Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

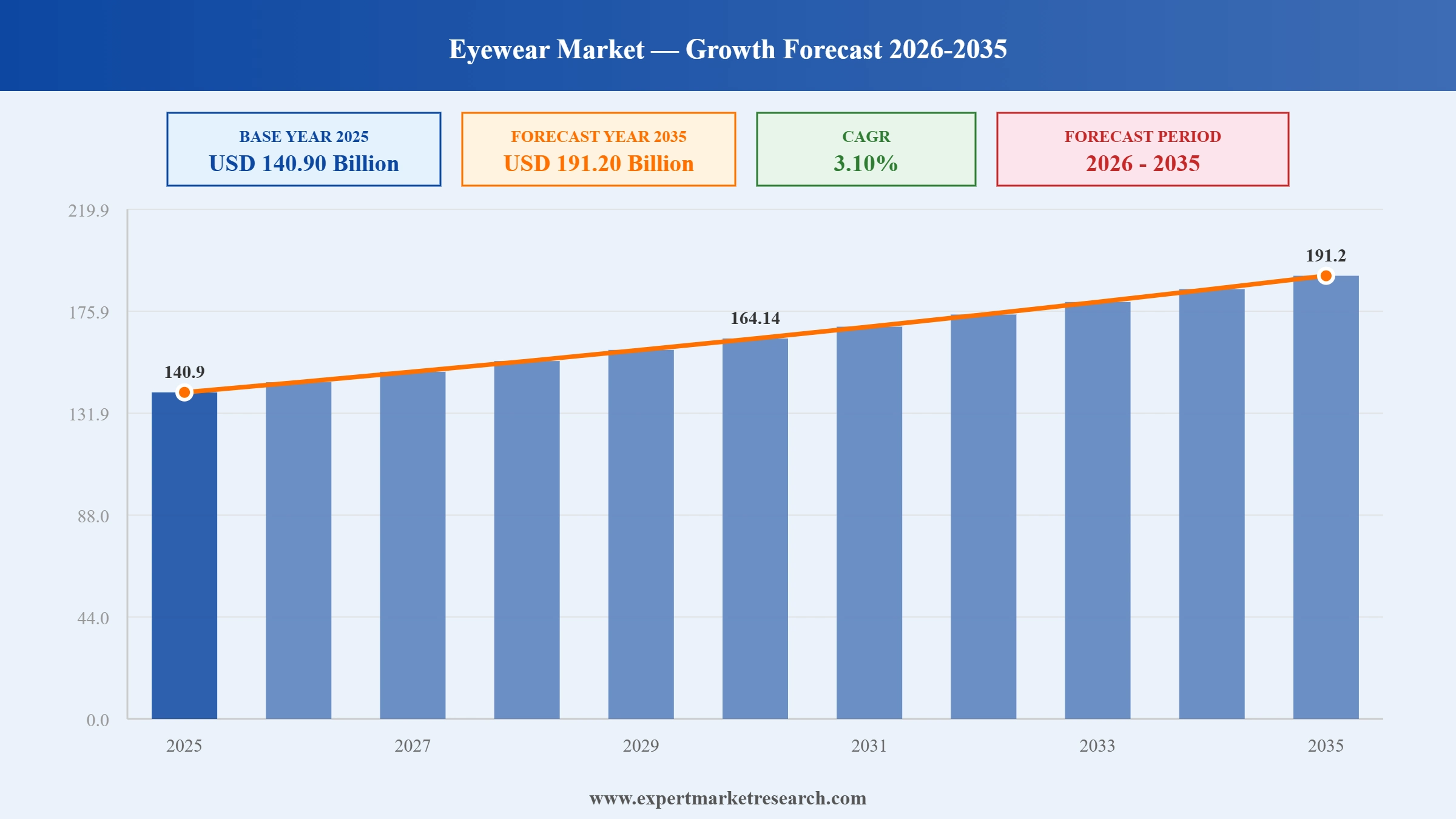

The Global Eyewear Market reached a value of USD 140.90 Billion at 2025 and is projected to expand at a CAGR of around 3.10% during the forecast period of 2026-2035. With accelerating myopia and presbyopia prevalence globally, the breakout commercial success of Ray-Ban Meta AI smart glasses, the EUR 3 billion Meta strategic equity investment in EssilorLuxottica, growing online optical retail, and rising premium and luxury sunglasses demand across Asia Pacific, the market is expected to reach USD 191.20 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Eyewear Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 140.90 |

| Market Size 2035 | USD Billion | 191.20 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.10% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 3.5% |

| CAGR 2026-2035 - Market by Country | India | 3.7% |

| CAGR 2026-2035 - Market by Country | China | 3.4% |

| CAGR 2026-2035 - Market by Product | Sunglasses | 3.8% |

| CAGR 2026-2035 - Market by Gender | Unisex | 4.0% |

| Market Share by Country 2025 | Mexico | 1.9% |

The Global Eyewear Market is being shaped by the breakout commercial success of Ray-Ban Meta AI smart glasses, the structural rise in global myopia and presbyopia prevalence, the rapid scale-up of online and direct-to-consumer optical retail, and continued premiumisation in sunglasses across Asia Pacific.

EssilorLuxottica and Meta confirmed plans to roughly double Ray-Ban Meta AI smart glasses production capacity to at least 20 million units annually by the end of 2026, more than tripling the 7 million units sold in 2025. The capacity ramp covers wholesale and direct-retail expansion across North America, Europe, and Asia Pacific, alongside product line extensions onto the Oakley sport-eyewear brand. The plan reinforces smart eyewear as a structural growth vector and signals long-term confidence in the AI-glasses category. Combined with Meta's EUR 3 billion equity stake, the production commitment positions EssilorLuxottica as the de facto manufacturing partner for AI-enabled consumer eyewear at global scale.

EssilorLuxottica announced that it more than tripled sales of its Meta artificial-intelligence smart glasses in 2025, selling more than 7 million units of Ray-Ban Meta AI glasses - up from approximately 2 million units across 2023 and 2024 combined. The product line, developed in partnership with Meta Platforms, Inc., was the single largest contributor to EssilorLuxottica's growth, accounting for more than a third of the group's third-quarter 2025 expansion. Q3 2025 sales rose 11.7% to EUR 6.9 billion (USD 8.1 billion), with smart glasses driving both volume and average-selling-price uplift across the wholesale and direct retail channels. The breakout success has positioned smart eyewear as a structural growth vector for the wider Global Eyewear Market.

Meta Platforms, Inc. invested approximately EUR 3 billion in EssilorLuxottica during 2025, taking a 3% strategic equity stake in the world's largest eyewear group. The investment formalises and deepens the multi-year smart glasses partnership between the two companies, supports joint product development across the Ray-Ban, Oakley, and Persol franchises, and underwrites planned production scale-up. Meta and EssilorLuxottica have publicly discussed plans to double smart-glasses output to at least 20 million units by the end of 2026, reflecting continued strong demand for AI-enabled eyewear and the strategic alignment of capital, manufacturing capacity, and brand reach across the partnership.

Safilo Group, the Italian licensed-brand eyewear specialist, more than doubled net profit in 2025 to approximately EUR 48.6 million, up 118.2% from EUR 22.3 million in 2024, with the adjusted EBITDA margin reaching 9.4% (+40 basis points). Group revenue at current exchange rates declined 1% to EUR 983.4 million on the back of US dollar weakening, while at constant exchange rates net sales rose 1.8%, underscoring underlying demand strength. The performance reflects portfolio rationalisation following the expiration of the Jimmy Choo licence and continued growth in Safilo's owned brands and David Beckham, Tommy Hilfiger, Carolina Herrera, and Marc Jacobs licensed franchises.

EssilorLuxottica completed the acquisition of streetwear brand Supreme from VF Corporation for approximately USD 1.5 billion in 2024, expanding the group beyond pure-play eyewear into adjacent youth-led lifestyle and accessories categories. The transaction provides EssilorLuxottica with a globally recognised streetwear platform that complements its Ray-Ban, Oakley, Persol, and licensed-brand eyewear portfolio, and creates cross-merchandising opportunities across retail, e-commerce, and brand-led activations. The deal closed alongside EssilorLuxottica's 2024 group revenue of EUR 26.51 billion, underscoring the scale of M&A capacity available to the eyewear leader.

The Ray-Ban Meta AI smart glasses partnership between EssilorLuxottica and Meta Platforms has shifted smart eyewear from a niche category into a meaningful growth vector for the Global Eyewear Market. Sales of more than 7 million units in 2025, more than triple the 2 million units sold across 2023 and 2024 combined, were driven by camera, voice-assistant, and AI-translation features, attractive Ray-Ban styling, and aggressive retail expansion. Q3 2025 alone saw EssilorLuxottica sales rise 11.7% to EUR 6.9 billion, with smart glasses contributing more than a third of growth. The trend is supporting Global Eyewear Market growth by extending the category into AR/AI use-cases and lifting realised average selling prices.

Meta's EUR 3 billion equity investment in EssilorLuxottica for a 3% stake during 2025, alongside the joint plan to double smart-glasses production to at least 20 million units by end-2026, signals a long-term capital and capacity alignment between the world's largest eyewear group and one of the most important consumer-AI platforms. The trend is supporting Global Eyewear Market growth by underwriting multi-year R&D, manufacturing, and brand investment, anchoring AR/AI-enabled eyewear as a permanent product category, and creating a high-margin premium tier that lifts the wider category's pricing power.

Online and direct-to-consumer eyewear retail continues to expand rapidly, supported by virtual try-on AR technology, AI-driven prescription tools, telehealth-enabled refraction services, and the structural shift in consumer purchasing behaviour. Brands such as Warby Parker, Lenskart, and EssilorLuxottica's own digital channels have scaled aggressively, while traditional optical retailers are responding with omnichannel investments. The trend is supporting Global Eyewear Market growth by widening access to corrective and fashion eyewear in tier-II and tier-III geographies, lifting purchase frequency, and creating premium-segment opportunities for AI-enabled customisation and subscription models across optical and sunglasses categories.

Premium and luxury sunglasses continue to outperform mass-market categories, anchored by Asia Pacific consumer demand, K-beauty and J-fashion cultural influence, and the broader resilience of luxury accessories. EssilorLuxottica's Ray-Ban, Oakley, Persol, and licensed-brand portfolio, alongside Safilo Group's licensed franchises and LVMH-owned eyewear, capture the category's premium tailwinds. The trend is supporting Global Eyewear Market growth by lifting realised prices, sustaining licensed-brand royalty economics, and structurally enlarging the high-margin sunglasses tier alongside the still-larger spectacles category.

“Eyewear Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

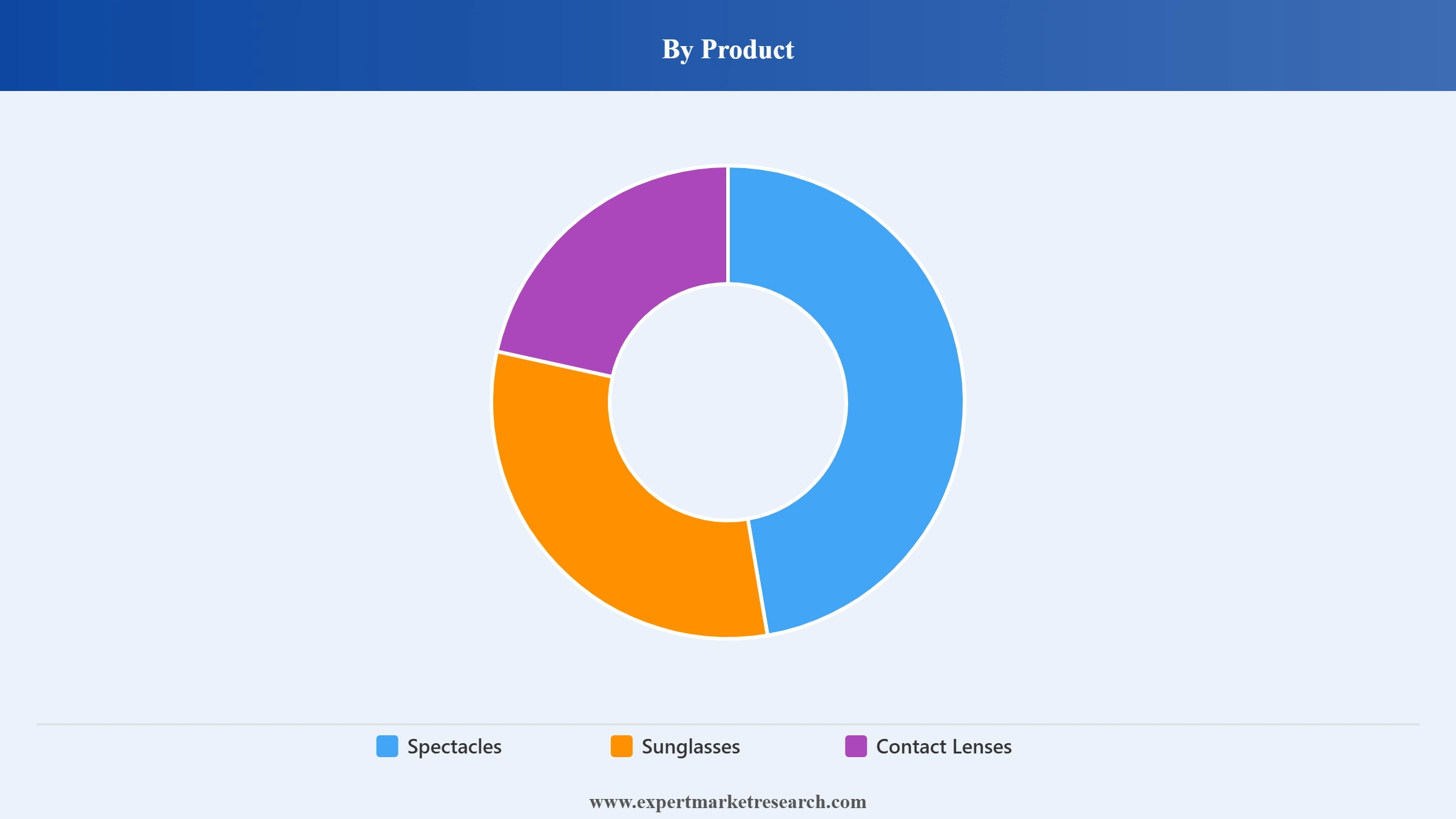

Market Breakup by Product

Key Insight: Spectacles dominate the Global Eyewear Market with approximately 66% revenue share in 2025, anchored by aging populations in Europe and North America requiring presbyopia correction and rising prescription-spectacle volumes among Asia Pacific schoolchildren due to structurally elevating myopia prevalence. Sunglasses represent the second-largest product category, with a forecast CAGR of approximately 6.7% over the medium term, supported by premium and luxury demand led by EssilorLuxottica (Ray-Ban, Oakley, Persol), LVMH, Safilo Group's licensed franchises, and rising disposable incomes in Asia Pacific. Contact Lenses are a strategically important high-margin category, anchored by Johnson & Johnson Vision Care, Alcon Vision, and The Cooper Companies, with continued growth in daily-disposable and silicone hydrogel formats.

Market Breakup by Gender

Key Insight: Women's eyewear is the largest gender sub-segment by revenue, anchored by higher purchase frequency, stronger fashion-led sunglasses demand, and broader licensed-brand appeal across LVMH, Prada, and licensed Safilo franchises. Men's eyewear remains structurally important, particularly in sport sunglasses (Oakley) and prescription spectacles. Unisex frames have grown rapidly on the back of streetwear culture, AI smart-glasses (Ray-Ban Meta), and the broader normalisation of gender-neutral fashion accessories. EssilorLuxottica's Supreme acquisition further strengthens the unisex youth-led tier alongside its core Ray-Ban Wayfarer franchise.

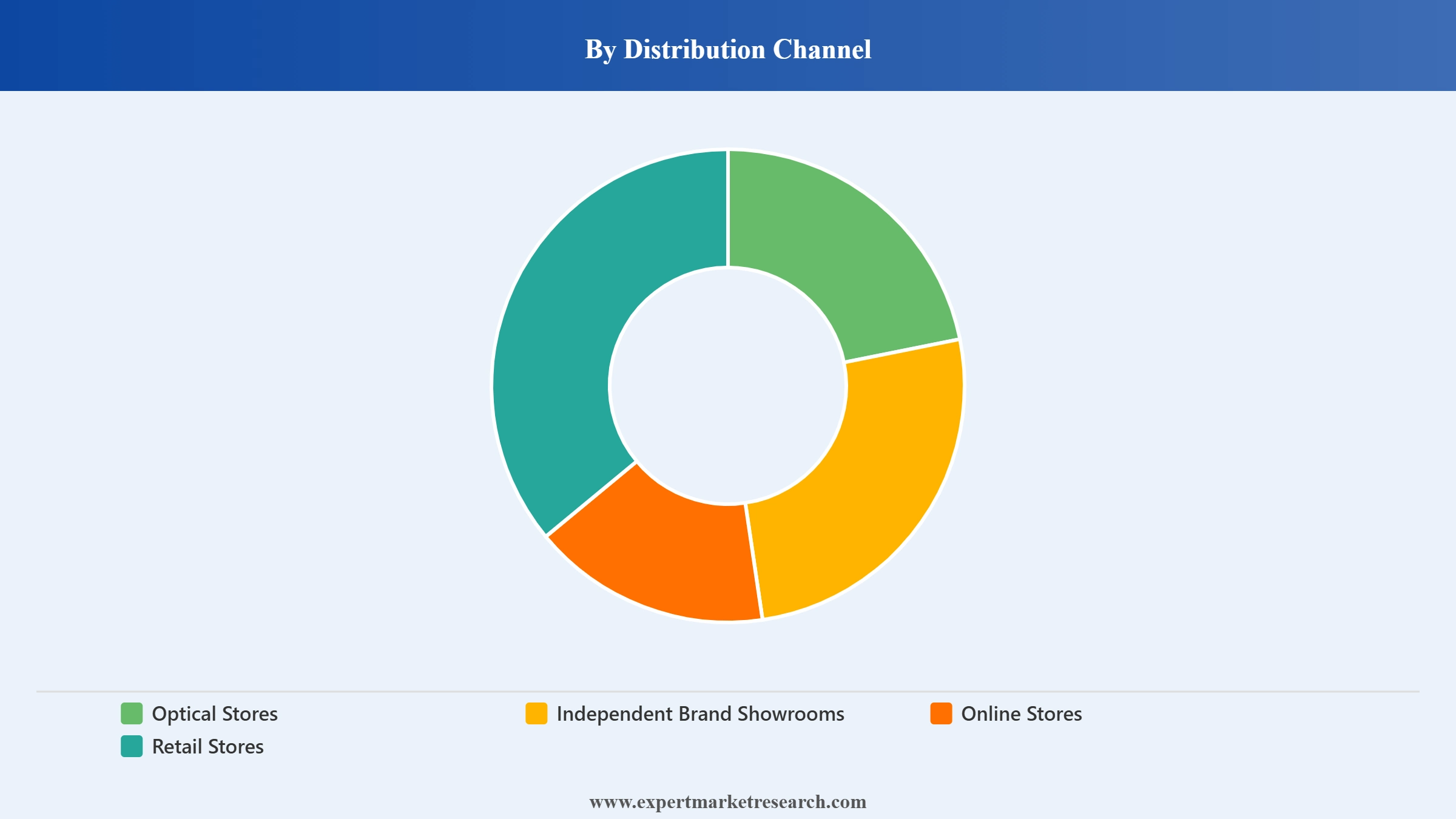

Market Breakup by Distribution Channel

Key Insight: Optical Stores remain the dominant distribution channel for the Global Eyewear Market, anchored by prescription-led services that require professional refraction, fitting, and after-sales adjustment, with EssilorLuxottica's owned-retail networks (LensCrafters, Sunglass Hut, Pearle Vision) leading the global premium segment. Independent Brand Showrooms anchor luxury and prestige eyewear sales, while Retail Stores (department stores, specialty fashion retail) capture mass-market sunglasses volume. Online Stores are the fastest-growing channel, driven by virtual try-on AR, AI-led prescription tools, and digital-first brands such as Warby Parker and Lenskart, lifting access in tier-II and tier-III geographies and supporting premium-tier subscription models.

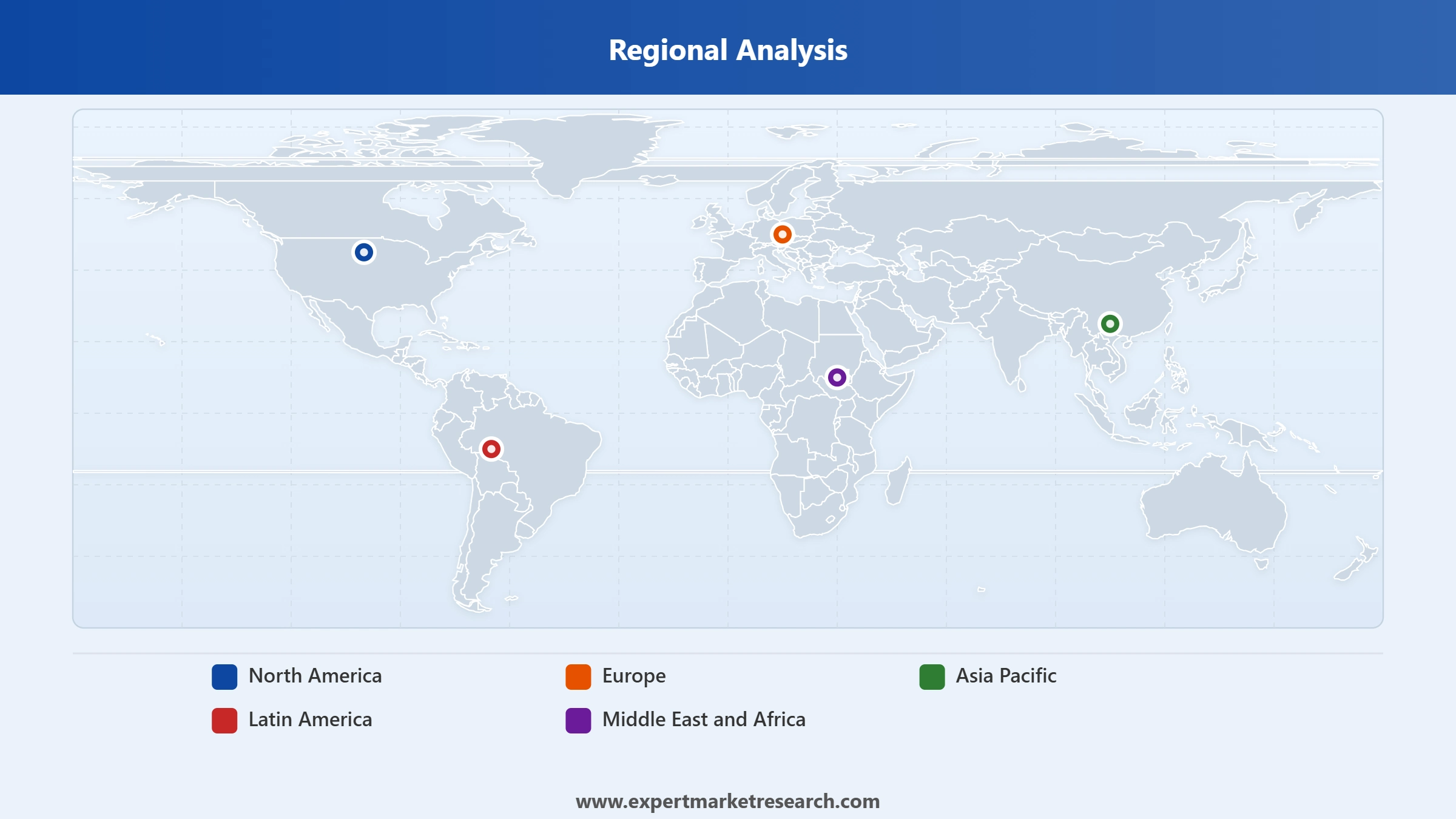

Market Breakup by Region

Key Insight: Europe and North America together command the largest share of the Global Eyewear Market, anchored by aging populations, established optical healthcare systems, and high premium-and-luxury sunglasses penetration. Europe is led by EssilorLuxottica (Italy/France), Safilo Group (Italy), Silhouette International (Austria), Prada and LVMH-owned eyewear, while North America is led by EssilorLuxottica's owned-retail base, Johnson & Johnson Vision Care, and Alcon. Asia Pacific is the fastest-growing region, anchored by China's structurally rising myopia prevalence, India's digital-first optical retail led by Lenskart, and Japanese-Korean premium consumer demand. Latin America and Middle East and Africa are smaller but rising demand pools.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Product segmentation, Spectacles and Sunglasses represent the most strategically important categories of demand and revenue. Spectacles command approximately 66% revenue share in 2025 thanks to demographic tailwinds from aging populations in Europe and North America, accelerating myopia prevalence in Asia Pacific schoolchildren, and the broader structural shift toward prescription-led optical retail. Sunglasses are the second-largest product category, with a forecast CAGR of approximately 6.7% supported by premium and luxury demand led by EssilorLuxottica (Ray-Ban, Oakley, Persol), Safilo Group's licensed franchises, LVMH-owned eyewear, and rising Asia Pacific disposable incomes. Contact Lenses are smaller but a high-margin strategically important category anchored by Johnson & Johnson Vision Care, Alcon Vision, and The Cooper Companies, with daily-disposable and silicone hydrogel formats leading volume growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Distribution Channel segmentation, Optical Stores and Online Stores dominate the competitive narrative. Optical Stores remain the largest channel by value, anchored by prescription-led services and EssilorLuxottica's globally integrated owned-retail base (LensCrafters, Sunglass Hut, Pearle Vision, Salmoiraghi & Viganò). Online Stores are the fastest-growing channel, with a forecast CAGR of approximately 7.5%, supported by virtual try-on AR, AI-led prescription tools, and digital-first brands across North America, Europe, and Asia Pacific. Independent Brand Showrooms anchor luxury and prestige eyewear, while Retail Stores capture mass-market sunglasses volume across department stores and specialty fashion retail.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Regional lens, Europe, North America, and Asia Pacific together account for the bulk of demand. Europe leads on the strength of EssilorLuxottica, Safilo, Silhouette, Prada, and LVMH-owned eyewear, supported by aging populations and high optical healthcare penetration. North America anchors prescription, contact-lens, and premium-luxury sunglasses growth led by EssilorLuxottica's owned retail and Johnson & Johnson Vision Care's contact-lens leadership. Asia Pacific is the fastest-growing region, with structurally rising myopia prevalence in China, India's Lenskart-led digital optical retail revolution, and Japanese-Korean premium consumer demand collectively underpinning the long-run growth narrative.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe and North America are the leading regional markets in the Global Eyewear Market and together account for the bulk of premium and prestige demand. Europe leads on the strength of EssilorLuxottica's headquarters operations across Italy and France, Safilo Group's Italian licensed-brand business, Silhouette International's Austrian rimless eyewear platform, and the eyewear divisions of Prada and LVMH, supported by structurally aging populations, established optical healthcare systems, and high premium-and-luxury sunglasses penetration. North America is anchored by EssilorLuxottica's owned-retail networks (LensCrafters, Sunglass Hut, Pearle Vision), the contact-lens leadership of Johnson & Johnson Vision Care and Alcon Vision, and the strong direct-to-consumer scale-up of Warby Parker and similar brands.

Asia Pacific is the fastest-growing regional market in the Global Eyewear Market, anchored by China's structurally rising myopia prevalence and the corresponding scale-up of prescription-spectacle volumes among schoolchildren, India's Lenskart-led digital optical retail revolution, and Japanese-Korean premium consumer demand. The Ray-Ban Meta AI smart glasses partnership with EssilorLuxottica, alongside strategic capacity expansion for Asia Pacific demand, reinforces the region's position as a structural growth engine. Latin America and Middle East and Africa are smaller but rising demand pools, with Brazil, Mexico, the United Arab Emirates, and South Africa anchoring regional volumes through urban middle-class consumption.

The Global Eyewear Market is highly consolidated at the top end, with EssilorLuxottica - the merged parent of Luxottica Group and Essilor International - capturing the dominant share of premium spectacles, sunglasses, lenses, and integrated optical retail. The contact lens sub-segment is led by Johnson & Johnson Vision Care, Alcon Vision, and The Cooper Companies. Mid-tier and licensed-brand specialists including Safilo Group, Silhouette International Schmied AG, Prada, and LVMH-owned eyewear compete on Italian and European craftsmanship, licensed-brand royalty economics, and prestige distribution.

Recent strategic moves include the Ray-Ban Meta AI smart-glasses scale-up to 7 million units in 2025, Meta's EUR 3 billion strategic equity investment in EssilorLuxottica, EssilorLuxottica's USD 1.5 billion Supreme acquisition, and Safilo Group's net-profit-doubling 2025 turnaround. Competitive priorities have shifted toward AI-enabled smart eyewear, vertical integration of optical retail, prescription-led contact-lens innovation, and licensed-brand portfolio rationalisation across the industry leaders.

Formed via the 2018 merger of Italy's Luxottica Group and France's Essilor International, EssilorLuxottica is headquartered in Charenton-le-Pont, France and Milan, Italy, and is the world's largest vertically integrated eyewear group with 2024 group revenue of EUR 26.51 billion. In 2025, the group sold more than 7 million Ray-Ban Meta AI smart glasses (>3x 2023-2024 combined), received a EUR 3 billion strategic equity investment from Meta Platforms (3% stake), and acquired streetwear brand Supreme for USD 1.5 billion in 2024.

Founded in 1981 and headquartered in Jacksonville, Florida, USA, Johnson & Johnson Vision Care, Inc. is the world's largest contact lens producer through its Acuvue brand portfolio, spanning daily-disposable, silicone hydrogel, multifocal, and astigmatism formats. Owned by parent Johnson & Johnson (NYSE: JNJ), the business benefits from scale R&D investment, vertically integrated manufacturing, and global optometrist-led distribution, anchoring the high-margin contact-lens sub-segment alongside Alcon Vision and The Cooper Companies.

Founded in 1934 and headquartered in Padua, Italy, Safilo Group S.p.A. is one of the world's leading licensed-brand eyewear specialists, designing and manufacturing prescription frames and sunglasses for owned brands and licensed franchises including David Beckham, Tommy Hilfiger, Carolina Herrera, and Marc Jacobs. In 2025, Safilo doubled net profit to approximately EUR 48.6 million (up 118.2% versus 2024), with adjusted EBITDA margin reaching 9.4% and constant-currency net sales growth of 1.8%.

Founded in 1945 and headquartered in Geneva, Switzerland (with US operations in Fort Worth, Texas), Alcon Vision LLC is one of the world's leading contact lens and ophthalmic surgical-device producers, anchored by its Dailies, Total, and Precision contact-lens portfolios. Alcon competes directly with Johnson & Johnson Vision Care and The Cooper Companies in the high-margin contact-lens segment, supported by deep R&D in silicone hydrogel materials, multifocal optics, and integrated ophthalmic-care offerings across the global ECP (eye care professional) channel.

Other key players in the market are Prada S.p.A., Oakley, Inc. (EssilorLuxottica), The Cooper Companies Inc., Silhouette International Schmied AG, LVMH Group, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Eyewear Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on Ray-Ban Meta AI smart-glasses scale-up, the EUR 3 billion Meta-EssilorLuxottica capital alignment, online optical retail growth, and premium-luxury sunglasses momentum across Asia Pacific. Whether you are scaling a digital-first optical brand, launching AI-enabled smart eyewear, or expanding contact-lens manufacturing capacity, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Eyewear industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global eyewear market attained a value of nearly USD 140.90 Billion.

The market is projected to grow at a CAGR of 3.10% between 2026 and 2035.

The market is estimated to grow in the forecast period of 2026-2035 to attain a value of more than USD 191.20 Billion by 2035.

The major drivers of the market are rising disposable incomes, growing consumer focus on appearance and aesthetics, increasing public awareness regarding eyecare, rising demand from the developing regions, increasing prevalence of visual deficiencies and ophthalmic disorders, and growing technological advancements.

The key trends guiding the growth of the eyewear market include the availability of premium and customised eyewear products and the increasing purchases from online stores.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific, with Europe accounting for the largest market share.

Spectacles represent the leading product type in the market.

The significant segments based on gender include men, women, and unisex.

The major distribution channels of the product include optical stores, independent brand showrooms, online stores, and retail stores.

The major players in the market are Luxottica Group S.p.A., Essilor of America, Inc., Johnson & Johnson Vision Care, Inc. (Johnson & Johnson Medical GmbH), Safilo Group S.p.A, Alcon Vision LLC, Prada S.p.A., Oakley, Inc., The Cooper Companies Inc., Silhouette International Schmied AG, and LVMH Group, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Gender |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.