Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

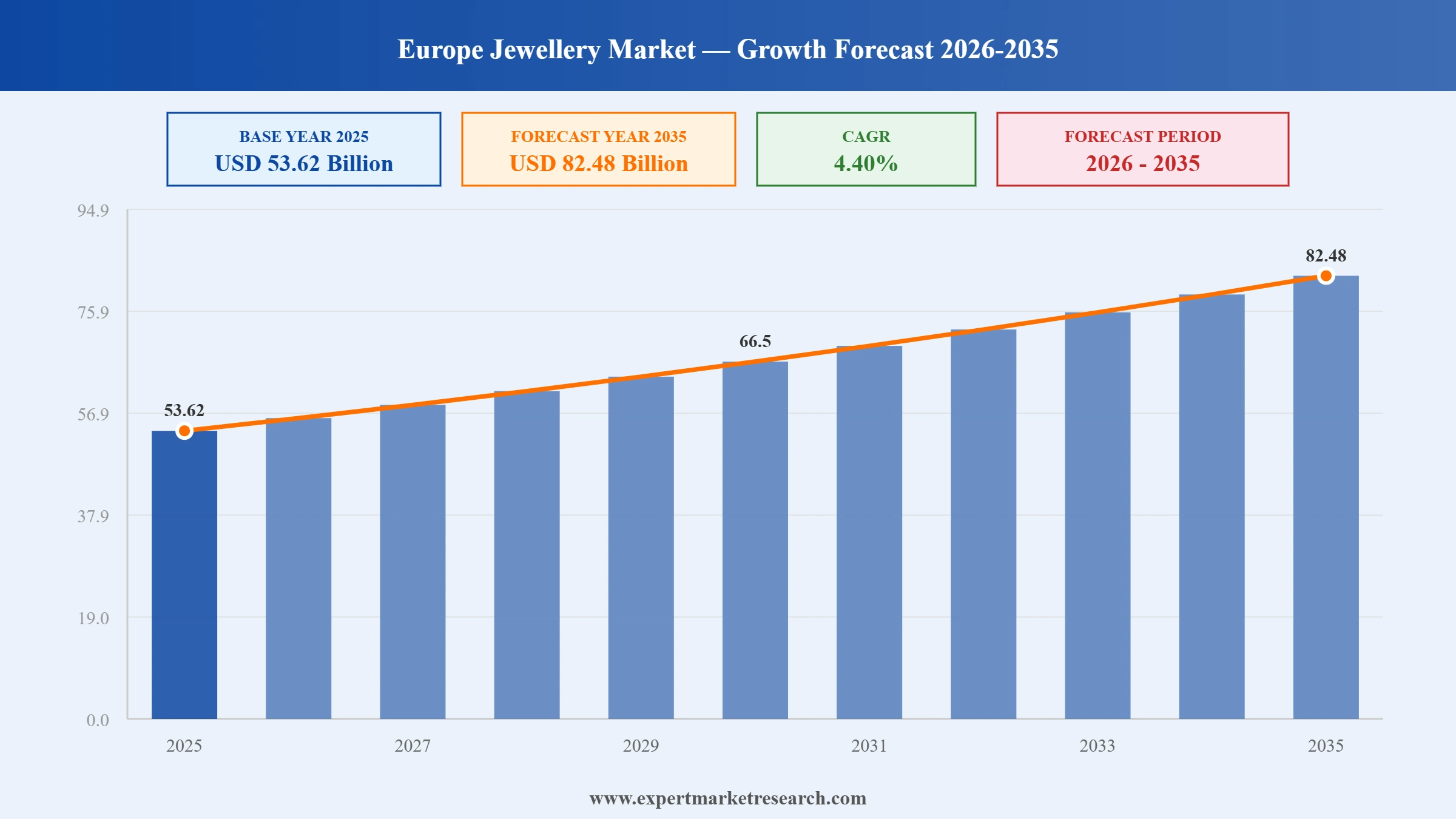

The Europe Jewellery Market reached a value of USD 53.62 Billion at 2025 and is projected to expand at a CAGR of around 4.40% during the forecast period of 2026-2035. With rising consumer preference for sustainable and recycled-metal jewellery backed by major brand commitments, growing appetite for personalized and premium ring and necklace designs across key markets, accelerating adoption of online retail and virtual try-on tools, and sustained cultural demand for jewellery across gifting occasions and milestones, the market is expected to reach USD 82.48 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Europe Jewellery Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 53.62 |

| Market Size 2035 | USD Billion | 82.48 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.40% |

| CAGR 2026-2035 - Market by Region | Germany | 5.0% |

| CAGR 2026-2035 - Market by Region | United Kingdom | 4.7% |

| CAGR 2026-2035 - Market by Product | Necklace | 5.1% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 7.2% |

| 2025 Market Share by Region | United Kingdom | 15.4% |

The Europe Jewellery Market is being reshaped by several converging forces: a strong consumer shift toward sustainable and ethically sourced precious metals, rapid technology adoption spanning lab-grown diamonds and 3D design tools, expanding omni-channel retail models driven by the growth of online platforms, and rising consumer appetite for personalized and premium jewellery across milestone occasions. These dynamics are collectively supporting a healthy and consistent growth outlook through 2035.

In February 2026, Pandora announced the launch of platinum-plated jewellery as an expansion of its precious metal portfolio, with a pilot covering 30 stores and online platforms across Northern Europe in Q1 2026. Built on the company's proprietary PANDORA EVERSHINE metal-alloy core and using a new platinum plating technique, the collection initially covers best-selling bracelet designs. This initiative aims to reduce dependence on volatile sterling silver prices while maintaining Pandora's accessible price positioning in the European market. A broader global rollout is planned for the second half of 2026.

As of August 2024, Pandora completed its commitment to use only recycled silver and gold across its entire jewellery production, marking a significant sustainability milestone for the Europe-headquartered jewellery brand. The transition, initiated in 2020, covered both Pandora's own manufacturing and those of its sub-suppliers globally. The company also confirmed plans to gradually extend recycled sourcing to platinum as it integrates the new precious metal into its product range. This milestone reinforces Pandora's position as a leader in sustainable jewellery within the European and global market.

In 2024, Compagnie Financiere Richemont acquired Vhernier, an Italian luxury jewellery brand renowned for its distinctive sculptural designs and high-quality gemstone craftsmanship, to enhance its Jewelry Maisons division. The acquisition brings a prestigious Italian artisanal jewellery name under the Richemont umbrella, alongside existing flagship brands Cartier and Van Cleef and Arpels. This move reinforces Richemont's ambition to consolidate its leadership in the European luxury jewellery segment and strengthens its presence in the Italian jewellery manufacturing ecosystem.

In fiscal year 2025, Richemont's Jewellery Maisons division, which includes Cartier, Van Cleef and Arpels, and Buccellati, reported a 14% increase in sales to reach EUR 6.2 billion across the fiscal quarter, driven by sustained European consumer demand for high-end jewellery pieces. The performance underscored the resilience of the European luxury jewellery segment against broader macroeconomic headwinds, with Cartier and Van Cleef and Arpels recording notably strong sell-through rates across flagship European boutiques. Richemont's total group sales rose 10% to EUR 17.0 billion over nine months to December 2025.

Pandora acquired the distribution and retail network of Visao do Tempo, its long-standing distributor in Portugal, converting all 34 concept stores and shop-in-shops to Pandora owned-and-operated locations as part of the company's Phoenix growth strategy. The acquisition gives Pandora direct control over its brand development, omni-channel journey, and product offering in Portugal, one of its key Western European markets. This strategic move is consistent with Pandora's broader objective to deepen its European retail presence and deliver superior consumer experiences across the region.

Across Europe, sustainability has moved from a niche selling point to a baseline purchase criterion for jewellery buyers, particularly among younger consumer cohorts. Brands are responding by embedding recycled metals, traceable gemstone sourcing, and reduced carbon manufacturing into their core product promises. The Europe Jewellery Market growth trajectory is being reinforced by this structural shift, as consumers increasingly select brands that can demonstrate credible sustainability credentials. In August 2024, Pandora, the world's largest jewellery brand, completed its transition to using 100% recycled silver and gold across all jewellery, setting a new benchmark for sustainable sourcing across the European jewellery landscape.

European jewellery brands are accelerating investment in materials innovation, 3D printing, AI-assisted design tools, and new precious metal formulations to meet evolving consumer expectations for novelty and craftsmanship. These technologies reduce production timelines, enable precise customization, and allow brands to respond more nimbly to shifting fashion cycles. In February 2026, Pandora introduced a new platinum-plated jewellery line using an advanced plating technique built on its EVERSHINE metal-alloy core, piloting across 30 stores and online in Northern Europe. This launch represents a blend of materials science innovation with accessible luxury positioning that is increasingly defining the European jewellery competitive landscape.

The European luxury jewellery sector is experiencing a pronounced consolidation trend, as leading conglomerates seek to broaden their prestige portfolios through targeted acquisitions of artisanal and heritage brands. This strategy allows acquirers to capture differentiated craftsmanship, access new customer segments, and strengthen their positioning in the high-value jewellery tier. In 2024, Richemont acquired Vhernier, an Italian luxury jewellery brand celebrated for its sculptural design language, to complement its existing Jewelry Maisons division anchored by Cartier and Van Cleef and Arpels. The deal reflects a broader industry trend toward portfolio diversification as a buffer against single-brand demand cycles.

Despite macroeconomic pressures including persistent inflation and cost-of-living concerns across several European markets, the premium and luxury jewellery segment has demonstrated notable resilience. European consumers continue to prioritize quality, brand heritage, and emotional significance when purchasing jewellery, treating it as a store of value and a meaningful gift rather than a discretionary impulse purchase. In fiscal year 2025, Richemont's Jewellery Maisons recorded a 14% rise in sales, with flagship brands Cartier and Van Cleef and Arpels generating strong sell-through rates across European boutiques, evidencing the enduring demand for high-end jewellery even in uncertain economic conditions.

The Expert Market Research's report titled “Europe Jewellery Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

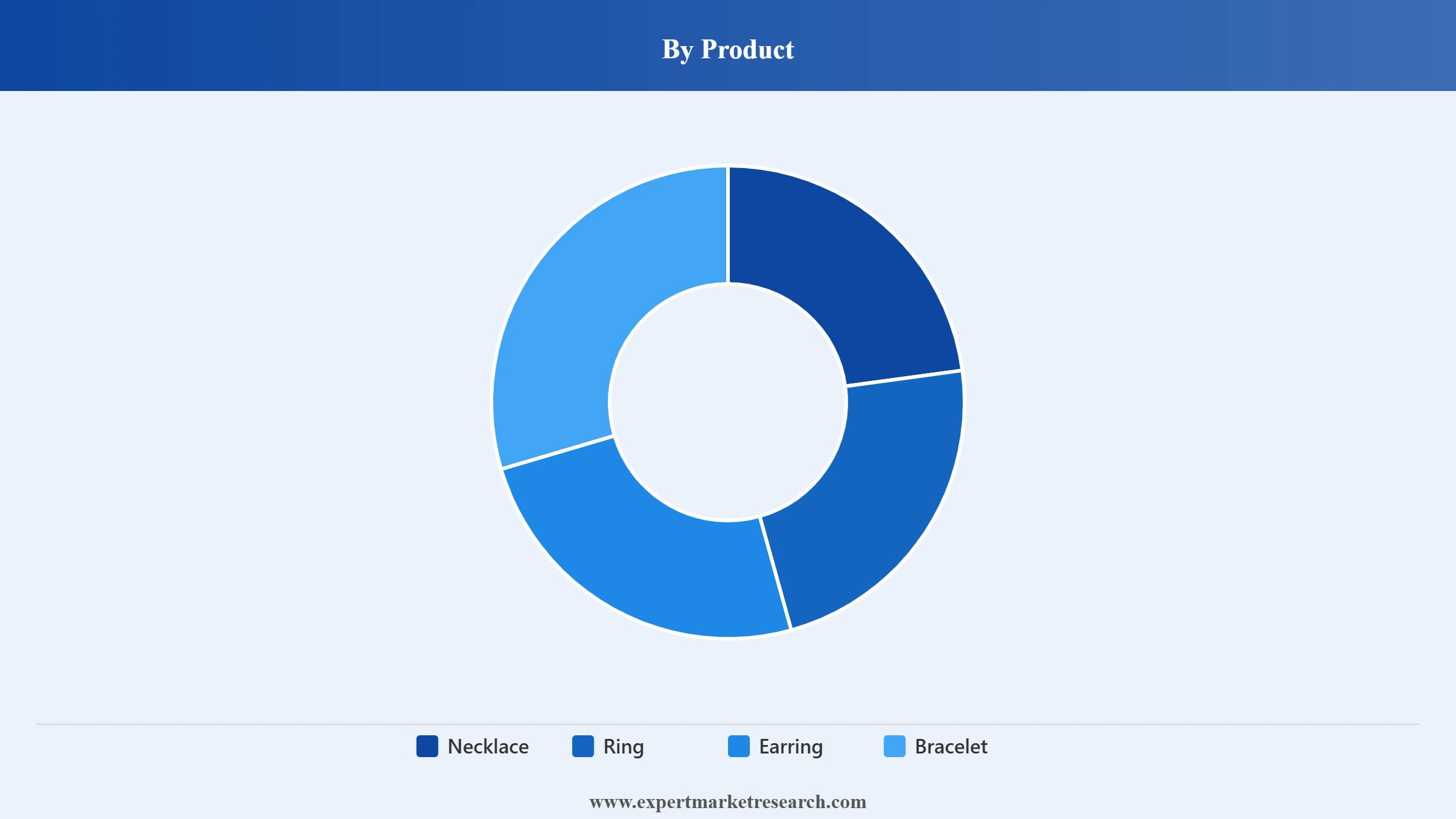

Market Breakup by Product

Key Insight: The Ring segment holds the largest product share in the European jewellery market, driven by its deep cultural significance in engagements, weddings, and anniversaries. European consumers consistently allocate greater spending to rings than to other jewellery categories, with personalized and bespoke ring designs seeing particularly strong demand from premium-seeking buyers. Necklaces represent the second most significant product category, benefiting from their versatility as both everyday fashion accessories and milestone gift items. Earrings hold meaningful market share, favoured for everyday and occasion wear across broad age demographics. Bracelets, including charm-based formats popularized by brands such as Pandora, maintain consistent demand particularly among younger consumers. The Others segment covers an array of body jewellery, anklets, and fashion accessories that cater to diverse personal expression preferences across European markets.

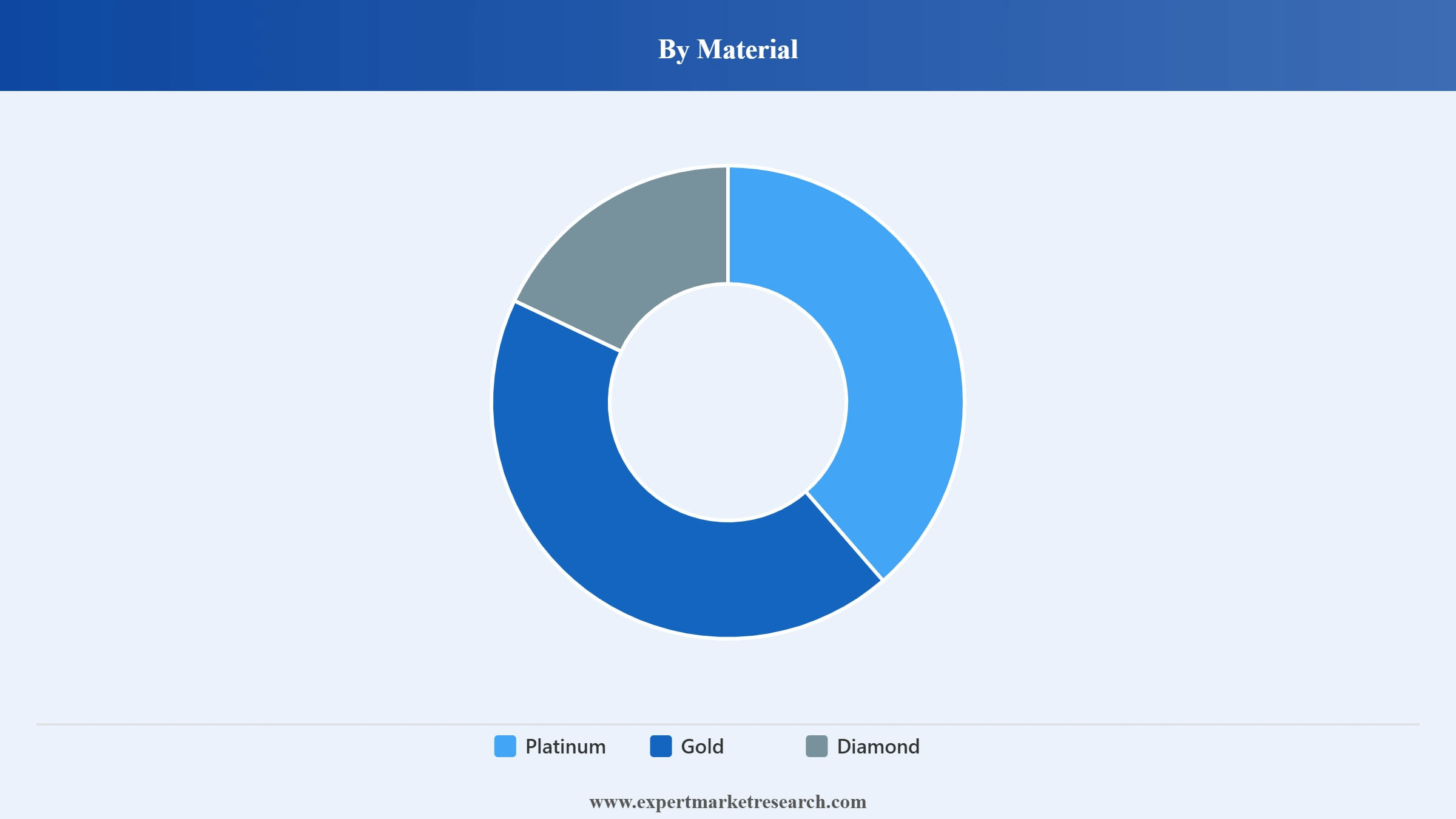

Market Breakup by Material

Key Insight: Gold is the dominant material in the European jewellery market, accounting for approximately 51% of material-based market revenue in the base year, reflecting its enduring cultural resonance, investment appeal, and versatility across both luxury and everyday jewellery formats. Italy, Europe's leading jewellery exporter, produces and exports significant volumes of gold jewellery, reinforcing gold's dominance across the regional supply chain. Diamond jewellery represents a critical high-value segment, particularly for engagement rings and special occasion pieces, with growing consumer interest in lab-grown diamonds as an ethically conscious and cost-competitive alternative. Platinum, historically associated with premium engagement and bridal jewellery, is seeing renewed momentum as brands such as Pandora introduce platinum-plated formats at accessible price points, broadening the material's appeal beyond its traditional luxury-only positioning. The Others category, covering silver, gemstone-set pieces, and mixed metals, serves value-oriented and fashion-driven consumers.

Market Breakup by Distribution Channel

Key Insight: Offline retail channels continue to dominate the European jewellery market, accounting for over 80% of total revenue in the base year. Physical stores remain central to the jewellery purchase journey because consumers place high value on tactile inspection, personalized service, and in-store consultation, particularly for high-value pieces such as engagement rings and fine jewellery. Heritage boutiques, multi-brand jewellery specialists, and department store concessions are the primary offline formats. Online channels are the fastest-growing distribution segment, supported by improvements in virtual try-on technology, detailed product visualization, and expanding digital marketing capabilities. Brands including Pandora have invested significantly in omni-channel strategies that blend digital discovery with in-store fulfilment, reflecting the evolving European consumer purchase journey.

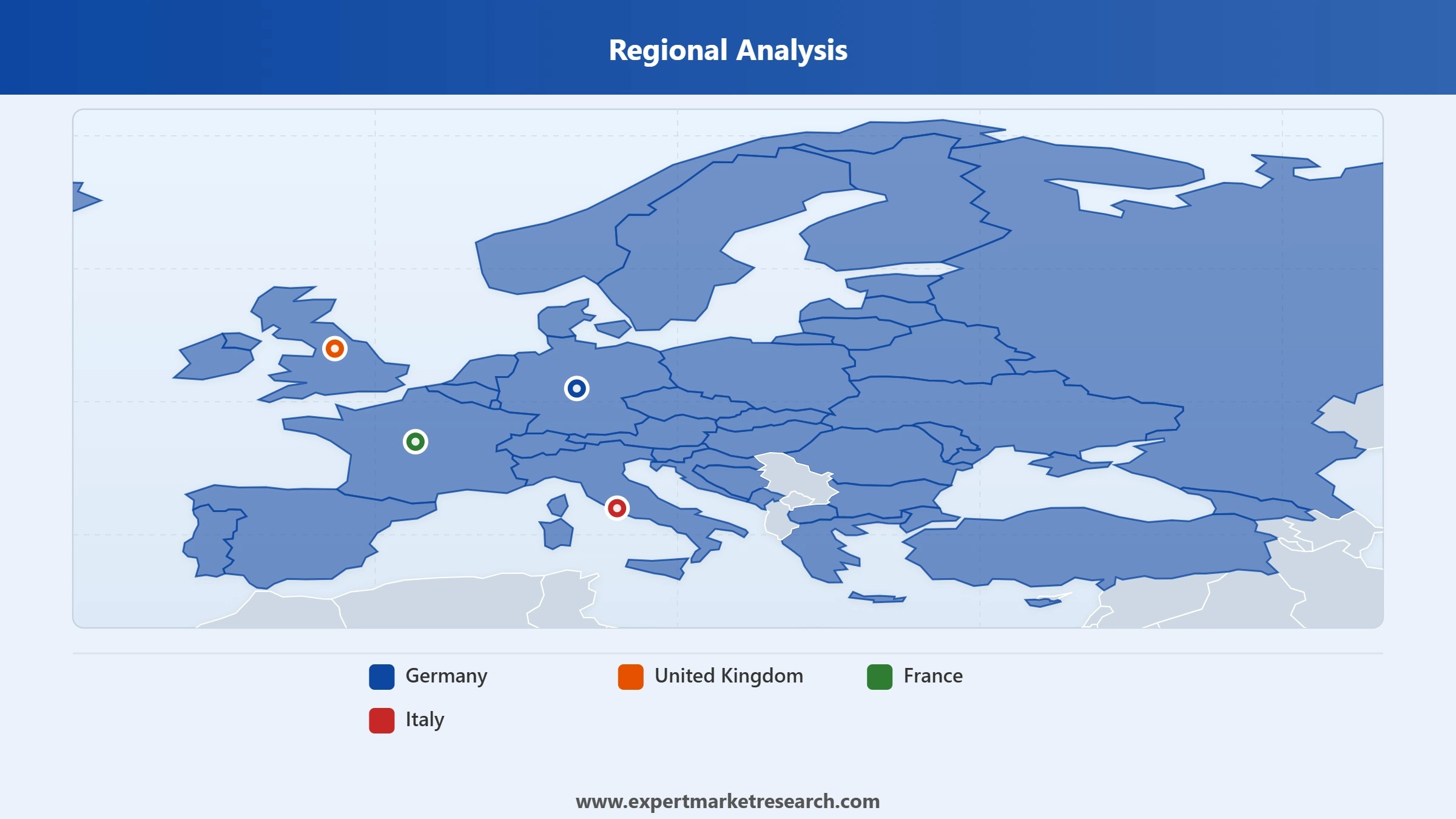

Market Breakup by Country

Key Insight: The United Kingdom holds the dominant country position in the Europe jewellery market, representing approximately 15% of total European market share, supported by London's role as a hub for global jewellery brands and designers and strong domestic demand for diamond and platinum engagement rings. Germany is projected to be the fastest-growing country over the forecast period with a CAGR of 5.0%, driven by growing consumer preference for ethical and sustainable jewellery and increasing disposable incomes among urban demographics. France, home to luxury conglomerates LVMH and Richemont, is a major market for high-end and haute joaillerie pieces, with Paris serving as the global centre for luxury jewellery design. Italy combines both manufacturing leadership and domestic consumption, with its jewellery industry anchored in goldsmithing districts such as Arezzo and Valenza.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product

Within the product segmentation, Rings command the largest revenue share in the European jewellery market, owing to their cultural primacy in engagements, marriages, and milestone celebrations. The ring category benefits from consistent replenishment demand, as consumers regularly upgrade or expand their ring collections, and it also commands the highest average selling prices among product categories due to the prevalence of diamond-set and bespoke designs. Necklaces occupy the second-largest product share, prized for their dual role as fashion statements and meaningful gifts. Brands such as Tiffany and Co and Pandora have driven significant necklace category growth through iconic product lines that blend heritage design with contemporary appeal.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Material

Within the material segmentation, Gold jewellery maintains the dominant share position, reflecting its historic status as a preferred jewellery material among European consumers and its central role in the output of Europe's premier jewellery manufacturing regions in Italy and France. Gold's investment-grade qualities and cultural associations with luxury and tradition sustain its broad appeal across demographic segments. Diamond jewellery follows as the second most significant material category, with engagement ring demand providing a reliable demand foundation. Offline retail remains the dominant distribution channel, accounting for the majority of European jewellery transactions, as consumers continue to prioritize in-store discovery and expert consultation for significant jewellery purchases.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom is the dominant European jewellery market by country share, accounting for approximately 15% of regional market revenue. London serves as a global jewellery hub, hosting flagship boutiques of both heritage luxury houses and emerging independent designers, and functions as a primary destination for international jewellery tourism. Consumer demand is particularly strong for diamond engagement rings and platinum-set bridal jewellery, reflecting the UK's deep cultural traditions around milestone purchases. The UK's growing appetite for sustainable and ethically sourced pieces is also contributing to premiumization trends across the market. Premium retail destinations including Bond Street, Mayfair, and the Hatton Garden district continue to anchor the UK's position as Europe's leading jewellery retail market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Germany represents the fastest-growing European jewellery market, projected to expand at a CAGR of 5.0% over the forecast period, underpinned by a strong middle class with rising disposable incomes and an increasingly discerning appetite for ethical, sustainably produced jewellery. German consumers show a preference for quality over volume, favouring artisanal and brand-verified pieces over mass-market options. The country's robust gifting culture and high engagement with online jewellery retail platforms are further accelerating market penetration. Italy, while a smaller domestic consumption market relative to the UK, holds strategic importance as Europe's manufacturing powerhouse, with gold jewellery exports worth EUR 9.2 billion in 2023, supporting regional supply chains that serve the entire European jewellery sector.

The Europe Jewellery Market operates as a moderately consolidated competitive landscape, structured across three distinct tiers: ultra-luxury heritage houses with multi-century brand equity, premium accessible brands with broad European retail footprints, and specialist fine jewellery houses targeting affluent niche segments. Competition is defined by brand heritage, design distinctiveness, gemstone sourcing transparency, retail network quality, and, increasingly, sustainability credentials. The digital acceleration in jewellery retail is reshaping competitive dynamics, with brands investing in virtual try-on technology, social commerce, and personalized online experiences as key differentiators.

Strategic mergers and acquisitions are reshaping competitive positions, with luxury conglomerates such as Richemont and LVMH expanding their jewellery portfolios through targeted brand acquisitions. Meanwhile, accessible luxury brands such as Pandora are investing in product innovation and owned-retail expansion to defend and grow their European market share. Smaller artisanal houses, known for bespoke craftsmanship and sustainable practices, are capturing increasing consumer interest, particularly among younger European buyers who prioritize brand values alongside product aesthetics.

Founded in 1837 and headquartered in New York, USA, Tiffany and Co is one of the world's most iconic luxury jewellery houses, acquired by LVMH Moet Hennessy Louis Vuitton in 2021. In Europe, Tiffany operates flagship boutiques in major cities including London, Paris, Milan, and Zurich, serving premium consumers with its signature blue-box gift jewellery, diamond engagement rings, and sterling silver fashion pieces. Its association with timeless American luxury and celebrity culture gives it strong brand recognition and aspirational appeal across European markets.

Founded in 1949 and headquartered in Hamilton, Bermuda, Signet Jewelers is the world's largest specialty jewellery retailer by store count. While its primary markets are the United States and Canada, Signet operates retail brands including H. Samuel and Ernest Jones in the United Kingdom, serving mid-market and accessible premium consumers with diamond and gold jewellery, engagement rings, and personalized pieces. Its UK presence gives it a significant footprint in Europe's largest jewellery market, where it competes effectively in the accessible luxury segment.

Founded in 1895 and headquartered in Wattens, Austria, Swarovski is a globally recognized crystal jewellery and accessories brand with deep European roots. The company operates over 3,000 retail locations worldwide, with a strong presence across Europe through both owned boutiques and wholesale partnerships. Swarovski's core strengths lie in its proprietary crystal cutting technology, wide accessible-luxury product range, and strong gifting appeal. In recent years, Swarovski has repositioned itself toward fine jewellery and higher price points while sustaining its broad consumer accessibility across European markets.

Founded in 1932 and headquartered in New York, USA, Harry Winston is a premier ultra-luxury jewellery and watch house with a storied heritage in exceptional diamond jewellery. Acquired by Swatch Group in 2013, Harry Winston operates boutiques in key European luxury retail destinations including London, Paris, Geneva, and Zurich. The brand is celebrated for its extraordinary high jewellery collections, rare coloured gemstones, and bespoke couture pieces created for ultra-high-net-worth clientele, positioning it firmly at the apex of the European luxury jewellery market.

Other key players in the market are Compagnie Financiere Richemont S.A., Chanel SA, Pandora A/S, Graff Diamonds Limited, LVMH Moet Hennessy Louis Vuitton SE, Le petit-fils de L.U. Chopard and Cie SA, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Looking to capitalize on the growing European jewellery market? Our 2026-2035 research report gives you a thorough view of market sizing, category-level forecasts, country-specific growth dynamics, and the competitive strategies of leading players from Pandora to Richemont and LVMH. Whether you are a jewellery brand, a luxury retailer, a private equity investor, or a supplier of precious metals and gemstones, this report delivers the clarity you need to make confident strategic moves. Download your free sample today and start uncovering the key opportunities in the European jewellery sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 53.62 Billion.

The market is projected to grow at a CAGR of 4.40% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 82.48 Billion by 2035.

Key trends aiding the market expansion are rising demand for ethical and sustainable jewellery; introduction of 3-D printed jewellery; and focus on minimalist designs.

The different products available in the market are necklace, ring, earring, and bracelet, among others.

The different materials used to make jewellery in the market are platinum, gold, and diamond, among others.

The different countries covered in the market report are Germany, the United Kingdom, France, and Italy, among others.

Key market players are Tiffany & Co, Signet Jewelers Ltd., Swarovski AG, Harry Winston, Inc., Compagnie Financière Richemont S.A., Chanel SA, Pandora A/S, Graff Diamonds Limited, LVMH Moet Hennessy Louis Vuitton SE, and Le petit-fils de L.U. Chopard & Cie SA, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Material |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.