Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

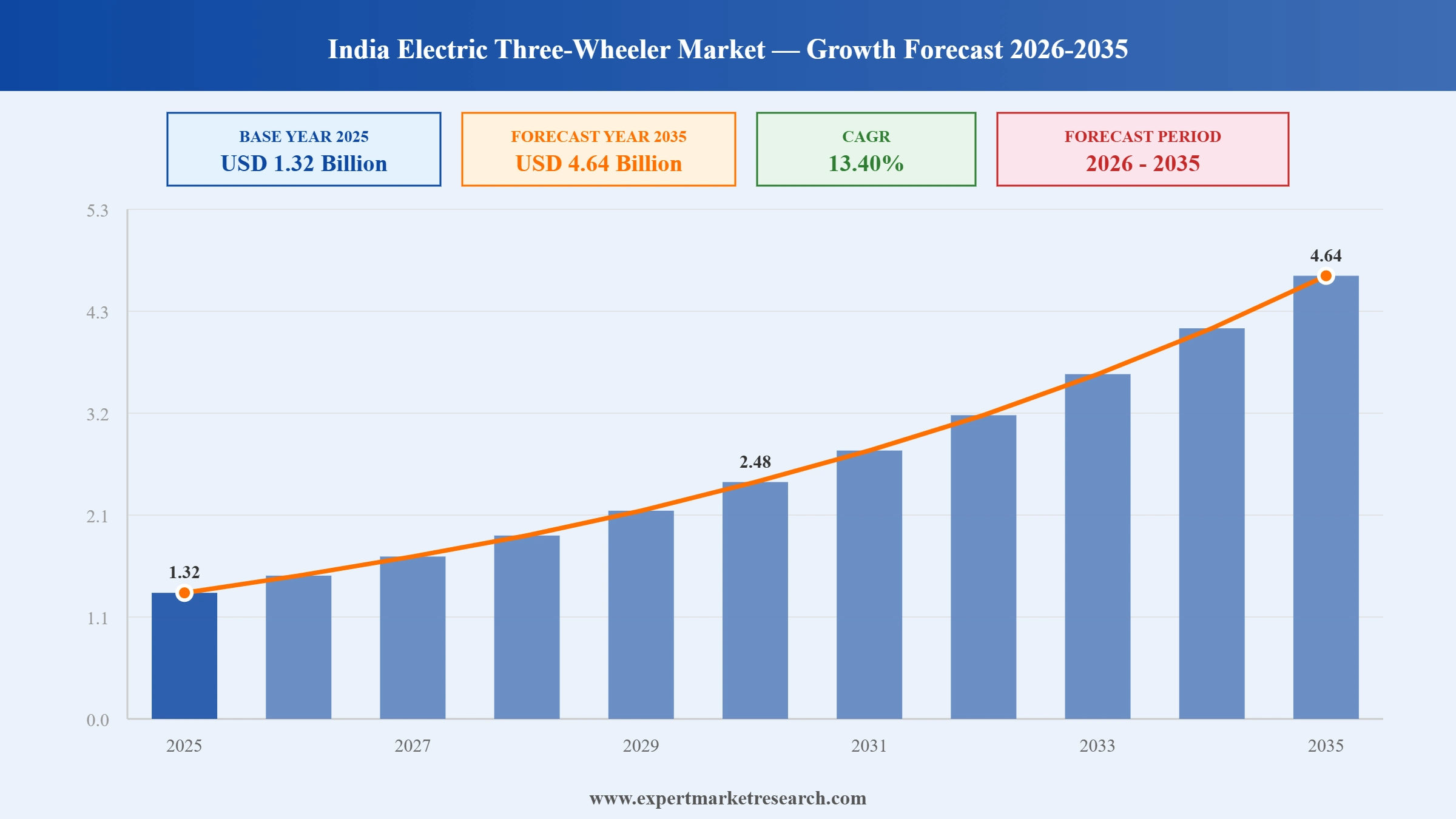

The India electric three-wheeler market reached a value of USD 1.32 Billion at 2025 and is projected to expand at a CAGR of around 13.40% during the forecast period of 2026-2035. With rising demand for affordable last-mile passenger and cargo transport, continuous government support through schemes like PM E-Drive, advancements in battery technology extending range and reducing costs, and surging e-commerce delivery requirements, the market is expected to reach USD 4.64 Billion by 2035.

India's electric three-wheeler segment registered record FY2026 retail sales of 830,819 units, up 19% year on year, according to Vahan portal data analysed by industry trackers in early April. Mahindra Last Mile Mobility led with 101,873 units, followed by Bajaj Auto at 89,604 (up 76%) and TVS Motor at 27,831 units, with the segment commanding 60.9% of overall three-wheeler sales, the Economic Times reported.

The Federation of Automobile Dealers Associations reported retail three-wheeler sales of 1,09,777 units in March 2026, up 10.52% year on year, driven by both internal combustion and electric variants. Mahindra (9,328 units) overtook Bajaj Auto (9,050 units) in monthly e-3W sales for the first time, while Bajaj's P9018 and Mahindra's UDO launches in February reshaped the passenger e-3W competitive map, Autocar Professional reported.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Electric Three-Wheeler Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

1.32 |

|

Market Size 2035 |

USD Billion |

4.64 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

13.40% |

|

CAGR 2026-2035 - Market by Region |

North India |

14.7% |

|

CAGR 2026-2035 - Market by Region |

South India |

14.2% |

|

CAGR 2026-2035 - Market by Vehicle Type |

Goods Carrier |

14.7% |

|

CAGR 2026-2035 - Market by Battery Range |

Above 100 KM |

14.1% |

India's electric three-wheeler market is being shaped by a powerful combination of policy tailwinds, e-commerce-driven logistics demand, rapid battery technology progress, and the entry of well-funded new players. These forces are collectively accelerating the transition from conventional auto-rickshaws and cargo carriers toward electric alternatives across urban, semi-urban, and increasingly rural areas.

Bajaj Auto launched its dedicated electric three-wheeler brand, GoGo, in February 2025, offering models with a 251 km range across three passenger variants. Priced starting at INR 3,26,797, the GoGo lineup includes features such as Hill Hold Assist, Auto Hazard Detection, and a five-year battery warranty, addressing key concerns around safety and long-term ownership costs. The launch reinforces Bajaj Auto's aggressive move into the electric three-wheeler segment, where it grew from under 1% market share in early 2023 to 6% market share by the close of 2024, making it one of the fastest-climbing players in the category.

TVS Motor Company made its entry into the electric three-wheeler market in January 2025 with the launch of the TVS King EV MAX, priced at INR 2,95,000. The vehicle delivers a range of 179 km, supports fast charging from 0 to 80% in 2.25 hours, and includes Bluetooth connectivity, fleet management tools, and three selectable drive modes. A nationwide rollout was planned following the launch, signalling TVS's intent to compete directly with established players in both urban passenger mobility and last-mile logistics segments across India.

Greaves Electric Mobility announced plans in December 2024 to expand its electric three-wheeler manufacturing capacity to 80,696 units across its Telangana and Uttar Pradesh plants ahead of the FY2027 deadline. The Uttar Pradesh facility is slated for a capacity increase to 45,896 units and the Telangana plant to 34,800 units, reflecting the company's strategic bet on North India's continued leadership in electric three-wheeler demand. The expansion aligns with the broader upward trend in production investments across the sector as OEMs race to capture growing demand from both fleet buyers and individual operators.

Digital lending platform Revfin Services Private Limited signed a strategic partnership with Bajaj Auto Limited in August 2024 to improve financing access for electric three-wheeler buyers, particularly in Tier 2 and Tier 3 cities. The collaboration was designed to lower the financial barriers that have historically prevented owner-operators in smaller cities from transitioning to electric vehicles. By combining Bajaj's manufacturing and brand strength with Revfin's digital lending infrastructure, the partnership aims to accelerate adoption among cost-sensitive segments and broaden the geographic reach of the GoGo and other Bajaj EV products.

ElectroRide and Battery Smart announced a joint battery-swapping initiative in June 2024 targeting electric two- and three-wheelers across India. By enabling operators to swap depleted batteries for charged ones in minutes rather than waiting for hours of charging, the initiative directly addresses one of the most cited pain points for commercial electric three-wheeler operators. Battery Smart had already completed 50 million battery swaps at its 1,400 stations by October 2025, demonstrating the practical scale and viability of this infrastructure model in supporting India's growing electric three-wheeler fleet.

The Indian government's PM E-Drive scheme, which took effect in late 2024 following the expiry of the EMPS programme, has become one of the India electric three-wheeler market growth's most significant demand catalysts. The scheme provides subsidies of INR 25,000 per unit for passenger electric three-wheelers and INR 50,000 for L5-category cargo vehicles in the first year, incentivising both individual operators and fleet buyers. Covering 316,000 units over a two-year period, the programme extends a clear policy signal to manufacturers and investors that government commitment to electric mobility remains firm. In November 2024, the government confirmed continuation of PM E-Drive incentives for cargo three-wheelers, reinforcing confidence among logistics fleet operators planning to electrify their operations.

The explosive growth of India's e-commerce and quick-commerce sector is creating sustained and growing demand for electric goods carrier three-wheelers, which are increasingly preferred over diesel or CNG alternatives for urban and peri-urban deliveries due to their lower operating costs and zero-emission profile. In January 2025, logistics operators cited electric three-wheelers as the preferred vehicle for last-mile delivery in congested urban corridors, where compact vehicle dimensions, silent operation, and low per-kilometre energy costs provide clear operational advantages over larger vehicles. The goods carrier segment is projected to grow at 14.7% CAGR, outpacing the broader market, as major e-commerce and grocery delivery platforms expand their electric fleets across Tier 1 and Tier 2 cities.

Improvements in lithium-ion battery chemistry and pack design are steadily increasing the practical range of electric three-wheelers while simultaneously reducing per-unit costs, making the total-cost-of-ownership case against conventional vehicles increasingly compelling. Lithium-ion battery pack prices fell approximately 12% in 2024 alone, narrowing the gap with lead-acid systems and enabling manufacturers to offer longer-range variants at more competitive price points. The above 100km battery range segment is growing fastest at a projected CAGR of 14.1%, reflecting the growing appetite of both passenger and cargo operators for vehicles that can complete full working days without mid-shift downtime. In June 2024, the expansion of battery-swapping networks such as Battery Smart further complemented this shift, allowing commercial operators to decouple range from wait time.

India's electric three-wheeler market attracted a significant wave of new product launches and brand entries in late 2024 and early 2025, expanding the range of vehicles available to buyers across price points and use cases. Bajaj Auto's GoGo brand, TVS's King EV MAX, and Lohia Auto's Youdha brand all entered the market within a concentrated period, each targeting distinct customer profiles from mass-market e-rickshaw operators to commercial fleet buyers. In January 2025, TVS Motor's entry in particular underscored how established two-wheeler OEMs are leveraging their manufacturing scale, distribution networks, and brand recognition to compete with pure-play EV startups in the electric three-wheeler space, intensifying both competition and innovation across the sector.

The Expert Market Research's report of Expert Market Research titled "India Electric Three-Wheeler Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

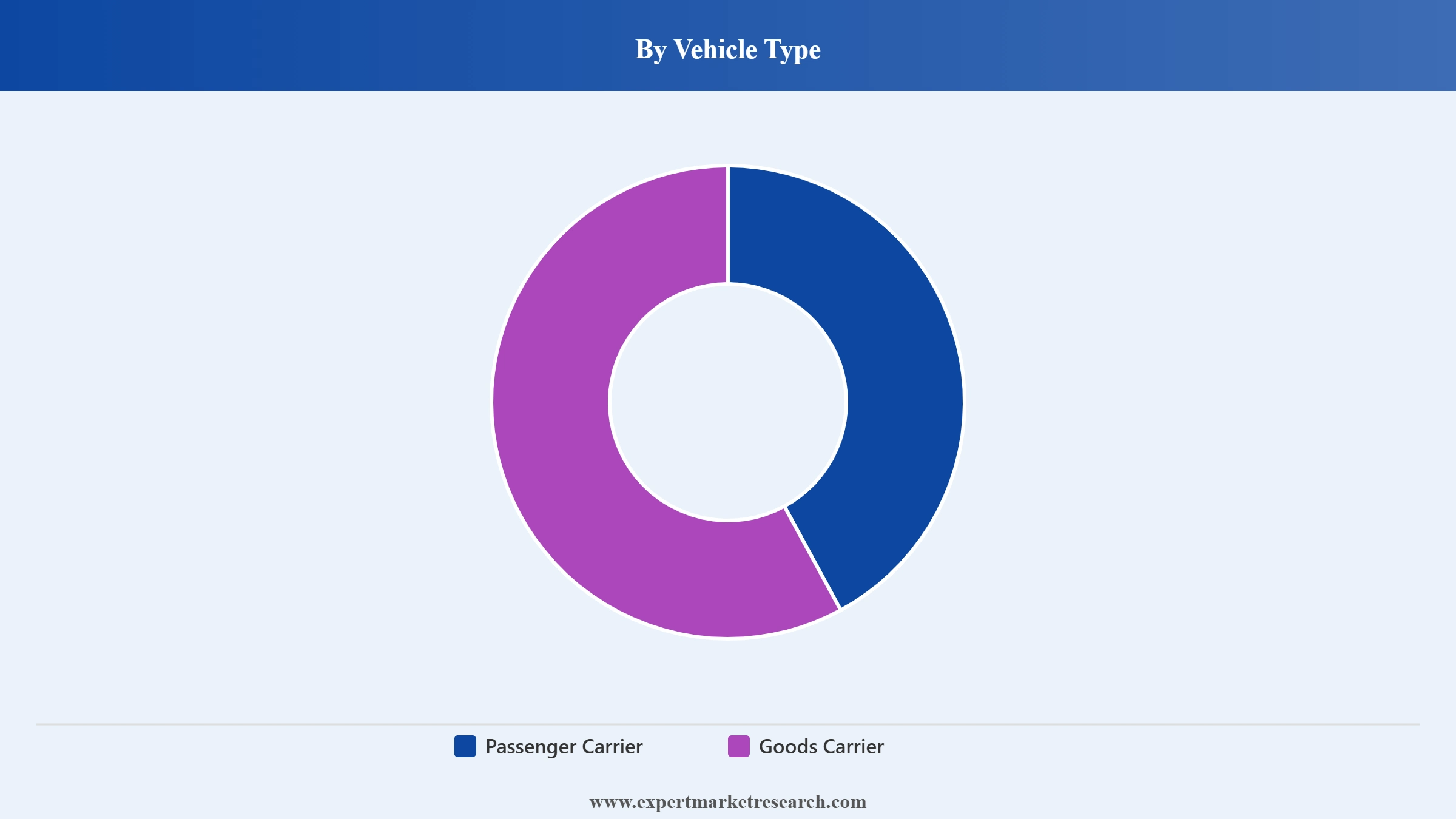

Market Breakup by Vehicle Type

Key Insight: Passenger carriers, commonly known as e-rickshaws, hold the dominant position in India's electric three-wheeler market, driven by strong urban and semi-urban demand for affordable last-mile connectivity. Cities across Uttar Pradesh, Bihar, and Delhi have seen deep penetration of passenger e-rickshaws, supported by state subsidies and low barriers to entry for individual operators. The Goods Carrier segment, however, is the fastest-growing at a projected CAGR of 14.7%, reflecting the rapid expansion of e-commerce and urban logistics operations that require cost-efficient and emission-free delivery vehicles. Companies like Mahindra, Bajaj, and Omega Seiki are increasingly catering to fleet operators seeking cargo three-wheelers for micro-fulfilment and last-mile delivery.

Market Breakup by Power Type

Key Insight: The Up to 1000W power segment is widely used in rural and semi-urban Tier 2 and Tier 3 towns, typically powered by lead-acid batteries and serving as affordable, entry-level last-mile transport. The 1001W to 1500W band represents the mainstream urban market, balancing performance and cost in a way that appeals to the broadest cross-section of operators. Above 1500W vehicles are gaining rapid share in the goods carrier space, where load capacity and torque requirements make higher-wattage motors essential. Manufacturers like Piaggio and Omega Seiki are focusing heavily on the above-1500W segment as e-commerce logistics evolve toward heavier cargo applications.

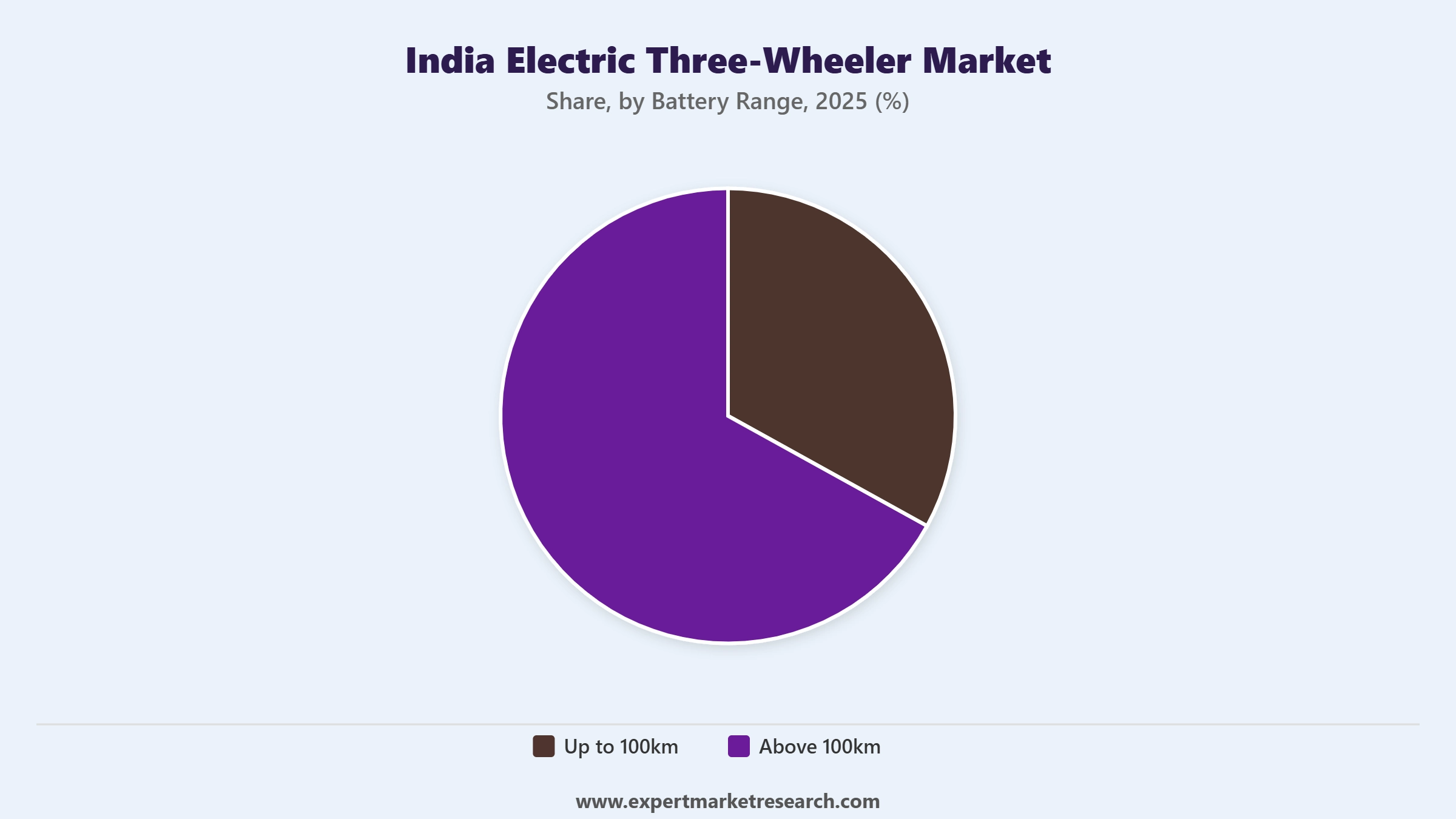

Market Breakup by Battery Range

Key Insight: Vehicles with above 100km battery range are the fastest-growing segment at a projected CAGR of 14.1%, driven by operator demand for full-shift coverage without mid-day interruption. Commercial operators in particular are driving this shift as they compare the total-cost-of-ownership of electric vehicles against CNG alternatives and increasingly factor in the operational downtime savings. The up to 100km segment retains a strong share in passenger e-rickshaws deployed on short intra-city routes where daily range requirements are modest and battery recharging is feasible at fixed stands during off-peak hours.

Market Breakup by Component

Key Insight: The Battery Pack and High Voltage Component segment commands the highest value share within the electric three-wheeler component market, reflecting the central role of battery systems in determining vehicle performance, range, and price. As lithium-ion adoption grows and pack prices continue to decline, this segment is also attracting significant R&D investment from OEMs and battery suppliers alike. The Motor segment is gaining value as manufacturers shift toward more efficient and compact brushless DC motors. Low Voltage Electric Components including telematics, fleet management systems, and connectivity modules are becoming increasingly important as OEMs differentiate on smart features and fleet-operator services.

Market Breakup by Region

Key Insight: North India leads the Indian electric three-wheeler market and is projected to grow at 14.7% CAGR through 2035, driven by the concentrated presence of e-rickshaw fleets in Uttar Pradesh, Delhi NCR, Bihar, and other northern states with dense urban-rural corridors. EV penetration in electric three-wheeler goods segments in Delhi reportedly reached 74.8% in 2024, underscoring the depth of adoption in the region. South India is seeing growing momentum in cargo three-wheelers driven by logistics and e-commerce activity in cities like Bangalore, Hyderabad, and Chennai. East India remains a large volume market for passenger e-rickshaws due to cultural familiarity and state-level support, while West India is emerging as a hub for goods carrier adoption linked to manufacturing and port-based logistics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vehicle Type: Passenger carriers account for the largest share in the India electric three-wheeler market by vehicle type, a position built on decades of e-rickshaw adoption across the country's vast urban and semi-urban belt. Their dominance is reinforced by affordable pricing, easy financing availability, and operational simplicity that appeals to owner-drivers. The Goods Carrier segment, though smaller in volume terms, is growing at pace with the fastest CAGR in the market, propelled by Mahindra Last Mile Mobility, Omega Seiki, and Bajaj Auto actively launching cargo models tailored to the e-commerce and cold-chain delivery sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Battery Range: The above 100km battery range segment is gaining market share at the expense of shorter-range models as operators increasingly seek vehicles capable of covering full working days. The growing availability of lithium-ion powered models in this range, including Bajaj's GoGo at 251 km and TVS King EV MAX at 179 km, is normalising longer-range expectations among buyers. The up to 100km segment retains significance in price-sensitive rural markets where short daily routes make the economics of lower-capacity models compelling for individual owner-operators.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India's dominance in India's electric three-wheeler market is rooted in a combination of geographic, demographic, and policy advantages that no other region currently matches. Uttar Pradesh alone accounts for a disproportionate share of national e-rickshaw registrations, supported by state-level subsidies, low commercial vehicle permit requirements, and the sheer density of short-haul passenger transport routes connecting urban centres with surrounding towns and villages. Delhi has emerged as a particularly strong market for goods carrier electric three-wheelers, where EV penetration in the electric three-wheeler goods segment reached 74.8% in 2024 according to EVreporter data. Government-issued e-rickshaw financing through schemes like PM E-Drive continues to incentivise first-time buyers, while the expanding network of battery swapping stations in the NCR is addressing range anxiety for commercial operators.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India represents a fast-growing secondary market, particularly in Bangalore, Hyderabad, and Chennai, where rapid expansion of food delivery, quick-commerce, and B2B logistics is creating strong demand for goods carrier electric three-wheelers. The region benefits from a higher concentration of technology-oriented logistics startups that prefer electric fleets for their lower per-kilometre fuel cost and improved ESG credentials. East India, anchored by West Bengal and Bihar, remains a high-volume market for lower-cost passenger e-rickshaws, largely driven by the affordability and cultural familiarity of e-rickshaws as a form of public transport. Manufacturers are increasingly tailoring product offerings to each region's specific requirements: long-range cargo vehicles for South and West India's logistics corridors, and cost-optimised passenger models for East and North India's mass-market e-rickshaw operators.

India's electric three-wheeler market presents a dynamic and intensely competitive landscape, with established automotive groups, dedicated EV startups, and new entrants from the two-wheeler industry all vying for position in a market that grew 18% in unit terms in CY2024 to reach 691,000 units. The sheer number of active participants, nearly 580 players, ensures that no single company holds a commanding majority, leaving meaningful room for challengers to grow through product differentiation, financing partnerships, and regional focus strategies.

Competition is increasingly playing out across multiple fronts: battery technology and range, pricing and financing accessibility, after-sales service and spare parts availability, and smart feature integration for fleet operators. Companies that can combine strong OEM capabilities with fintech partnerships and battery infrastructure integration are positioned to outperform in both the passenger and goods carrier segments over the forecast period.

Additionally, after-sales service networks are being expanded to boost customer confidence, while digital platforms are being leveraged for vehicle diagnostics, customer engagement, and real-time tracking. Many India electric three-wheeler companies are setting up local assembly and R&D facilities to stay competitive. Partnerships and collaborations with battery suppliers, fintech companies, and fleet operators are helping expand distribution and financing accessibility. These integrated strategies are enabling players to cater to both passenger and cargo segments, particularly in urban and semi-urban regions.

Founded in 1945 and headquartered in Mumbai, Mahindra Group operates across a broad range of sectors with Mahindra Last Mile Mobility as its dedicated electric three-wheeler unit. Mahindra is India's largest three-wheeler manufacturer and exporter, with strong brand equity across both passenger and cargo segments. The company's electric portfolio includes the Treo and Zor Grand models, and it has been actively investing in expanding distribution and after-sales infrastructure. Mahindra Last Mile Mobility's leadership sees long-term growth driven by organic demand, lower operational costs, and improving financing conditions.

Piaggio Vehicles Pvt. Ltd, the Indian arm of Italy's Piaggio Group, is headquartered in Pune and has been a long-standing presence in the Indian three-wheeler market through its Ape brand. The company has expanded its electric lineup with the Ape Electrik series across both cargo and passenger variants, combining lithium-ion battery systems with Piaggio's global engineering expertise. Piaggio positions itself on quality, reliability, and technological sophistication, targeting buyers willing to pay a modest premium for a proven product with strong dealer support. The company is also expanding its Southeast Asia and Africa presence, leveraging learnings from its India operations.

Kinetic Green Energy and Power Solutions Ltd is a Pune-headquartered company and part of the USD 600 million Firodia Group. It specialises in electric battery-operated vehicles ranging from compact personal carriers to multi-seat configurations. Kinetic Green has established a credible market position in the passenger electric three-wheeler space and competes on price competitiveness and reach in semi-urban and rural markets. The company benefits from the Firodia Group's deep automotive manufacturing heritage and distribution infrastructure, providing a stable foundation for scaling its EV operations as demand from Tier 2 and Tier 3 cities continues to grow.

Omega Seiki Mobility, headquartered in New Delhi, is one of India's most active players in electric cargo three-wheelers and specialised last-mile logistics EVs. The company's product range includes the Rage+, Stream, and other models targeting urban freight and cold-chain logistics. Omega Seiki has formed several strategic partnerships with fleet operators and logistics companies to deploy its vehicles at scale across Indian cities. Its focus on the commercial and B2B segment positions it directly in the highest-growth demand pocket within India's electric three-wheeler market, where e-commerce-driven cargo volumes are expected to sustain strong double-digit growth through 2035.

Other key players in the market are Zuperia Auto Private Limited, ATUL Auto Limited, Yatri Electric Vehicle, Saera Auto Private Limited, Citylife Electric Vehicles, Bajaj Auto Limited, TVS Motor Company, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

India's electric three-wheeler sector is moving faster than most markets expected even three years ago. Whether you are an OEM planning a new product launch, a fleet operator evaluating a switch to electric, or an investor assessing the sector's growth runway, our 2026 to 2035market report delivers the data and competitive intelligence you need to act with clarity. From North India's e-rickshaw dominance to the surging goods carrier opportunity, every critical segment is covered in detail. Download your free sample report today and gain your first look at the trends reshaping India's last-mile mobility landscape.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India electric three‑wheeler market reached an approximate value of USD 1.32 Billion.

The market is projected to grow at a CAGR of 13.40% between 2026 and 2035.

The key players in the market include Mahindra Group, Piaggio Vehicles Pvt. Ltd., Terra Motors India, Kinetic Green, Zuperia Auto Private Limited, Omega Seiki Mobility Private Limited, ATUL Auto Limited, Yatri Electric Vehicle, Saera Auto Private Limited, and Citylife Electric Vehicles, among others.

North India is expected to grow at 14.7% CAGR through 2035.

Key strategies driving the market include localized manufacturing to control costs, fleet-focused product customization, and integration of telematics for uptime monitoring.

Key challenges include uneven charging infrastructure availability, battery degradation under high daily usage, and limited standardization across components.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Vehicle Type |

|

| Breakup by Power Type |

|

| Breakup by Battery Range |

|

| Breakup by Component |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.