting toward platforms that combine comprehensive data capabilities with physical service infrastructure. Companies that can offer AI-powered vehicle appraisals, verified ownership documentation, financing integration, and after-sales service bundles in a single customer experience are building the strongest moats. Price competition remains intense but is increasingly being supplemented by trust and service as the primary buyer decision criteria, particularly among younger urban buyers transacting digitally.

Founded in 2011 and headquartered in China, Uxin Ltd. operates as the country's largest online used car trading platform, offering B2B, B2C, and C2B transaction services. The company's inventory-owning omnichannel model enables full-service used car transactions, covering acquisition, inspection, reconditioning, financing, and after-sales support. In Q2 2025, Uxin posted retail revenues of approximately RMB 607.6 million, up 87% year on year, demonstrating strong commercial momentum. Its physical superstore network complements its digital platform, serving buyers who prefer in-person vehicle evaluation before completing online transactions.

Founded in 2015 and headquartered in Beijing, Guazi is a leading C2B and C2C used car platform in China, operating across more than 200 cities nationwide. Powered by big data and artificial intelligence, Guazi provides end-to-end services including vehicle assessment, pricing, e-commerce transactions, auto financing, logistics, and after-sales support. The platform is at the forefront of digitizing non-standard second-hand vehicle asset circulation in China. Guazi has been an active voice in calling for unified industry inspection standards, recognizing the importance of standardization for long-term consumer confidence and market development.

CAR Inc. is a prominent Chinese automobile services company that operates across rental, leasing, and second-hand vehicle segments. The company's access to large fleet inventories from its rental operations provides a consistent and quality-controlled supply of relatively young used vehicles to the market. This positions CAR Inc. advantageously in the growing consumer preference for certified, younger pre-owned cars. The company's established brand presence in China's automotive services landscape and its operational infrastructure across major cities support its used car sales operations as a natural extension of its broader vehicle lifecycle management business.

Founded in 2005 and listed on NYSE, Autohome Inc. is China's leading online destination for automobile buyers and sellers, encompassing new car listings, used car transactions, and automotive financing referrals. The platform generates substantial value from its large and loyal user base of vehicle purchasers, providing it with rich behavioral data that informs both its own services and those of dealer and financial partners. Autohome's recent integration with Haier's ecosystem signals its evolution toward a broader digital commerce and data platform. Its analytical tools and consumer insights are used by dealerships across China to optimize pricing, marketing, and inventory management.

Other key players in the market are Souche, Renrenche, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of China's booming pre-owned vehicle market with our definitive 2026 used car market report. Gain precise data on transaction volumes, platform growth trajectories, regional demand hotspots, and the strategies of leading players like Guazi and Uxin. Whether you are entering the market, scaling operations, or tracking competitive dynamics, this report gives you the intelligence to make confident, informed decisions. Download your free sample today and explore what is driving China's thriving used car market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China used car market reached an approximate value of USD 250.29 Billion.

The China used car market is assessed to grow at a CAGR of 7.60% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 520.67 Billion by 2035.

The regional markets include North China, East China, Southwestern China, Southcentral China, Northeast China, and Northwestern China.

The various types of used cars include sports utility vehicle (SUV), sedans, hatchbacks, and others.

The major vendor types studied in the market report are unorganised and organised.

The several sales channels in the market report include online and offline.

The market segmentation based on fuel types includes diesel, hybrid/electric, gasoline, petrol and others.

The key players in the market are Uxin Ltd., Guazi, CAR Inc., Souche, Autohome Inc., and Renrenche, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Vehicle Type |

|

| Breakup by Vendor Type |

|

| Breakup by Fuel Type |

|

| Breakup by Sales Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.