Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

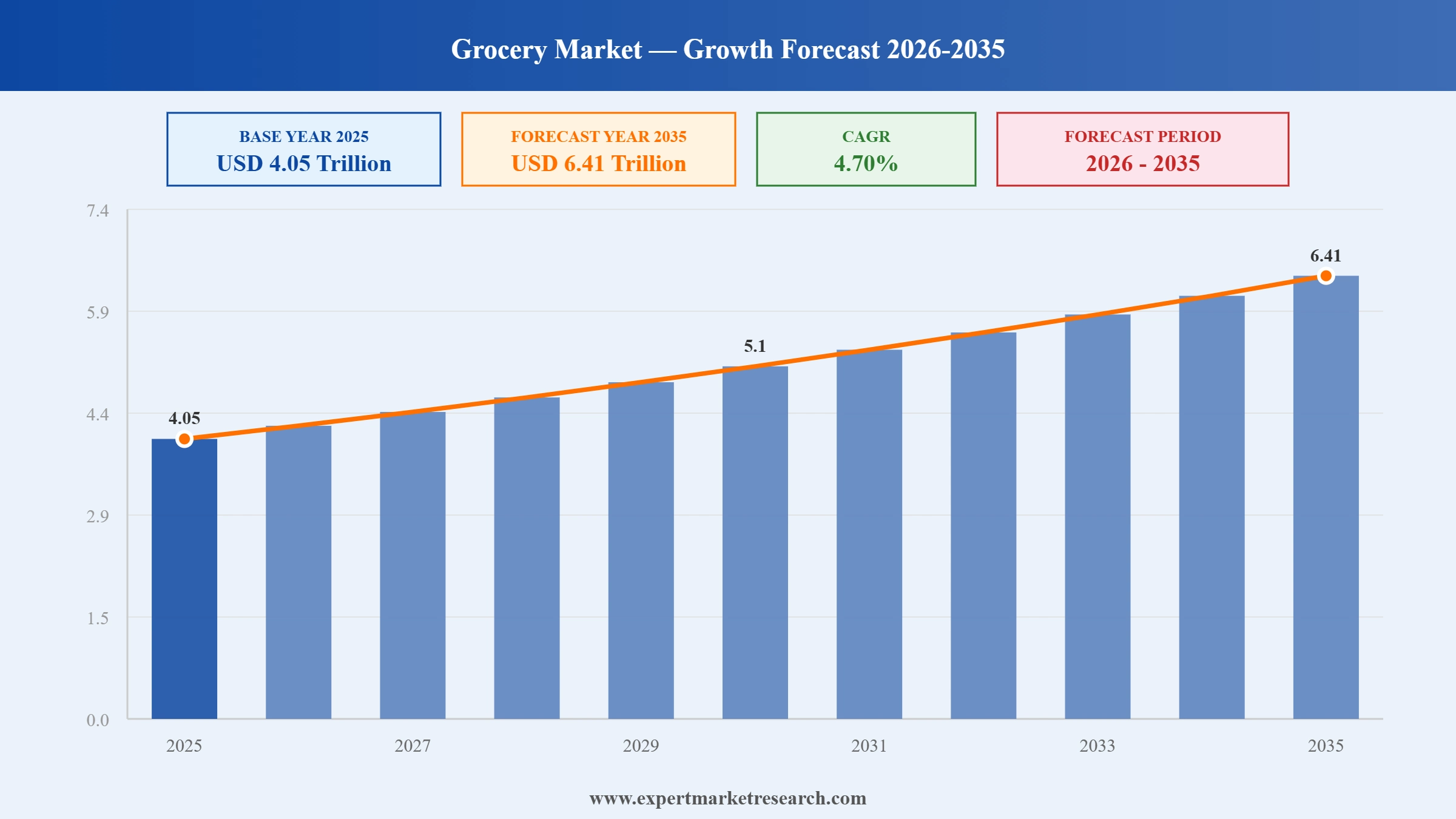

The global grocery market reached a value of USD 4.05 Trillion in 2025 and is projected to expand at a CAGR of around 4.70% during the forecast period of 2026-2035. Major FMCG portfolio restructuring including Mars Inc.'s USD 36 Billion acquisition of Kellanova, Kraft Heinz's planned split, Unilever's ice cream divestiture, and the accelerating shift to clean-label and health-focused grocery products are reshaping the global grocery market. The market is expected to reach USD 6.41 Trillion by 2035.

As reported by Market place, grocery inflation cooled in March 2026 but food prices continued climbing, with tomatoes hit hard by a 17% tariff on Mexican imports. The USDA forecast food-at-home prices to rise over 3% in 2026, reflecting persistent pressure from trade policy, shrinking cattle herds, and coffee shortages that collectively reshape consumer spending patterns across the grocery market.

According to Grocery Dive, Walmart announced plans to remodel more than 650 supercenters and Neighborhood Market stores and open around 20 new locations over the next two years. So far in 2026, the retailer has opened four supercenters across Florida and California, signaling aggressive expansion as competition from Aldi, Amazon, and discount grocers intensifies across the US market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global grocery market is driven by FMCG mega-mergers which are essentially reshaping the competitive landscape, consumer demand for clean-label and functional food products, e-commerce grocery penetration accelerating through quick-commerce platforms, health-conscious dietary shifts, and the expansion of private label brands by major retailers.

Mars, Incorporated completed its USD 36 Billion acquisition of Kellanova in December 2025, one of the largest FMCG transactions in history. The deal brings Pringles, Cheez-It, Pop-Tarts, Eggo, and Rice Krispies Treats under the Mars umbrella alongside M&M's, Snickers, and Wrigley's chewing gum. The acquisition makes Mars a global snack powerhouse and directly reshapes grocery shelf allocation across North America, Europe, and Asia Pacific supermarkets for both savoury and sweet snack categories.

Clean-label food and grocery products accounted for approximately USD 145 Billion in global retail sales in FY25 per Ingredion research, reflecting the accelerating consumer preference for simple ingredient lists, free-from claims, and minimally processed grocery products. Nestlé, General Mills, Danone, and Coca-Cola expanded their clean-label and functional product ranges in 2025. GLP-1 drug adoption among consumers is also driving demand for high-protein and low-calorie grocery formulations.

The Kraft Heinz Company announced plans in 2025 to split into two separate publicly traded companies, separating its snack foods and condiments/meals divisions. The split follows consecutive years of volume decline and brand reinvestment challenges. Kraft Heinz, Danone, and General Mills all reported volume pressure in 2025 as consumers traded down to private label grocery brands, accelerating retailer own-label market share growth globally.

Unilever plc completed the sale of its global ice cream business in 2025, including the Ben and Jerry's, Magnum, Wall's, and Cornetto brands, establishing the business as an independent standalone company. The divestiture is part of Unilever's portfolio simplification strategy to refocus investment on beauty, personal care, and home care grocery products. Unilever's restructuring reflects the broader global FMCG trend of portfolio rationalisation and value-focused brand strategy.

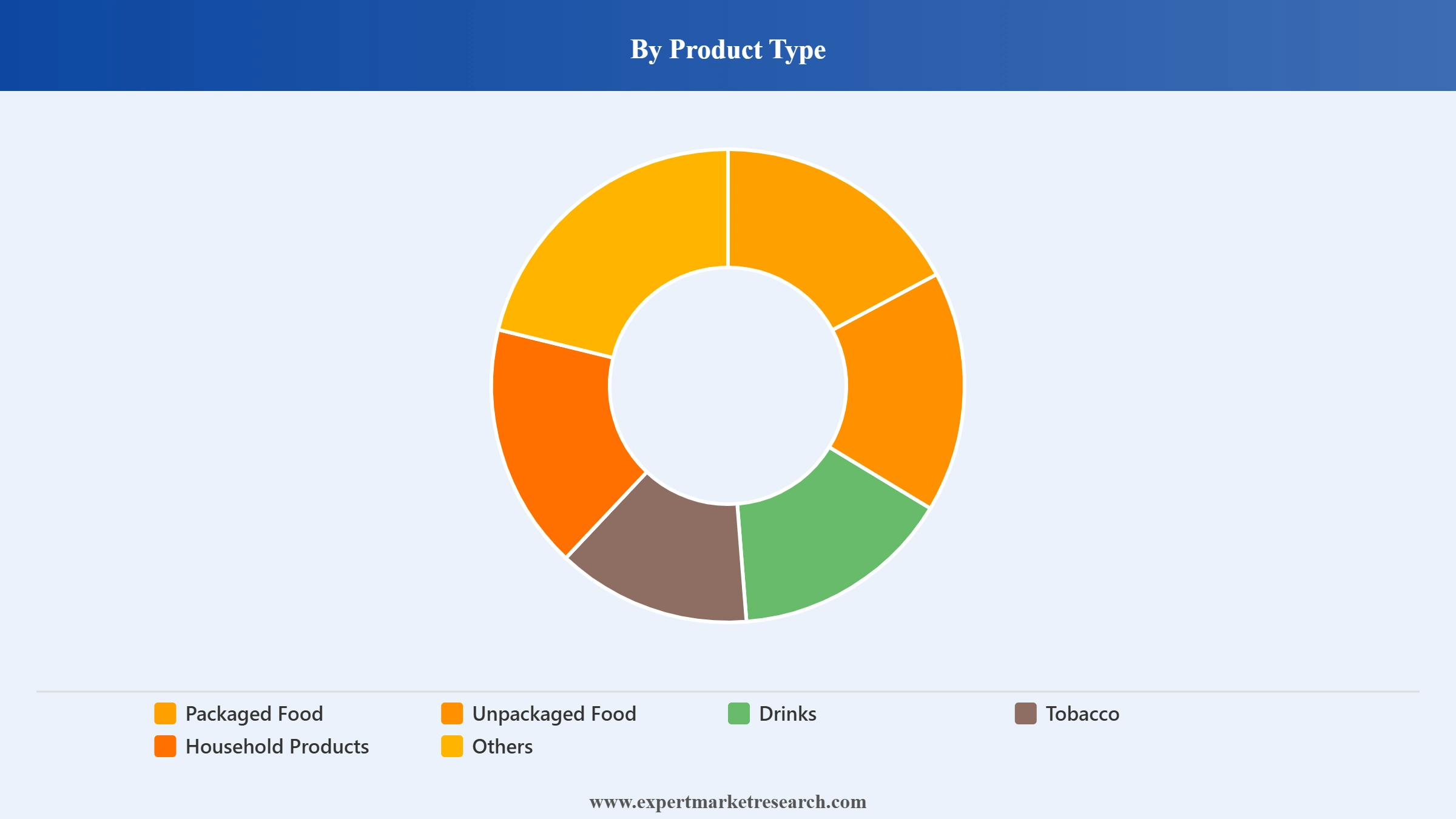

Packaged Food is the dominant global grocery product type through FMCG brand infrastructure and convenience demand. Nestlé, Mondelez, Kraft Heinz, and General Mills command the largest packaged food share. Unpackaged Food is significant through fresh produce markets in Asia Pacific and Latin America. Drinks command significant value through Coca-Cola, PepsiCo, and Danone brands.

Unpackaged Food is a significant global grocery segment through fresh fruit, vegetables, meat, and bakery demand across global supermarkets and traditional wet markets. Household Products are significant through Procter and Gamble, Unilever, and Reckitt household care brands. Tobacco is declining through regulatory restrictions across major markets. Others include pet food, infant nutrition, and health supplements.

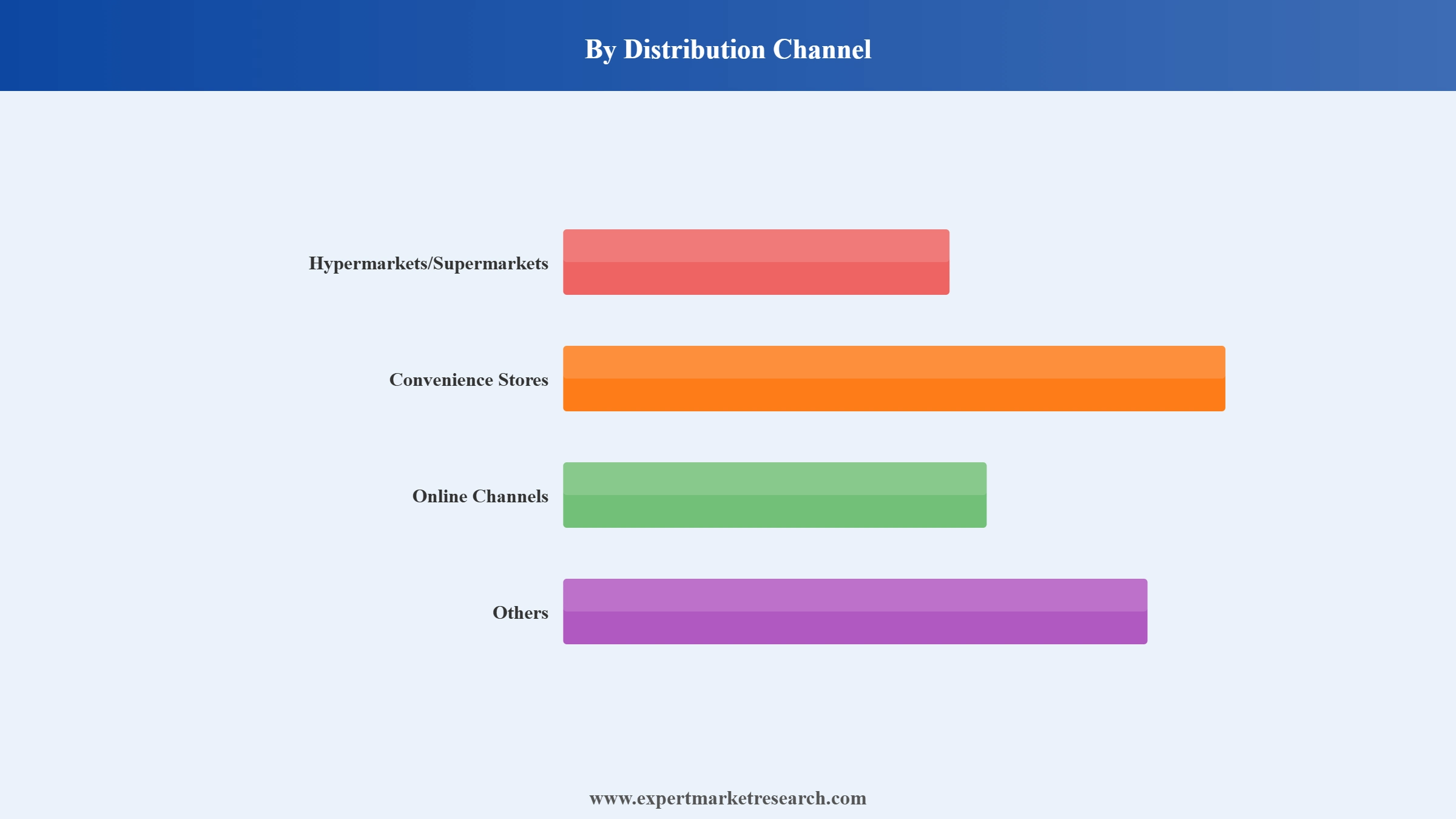

Online Channels are the fastest-growing global grocery distribution channel through e-commerce penetration in China, the US, UK, and South Korea. Hypermarkets and Supermarkets remain the dominant channel through physical retail scale. Convenience Stores are growing through urban proximity and on-the-go consumption patterns globally.

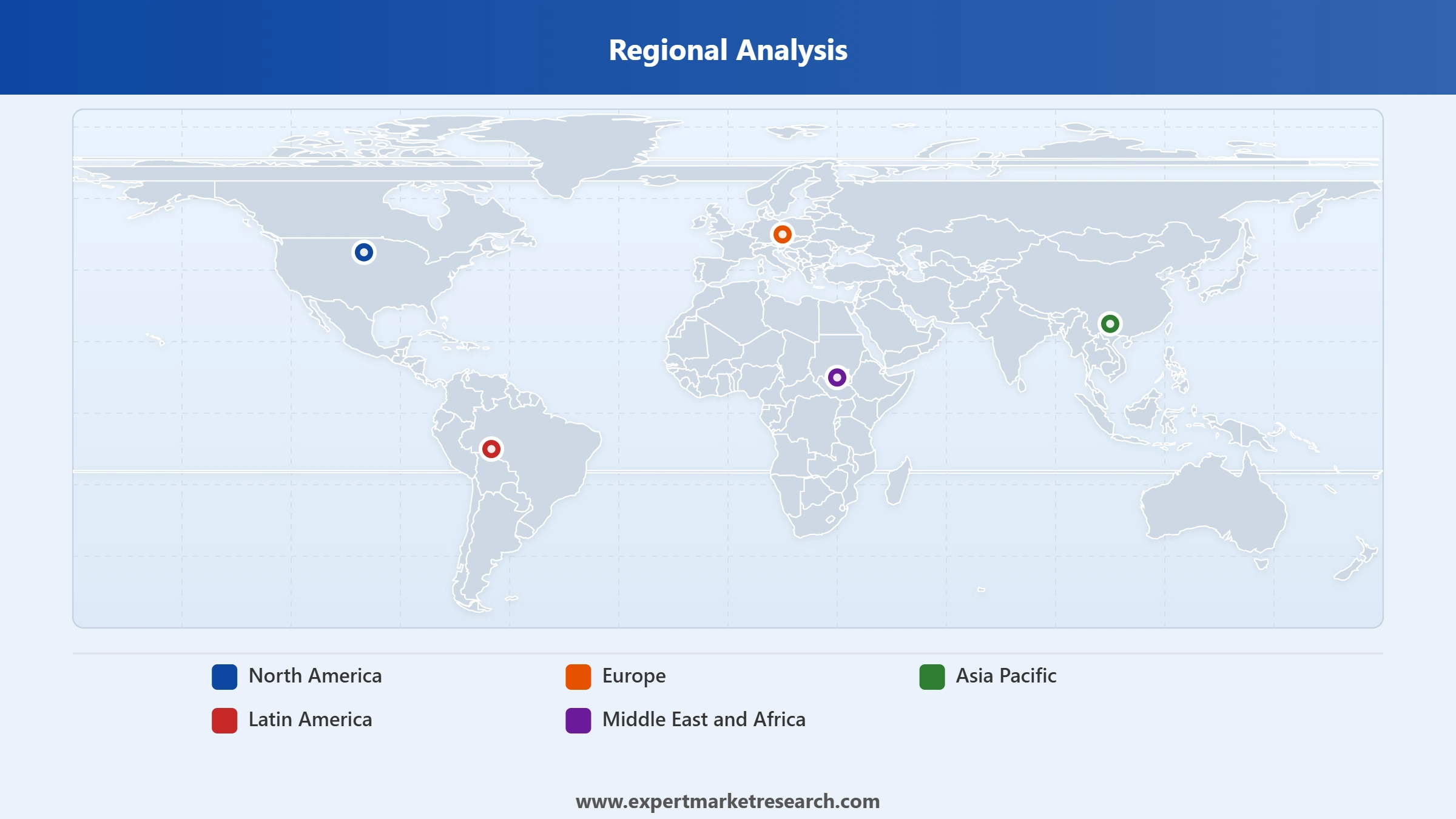

North America is a significant global grocery market region through the United States' dominant grocery retail infrastructure led by Walmart, Costco, Kroger, and Amazon Fresh. Europe is significant through organised retail chains in Germany, UK, France, and Italy. Latin America and MEA are growing regions through urbanisation and modern retail expansion.

Asia Pacific is the dominant global grocery region through China, India, Japan, and ASEAN population scale and rapid e-commerce grocery growth. China's online grocery market leads globally through Alibaba, JD.com, and Meituan. India's grocery market is expanding through Reliance Retail and quick-commerce platforms. Japan and South Korea lead in premium packaged food innovation.

The Expert Market Research's report titled “Global Grocery Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Packaged Food is the dominant global grocery product type. Drinks are significant through Coca-Cola and PepsiCo brand infrastructure. Household Products are significant. Unpackaged Food is growing in Asia Pacific. Tobacco is declining.

Market Breakup by Distribution Channel

Key Insight: Hypermarkets/Supermarkets are the dominant global grocery channel. Online Channels are fastest-growing. Convenience Stores are growing through urban proximity demand.

Market Breakup by Region

Key Insight: Asia Pacific is the dominant global grocery region. North America and Europe are significant. Latin America and MEA are growing through urbanisation and modern retail expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, Packaged Food is the dominant product in the global grocery market

Packaged Food commands the largest global grocery market share, anchored by FMCG brand infrastructure across Nestlé, Kraft Heinz, Mondelez, and Danone and consumer preference for convenience-driven, shelf-stable products. Mars Inc.'s USD 36 Billion acquisition of Kellanova in December 2025 expanded the packaged food segment's snack and breakfast category control globally. Drinks hold a significant share through Coca-Cola and PepsiCo's global grocery distribution, while Household Products are significant through P&G, Unilever, and Reckitt. Others encompass pet food, infant nutrition, and health supplement categories.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, Hypermarkets/Supermarkets dominate while Online Channels are fastest-growing

Hypermarkets and Supermarkets command the largest global grocery distribution channel share through the dominant scale of Walmart, Costco, Carrefour, and Tesco international store networks. Online Channels are the fastest-growing channel as quick-commerce platforms in China, South Korea, the UK, and the US drive e-grocery penetration to record highs. Convenience Stores hold a significant share through urban proximity and on-the-go demand, particularly in Japan, South Korea, and the United States. Others include specialist food retail, membership club stores, and forecourt petrol station grocery formats.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the dominant global grocery market region driven by China, India, Japan, ASEAN, and Australia's combined population of over 4.5 billion

Other factors driving it are rapid urbanisation, expanding middle class, and the world's fastest-growing online grocery channel led by Alibaba, JD.com, and quick-commerce platforms including Meituan Maicai. North America is the second-largest global grocery region through the United States' Walmart, Costco, Kroger, and Amazon Fresh retail infrastructure, while Europe is significant through Germany, UK, France, and Italy's organised modern grocery retail Asia Pacific leads the global grocery market through population scale and e-commerce growth. North America is significant through the United States. Europe is significant through organised retail. Latin America and MEA are growing through urbanisation and modern retail penetration.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global grocery market is highly competitive, with Swiss food conglomerates, American FMCG leaders, British-Dutch household products multinationals, and US beverage giants competing through product innovation, portfolio M&A, sustainable packaging, and omnichannel distribution strategies.

Nestlé S.A. is a Swiss multinational food and beverage company with a dominant global grocery market presence through its portfolio of over 2,000 brands across packaged food, beverages, dairy, and nutrition. Nestlé reported net sales of CHF 91.4 Billion in FY24 and is restructuring its portfolio to focus on high-growth health science, premium coffee, and pet care categories. In 2025, Nestlé announced plans to sell its Blue Bottle Coffee chain as part of continued portfolio focus.

The Procter and Gamble Company is a US-based FMCG conglomerate with a significant global grocery market presence through its household products portfolio including Tide, Ariel, Pampers, Gillette, and Oral-B across grocery retail. P&G serves global grocery channels through mass retail, e-commerce, and club store channels. P&G reported strong household and personal care grocery performance driven by premiumisation in the US, Europe, and Asia Pacific.

Unilever plc is a British-Dutch FMCG multinational with a significant global grocery market presence through Dove, Rexona, Lipton, Knorr, and Hellmann's brands across personal care, food, and home care grocery categories. In 2025, Unilever completed the divestiture of its ice cream business, refocusing investment on beauty, personal care, and household grocery products. Unilever serves grocery markets across 190+ countries.

The Coca-Cola Company is a US-based global beverage company with a dominant global grocery market presence through Coca-Cola, Sprite, Fanta, Powerade, Minute Maid, and Dasani brands in the drinks grocery category. Coca-Cola reported flat unit-case volume growth in FY25 and is expanding its portfolio through functional beverages, energy drinks, and zero-sugar variants to address health-conscious grocery consumers.

Other key players include PepsiCo Inc., MONDELEZ INTERNATIONAL INC., Danone SA, General Mills Inc., Kraft Heinz Co., and Kellanova, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides comprehensive market sizing, segmentation analysis across product type and distribution channel, key trends and competitive benchmarking for the global grocery market. Coverage spans historical data from 2019 through 2035, equipping manufacturers, retailers, and investors with the intelligence required for market entry, product positioning, and investment decisions. Reach out to our team to access the complete report or request a customised version aligned to your specific research objectives.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global grocery market reached an approximate value of USD 4.05 Trillion.

The market is projected to grow at a CAGR of 4.70% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 6.41 Trillion by 2035.

Key strategies driving the market include product innovation and diversification, private-label expansion, omni-channel integration, strategic partnerships and collaborations, mergers and acquisitions, and investment in digital platforms and supply chain modernization to enhance reach, efficiency, and consumer engagement.

The key trends aiding the market include pre-ordering facilities in online shopping, the rise of omnichannel strategy, and the introduction of subscription models.

Regions considered in the market are North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Based on product type, market segmentations include packaged food, unpackaged food, drinks, tobacco, and household products, among others.

Different distribution channels are packaged food, unpackaged food, drinks, tobacco, and household products, among others.

The key players in the market include Nestlé S.A., The Procter & Gamble Company, Unilever plc, The Coca-Cola Company, PepsiCo, Inc., MONDELEZ INTERNATIONAL INC., Danone SA, General Mills Inc., Kraft Heinz Co., and Kellanova, among others.

Key challenges that the global grocery market players face includes intense competition, fluctuating raw material costs, regulatory compliance across regions, evolving consumer preferences, supply chain disruptions, and the need for continuous digital transformation to meet online and convenience-driven demand.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.