Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

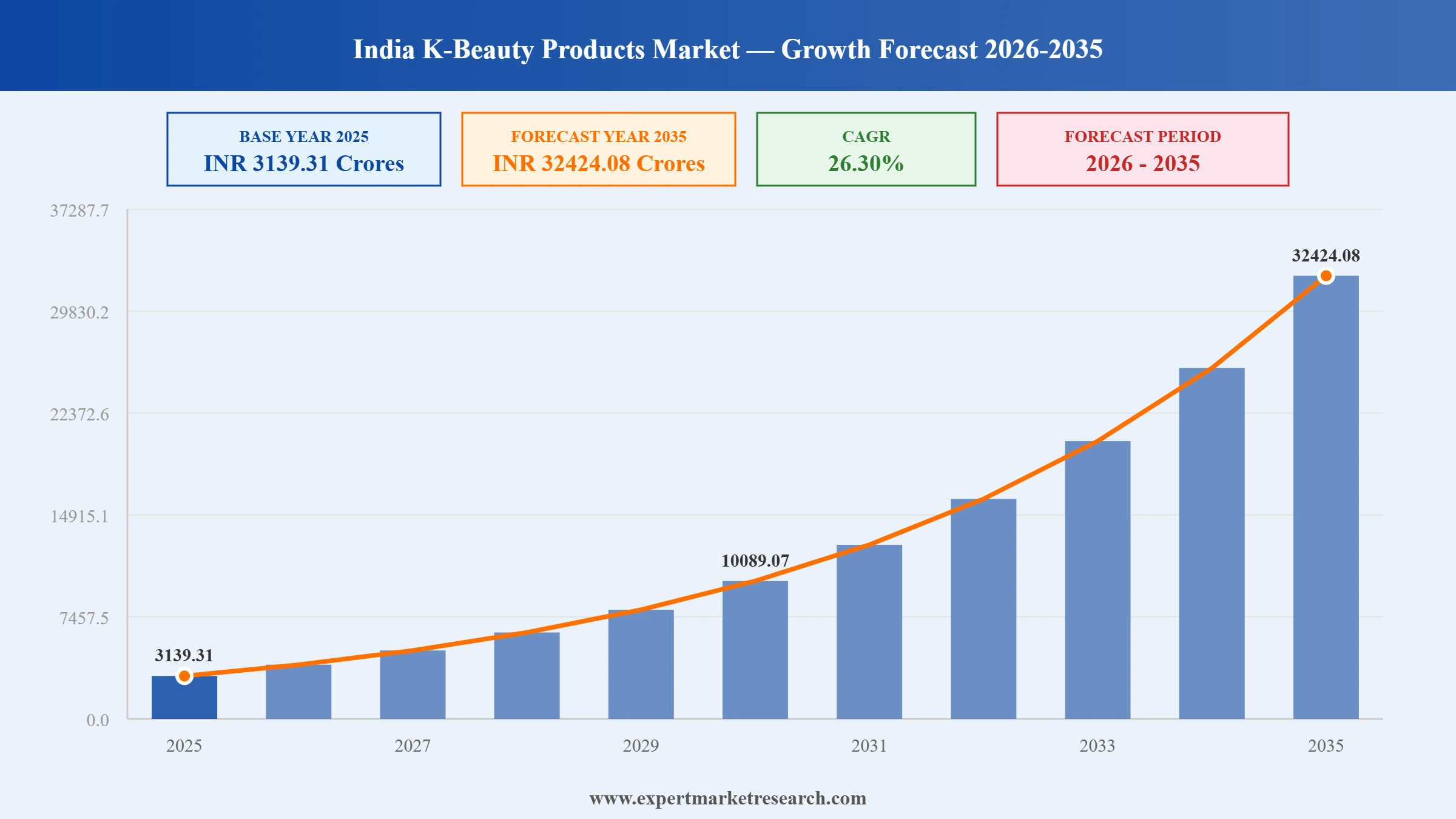

The India K-Beauty Products Market reached a value of INR 3139.31 Crores at 2025 and is projected to expand at a CAGR of around 26.30% during the forecast period of 2026-2035. With surging K-pop and K-drama cultural influence, rising consumer preference for ingredient-led skincare, growing male grooming awareness, and rapid e-commerce penetration into tier-2 and tier-3 cities, the market is expected to reach INR 32424.08 Crores.

Personal Care Insights reported on April 2, 2026 that Korean beauty companies are accelerating their entry into India to offset volatility across the SWANA region. APR rolled out its Medicube line on Nykaa, while Amorepacific introduced dermocosmetic brand Illiyoon to local consumers. The pivot signals a structural shift in the India K-beauty products market, anchored by quick-commerce reach, young buyers, and rising premium skincare demand.

According to Adgully, Nykaa announced the exclusive India launch of Illiyoon on March 4, 2026, deepening its decade-long alliance with Amorepacific. The dermocosmetic brand, known for its Soy-Ceramide and Ceramide Skin Complex 2.0 formulations, targets sensitive and barrier-compromised skin. The launch reinforces Nykaa's K-beauty shelf alongside Aestura, Laneige, and Sulwhasoo, positioning dermocosmetics as a high-growth pillar within the India K-beauty products market.

The India K-Beauty products market growth is rooted in surging consumer interest in innovative, ingredient-centric skincare. As local awareness around specialized skincare increases, demand for imported K-Beauty items has soared. For instance, Nykaa has exclusively launched the Korean skincare brand Numbuzin in India, offering a range of numbered products targeting specific skin concerns. This move reflects the growing consumer preference for personalized skincare solutions and the increasing availability of K-Beauty products across the Indian market.

Community engagement through micro-influencers and native content creators is a mechanism for receiving grassroots adoption of K-Beauty. These individuals are important for establishing trust with new participants and communicating with customers in Hindi and regional languages. For example, Tira Beauty partnered with prominent influencers to demonstrate their products, specifically, Milktouch Jelly Fit Tinted Glow Tint and Hedera Helix Relaxing Cream. These influencers will share tutorials and reviews about products on platforms like Instagram and YouTube. Their content reached the tech-native youth and first-time buyers in semi-urban and rural markets, increasing awareness and promoting adoption.

Collagen-infused products are rapidly gaining traction in the India K-beauty market as consumers increasingly seek solutions for anti-aging, skin elasticity, and hydration. Inspired by Korean skincare routines emphasizing youthful, radiant skin, Indian buyers are adopting collagen-based serums, creams, and supplements, thus bolstering the India k-beauty products demand. For example, brands like Renee Cosmetics, Innisfree, and The Face Shop are capitalizing on India’s growing fascination with K-beauty by launching collagen-infused creams, serums, and sheet masks. Renee’s Glass Glow Serum and Hydra Boost Collagen Cream mirror Korean skincare principles focusing on hydration and radiance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India K-Beauty Products Market Report Summary |

Description |

Value |

|

Base Year |

INR Crores |

2025 |

|

Historical Period |

INR Crores |

2019-2025 |

|

Forecast Period |

INR Crores |

2026-2035 |

|

Market Size 2025 |

INR Crores |

3139.31 |

|

Market Size 2035 |

INR Crores |

32424.08 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

26.30% |

|

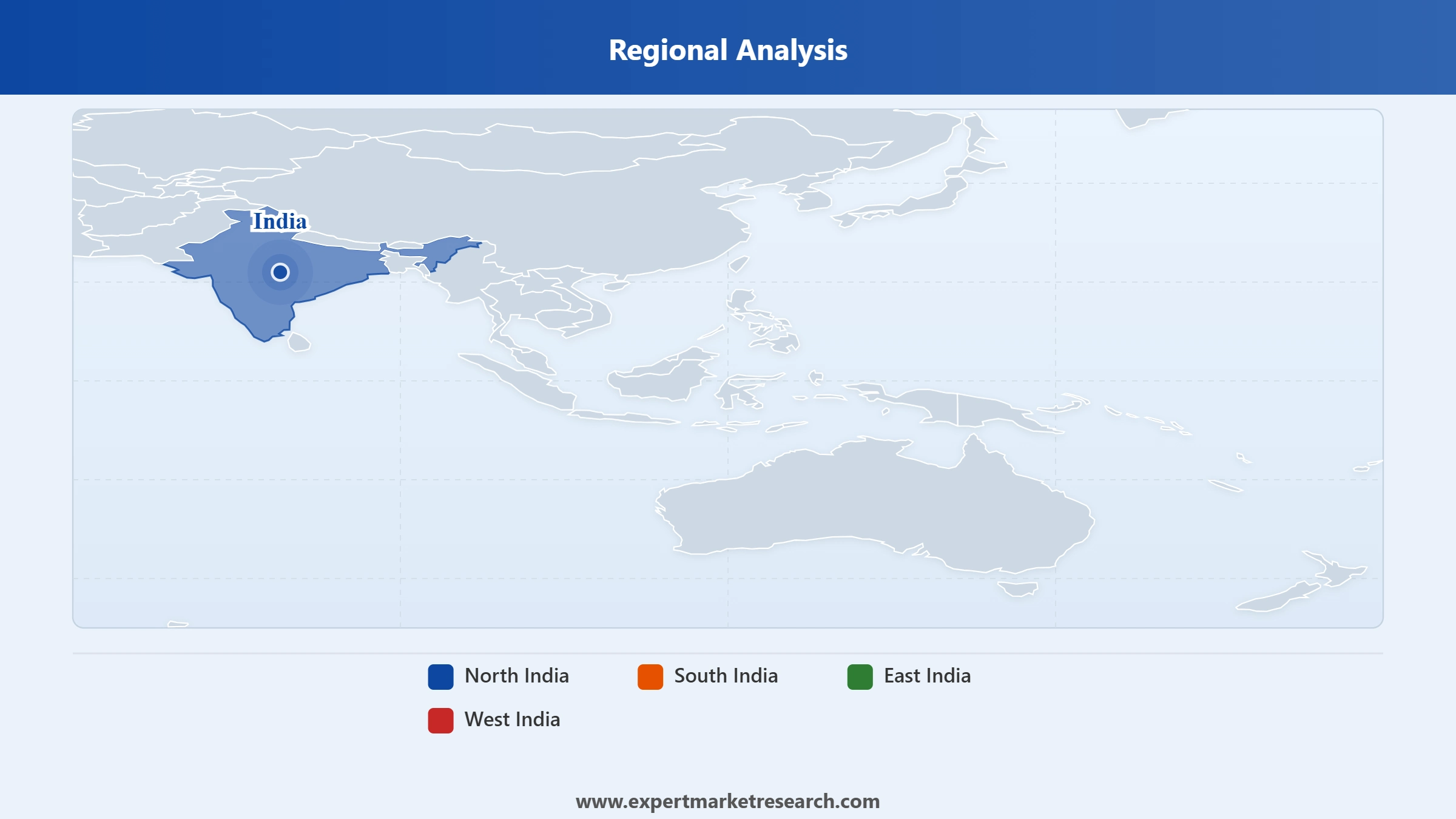

CAGR 2026-2035 - Market by Region |

South India |

28.9% |

|

CAGR 2026-2035 - Market by Region |

West India |

27.9% |

|

CAGR 2026-2035 - Market by Product |

Skin Care |

28.6% |

|

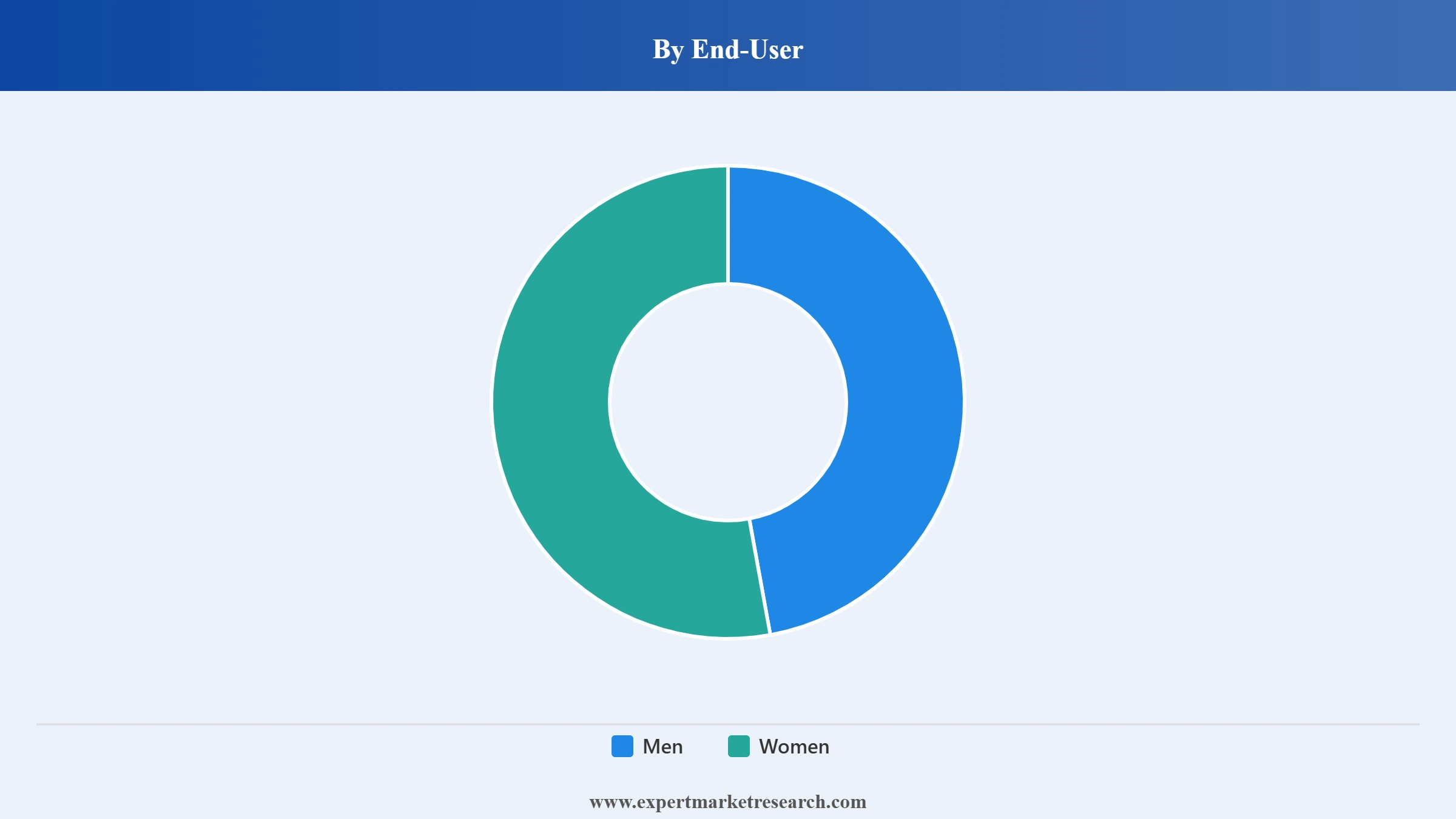

CAGR 2026-2035 - Market by End-User |

Men |

28.1% |

|

2025 Market Share by Region |

South India |

33.1% |

The India K-Beauty Products Market is witnessing transformative growth shaped by cultural shifts, ingredient innovation, digital retail expansion, and the emergence of new consumer demographics. These trends are collectively pushing the market to one of the fastest growth trajectories in Asia's beauty sector.

In September 2025, Nykaa broadened its Korean beauty offering by launching two new haircare brands in India under a renewed partnership with South Korean beauty giant Amorepacific: Mise En Scene and RYO. The move marked nearly a decade of collaboration between both companies. Mise En Scene focuses on "glass hair" shine and repair technology, while RYO brings scalp health solutions rooted in traditional Korean herbal science. The dual launch signals that the K-beauty category in India is expanding well beyond skincare into a robust haircare segment, opening a new growth avenue for both platforms.

In early 2025, South Korean K-beauty technology company APR entered the Indian market through a strategic partnership with Nykaa, the country's leading lifestyle and beauty platform. Through this collaboration, APR introduced its Medicube brand, bringing dozens of clinically inspired skincare products to Indian consumers for the first time. The partnership leverages Nykaa's deep consumer reach across both metro cities and emerging tier-2 markets, while giving APR a credible, high-traffic retail channel to build brand familiarity among India's rapidly expanding base of skincare-conscious shoppers.

Laneige, the iconic South Korean beauty label, officially introduced its Bouncy and Firm Serum in Mumbai in March 2025. The serum features the brand's proprietary Peony and Collagen Complex, specifically designed to enhance skin elasticity and deep hydration. The launch directly addressed the growing Indian consumer appetite for science-backed, result-oriented K-beauty products. By entering one of Asia's fastest-growing beauty markets with a flagship serum product, Laneige reinforced its intent to establish a strong long-term retail footprint across India's premium skincare segment.

In August 2024, Tira, the beauty retail platform backed by Reliance Industries, introduced Mixsoon, a South Korean clean beauty brand, to Indian consumers. Mixsoon's product range includes minimalist, ingredient-focused skincare formulations that have gained a loyal following in South Korea and globally. The launch underscored Tira's strategy of curating premium international beauty brands for Indian shoppers and reflected Reliance's broader ambition to dominate the premium beauty retail market in India through differentiated K-beauty positioning.

In April 2024, Tira Beauty exclusively launched the Korean brand Kundal on its e-commerce platform. Kundal, known for its botanical hair care range featuring honey and macadamia ingredients, was among the first Korean brands to enter the Indian market through a single-platform exclusive retail arrangement. The launch highlighted the growing importance of digital-first distribution strategies for K-beauty brands entering India, where online platforms offer direct access to millions of millennial and Gen Z consumers who drive the majority of K-beauty discovery and purchases.

The deepening influence of K-pop and K-drama on Indian youth continues to reshape beauty preferences at a fundamental level. Korean entertainment content consumed through platforms like Netflix, YouTube, and Instagram has embedded the concept of "glass skin" and multi-step skincare into the aspirational identity of Indian millennials and Gen Z. This cultural connection drives purchase intent beyond mere product awareness, as consumers actively seek to replicate Korean beauty routines. In March 2025, Laneige introduced its Bouncy and Firm Serum in Mumbai, directly leveraging this cultural pull to convert aspirational demand into product adoption. The India K-Beauty Products Market growth continues to benefit meaningfully from this K-culture wave.

Historically dominated by skincare, the K-beauty category in India is now witnessing a clear expansion into hair care. Consumers who discovered K-beauty through sheet masks and serums are showing strong willingness to extend the same ingredient-led logic to shampoos, conditioners, and scalp treatments. Korean haircare brands differentiate themselves through science-driven formulations targeting scalp health, hair repair, and shine enhancement. In September 2025, Nykaa and Amorepacific jointly launched the Mise En Scene and RYO brands in India, marking a deliberate push to develop K-beauty haircare as a distinct retail category alongside the established skincare segment.

Digital retail channels, including platforms like Nykaa, Amazon India, Purplle, and quick-commerce services such as Blinkit and Zepto, are making K-beauty accessible far beyond metropolitan hubs. Consumers in smaller Indian cities who previously had limited access to international beauty brands can now discover, research, and purchase K-beauty products within minutes. This democratisation of access is one of the most powerful structural drivers behind the market's rapid expansion. According to a kindlife and Datum Intelligence joint study released in 2025, the number of K-beauty buyers in India is projected to more than double from 11.9 million in 2024 to 27.2 million by 2030, with tier-2 and tier-3 markets contributing a significant share of that growth.

Indian men are increasingly adopting structured skincare routines, moving well beyond the traditional category of face wash and moisturiser. The influence of K-beauty on male grooming stems from the global K-pop aesthetic where polished, hydrated, and even-toned skin is considered aspirational for men as much as women. K-beauty brands have been proactive in developing product lines specifically addressing male skin concerns such as oiliness, acne, and pigmentation. The men's segment of the India K-Beauty Products Market is projected to grow at a CAGR of 28.1% during the forecast period, making it the single fastest-growing demographic group within the market and a key target for brand investment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “India K-Beauty Products Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Product

Key Insight: Skin Care is the dominant product category in the India K-Beauty Products Market, driven by the overwhelming consumer interest in targeted, ingredient-led formulations like serums, sunscreens, and cleansers that form the backbone of the classic Korean skincare routine. The segment is projected to grow at a CAGR of 28.6% during the forecast period, supported by viral trends such as the "glass skin" aesthetic, growing awareness about UV protection, and the rising adoption of multi-step routines by Indian women. Hair Care is the faster-rising secondary segment, propelled by innovations in scalp science and brand launches from Amorepacific-owned labels like RYO and Mise En Scene that are entering India specifically to serve this demand.

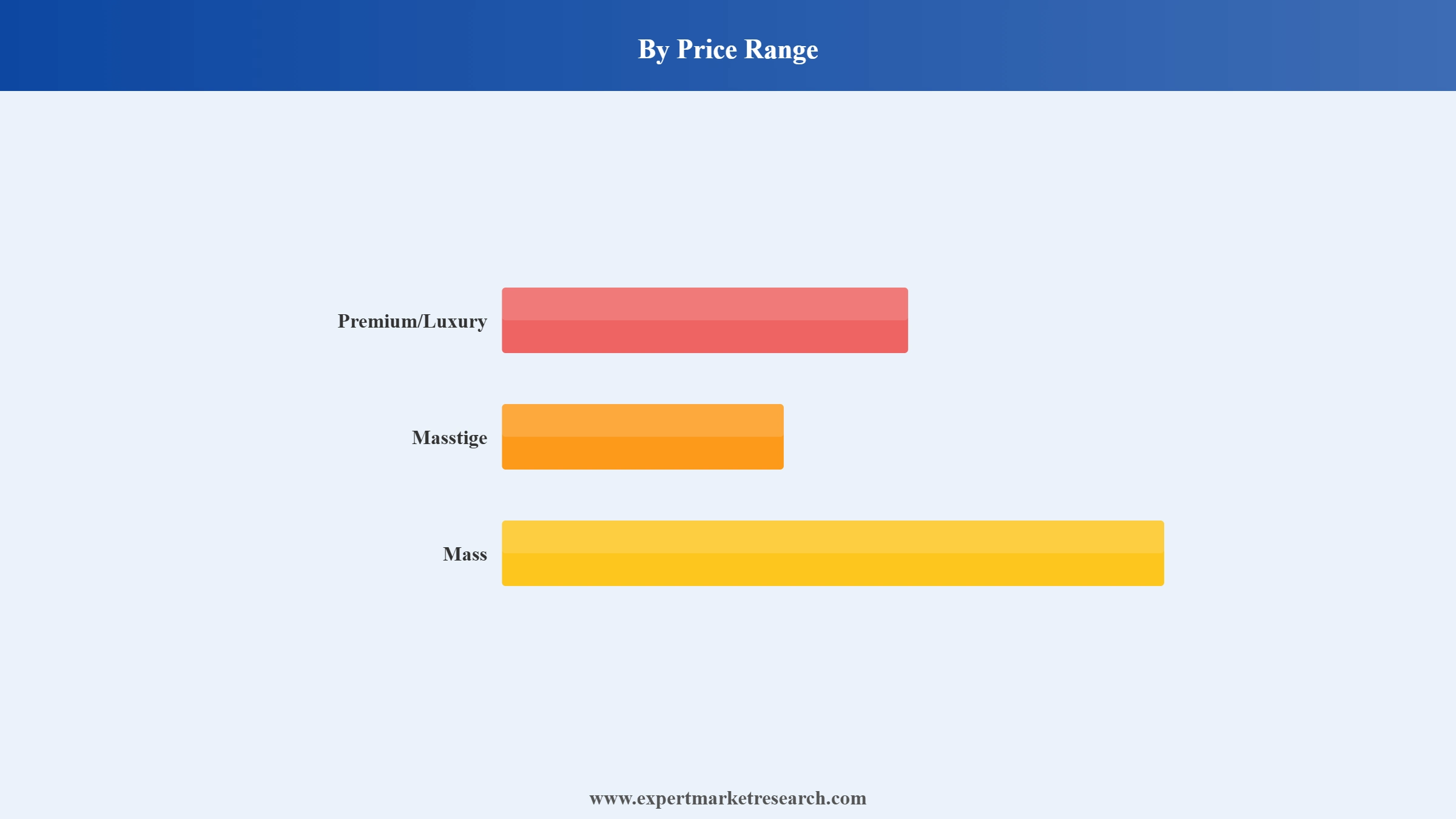

Market Breakup by Price Range

Key Insight: The Premium/Luxury segment leads the India K-Beauty Products Market in terms of revenue share, driven by a growing cohort of high-income urban consumers in cities like Delhi, Mumbai, and Bengaluru who actively seek advanced, clinically formulated Korean skincare. These consumers associate premium pricing with product efficacy and are brand-loyal to labels like Sulwhasoo, Laneige, and Amorepacific. Masstige products are the fastest-growing price tier as they allow first-time K-beauty adopters to access aspirational Korean formulations at accessible price points, particularly through e-commerce platforms that facilitate affordable luxury discovery.

Market Breakup by End-User

Key Insight: Women remain the dominant end-user segment in the India K-Beauty Products Market, accounting for the majority of revenues through strong adoption of skincare routines, hair care regimens, and colour cosmetics influenced by K-drama beauty aesthetics. The women's segment is sustained by active experimentation with products like essences, sleeping packs, and multi-step routines. However, the Men segment is growing at a CAGR of 28.1%, as K-beauty brands introduce targeted solutions for acne, pigmentation, and SPF protection tailored specifically to male skin types, appealing to younger Indian men who have been drawn into grooming through K-pop culture.

Market Breakup by Distribution Channel

Key Insight: Online/e-commerce platforms dominate due to convenience, wide product variety, and access to international brands. E-commerce supports targeted marketing, influencer marketing, and easy viewing of product reviews, and is therefore especially popular among urban millennials and Gen Z. In April 2024, Tira, a multi-brand beauty retailer, exclusively launched the Korean beauty brand Kundal on Tira e-commerce. Such occurrences will further bolster the demand for K-Beauty products in India.

Market Breakup by Region

Key Insight: North India is the largest regional market for K-beauty products, underpinned by the high concentration of affluent urban consumers in Delhi, Gurugram, and Chandigarh who display strong affinity for premium imported beauty products. The region's established premium retail infrastructure, including multi-brand stores, Nykaa physical outlets, and specialty boutiques, provides ideal distribution access. South India, meanwhile, is the fastest-growing regional market at a projected CAGR of 28.9%, with Bengaluru and Chennai emerging as vibrant hubs for K-beauty adoption among tech-savvy, digitally connected younger consumers. West India and East India are developing steadily, supported by e-commerce accessibility and rising disposable income in cities like Mumbai, Pune, and Kolkata.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Skin Care segment commands the largest share within the product segmentation of the India K-Beauty Products Market. Its dominance stems from the deep resonance of Korean skincare philosophy among Indian consumers, particularly the multi-step approach centered on hydration, sun protection, and brightening. Sheet masks, serums, and sunscreens have become gateway products that introduce Indian consumers to the broader K-beauty ecosystem, with brands like COSRX, Innisfree, and Laneige capitalising on this entry pathway. The serum sub-segment is particularly strong, driven by the anti-ageing and brightening claims that align well with the aspirations of Indian women aged 22 to 40.

Within the price range segmentation, the Premium/Luxury and Masstige tiers collectively dominate the India K-Beauty Products Market share. Premium K-beauty holds the higher revenue share due to strong brand loyalty among high-income urban consumers, while Masstige is gaining ground rapidly as e-commerce platforms lower the discovery and purchase barrier for first-time buyers in tier-2 cities. The mass segment, while smaller in revenue contribution, is growing through the proliferation of affordable Korean skincare lines on Amazon India and Flipkart that cater to price-sensitive buyers seeking quality at accessible price points.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Women segment holds the dominant share within end-user segmentation, reflecting the historically strong female consumer base for skincare and personal care products in India. Women account for the overwhelming majority of skincare and hair care purchases within the K-beauty category. However, the Men segment is experiencing the most significant structural shift, growing at nearly 28% CAGR, driven by younger male consumers discovering Korean grooming products through social media and sports endorsements. This shift is forcing brands to think beyond unisex products and invest in male-specific K-beauty product lines.

North India continues to hold the commanding position as the leading regional market in the India K-Beauty Products Market, backed by the region's high urbanisation rates, strong digital infrastructure, and a sizable base of affluent consumers willing to invest in premium skincare. Metropolitan cities such as Delhi, Gurugram, and Chandigarh serve as critical launch pads for K-beauty brands entering India, offering well-developed specialty retail channels including Nykaa stores, Sephora, and Tira outlets. Consumer preferences in North India lean towards glow-enhancing, winter-friendly skincare solutions, making moisturisers, sleeping packs, and serums especially popular. The region's deeply connected influencer ecosystem amplifies brand visibility and accelerates product adoption cycles. North India's institutional retail infrastructure and high per-capita beauty spending make it the commercial anchor of the Indian K-beauty landscape.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is positioned as the fastest-growing region in the India K-Beauty Products Market, projected to expand at a CAGR of 28.9% during the forecast period. Bengaluru and Chennai, in particular, have emerged as dynamic K-beauty hubs driven by a large base of tech-sector professionals and students who are digitally fluent and culturally attuned to global beauty trends. The widespread use of quick-commerce and beauty e-commerce platforms in these cities has lowered access barriers, enabling rapid consumer experimentation with Korean skincare products. South Indian consumers show particular affinity for lightweight gel formulations, SPF products suited to tropical climates, and ingredient-transparent serums with clearly stated efficacy claims. The region's growth momentum is expected to attract increased brand attention over the coming decade, particularly in specialty store expansion.

The India K-Beauty Products Market features a moderately consolidated competitive structure, characterised by the strong presence of leading South Korean conglomerates alongside a growing number of indie and mid-tier Korean brands entering through e-commerce partnerships. Established players like Amorepacific Corporation and LG H&H Co Ltd. dominate through diversified brand portfolios and deep retail relationships, while niche players like Banila Co. and Nature Republic carve out loyal followings through targeted product innovation and influencer-led marketing. The competitive dynamics are intensifying as the market grows, with brands actively investing in local pricing strategies, climate-adapted formulations, and digital-first go-to-market approaches.

Distribution partnerships with platforms like Nykaa and Tira are becoming a primary point of competitive differentiation, providing brands with direct access to India's expanding base of online beauty shoppers. Companies that combine ingredient transparency, cultural relevance, and competitive pricing are best positioned to capture share in both the premium and masstige tiers of the growing Indian K-beauty landscape.

Founded in 2006 and headquartered in Seoul, South Korea, Banila Co. is widely recognised for its Clean It Zero cleansing balm, a product that became a global K-beauty icon. The brand focuses on skin-friendly formulations developed for sensitive skin types and is available in India through major e-commerce platforms. Its strategy centres on affordable innovation and broad demographic appeal, positioning it as an accessible entry point into premium K-beauty for Indian consumers.

Established in 1945 and headquartered in Seoul, Amorepacific is South Korea's largest beauty conglomerate, with a portfolio spanning luxury and mass brands including Sulwhasoo, Laneige, Innisfree, and Etude House. In India, Amorepacific has pursued a multi-brand distribution strategy through Nykaa and specialty retailers. Its decade-long partnership with Nykaa was reinforced in September 2025 with the launch of Mise En Scene and RYO, extending the brand's India presence into the haircare category.

Founded in 2012 and headquartered in Los Angeles, The Creme Shop is a K-beauty inspired brand that combines Korean cosmetic philosophy with Western consumer aesthetics. The brand is particularly popular among younger shoppers for its playful packaging and affordable skincare and makeup products. In India, it is distributed primarily through e-commerce channels, reaching millennial and Gen Z consumers who prioritise novelty and value. Its wide product range across skincare and colour cosmetics makes it a versatile competitor in both the mass and masstige tiers.

Founded in 1993 and headquartered in Seoul, Clio is a South Korean cosmetics brand known for its professional-grade colour cosmetics and skincare range. The brand has built a strong following in India among consumers seeking high-pigment makeup products with skincare benefits. Clio's competitive advantage lies in its ability to bridge premium colour cosmetics with K-beauty skincare values, offering products that appeal to Indian women seeking multi-functional beauty solutions. The brand's presence through Nykaa and Amazon India has contributed to steady brand equity growth in the Indian market.

Other key players in the market are The Face Shop, Inc., Nature Republic, TolyMoly, LG H&H Co Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Ready to tap into one of the fastest-growing beauty markets in Asia? Our comprehensive India K-Beauty Products Market report for 2026 delivers the intelligence you need, from product innovation trends and pricing dynamics to regional hotspots and key competitor strategies. Whether you are launching a new Korean beauty brand in India or looking to expand an existing portfolio, this report gives you the clarity and confidence to act decisively. Download your free sample today and uncover the opportunities shaping India's K-beauty revolution.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 26.30% between 2026 and 2035.

The key players in the market include Banila Co., Amorepacific Corporation, The Crème Shop, Clio, The Face Shop, Inc., Nature Republic, TolyMoly, LG H&H Co Ltd. and others.

The market faces several significant challenges. High price sensitivity among Indian consumers, especially in tier-2 and tier-3 cities, limits the appeal of premium-priced Korean beauty products, leading some to opt for more affordable domestic alternatives.

Key strategies driving the market include localized product development, such as Innisfree’s oil-free moisturizers and sunscreens tailored to India’s climate, enhancing relevance and appeal. Brands leverage digital engagement and influencer collaborations.

Key trends in the market include expanding product portfolios to cater to diverse consumer needs. Localized product development, such as oil-free moisturizers and sunscreens, aligns with India’s climate, and omnichannel retail strategies ensure a seamless shopping experience across online and offline platforms.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Price Range |

|

| Breakup by End-User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.