Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

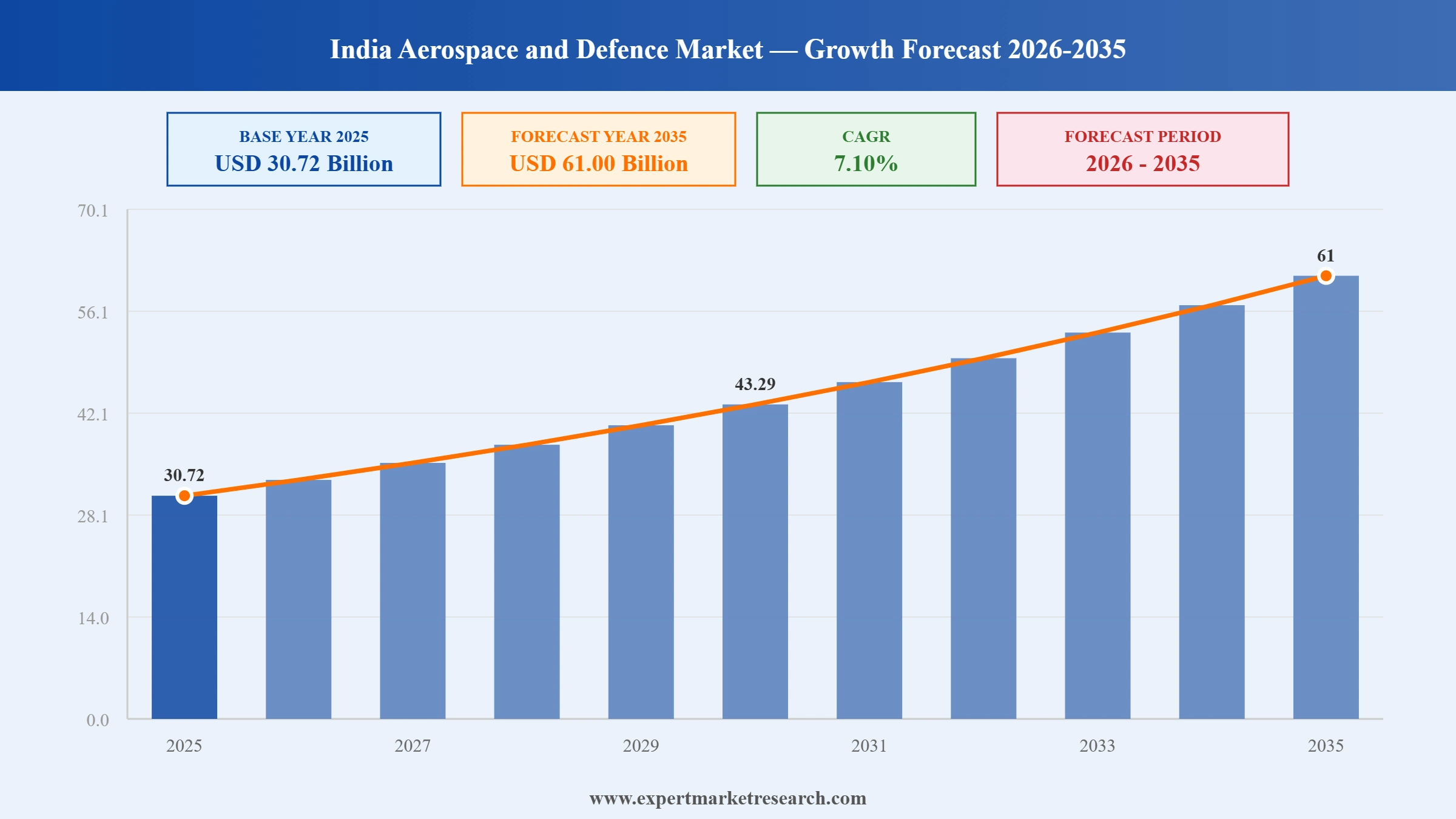

The India Aerospace and Defence Market reached a value of USD 30.72 Billion at 2025 and is projected to expand at a CAGR of around 7.10% during the forecast period of 2026-2035. With escalating defence budgets, rapid indigenisation of platforms, expanding private sector manufacturing capacity, and fast-growing civil aviation and space sectors, the market is expected to reach USD 61.00 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Aerospace and Defence Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

30.72 |

|

Market Size 2035 |

USD Billion |

61.00 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

7.10% |

|

CAGR 2026-2035 - Market by Region |

South India |

8.1% |

|

CAGR 2026-2035 - Market by Region |

East India |

7.6% |

|

CAGR 2026-2035 - Market by Platform |

Aerospace |

7.5% |

|

CAGR 2026-2035 - Market by Offerings |

Communication Systems |

8.3% |

|

2025 Market Share by Region |

West India |

27.2% |

The India Aerospace and Defence Market is undergoing a fundamental structural transformation, shaped by the government's indigenisation mandate, rising defence budgets, private sector entry, and expanding commercial aviation and space ambitions that are collectively elevating India's position from a major defence importer to an emerging global manufacturing hub.

In February 2025, U.S. President Donald Trump and Indian Prime Minister Narendra Modi jointly announced the U.S.-India COMPACT (Catalyzing Opportunities for Military Partnership, Accelerated Commerce and Technology), a strategic framework to deepen defence industrial cooperation, technology sharing, and military interoperability between the two countries. The agreement builds on prior defence cooperation frameworks and includes plans to sign a ten-year Framework for the U.S.-India Major Defence Partnership. For India's aerospace and defence market, COMPACT opens pathways for advanced technology transfers, joint manufacturing under the Make in India initiative, and expanded defence exports.

Adani Defence Systems and Technologies completed the acquisition of an 85.8% stake in Air Works India (Engineering) Private Ltd. in December 2024 for approximately Rs 400 crore. Air Works is India's largest private-sector Maintenance, Repair, and Overhaul company, operating facilities in Hosur, Mumbai, and Kochi with certifications from over 20 international aviation authorities. The acquisition significantly strengthens Adani Defence's ability to service both military and civilian aircraft across defence and commercial aviation segments. It also positions the conglomerate to bid for larger government MRO contracts, including those involving helicopters, drones, and transport aircraft.

In October 2024, Tata Advanced Systems Limited inaugurated India's first private-sector Final Assembly Line (FAL) for a military aircraft at Vadodara, Gujarat - a facility purpose-built to assemble Airbus C295 transport aircraft for the Indian Air Force. The plant, established under a USD 2.5 billion contract covering 56 aircraft for the IAF, will produce 40 of those units domestically. The remaining 16 were delivered from Spain, six of which had already been handed over. This milestone is a landmark achievement for the Make in India programme and marks a structural shift in India's defence manufacturing landscape, opening the door for similar private-sector assembly lines in future platform programmes.

Adani Defence and Aerospace signed a manufacturing agreement with France's Thales Group in June 2024 to produce 70mm rockets in India, specifically targeting supply for the HAL Rudra and Prachand helicopter programmes. The partnership aligns with the government's indigenisation drive for ammunition and weapon systems, reducing dependency on imports for frontline helicopter armaments. Adani concurrently signed a separate collaboration with UAE-based EDGE Group targeting missiles, unmanned systems, and electronic warfare technologies. Together, these partnerships reflect the growing role of private Indian conglomerates in high-value weapon systems manufacturing.

Tata Advanced Systems Limited (TASL) and Air India signed a Memorandum of Understanding in February 2024 to jointly develop a 35-acre MRO complex at Kempegowda International Airport in Bengaluru. The facility, expected to be operational by early 2026, will support both wide-body and narrow-body aircraft maintenance and positions India to reduce the approximately 85% of MRO work currently outsourced overseas by domestic carriers. The project directly supports the government's ambition to establish India as a global aviation MRO hub, aided by a GST reduction from 18% to 5% on MRO services introduced in recent policy reforms.

India's Aatmanirbhar Bharat initiative has evolved from a policy aspiration into a structural driver of the India Aerospace and Defence market growth. The government has released multiple positive indigenisation lists banning or restricting imports of defence equipment that India can manufacture domestically, creating captive demand worth hundreds of thousands of crore for Indian suppliers. With 75% of the modernisation budget ring-fenced for domestic procurement and DRDO running 100 priority research projects, the policy is fundamentally reshaping supply chains. In October 2024, Tata Advanced Systems inaugurated India's first private-sector military aircraft Final Assembly Line for the Airbus C295 in Vadodara, a tangible milestone of the Make in India policy converting into production-level reality.

The entry and consolidation of large Indian conglomerates including Tata, Adani, and Mahindra into the aerospace and defence manufacturing space is a defining competitive shift in the sector. These private players are bringing capital, managerial agility, and supply chain integration capabilities that are compressing the traditional dominance of defence PSUs. The MRO segment, in particular, is attracting significant private investment as India moves to capture a larger share of the USD 4 billion in annual MRO expenditure currently sent abroad. In December 2024, Adani Defence acquired Air Works India, the country's largest private MRO operator, for Rs 400 crore, signaling ambitions to become a full-spectrum aerospace services provider.

Advanced communication systems, radar platforms, and electronic warfare capabilities have become among the highest-priority procurement categories for India's armed forces. The integration of AI into battlefield communication networks, the development of indigenous AESA radar systems, and the push for satellite-based surveillance are driving demand for domestic electronics at scale. Bharat Electronics Limited (BEL) is the primary beneficiary, with an order book exceeding Rs 94,000 crore and Maharatna status granted in October 2024. The communication systems segment is expected to grow at a CAGR of 8.3% through the forecast period - the fastest among all offerings. In February 2024, Air India and TASL formalized their MoU for a 35-acre MRO and systems complex at Bengaluru's KIA, reinforcing the convergence of aviation infrastructure and high-tech systems servicing.

India's defence budget trajectory is one of the most reliable structural tailwinds supporting the aerospace and defence market over the forecast horizon. The FY2025-26 Union Budget allocated Rs 6.81 trillion (approximately USD 78.7 billion) to defence, a 9.5% increase year-on-year. With India ranking as the third-largest defence spender globally, this consistent budget growth underpins long-cycle procurement programmes across all four services, from fifth-generation fighter jets under the AMCA programme to submarine and naval vessel construction. In February 2025, the US-India COMPACT framework further validated India's emergence as a premier global defence partner, unlocking advanced technology co-production opportunities that are expected to accelerate domestic manufacturing sophistication.

The Expert Market Research's report titled "India Aerospace and Defence Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

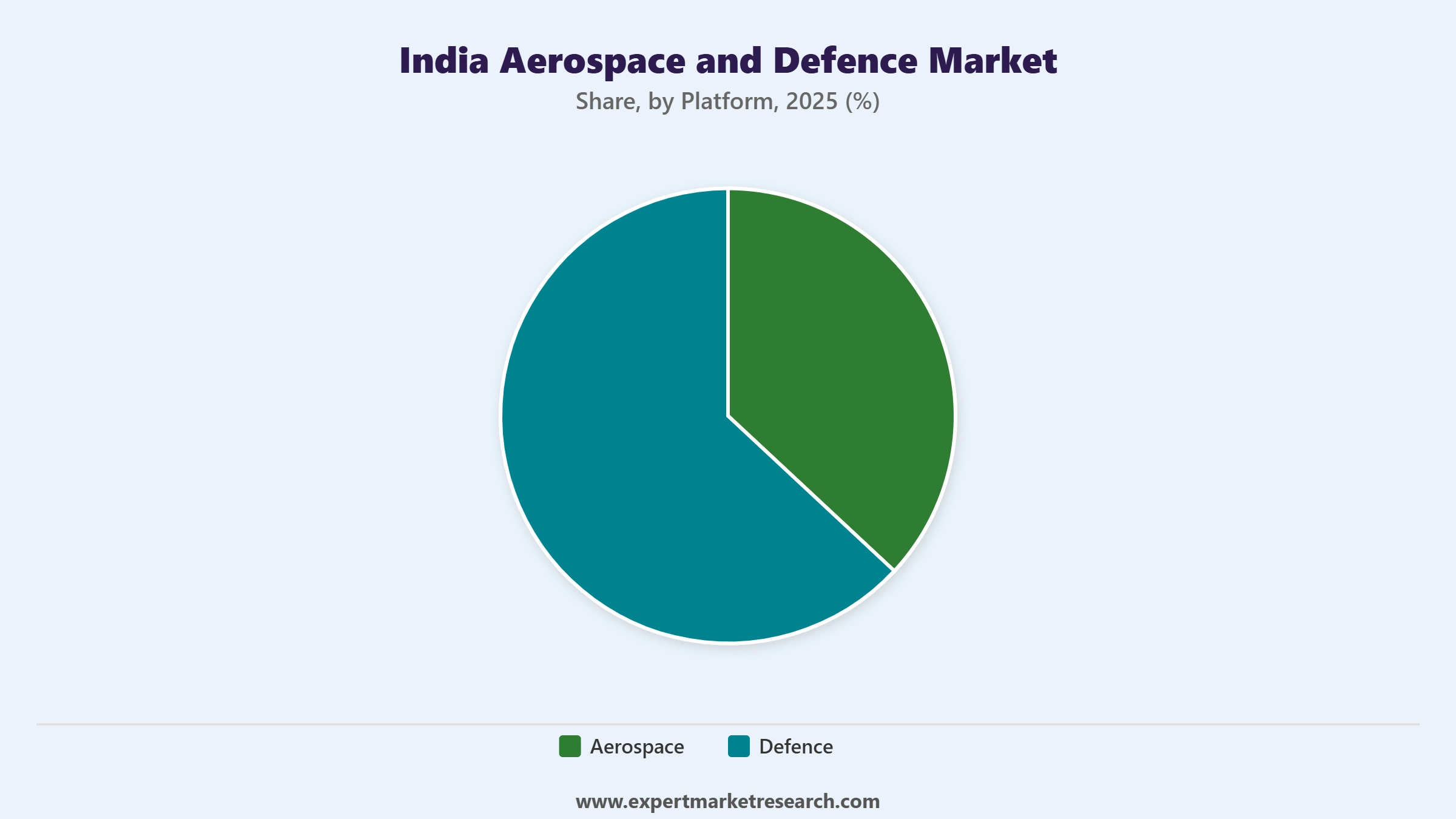

Market Breakup by Platform

Key Insight: The aerospace platform segment generates substantial revenue through military aviation procurement, with the Indian Air Force operating over 900 aircraft and actively replacing legacy platforms with domestically manufactured or co-produced alternatives. The civil aviation sub-segment is experiencing rapid fleet expansion, with Indian carriers expected to add over 500 aircraft in the 2024-2026 period. The space sector is growing fastest, driven by India's ambition to place 52 surveillance satellites in orbit within five years, with 50% developed by private firms. In the defence segment, naval systems have emerged as a critical investment area, with the Indian Navy pressing to expand its submarine fleet under Project 75(I) and fast-tracking surface vessel construction at Mazagon Dock, Goa Shipyard, and Cochin Shipyard.

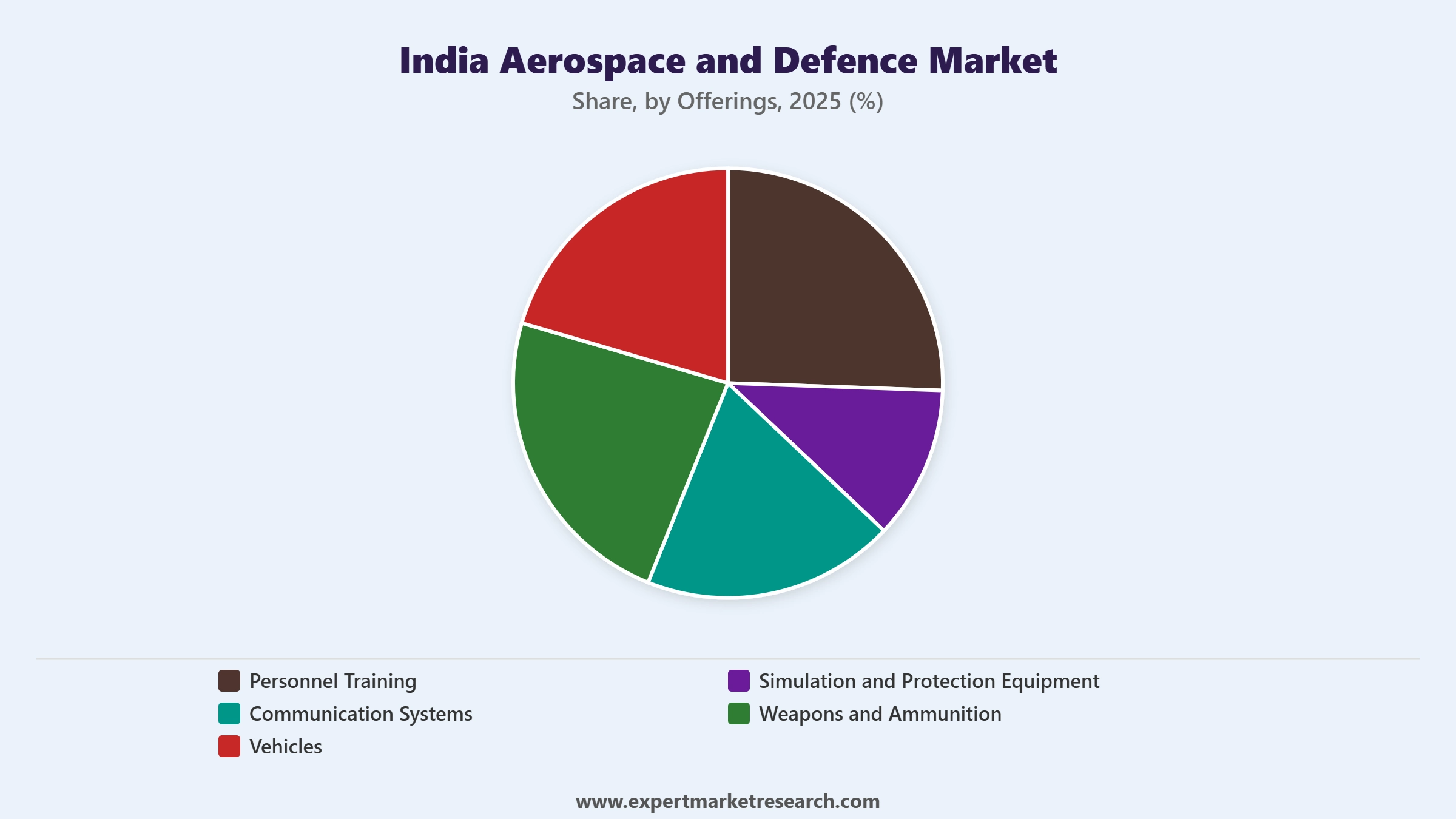

Market Breakup by Offerings

Key Insight: Communication systems represent the highest-growth offerings segment, projected to expand at a CAGR of 8.3% through the forecast period. India's armed forces are modernising command-and-control infrastructure, deploying advanced radars, and integrating electronic warfare and satellite communication platforms across all services. Bharat Electronics Limited is the dominant supplier in this space, with its order book backed by system-level contracts covering ship-borne systems, radar networks, and battlefield management software. The weapons and ammunition segment is also gaining momentum as India phases out legacy import-dependent systems, with domestic players including Adani, Bharat Forge, and Munitions India capturing a growing share of army artillery, missile, and small arms requirements.

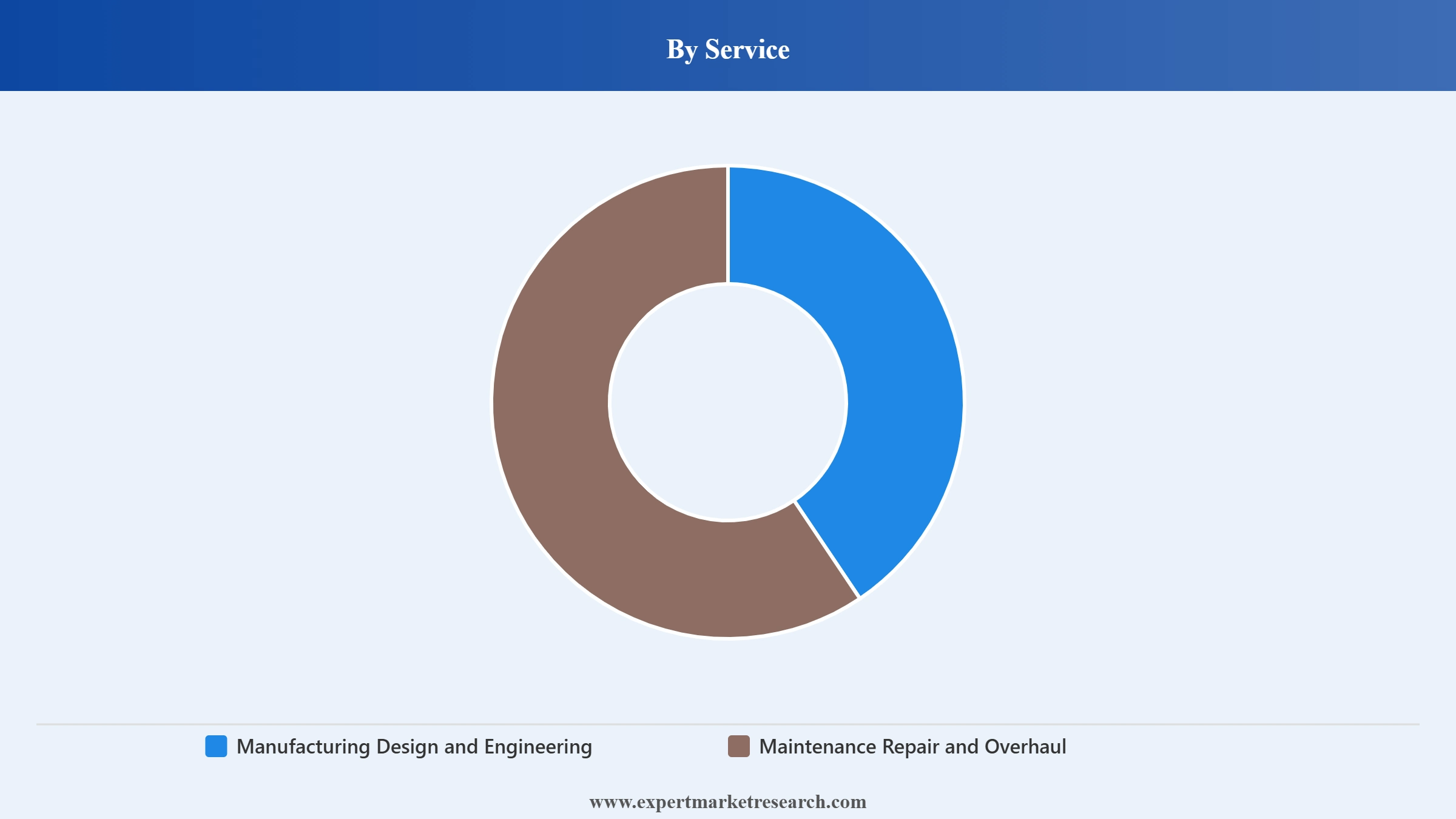

Market Breakup by Service

Key Insight: Manufacturing, Design, and Engineering services constitute the larger of the two service categories, underpinned by active production of platforms such as the LCA Tejas Mk1A, the HAL Prachand helicopter, BrahMos missile systems, and the Arjun main battle tank. Tata Advanced Systems and Mahindra Aerostructures are expanding their aerostructures production for both domestic platforms and global OEMs including Airbus and Boeing. The MRO segment is growing rapidly as India works to reverse the long-standing trend of outsourcing 85% of commercial aircraft maintenance work overseas. Significant investments from Adani (Air Works acquisition), TASL (Bengaluru MRO complex), and IndiGo's own maintenance initiatives are beginning to shift that balance.

Market Breakup by Region

Key Insight: South India holds the largest share of India's aerospace and defence manufacturing base, with Bengaluru functioning as the sector's de facto capital. HAL's main production facilities, DRDO's key research laboratories including ADE and CABS, BEL's primary plant, and the campuses of Tata Advanced Systems and Mahindra Aerostructures are all concentrated in or around the city. The Bengaluru-Hyderabad corridor extends this footprint northward into Telangana, where BrahMos's new integration facility and Tata Boeing Aerospace's Apache fuselage plant operate. West India is gaining rapidly, anchored by the Vadodara C295 FAL and the broader Gujarat Defence Corridor, while North India benefits from the Uttar Pradesh Defence Industrial Corridor encompassing Lucknow, Kanpur, and Agra.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The defence segment within the platform classification commands the dominant market share in India's aerospace and defence sector, reflecting the primacy of military procurement in the country's overall expenditure mix. Land-based systems represent the largest sub-category given the Indian Army's sheer scale as the world's second-largest standing force, with requirements spanning armoured vehicles, artillery, missile systems, and infantry equipment. Naval systems are attracting the fastest investment growth rate, driven by ambitious blue-water expansion plans and the submarine shortfall that compels urgent procurement. Within the aerospace platform, civil aviation has overtaken military aviation in revenue contribution as a result of the unprecedented fleet expansion by Indian carriers, which collectively placed orders exceeding 1,200 aircraft with Airbus and Boeing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the offerings segmentation, communication systems and weapons and ammunition together account for the majority of procurement value. Communication systems' projected 8.3% CAGR reflects a sustained multi-year investment cycle that spans all services and includes satellite communication, electronic warfare, and AI-driven command systems.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the service dimension, manufacturing and engineering services dominate given the large-scale active production programmes running across HAL, BDL, BEL, and multiple private sector facilities. The MRO segment, though currently smaller, is the faster-growing service category as India builds the infrastructure to address its historically high share of offshore maintenance outsourcing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the epicentre of India's aerospace and defence industry, combining the research depth of DRDO's Bengaluru laboratories with the production scale of HAL's facilities and the growing commercial capabilities of private players including TASL and Mahindra Aerostructures. Bengaluru alone hosts over 40% of India's aerospace manufacturing capacity. The adjacent Hyderabad cluster adds a significant dimension through the Tata Boeing Aerospace facility - Boeing's exclusive global manufacturer for the Apache helicopter fuselage - and the BrahMos Aerospace integration plant that is scaling output toward 100-150 units annually by 2026. Aero India 2025, held at Bengaluru's Yelahanka Air Force Station, reaffirmed the city's centrality to the sector by attracting global OEMs and showcasing India's emerging stealth, AI, and unmanned systems capabilities. South India's dominant position is expected to strengthen through the forecast period as new platform programmes concentrate production capacity further in the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

West India is emerging as India's second-most significant aerospace manufacturing hub, primarily through the development of the Gujarat Defence and Aerospace Corridor. The October 2024 inauguration of Tata Advanced Systems' C295 Final Assembly Line in Vadodara marked the corridor's most visible milestone to date. The Uttar Pradesh Defence Industrial Corridor is simultaneously transforming North India's role in the sector, with BrahMos Aerospace operating a new production facility in Lucknow designed to produce 80-100 missiles annually from 2026, and Adani Defence's ammunition plant in Kanpur targeting supply for the Indian Army's small arms requirements. These corridor-based developments are distributing the aerospace and defence value chain beyond the traditional southern cluster, creating a more geographically balanced production ecosystem that aligns with the government's industrial decentralisation objectives.

The India Aerospace and Defence market is structured around a dual-tier competitive architecture. The first tier consists of Defence Public Sector Undertakings, led by Hindustan Aeronautics Limited and Bharat Electronics Limited, which collectively account for the majority of domestically manufactured defence output. The second tier comprises a rapidly growing cohort of private sector players, most prominently Tata Advanced Systems Limited and Adani Defence and Aerospace, whose aggressive acquisition strategies, joint ventures with global OEMs, and investment in new manufacturing facilities are challenging PSU dominance in specific product categories.

Foreign OEMs including Airbus, General Electric, and Collins Aerospace participate primarily through technology transfer arrangements, licensed production partnerships, and supply of specialized components and systems that India has not yet indigenised. Defence Research and Development Organisation (DRDO) operates as both a competitor and an enabler, designing platforms that are then transferred to HAL or private firms for production. The competitive dynamic is shifting in favour of private sector consolidation as government policy increasingly reserves new manufacturing programmes for industry-led consortia.

Founded in 1940 and headquartered in Bengaluru, HAL is India's largest aerospace and defence public sector company, holding Maharatna status since October 2024. The company manufactures and services military aircraft, helicopters, and aero-engines, with an order book exceeding Rs 94,000 crore. Current production programmes include the LCA Tejas Mk1A, the ALH Dhruv, the HAL Prachand light combat helicopter, and the HTT-40 trainer. HAL is the sole domestic production partner for India's current fighter fleet and manages licensed manufacture of the Su-30MKI. The company commissioned a third Tejas production line and a second HTT-40 line in FY2025-26, significantly increasing its output capacity.

Bharat Dynamics Limited, founded in 1970 and headquartered in Hyderabad, is India's primary manufacturer of guided missiles, underwater weapons, and allied defence equipment. The company produces the Akash surface-to-air missile system, the MRSAM naval and land variants (in joint development with IAI Israel), and the Helina helicopter-launched anti-tank missile. BDL has seen order inflows accelerate sharply as the Indian armed forces replace imported missile systems with indigenously produced alternatives. The company's Hyderabad plant is the primary production facility, supplemented by a new integration and testing facility in Lucknow that is being scaled for BrahMos production.

Established in 2007 and headquartered in Hyderabad as a wholly-owned subsidiary of Tata Sons, TASL has become India's leading private-sector aerospace and defence manufacturer. The company's October 2024 inauguration of India's first private military aircraft Final Assembly Line for the C295 at Vadodara is its defining milestone. TASL also operates the Tata Boeing Aerospace facility in Hyderabad - Boeing's exclusive global source for AH-64 Apache fuselages - which delivered its 300th unit in February 2025. In April 2024, TASL launched TSAT-1A, India's first privately assembled sub-metre optical remote sensing satellite, establishing its space sector credentials. TASL has signed multi-year supply agreements with both Airbus and Lockheed Martin.

Adani Defence and Aerospace is the defence and aerospace vertical of the Adani Group, representing one of the most aggressive private sector entries into India's strategic industries. The company has built its portfolio through targeted acquisitions and joint ventures: its December 2024 acquisition of Air Works India established it as a major MRO operator, while partnerships with Thales Group for 70mm rocket production and the EDGE Group for unmanned systems reflect its offensive supply expansion. Adani's Kanpur ammunition facility targets a substantial share of India's small arms ammunition market, and its drone delivery contracts with the Indian Navy illustrate growing platform capabilities. The company operates under the Aatmanirbhar Bharat framework with a declared export-oriented mandate.

Other key players in the market are Bharat Electronics Limited (BEL), Airbus SAS, General Electric Company, Collins Aerospace, Defence Research and Development Organisation (DRDO), and Mahindra Aerospace Private Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead in India's fastest-evolving defence and aerospace sector with our comprehensive 2026 market intelligence report. Whether you are assessing entry into India's expanding industrial corridors, evaluating technology transfer opportunities under bilateral programmes, or benchmarking competitive positioning in specific platform categories, this report delivers the precision data and forward-looking insights you need. Download your free sample today and unlock the strategic intelligence driving decisions in the India Aerospace and Defence market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India aerospace and defence market reached an approximate value of USD 30.72 Billion.

The market is projected to grow at a CAGR of 7.10% between 2026 and 2035.

The key players in the market includes Hindustan Aeronautics Limited (HAL), Bharat Dynamics Limited (BDL), Bharat Electronics Limited (BEL), Tata Advanced Systems Limited, Airbus SAS, General Electric Company, Collins Aerospace, Defence Research & Development Organisation, Mahindra Aerospace Private Limited, and Adani Defence and Aerospace, among others.

The communication systems segment by offerings is gaining traction and anticipated to expand with an 8.3% CAGR through 2035.

India’s aerospace and defence companies are accelerating indigenisation through strategic joint ventures—like TASL and Dassault producing Rafale fuselages in Hyderabad—and expanding manufacturing, exports, and MRO capabilities, backed by government corridors and AI-Cyber R&D initiatives.

Key trends include indigenous manufacturing, drone capability expansion, rising private sector participation, AI integration in defense tech, and growing defense exports. Strategic partnerships and government support are transforming India into a global aerospace and defense hub.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Platform |

|

| Breakup by Offerings |

|

| Breakup by Service |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.