Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

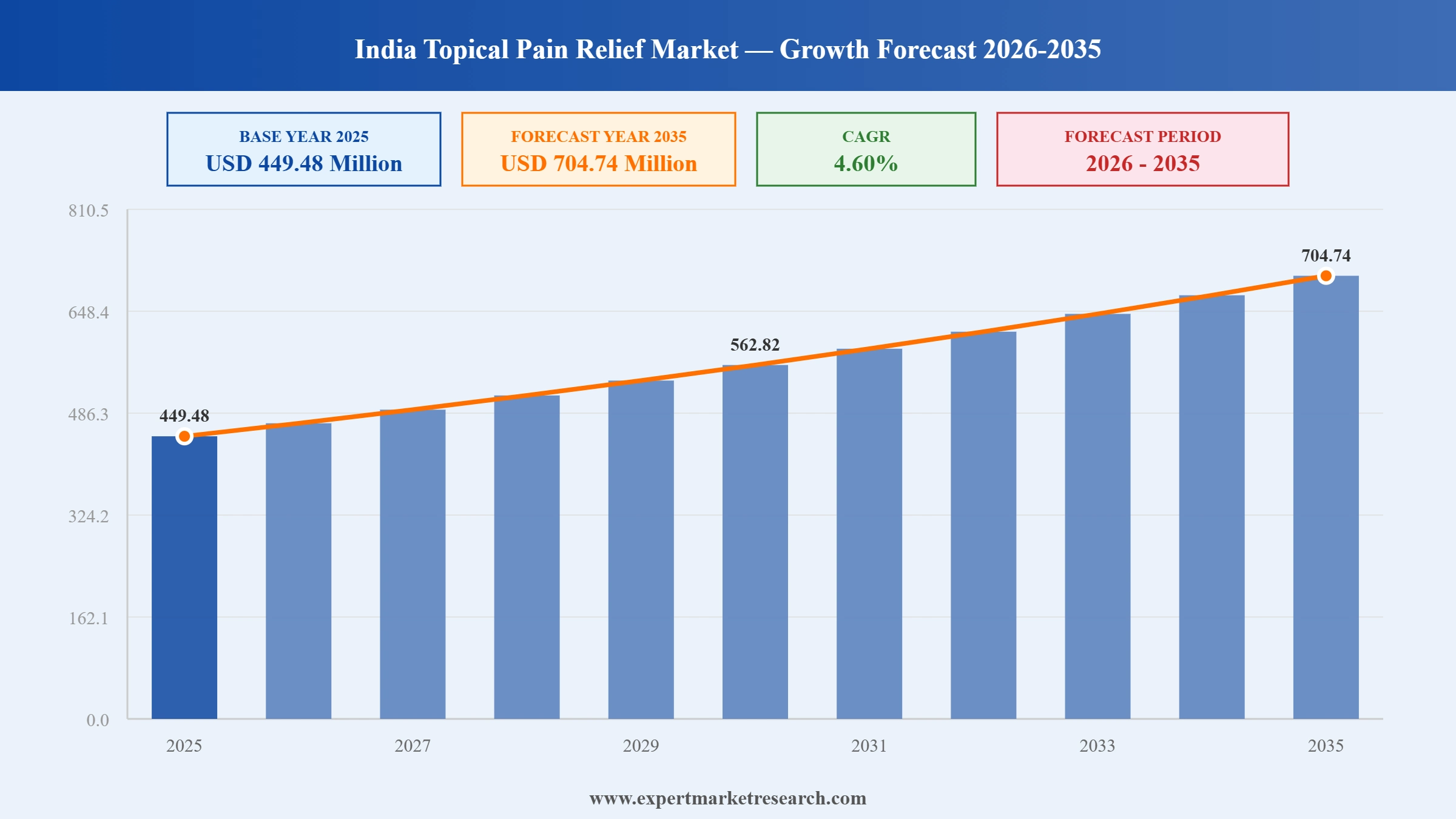

The India topical pain relief market was valued at USD 449.48 Million in 2025. It is poised to grow at a CAGR of 4.60% during the forecast period of 2026-2035, and reach USD 704.74 Million by 2035. The market growth is driven by increasing prevalence of chronic pain conditions, rising demand for non-invasive therapies, growing awareness of pain management products, expanding retail and online pharmacy networks, and continuous advancements in topical drug formulations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market reached a value of approximately USD 449.48 Million in 2025. The market is expanding steadily due to the rising prevalence of musculoskeletal disorders, arthritis, sports injuries, and chronic pain conditions. The increasing consumer preference for localized, non-invasive pain management solutions is supporting product adoption across diverse patient groups. Market growth is further encouraged by advancements in topical formulations, wider product availability through retail and online channels, and growing awareness of self-care treatments. Manufacturers are focusing on innovative delivery formats and enhanced efficacy, while improving healthcare access and changing lifestyles continue to strengthen demand for topical pain relief products across India.

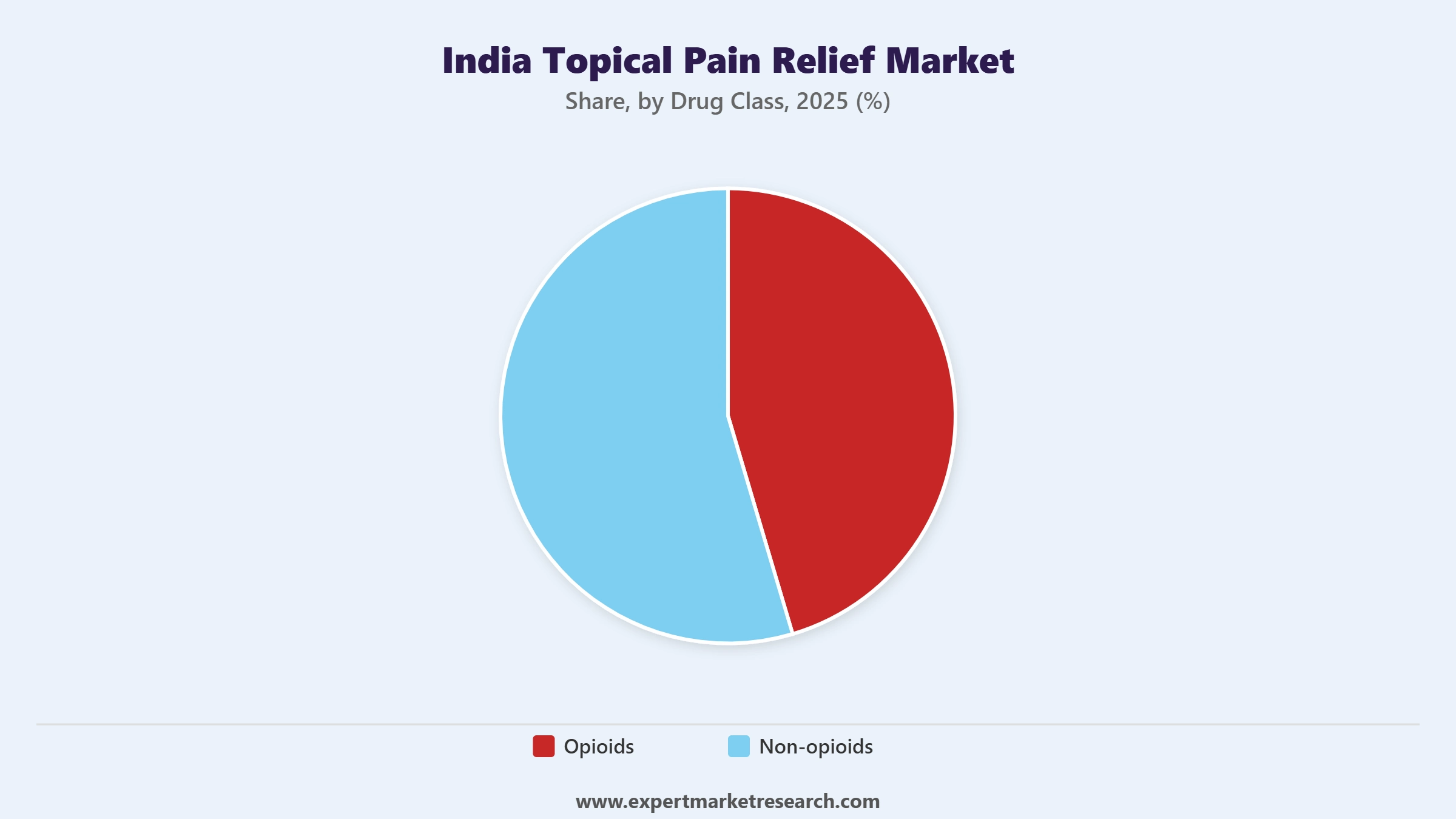

Market Breakup by Drug Class

The drug class segment comprises opioid and non-opioid therapies utilized in topical pain management. Market demand is influenced by treatment efficacy requirements, regulatory considerations, patient safety preferences, and evolving pain management practices.

Market Breakup by Formulation

The formulation segment includes creams and ointments, gels, liquids and oils, patches, sprays, and other delivery formats. Market adoption is driven by ease of application, absorption characteristics, consumer preferences, and treatment convenience.

Market Breakup by Packaging Type

The packaging type segment covers tubes, containers and jars, aerosol containers, dermal patches, and roll-on bottles. Packaging selection influences product differentiation, dosage convenience, portability, storage efficiency, and consumer purchasing decisions.

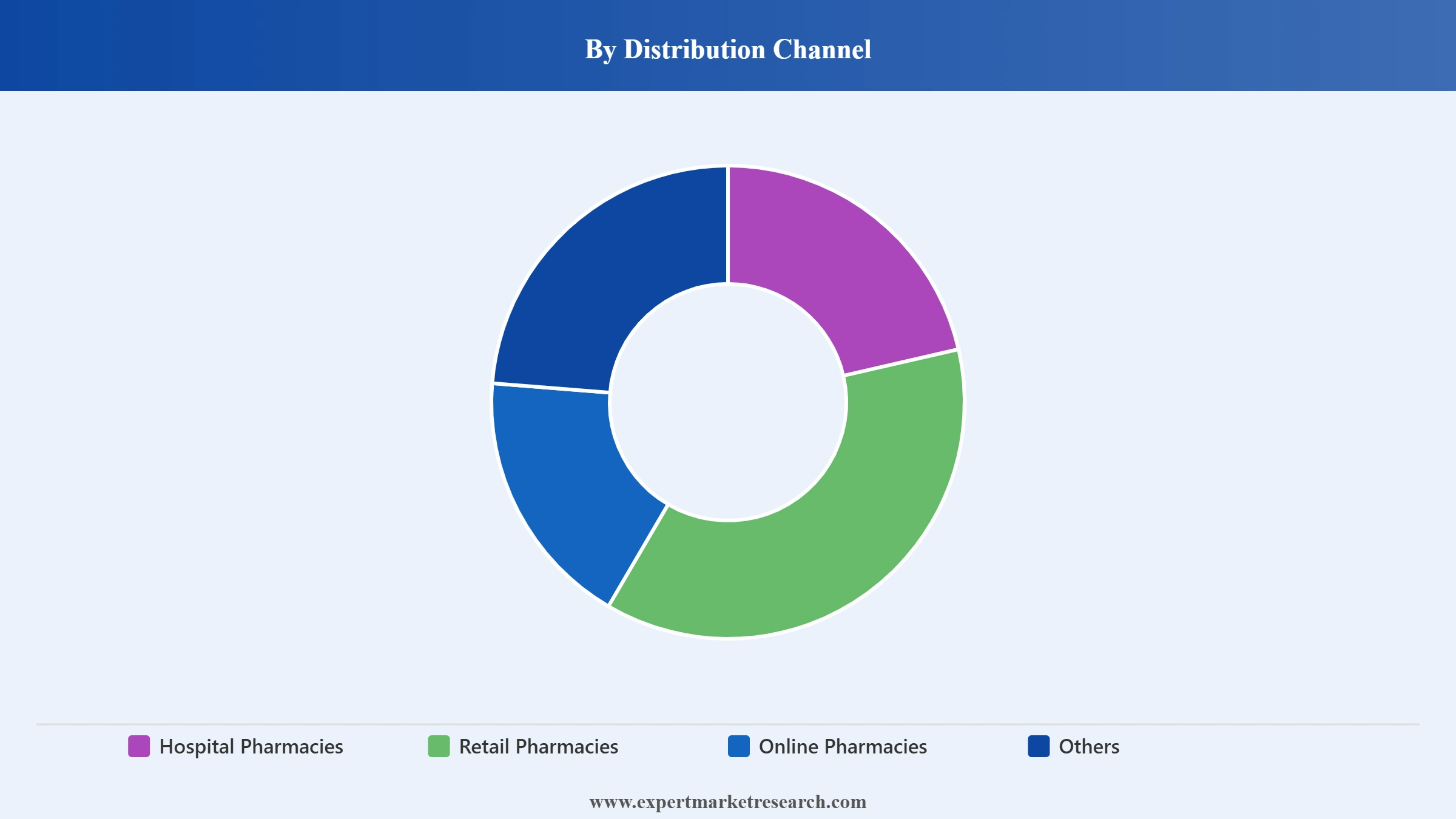

Market Breakup by Distribution Channel

The distribution channel segment encompasses hospital pharmacies, retail pharmacies, online pharmacies, and other sales outlets. Market performance is shaped by accessibility, purchasing behavior, healthcare infrastructure, prescription fulfillment, and digital commerce adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Analysis Type | Factors | Example |

| Market Drivers | Rising OTC self-care, growing muscle and nerve pain awareness, higher pharmacy availability, active lifestyle needs, and demand for targeted topical formats | For instance, in May 2026, P&G Health launched Neurobion Nerve Pain Relief Cream for nerve-related pain, tingling, and burning sensations. |

| Market Restraints | Product quality concerns, recall risk, labeling scrutiny, manufacturing compliance costs, and consumer trust issues linked to topical analgesics | For instance, in April 2025, a Class II recall was initiated for India-made Artridon Glucosamine topical analgesic after manufacturing concerns. |

| Market Opportunities | Herbal pain care, localized relief products, pharmacy-led OTC sales, e-commerce availability, and scalable natural formulations for wider consumer use | For instance, in August 2025, CSIR-CIMAP transferred technology for Panechhu pain relief balm and Relaxomap anti-inflammatory oil for mass production. |

This section analyzes key factors influencing market growth, including rising musculoskeletal disorders, increasing self-medication trends, expanding healthcare access, product innovation, evolving consumer preferences, and growing availability of topical pain management solutions.

Targeted Nerve Pain Cream Supporting Consumer Reach and Market Expansion

Rising nerve discomfort awareness and growing demand for targeted OTC care are supporting specialized topical formulations in India. For instance, in May 2026, P&G Health launched Neurobion Nerve Pain Relief Cream for symptomatic relief from nerve-related pain, tingling, and burning sensations in hands and feet. This is expected to support market growth during the forecast period by expanding condition-specific cream adoption, improving consumer trust in science-backed products, and strengthening retail pharmacy participation in differentiated pain care across urban Indian pharmacies.

Quality Concerns Pressure Topical Analgesics and Overall Market Stability

Rising OTC self-medication and wider availability of pain balms, sprays, and creams are increasing scrutiny of product quality, labeling, and manufacturing controls. For instance, in April 2025, a Class II recall was initiated for India-made Artridon Glucosamine topical analgesic after manufacturing concerns were identified for menthol and methyl salicylate tubes. This is expected to intensify market restraints during the forecast period by raising compliance costs, slowing distributor onboarding, weakening consumer trust, and pressuring manufacturers to improve batch-level quality systems.

Herbal Pain Balm Technology Transfer Opens Scalable Natural Market Avenues

Rising acceptance of herbal remedies and stronger interest in locally developed pain-care formulations are widening commercial scope for natural topical products. For instance, in August 2025, CSIR-CIMAP transferred technology for Panechhu pain relief balm and Relaxomap anti-inflammatory oil to a Haryana-based company for mass production. This is expected to create market avenues during the forecast period by supporting Ayurveda-led product scaling, expanding manufacturing participation, and improving access to plant-based topical solutions through wider distribution across pharmacies and wellness stores nationwide.

Active Muscle Care Launch Strengthens Brand Relevance and Market Development

Daily muscle stiffness and stronger consumer preference for fast topical relief are encouraging brands to refresh established pain-care portfolios. For instance, in March 2025, Haleon India launched Iodex Active Muscle Care Cream with a campaign highlighting relief from everyday muscle stiffness and pain. This is expected to support market development during the forecast period by improving brand recall, widening cream-format acceptance, strengthening active-lifestyle positioning, and helping organized retail channels serve consumers seeking convenient localized relief across metro and nonmetro areas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Tubes Likely to Dominate the Market Segment by Packaging Type

The tubes segment represented over 44% market share in the historical period and is likely to dominate the packaging landscape due to its practicality, product protection capabilities, and consumer convenience. This format supports efficient dispensing, portability, and controlled application, making it highly suitable for topical pain relief products. Manufacturers continue to favor tube-based packaging because of its compatibility with diverse formulations and cost-effective distribution benefits. Growing consumer preference for user-friendly packaging further strengthens the segment’s position. The market growth remains closely associated with sustained demand for this packaging format.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Headquartered in New Brunswick, New Jersey, United States, and established in 1886, Johnson & Johnson offers healthcare products globally. Its topical pain relief portfolio includes analgesic creams, patches, pain management solutions, and consumer healthcare products.

Headquartered in London, United Kingdom, and established in 2000 through a merger, GSK is a global healthcare company. Its portfolio includes pain relief formulations, consumer healthcare products, over-the-counter medicines, and wellness solutions.

Headquartered in New York City, United States, and established in 1849, Pfizer is a leading pharmaceutical company. Its portfolio includes pain management therapies, anti-inflammatory products, prescription medicines, and innovative healthcare solutions supporting patient care.

Headquartered in Paris, France, and established in 1973, Sanofi is a multinational healthcare company. Its portfolio includes pain relief products, consumer healthcare brands, prescription therapies, and pharmaceutical solutions addressing diverse therapeutic needs.

Other key players in the market include Reckitt Benckiser Group, Haleon Group, Bayer AG, Hisamitsu Pharmaceutical Co., Inc., Sun Pharmaceutical Industries Ltd., and Novartis AG.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

This report is developed through a robust mixed-methods research design combining:

Upto 15% Off

USD

$3099 $2789

$1999 $1799

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Drug Class |

|

| Breakup by Formulation |

|

| Breakup by Packaging Type |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.