Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

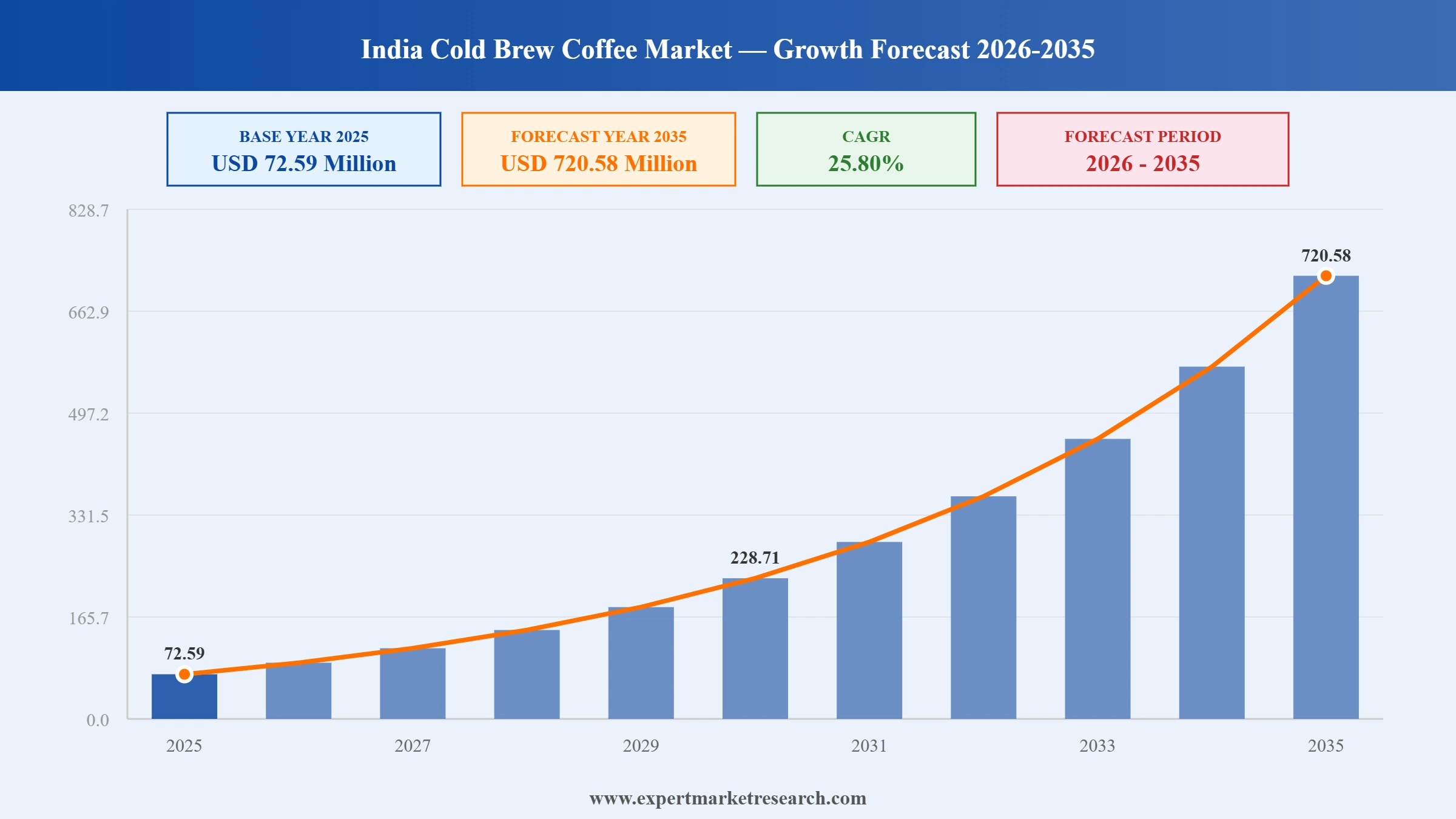

The India Cold Brew Coffee Market reached a value of USD 72.59 Million at 2025 and is projected to expand at a CAGR of around 25.80% during the forecast period of 2026-2035. With a rapidly maturing urban coffee culture, growing consumer interest in health-conscious and low-acidity beverages, accelerating adoption of e-commerce and D2C distribution, and the entry of both domestic specialty brands and multinational players into the cold brew segment, the market is expected to reach USD 720.58 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India cold brew coffee market is being shaped by a convergence of cultural, technological, and investment-driven forces that together are transforming what was until recently a niche urban phenomenon into a high-growth consumer category with pan-India ambitions. These forces include the rise of D2C specialty brands, the entry of institutional conglomerates, rapid e-commerce distribution expansion, and product format innovations.

In September 2025, Blue Tokai Coffee Roasters (Muhavra Enterprises Private Limited) raised USD 25 million in bridge funding from its existing investors, including A91 Partners, Anicut Capital, Verlinvest, and 12 Flags. The capital is earmarked for accelerating domestic store rollouts across India, upgrading roastery and bakery infrastructure in Bengaluru and Gurugram, and funding international market entry into Japan and Dubai. Blue Tokai had earlier opened its first store in Japan in July 2024, signalling the brand's confidence in the global appetite for premium Indian specialty cold brew coffee. With this latest round, Blue Tokai is targeting over 800 stores and INR 2,000 crore in revenue within the next four years.

In FY2025, Sleepy Owl Coffee Private Limited recorded a doubling of its revenue to approximately INR 44 crore compared to the prior year, while simultaneously reducing its net losses by approximately 80% to INR 2.1 crore. The strong financial performance reflects the brand's successful pivot toward a sustainable and profitable D2C growth model, with strong momentum across its instant, cold brew, and ready-to-drink product portfolio. Sleepy Owl had previously been recognised as a pioneer of India's cold brew coffee segment since its founding in 2016. The company's financial trajectory is being watched closely as an indicator of the commercial viability of India's premium specialty coffee market at scale.

In 2024, Sleepy Owl Coffee expanded its product range significantly beyond its core cold brew offerings, introducing protein-infused coffee beverages and a matcha latte ready-to-drink product, which the company identified as India's first of its kind in the ready-to-drink category. The diversification strategy reflects the broader ambition of India's leading cold brew brands to cross-sell within the premium beverage space, targeting health-conscious consumers who are simultaneously exploring protein supplementation, adaptogens, and Asian beverage traditions. These product line extensions leverage Sleepy Owl's existing D2C distribution infrastructure while opening new incremental revenue streams beyond the core cold brew market.

In 2024, TATA Consumer Products Limited, through its subsidiary Nourish Co, entered the India cold brew coffee segment, marking a significant expansion of the Indian cold brew market's competitive landscape. TATA Consumer's entry brings the institutional scale, distribution reach, and brand credibility of one of India's most trusted conglomerates into a segment that had previously been dominated by digitally-native startups. The move is expected to accelerate consumer awareness and mainstream adoption of cold brew coffee formats in Tier 2 and Tier 3 cities, where TATA's distribution network significantly outreaches that of specialty coffee startups, contributing meaningfully to India cold brew coffee market growth.

In 2024, the total planted area of coffee beans in India grew by approximately 1.67% between 2022 and 2023, according to agricultural data, increasing the domestic supply base for high-quality arabica and robusta beans used in cold brew production. In parallel, nitrogen-based cold brewing technology gained significant consumer traction in India's premium coffee segment during 2024, with brands offering nitro cold brew formats across cafe and packaged channels. Nitro cold brew's characteristic smooth, creamy texture and natural sweetness, achieved without dairy additions, strongly aligns with Indian consumers' growing interest in low-calorie, health-forward beverages. Karnataka, Kerala, and Tamil Nadu continue to account for approximately 97% of India's total coffee production, providing a deep domestic supply base for the cold brew sector.

India's cold brew coffee sector has attracted a sustained wave of venture capital and institutional investment that is directly financing the rapid expansion of brand portfolios, physical retail presence, and digital distribution capabilities. In September 2025, Blue Tokai raised USD 25 million to fund store rollouts and international expansion. Earlier rounds of investment from global firms such as Verlinvest, A91 Partners, and DSG Consumer Partners signal that India is now viewed as a priority market for premium beverage investment globally. This investment cycle is accelerating product development, distribution reach, and consumer marketing at a pace that is expanding the total addressable market for cold brew coffee well beyond metro cities, contributing to India cold brew coffee market growth across the forecast period.

Online stores and D2C platforms are transforming the cold brew coffee category from a metro cafe phenomenon into a nationwide consumer product accessible to buyers across India's tier 2 and tier 3 cities. India's online shopper base is expected to become the second largest globally by 2030, reaching 500 to 600 million shoppers, while internet access is projected to reach 87% of Indian households. Cold brew brands including Sleepy Owl, Blue Tokai, and Rage Coffee have built their primary commercial models around D2C and e-commerce channels, using platforms including Amazon, Flipkart, and their own websites to reach consumers without the capital intensity of physical retail expansion. Quick commerce platforms including Blinkit and Swiggy Instamart are further reducing friction by enabling sub-30-minute cold brew delivery in major urban centres.

Product innovation is playing a central role in driving trial and repeat purchase among Indian cold brew consumers. The adoption of nitrogen-based brewing technology, which produces a naturally creamy, low-acidity brew without dairy additives, has expanded the cold brew category's appeal among lactose-intolerant consumers and health-conscious buyers. Sleepy Owl's 2024 launches of protein-infused coffee beverages and India's first matcha latte RTD demonstrate the direction of premiumisation within the cold brew segment. These innovations serve a dual purpose: attracting first-time buyers through functional benefits and providing category loyalists with reasons to trade up within the brand's portfolio, sustaining revenue growth even as the base market for traditional cold brew matures.

South India's deep-rooted coffee culture, supported by centuries of cultivation in Karnataka, Kerala, and Tamil Nadu, is providing a natural foundation for the cold brew category's growth in the region. These three states account for approximately 97% of India's total coffee production, ensuring abundant access to fresh, high-quality arabica and robusta beans that are the primary raw material for premium cold brew products. Bengaluru and Chennai have emerged as the country's most mature markets for specialty and artisanal cold coffee, with a high density of specialty coffee cafes, roasteries, and D2C brand headquarters. The cultural familiarity with traditional South Indian filter coffee has made the transition to cold brew formats easier than in other regions, creating a highly receptive consumer base.

“India Cold Brew Coffee Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

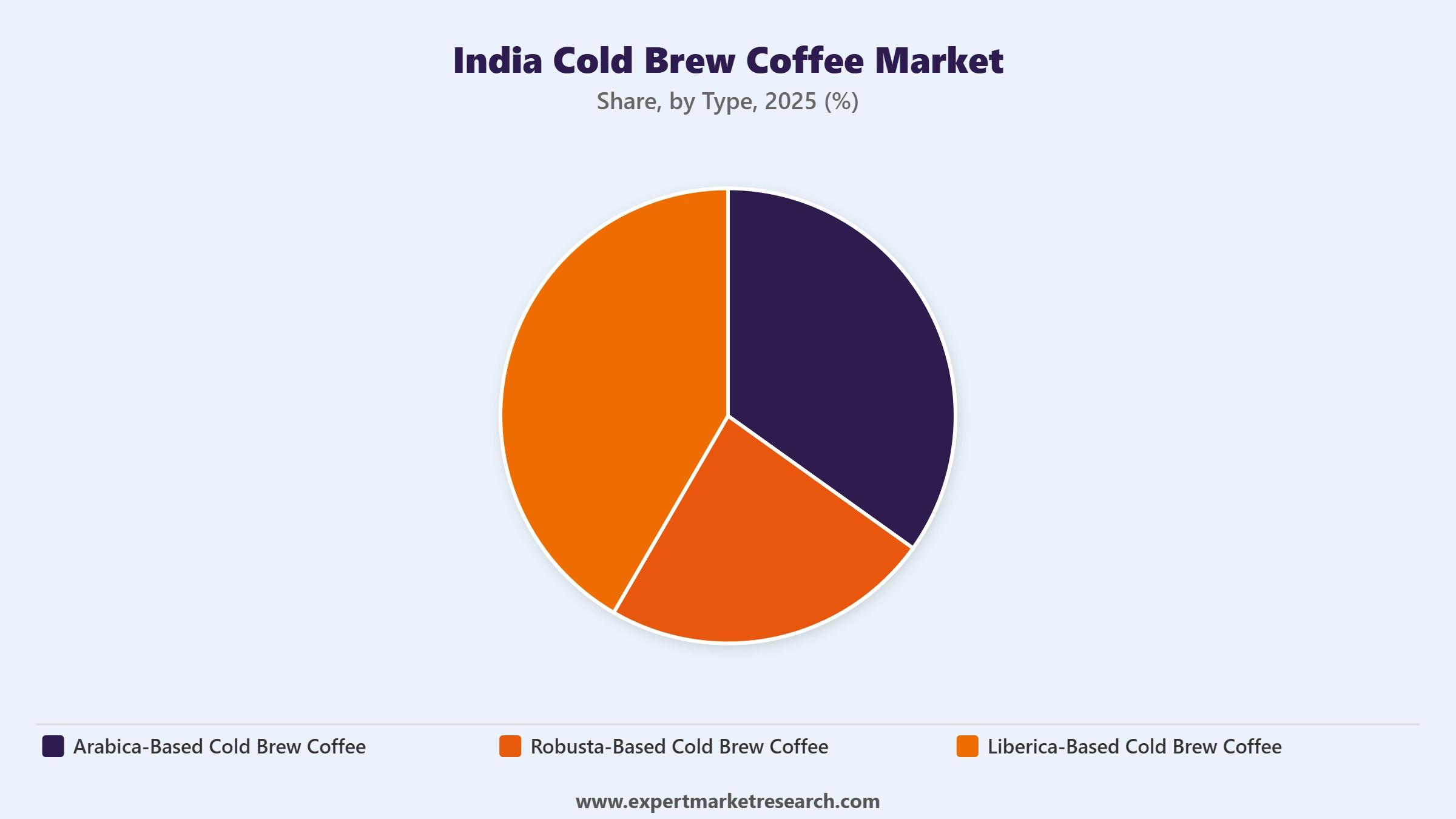

Market Breakup by Type

Key Insight: Arabica-based cold brew coffee holds the dominant share of the India cold brew coffee market by type, driven by the varietal's characteristic smooth, mild, and naturally sweet flavour profile that is particularly well-suited to cold water extraction. Arabica's lower bitterness and higher sugar content make it the preferred choice for ready-to-drink cold brew formats targeted at mainstream consumers. India produces a significant proportion of its arabica in the Nilgiris, Coorg, and Chikmagalur districts. Robusta-based cold brew holds a meaningful secondary share, particularly among consumers who prefer a more intense, higher-caffeine brew, and in blended products where robusta provides body and cost efficiency. Liberica-based products remain a niche offering positioned toward specialty coffee enthusiasts.

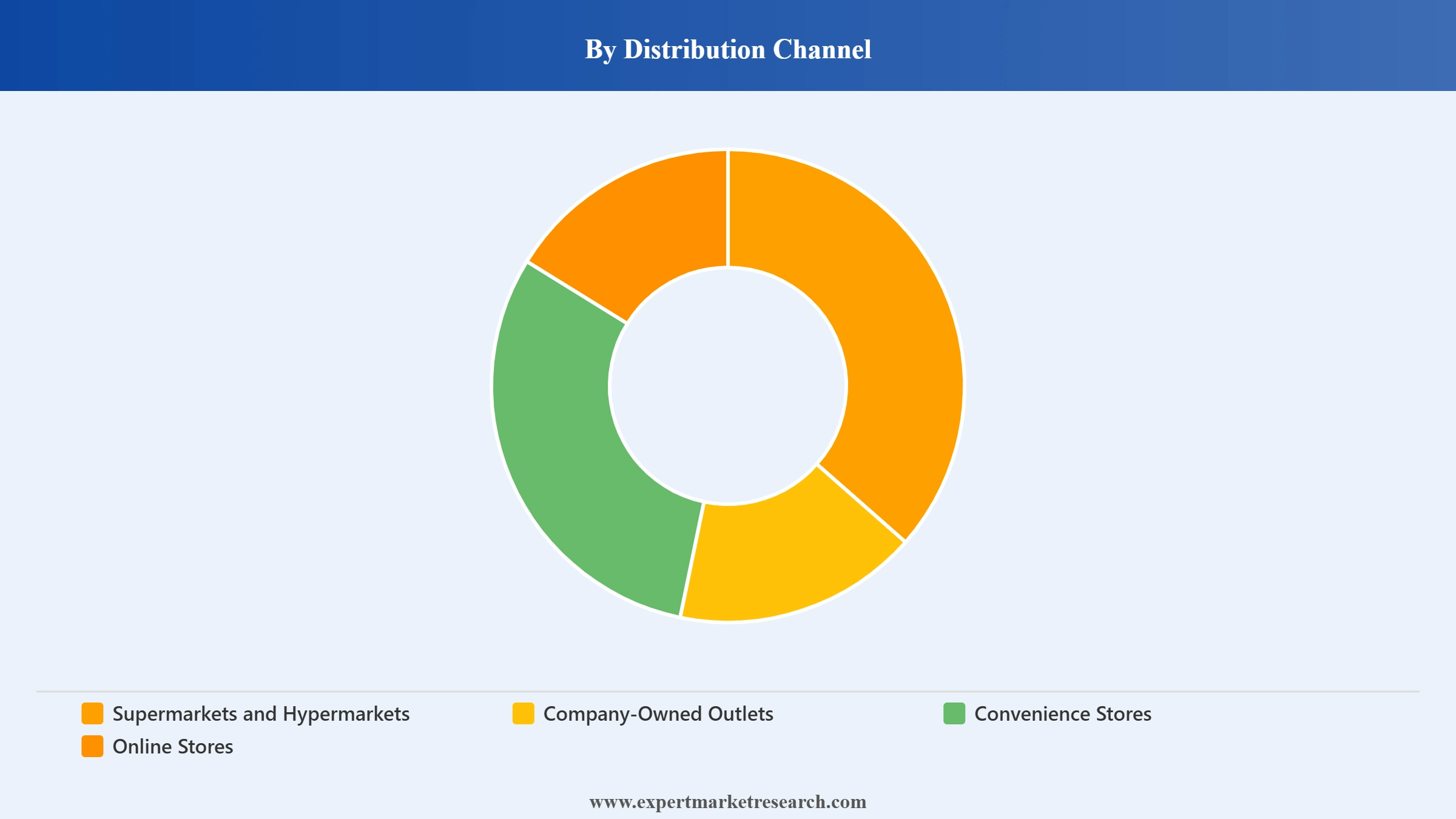

Market Breakup by Distribution Channel

Key Insight: Online stores represent the fastest-growing distribution channel in the India cold brew coffee market, driven by the proliferation of D2C brand websites, quick commerce platforms, and third-party e-commerce marketplaces. Leading brands including Sleepy Owl, Blue Tokai, and Rage Coffee have built their commercial models around digital-first distribution, leveraging social media, subscription services, and influencer marketing to acquire and retain customers without the capital intensity of physical retail. Supermarkets and hypermarkets are expanding their specialty coffee shelf space as mainstream acceptance of cold brew formats grows, while company-owned outlets through cafe chains such as Starbucks and Blue Tokai serve as premium consumption and brand experience destinations.

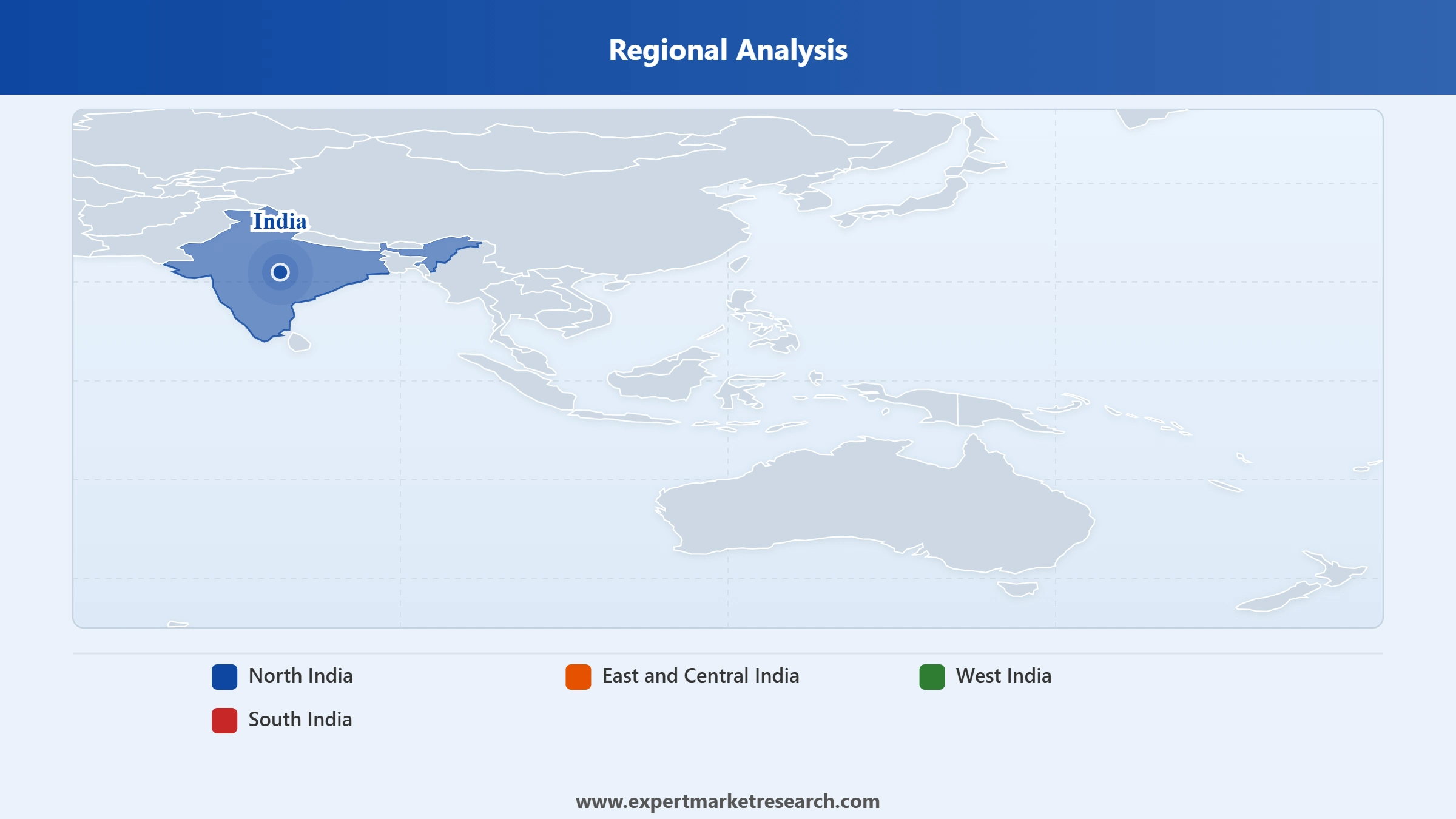

Market Breakup by Region

Key Insight: South India is both the production heartland and the most sophisticated consumption market for cold brew coffee in India. Karnataka, Kerala, and Tamil Nadu account for approximately 97% of domestic coffee production, and cities including Bengaluru, Chennai, and Hyderabad host the highest concentration of specialty coffee brands, roasteries, and artisanal cafes. North India, particularly Delhi-NCR, is the second most significant regional market, home to multiple cold brew startup headquarters including Sleepy Owl, and a large urban millennial and Gen Z consumer base with high disposable incomes and openness to premium beverage formats. West India, anchored by Mumbai and Pune, is growing rapidly as coffee culture continues to displace traditional chai preferences among urban professionals.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type

Arabica-based cold brew coffee commands the largest market share by type in India, benefiting from the varietal's superior flavour characteristics in cold extraction and its alignment with consumer preferences for smooth, mild, and low-bitterness beverages. Premium specialty coffee brands in India predominantly source and feature single-origin or blended arabica varieties, positioning arabica-based cold brew at the higher end of the category's pricing spectrum. Robusta-based cold brew maintains a meaningful share among price-sensitive consumers and in institutional formats such as office coffee supply and restaurant and hospitality cold brew procurement, where cost efficiency is a more significant purchasing criterion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Online stores have emerged as the primary growth driver for the India cold brew coffee market by distribution channel, with D2C platforms enabling premium brands to reach consumers across India without building expensive physical retail networks. Social media-driven discovery, subscription-based repurchase models, and quick commerce same-day delivery are collectively making online the channel of choice for both acquiring new cold brew consumers and retaining existing ones. Company-owned outlets through cafe chains serve a complementary brand-building function, driving trial among cafe visitors who subsequently convert to at-home cold brew purchasing through online platforms. Supermarkets and hypermarkets are the primary channel for mainstream consumers discovering and trialing packaged cold brew products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India

South India is expected to be the fastest-growing regional market for cold brew coffee through the forecast period, anchored by Karnataka, Kerala, and Tamil Nadu, which collectively produce approximately 97% of India's coffee. Bengaluru stands out as India's specialty coffee capital, hosting the highest density of roasteries, specialty cafes, and coffee-focussed D2C brand operations. The region's established filter coffee culture has created a consumer base that is more knowledgeable, discerning, and receptive to cold brew formats than other parts of India. Blue Tokai's roastery and bakery expansion in Bengaluru as part of its September 2025 funding deployment directly reflects the strategic importance of South India to India's cold brew market growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India

North India, and Delhi-NCR in particular, is a critical market for India's cold brew coffee sector, serving as the headquarters for several leading cold brew brands including Sleepy Owl and as a major consumer market for premium ready-to-drink and D2C cold brew products. Delhi-NCR's large urban professional population, high internet penetration, and strong e-commerce adoption make it one of the most commercially significant cold brew markets outside South India. Sleepy Owl's doubling of revenue to INR 44 crore in FY2025 reflects the strong D2C demand being generated within the North Indian urban consumer base. Brand marketing through social media, including Instagram and YouTube, is particularly effective in driving cold brew trial among Delhi-NCR's digitally engaged youth consumer base.

The India cold brew coffee market features a competitive landscape that spans global coffeehouse giants, domestic specialty brands, and a growing cohort of well-funded D2C startups. The entry of TATA Consumer's Nourish Co adds institutional scale to a market that was previously dominated by venture-backed digital-first brands, signalling the market's growing commercial maturity and attractiveness to mainstream consumer goods companies.

Competition is centred on product innovation, source quality, digital marketing effectiveness, and distribution reach. Specialty brands are differentiating through transparent farm-to-cup sourcing, premium packaging, and experiential retail while institutional players leverage distribution scale and brand trust. E-commerce and quick commerce platforms are the primary battleground for market share.

Founded in 1971 and headquartered in Seattle, Washington, USA, Starbucks Corporation is the world's largest coffeehouse chain and a major player in India's premium cold brew coffee segment through its operated and licensed store network. Starbucks entered India in 2012 as a joint venture with Tata Consumer Products and has since expanded to over 390 stores across multiple Indian cities. Starbucks' ready-to-drink cold brew and nitro cold brew offerings, available both through its stores and select retail channels, establish it as a premium reference point for cold brew quality and format in the Indian market. The brand's membership program and digital ordering capabilities further support its cold brew sales volumes through its existing customer base.

Founded in 2013 and headquartered in New Delhi, Blue Tokai Coffee Roasters is one of India's most recognised specialty coffee brands, pioneering the farm-to-cup model that directly sources beans from Indian coffee estates and roasts them in-house. The company offers a comprehensive cold brew portfolio including packaged cold brew bags, RTD cold brew bottles, and cafe-prepared cold brew beverages across its growing store network. In September 2025, Blue Tokai raised USD 25 million in bridge funding from A91 Partners, Anicut Capital, Verlinvest, and 12 Flags to fund expansion into over 800 stores and international markets including Japan and Dubai. Blue Tokai's estimated five-fold revenue growth over four fiscal years underscores its commercial momentum.

Founded in 2016 and headquartered in New Delhi, Sleepy Owl Coffee is widely credited with having pioneered the consumer cold brew coffee format in India. The brand distributes its range of cold brew sachets, RTD bottles, and ancillary coffee products through D2C channels, e-commerce marketplaces, and select supermarkets. In FY2025, Sleepy Owl doubled its revenue to approximately INR 44 crore while reducing losses by approximately 80%, demonstrating the viability of a capital-efficient growth model in the Indian specialty cold brew market. The company's 2024 product launches including protein-infused coffee and India's first matcha latte RTD illustrate its commitment to category expansion through format and functional innovation.

Headquartered in New Delhi, Rage Coffee (Swmabhan Commerce Private Limited) is an India-based specialty coffee brand known for its premium, fortified coffee products including cold brew, instant coffee, and RTD beverages enriched with functional ingredients such as vitamins and antioxidants. Rage Coffee has built a strong D2C presence across e-commerce marketplaces and its own digital platform, leveraging social media marketing and influencer partnerships to reach health-conscious millennial consumers. The brand competes on the functional and wellness positioning of its cold brew and coffee products, targeting consumers who view their coffee purchase as part of a broader health and performance-oriented lifestyle.

Other key players in the market are Nestle S.A., Inspire Brands Inc., Seven Beans Coffee Company, Home Blend Coffee Roasters, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

India's cold brew coffee market is on one of the steepest growth trajectories in the country's fast-moving consumer goods landscape. Our comprehensive India Cold Brew Coffee Market report for 2026 provides the depth of analysis needed to understand this opportunity clearly, covering D2C brand dynamics, regional demand variations, product format innovation trends, and the competitive strategies of both startups and institutional players. Whether you are a specialty coffee brand, retail investor, FMCG company, or e-commerce platform, this report delivers the intelligence to move decisively in one of India's most exciting beverage categories. Download your free sample today and begin uncovering the full potential of India's cold brew coffee market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The India cold brew coffee market is projected to grow at a CAGR of 25.80% between 2026 and 2035.

The major drivers of the market are increased production of coffee beans, the prevalence of online cold brew coffee sales, and growing awareness of the cold brew coffee health benefits.

The key trends of the market include the development of new brewing technologies, the rising influence of social media marketing, and the preference for high-quality arabica and robusta-based cold brew coffee products.

The major regions in the market are north India, east and central India, west India, and south India.

The various types of cold brew coffee considered in the market report are arabica-based cold brew coffee, robusta-based cold brew coffee, and liberica-based cold brew coffee.

The various distribution channels in the market are supermarkets and hypermarkets, company-owned outlets, convenience stores, and online stores.

The major players in the market are Starbucks Corp., Nestle S.A., Inspire Brands, Inc., Muhavra Enterprises Private Limited (Blue Tokai), Sleepy Owl Coffee Private Limited, Swmabhan Commerce Private Limited (Rage Coffee), Seven Beans Coffee Company, and Home Blend Coffee Roasters, among others.

In 2025, the market attained a value of nearly USD 72.59 Million.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 720.58 Million by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.