Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

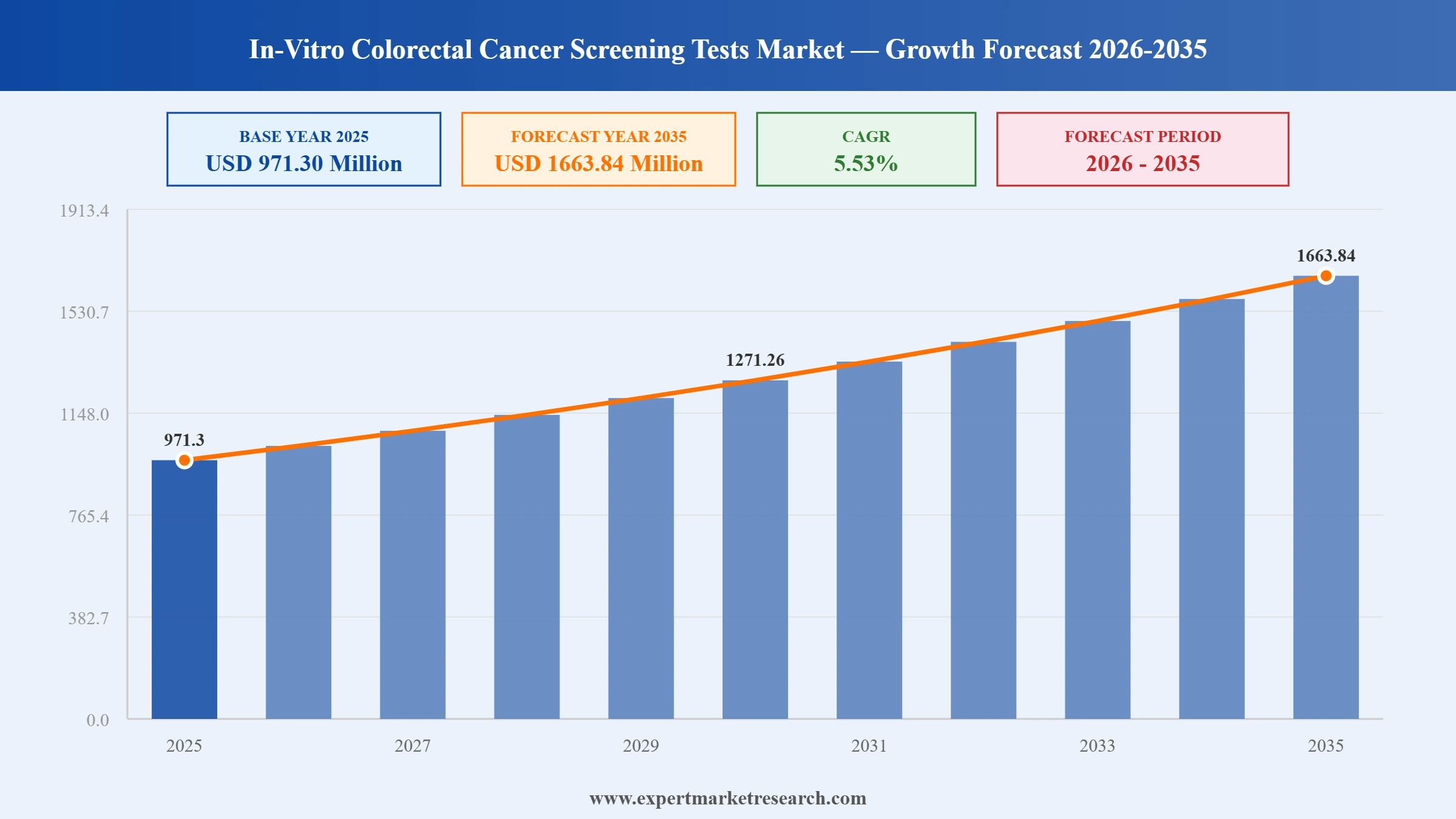

The in-vitro colorectal cancer screening tests market was valued at USD 971.30 Million in 2025. It is poised to grow at a CAGR of 5.53% during the forecast period of 2026-2035, reaching USD 1663.84 Million by 2035. The market is driven by the rising prevalence of colorectal cancer globally, growing adoption of minimally invasive colorectal cancer screening procedures, and increasing government-backed early detection initiatives across developed and emerging economies.

Read more about this report - Request a Free Sample

In-vitro colorectal cancer screening tests are diagnostic procedures performed outside the body to detect adenomas, polyps, and early markers of colorectal cancer. Common tests include fecal occult blood tests (FOBT), fecal immunochemical tests (FIT), CRC DNA screening tests, and biomarker tests. As per Expert Market Research (EMR), the market was valued at USD 971.30 Million in 2025, driven by the expanding access to non-invasive colon cancer screening protocols, advancements in liquid biopsy platforms, and rising awareness about the benefits of early detection of colorectal cancer, collectively driving market expansion.

Rising Prevalence of Colorectal Cancer Fuels Demand for Early-Stage Diagnostic Solutions

Colorectal cancer remains one of the most prevalent malignancies worldwide, ranking as the third most diagnosed cancer globally. According to the World Health Organization (WHO), colorectal cancer accounts for nearly 10% of all cancer-related deaths, with incidence continuing to rise due to aging populations, sedentary lifestyles, and dietary changes. This growing burden is directly fuelling adoption of fecal occult blood tests, fecal immunochemical tests (FIT), and CRC DNA screening tests as frontline diagnostic tools.

Read more about this report - Request a Free Sample

The market is witnessing a strong trend toward non-invasive, highly sensitive diagnostic technologies.

Technological Advancements in Non-Invasive Diagnostics are Reshaping the Colorectal Cancer Screening Landscape

The market is witnessing a significant shift toward non-invasive screening solutions driven by patient preference for convenience and improved compliance. The development of advanced stool DNA tests, liquid biopsy platforms, and next-generation sequencing tools is improving sensitivity in the early detection of colorectal cancer. Blood-based biomarker tests such as Guardant Health's Shield test are broadening diagnostic capabilities. In February 2023, researchers at the University of Technology Sydney (UTS) developed a microfluidic device capable of detecting cancer cells from blood samples. This representing a notable advancement in non-invasive cancer diagnostics and liquid biopsy technologies with potential applications in colorectal cancer detection.

Market Breakup by Test Type

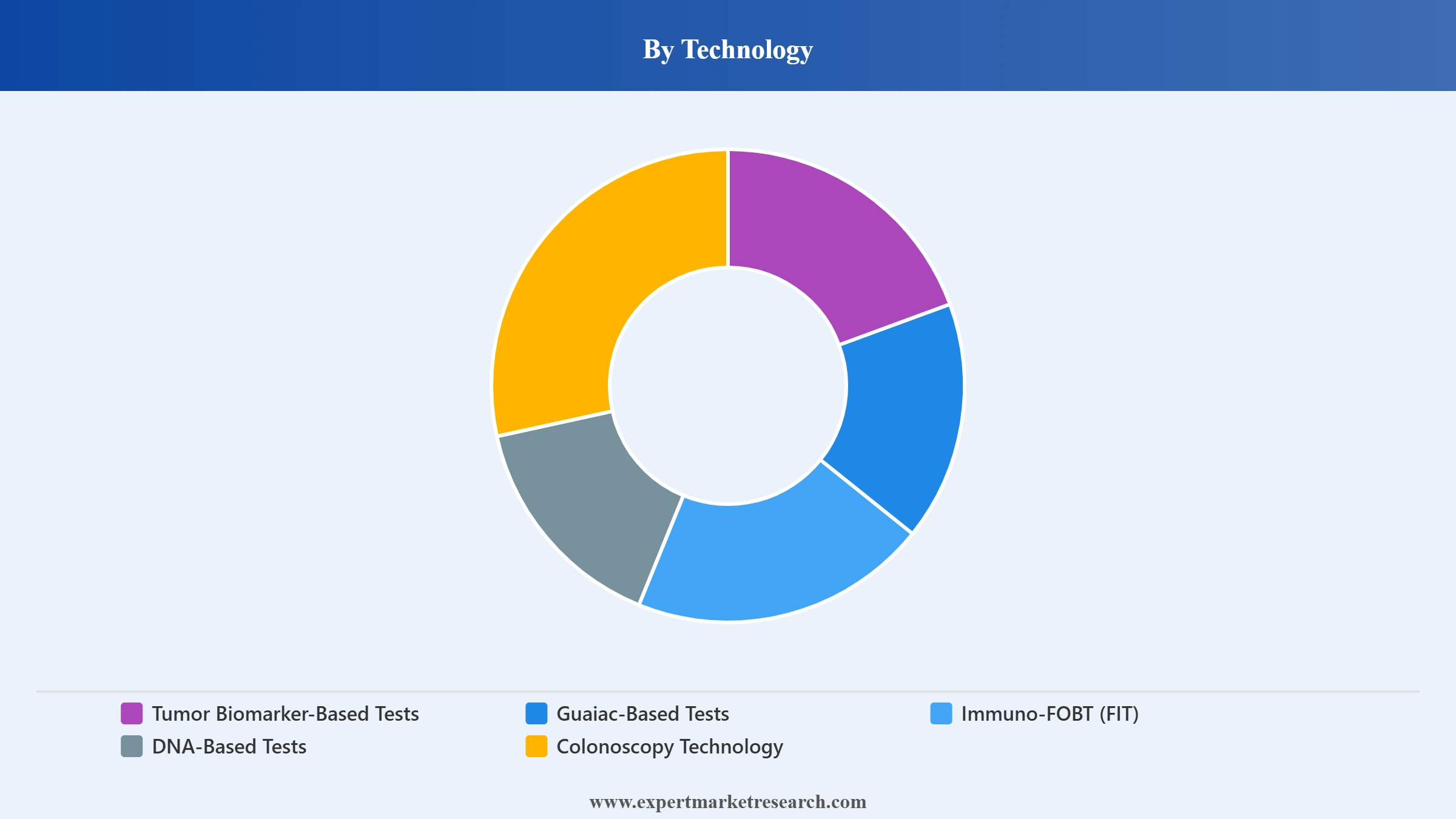

Market Breakup by Technology

Market Breakup by Collection Method

Market Breakup by End User

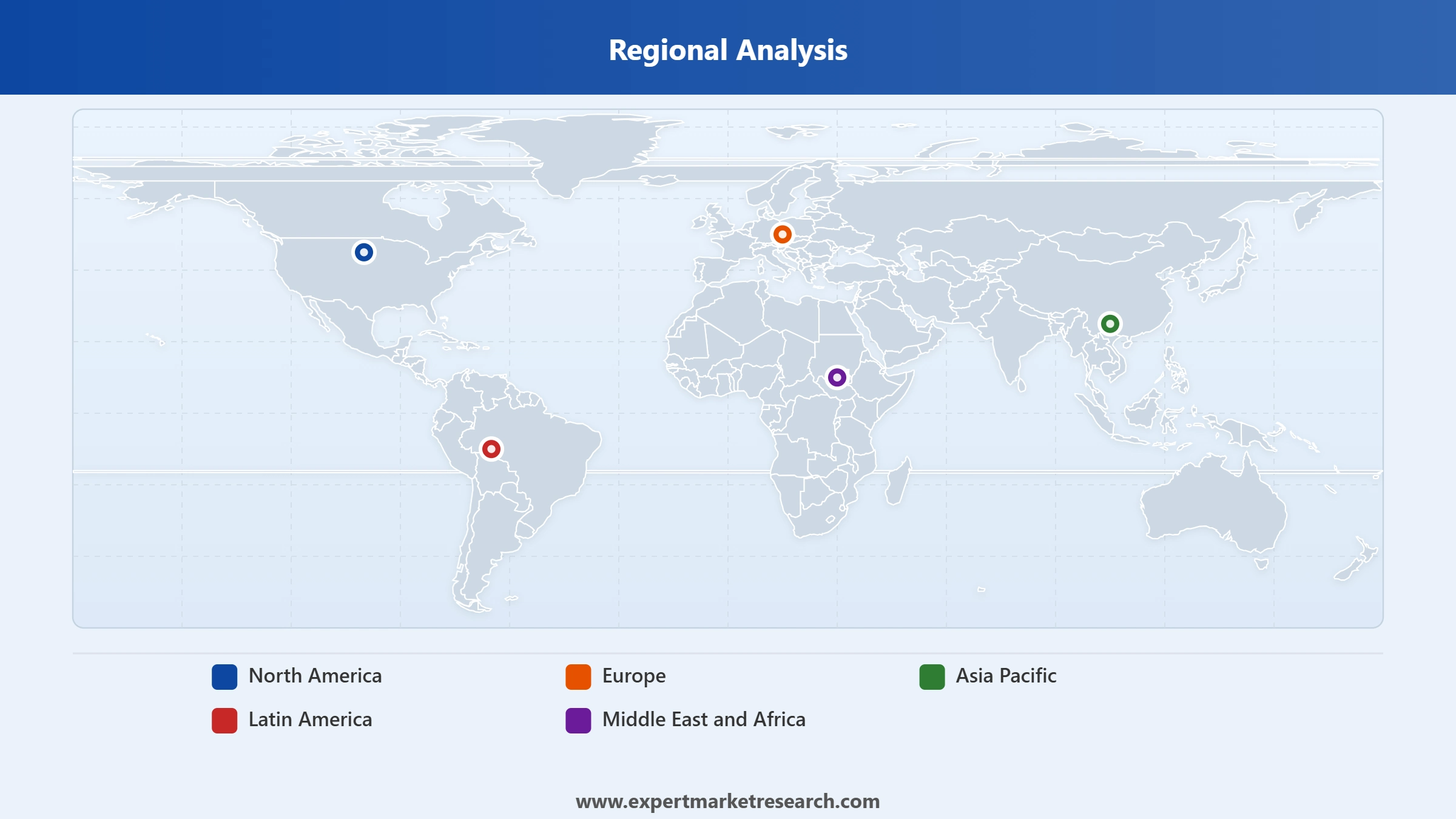

Market Breakup by Region

Read more about this report - Request a Free Sample

Biomarker Tests Segment is Expected to Witness the Fastest Growth Based on the Test Type

The market is segmented by test type into fecal occult blood test (FOBT), guaiac FOBT, immuno-FOBT (FIT), stool DNA test (sDNA), colonoscopy, flexible sigmoidoscopy, colonography (virtual colonoscopy), biomarker tests, CEA tests, and others. Among these, the biomarker tests segment is expected to witness the fastest growth during the forecast period, driven by rising demand for highly sensitive and minimally invasive colorectal cancer diagnostics. Increasing adoption of blood-based cancer screening technologies and advancements in molecular diagnostics are further supporting segment expansion. The growing burden of colorectal cancer is accelerating the need for early and accurate screening solutions, thereby strengthening demand for advanced biomarker-based testing approaches.

Read more about this report - Request a Free Sample

North America leads the global in-vitro colorectal cancer screening tests market, supported by advanced healthcare infrastructure, high colorectal cancer prevalence, and well-established national screening programs. The region benefits from strong regulatory frameworks and growing adoption of at-home fecal immunochemical test (FIT) kits. Asia Pacific is expected to register the fastest growth, driven by rising colorectal cancer incidence, improving healthcare access, and expanding reimbursement coverage for colon cancer screening procedures.

Read more about this report - Request a Free Sample

The key features of the market report comprise patent analysis, funding and investment analysis, and strategic initiatives by the leading players. The major companies in the market are as follows:

Abbott Laboratories is actively involved in colorectal cancer diagnostics through its broad oncology assay portfolio, including CEA biomarker assays and fecal occult blood testing solutions used in early cancer detection. The company’s Alinity and ARCHITECT platforms support laboratories with reliable in-vitro diagnostic capabilities, strengthening its presence in colorectal cancer screening and clinical oncology testing worldwide.

F. Hoffmann-La Roche AG plays a significant role in colorectal cancer diagnostics through its advanced pathology and molecular diagnostic solutions. The company offers VENTANA immunohistochemistry and in situ hybridization assays that support cancer biomarker detection and tissue analysis. Roche continues to strengthen laboratory efficiency and diagnostic accuracy through its automated in-vitro diagnostic platforms and oncology-focused assay portfolio.

Siemens Healthineers AG is a key player in the in-vitro colorectal cancer screening tests market, engaged in the colorectal cancer screening and oncology diagnostics sector through its extensive range of immunoassays and laboratory testing systems. The company provides oncology assay solutions and biomarker-based diagnostic technologies that assist healthcare professionals in cancer detection and disease monitoring. Its integrated diagnostic platforms enhance laboratory workflow efficiency and support precision-driven clinical decision-making.

Biohit Oyj is a Finnish biotechnology company actively involved in the in-vitro colorectal cancer screening tests market through its innovative gastrointestinal diagnostic solutions. The company offers fecal occult blood testing products and related screening technologies designed to support early detection of gastrointestinal disorders and colorectal cancer. Biohit continues to strengthen its presence in the market by focusing on cost-effective, non-invasive diagnostic innovations that improve screening accessibility and clinical efficiency.

Other key player includes Epigenomics AG, Randox Laboratories Ltd., QIAGEN N.V., Eiken Chemical Co., Ltd., Novigenix AI SA, and Exact Sciences Corporation.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$3299 $2969

$5499 $4949

$6999 $5949

$8199 $6969

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Test Type |

|

| Breakup by Technology |

|

| Breakup by Collection Method |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,299

USD 2,969

tax inclusive*

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,199

USD 6,969

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.