Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

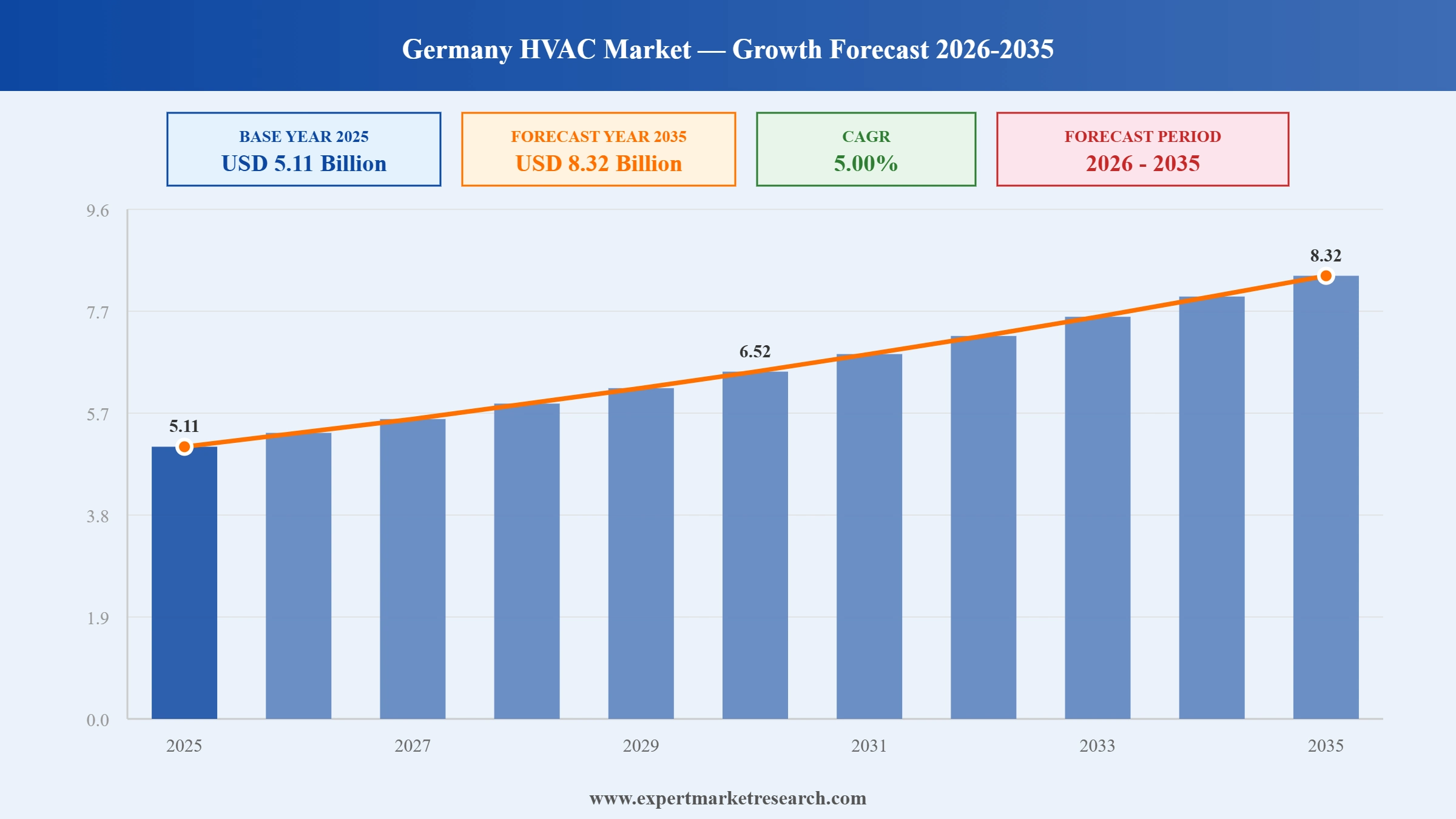

The Germany HVAC market reached a value of USD 5.11 Billion in 2025 and is projected to expand at a CAGR of around 5.00% during the forecast period of 2026-2035. Stringent EU and German energy efficiency regulations accelerating the replacement of gas boilers with heat pumps, strong retrofit demand across the large German building stock, growing adoption of energy-efficient ventilation and cooling systems, and government BEG subsidies of up to 70% for heat pump installations are driving Germany HVAC market growth. The market is expected to reach USD 8.32 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Germany HVAC market is driven by the Building Energy Act heat transition, BEG heat pump subsidies, EU F-Gas phase-down, ISH Frankfurt trade fair showcasing heat pump innovation, and the fact that 50% of EU energy consumption is attributed to heating and cooling.

The German government updated the BEG Heating Subsidy (Zuschuss Nr. 458), valid for projects starting after December 10, 2025, offering a 30% basic subsidy rising to 70% for eligible residential projects. The programme accelerates replacement of gas and oil heating with heat pumps, driving demand for Bosch, Vaillant, Stiebel Eltron, and Mitsubishi Electric products across Germany's residential and commercial building stock.

Germany's Building Energy Act amendments require large cities to complete municipal heat plans by mid-2026, with all other municipalities by mid-2028. The measures steer investments toward heat pumps, district heating networks, and low-carbon solutions. Around 70% of German household final energy use is for space and water heating, reinforcing the large scale of the residential HVAC retrofit market.

ISH 2025, the world's leading HVAC trade fair, was held in Frankfurt from March 17-21, 2025, with 2,000+ exhibitors from 55 countries. Bosch, Daikin, Mitsubishi, Vaillant, and Panasonic presented heat pump innovations. Daikin unveiled the Altherma 4 residential heat pump and CO2 VRV range, stating long-term growth expectations for European heat pumps despite a near-term market slowdown.

In January 2025, Carrier launched the AquaSnap 30 AWH-P, a propane-based (R290) air-to-water heat pump in eight models (4-14 kW) for European use. Units offer a COP up to 4.90, operating from -20 to 46 degrees C. The launch reflects the 2026 EU F-Gas phase-down transition to natural refrigerant heat pump designs.

Heating is the dominant Germany HVAC equipment type, driven by the shift to heat pumps under Germany's Building Energy Act and BEG subsidies. Heat Pumps are the fastest-growing product; Furnaces serve the transitional market. Bosch, Vaillant, and Stiebel Eltron are key German heat pump manufacturers.

Cooling is a significant Germany HVAC market equipment type, driven by rising summer temperatures and growing commercial building cooling requirements. Unitary Air Conditioners are dominant through split system adoption. VRF Systems serve large commercial cooling. Chillers and Cooling Towers serve industrial and data centre applications.

Ventilation is a growing Germany HVAC market equipment type, driven by indoor air quality awareness and Germany's large commercial and institutional building sector. Air-Handling Units dominate through commercial mechanical ventilation. Air Filters and Purifiers are growing through indoor air quality investment. Fans, Dehumidifiers and Humidifiers serve residential and specialist applications.

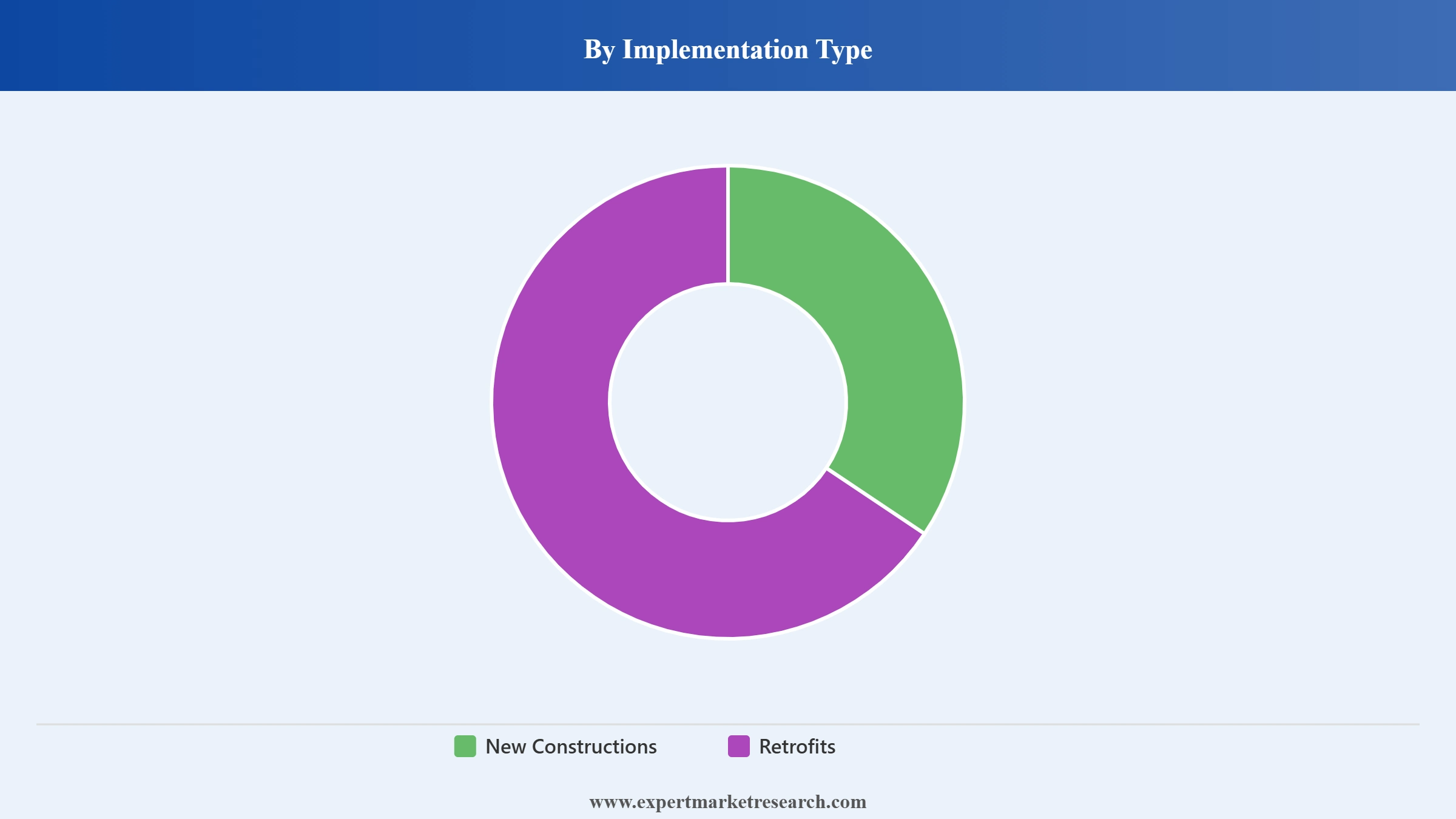

Retrofits are the largest Germany HVAC market implementation type, driven by the large existing building stock requiring energy upgrades to meet 2030 and 2045 climate targets. Germany's renovation rate needs to increase from 1% to 2.5%. BEG subsidies support residential and commercial retrofit projects. New Constructions are growing through active building activity.

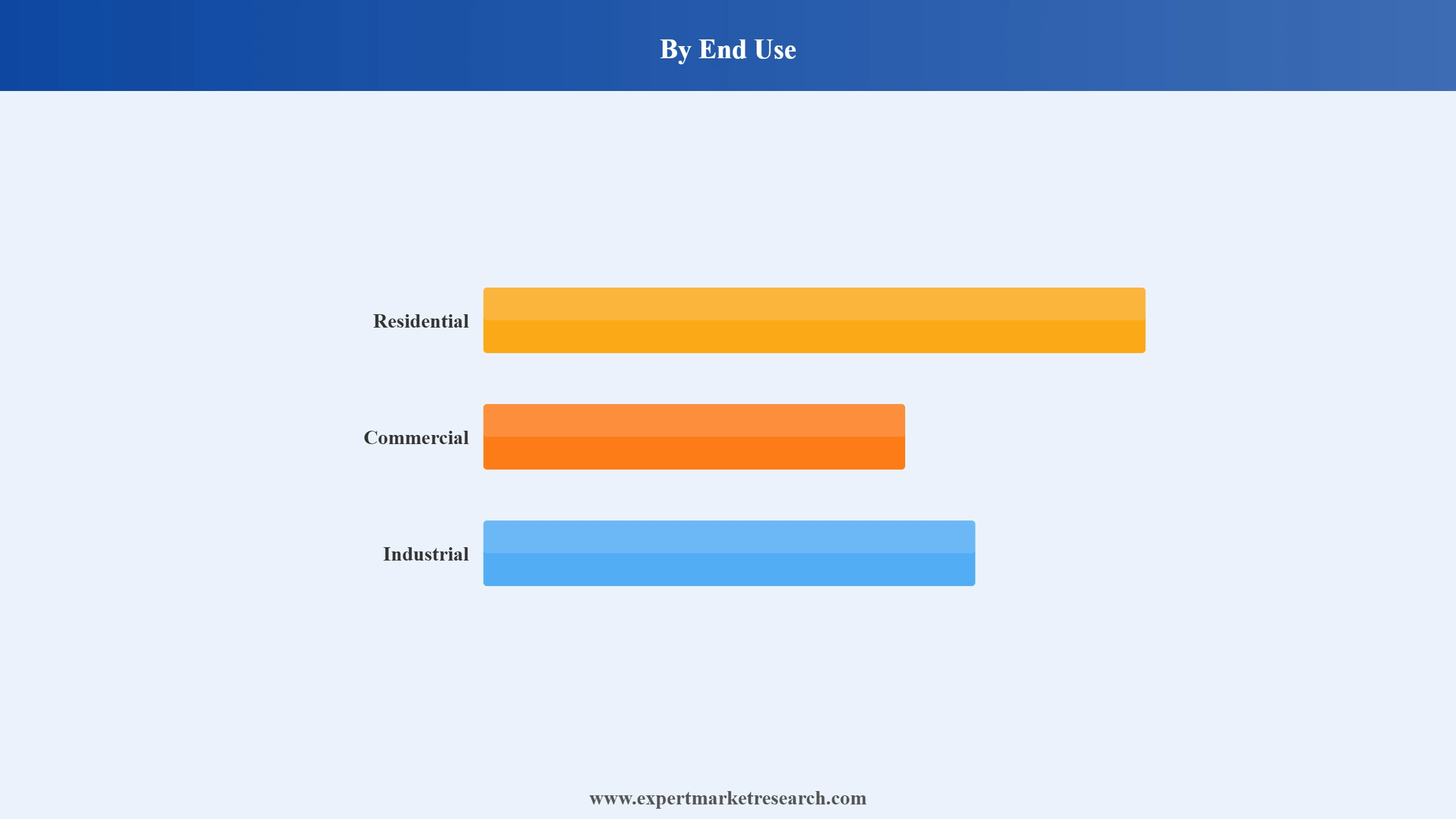

Residential is a significant Germany HVAC market end use, driven by the transition from gas boilers to heat pumps across approximately 12 million German homes. BEG subsidies of up to 70% drive residential heat pump adoption. Around 70% of German household energy use is for space and water heating. Commercial and Industrial are significant through their large and diverse building portfolios.

The Expert Market Research's report titled “Germany HVAC Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

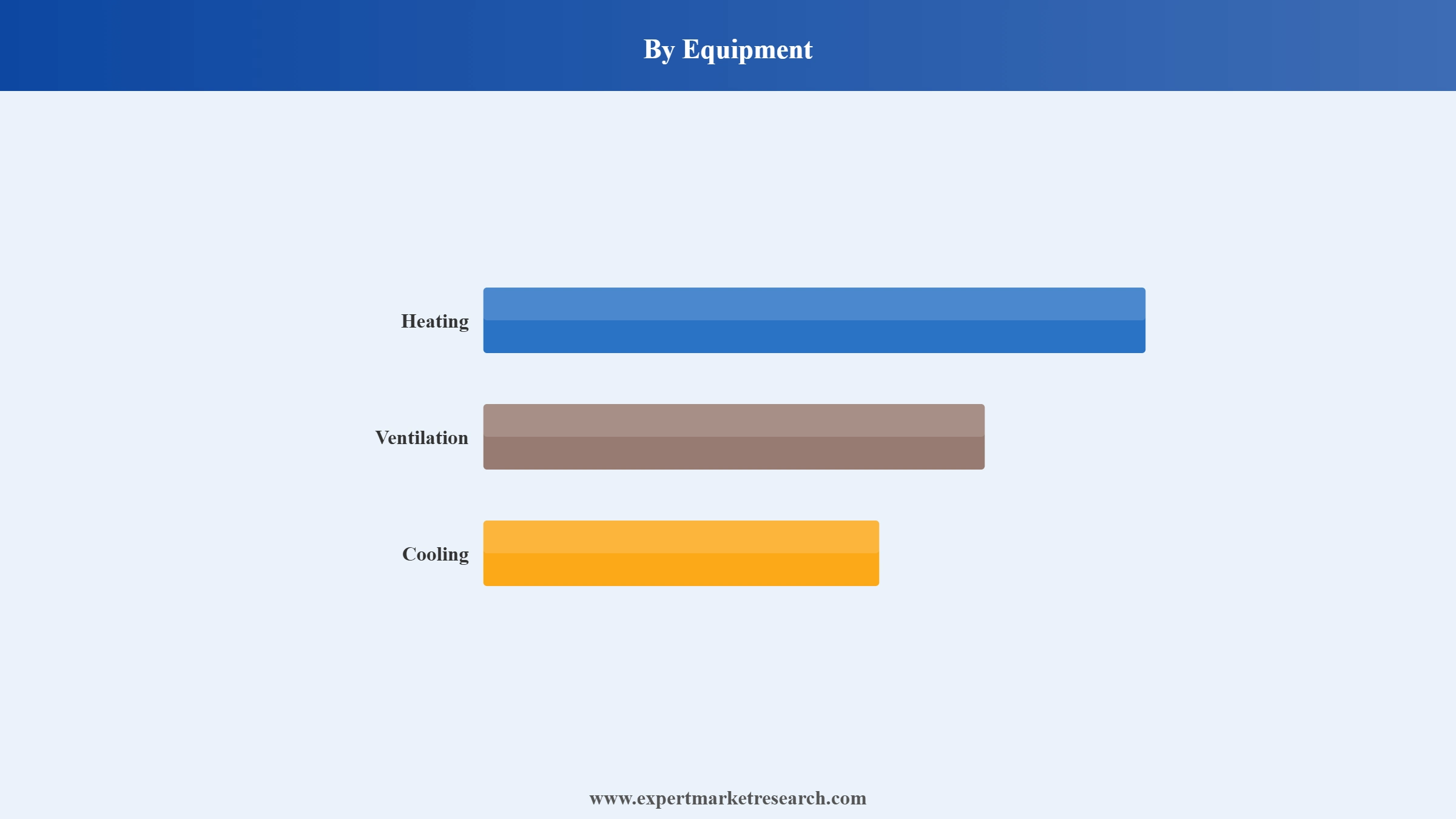

Market Breakup by Equipment

Key Insight: Heating leads as the primary Germany HVAC equipment type, driven by heat pump uptake and retrofit demand. Heating includes Heat Pumps, Furnaces, and Unitary Heaters. Ventilation includes Air-Handling Units, Air Filters and Purifiers, Ventilation Fans, Dehumidifiers and Humidifiers, and Others. Cooling includes Unitary Air Conditioners, VRF Systems, Chillers, Coolers, Cooling Towers, and Others.

Market Breakup by Implementation Type

Key Insight: Retrofits represent the largest Germany HVAC implementation type, driven by energy upgrade requirements across the aging building stock. New Constructions are growing through continued residential and commercial development.

Market Breakup by End Use

Key Insight: Commercial is a prominent Germany HVAC end use, supported by the large office, retail, healthcare, and institutional building sector. Residential holds notable importance through the large scale heat pump replacement programme. Industrial serves the heating and cooling needs of manufacturing and process operations.

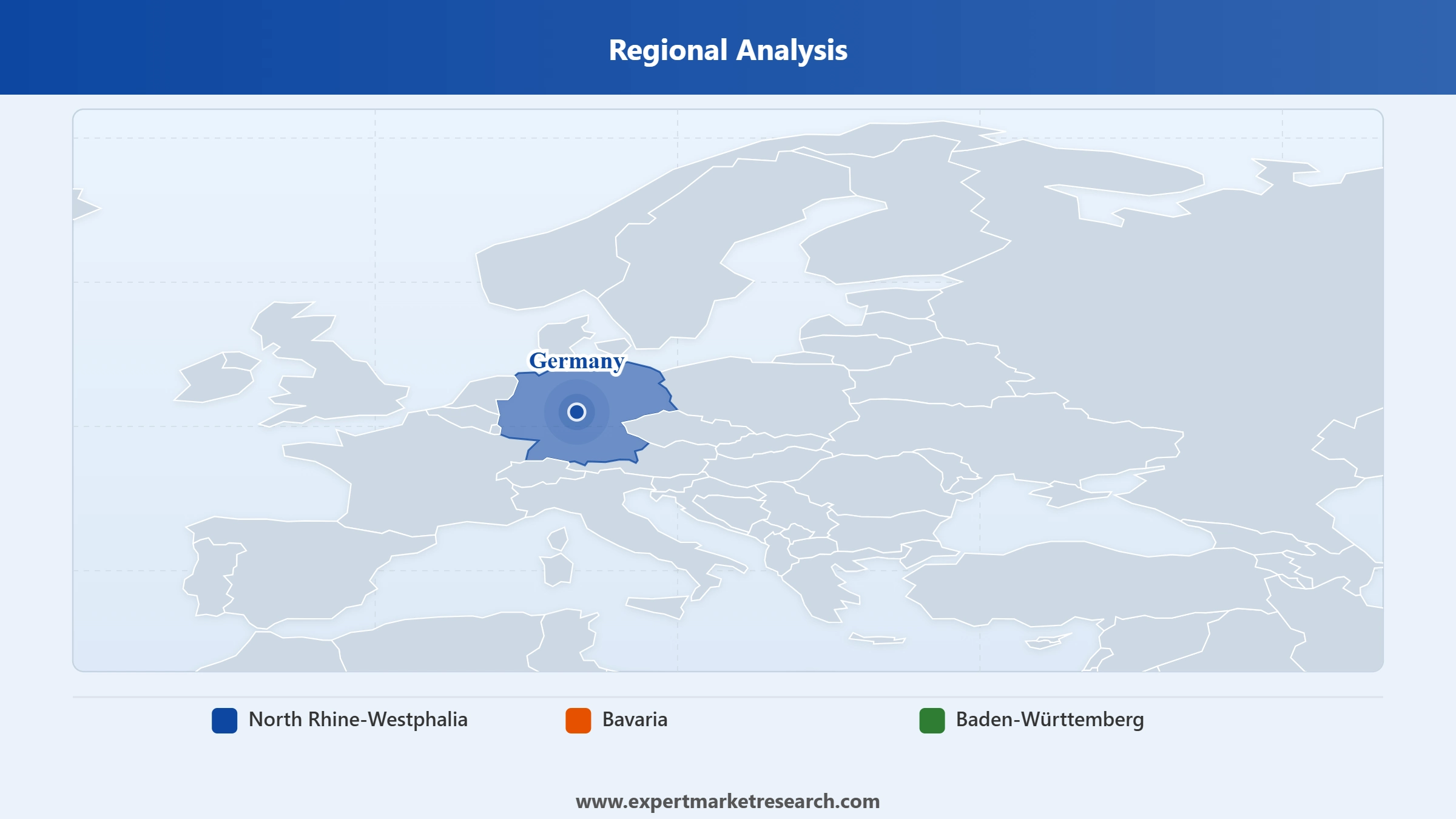

Market Breakup by Region

Key Insight: North Rhine-Westphalia ranks as the largest Germany HVAC region, being the country's most populous state with a broad commercial and industrial building stock. Bavaria and Baden-Württemberg are significant regions, together hosting 20 of Germany's 26 heat pump manufacturing sites.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Equipment, Heating is the dominant equipment type in the Germany HVAC market

Heating commands the largest Germany HVAC market share by equipment through the government-mandated shift from gas boilers to heat pumps and sustained retrofit demand across Germany's large residential and commercial building stock. Ventilation is a significant equipment type through mechanical ventilation and air quality solutions. Cooling is a growing type through rising temperature demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Implementation Type, Retrofits are the dominant implementation type in the Germany HVAC market

Retrofits command the largest Germany HVAC market share by implementation type through the large-scale energy efficiency upgrade programme across Germany's existing buildings. New Constructions are a growing type through building activity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, Commercial and Residential are the dominant end uses in the Germany HVAC market

Commercial and Residential command the largest Germany HVAC market shares by end use through the large German commercial property sector and the residential heat pump replacement programme. Industrial is a significant end use through process heating and cooling requirements.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North Rhine-Westphalia is the largest Germany HVAC market region driven by Germany's most populous state with approximately 18 million residents.

Also it is driven by a large commercial and industrial building stock, and strong institutional investment in energy-efficient HVAC systems. North Rhine-Westphalia leads the Germany HVAC market through its large residential, commercial, and industrial building base and significant infrastructure investment. Bavaria and Baden-Württemberg are major HVAC regions hosting the majority of Germany's heat pump manufacturing facilities and strong commercial HVAC investment. Germany's national heat transition policy drives HVAC demand uniformly across all regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Germany HVAC market is competitive, with German engineering companies, Japanese electronics manufacturers, Swedish specialists, and global HVAC leaders competing through heat pump innovation and energy efficiency performance.

Robert Bosch GmbH is a Germany-based global engineering company with a dominant Germany HVAC market presence through its Bosch Home Comfort Group and Buderus brand systems. Bosch reported an 84% rise in heat pump sales in Germany in 2023 and serves the market with heat pumps, boilers, and ventilation across all segments.

Mitsubishi Electric Corporation is a Japan-based global electronics and electrical equipment company with a significant Germany HVAC market presence through its heat pump, VRF, split system air conditioner, and industrial cooling product range. Mitsubishi Electric serves Germany's commercial and residential HVAC market with energy-efficient heating and cooling systems leveraging its inverter technology and heat recovery expertise.

Alfa Laval AB is a Sweden-based global heat transfer company with a significant Germany HVAC market presence through heat exchangers, district energy heat pumps, and industrial cooling solutions. Alfa Laval serves Germany's commercial buildings, district heating, and industrial cooling markets aligned with Germany's decarbonisation agenda.

Panasonic Holdings Corp. is a Japan-based global electronics and HVAC company with a significant Germany HVAC market presence through its Aquarea heat pump range and VRF commercial air conditioning systems. Panasonic serves Germany's residential heat pump replacement market and commercial ventilation and cooling sectors with energy-efficient products meeting EU energy performance standards.

Other key players include Vaillant GmbH, Johnson Controls-Hitachi Air Conditioning Company, Systemair AB, Carrier Global Corp., Ariston Holding N.V., and Kingspan Group Plc (Colt International GmbH), among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers market data and strategic analysis for Germany's HVAC market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Germany HVAC market reached an approximate value of USD 5.11 Billion.

The market is projected to grow at a CAGR of 5.00% between 2026 and 2035.

The market is assessed to witness a healthy growth in the forecast period to reach around USD 8.32 Billion in 2035.

The different end uses of HVAC in the market include residential, commercial, and industrial.

The different types of implementations of HVAC include new constructions and retrofits.

The different equipment types considered in the market report are heating, ventilation, and cooling.

The major regions in the market include North Rhine-Westphalia, Bavaria, and Baden-Württemberg.

The key players in the market include Robert Bosch GmbH, Mitsubishi Electric Corporation, Alfa Laval AB, Panasonic Holdings Corp., Vaillant GmbH, Johnson Controls-Hitachi Air Conditioning Company, Systemair AB, Carrier Global Corp., Ariston Holding N.V., Kingspan Group Plc (Colt International GmbH), and other regional and international manufacturers.

Key strategies driving the market include rapid adoption of energy-efficient and smart HVAC systems, partnerships to expand technological capabilities, increased investments in heat pumps and renewable-integrated solutions, and the development of sustainable products aligned with Germany’s climate-neutral building goals.

The major challenges that the Germany HVAC market faces include high installation and upgrade costs, evolving regulatory compliance requirements, shortage of skilled HVAC technicians, and supply chain delays affecting the availability of components and finished systems.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Equipment |

|

| Breakup by Implementation Type |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.