Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

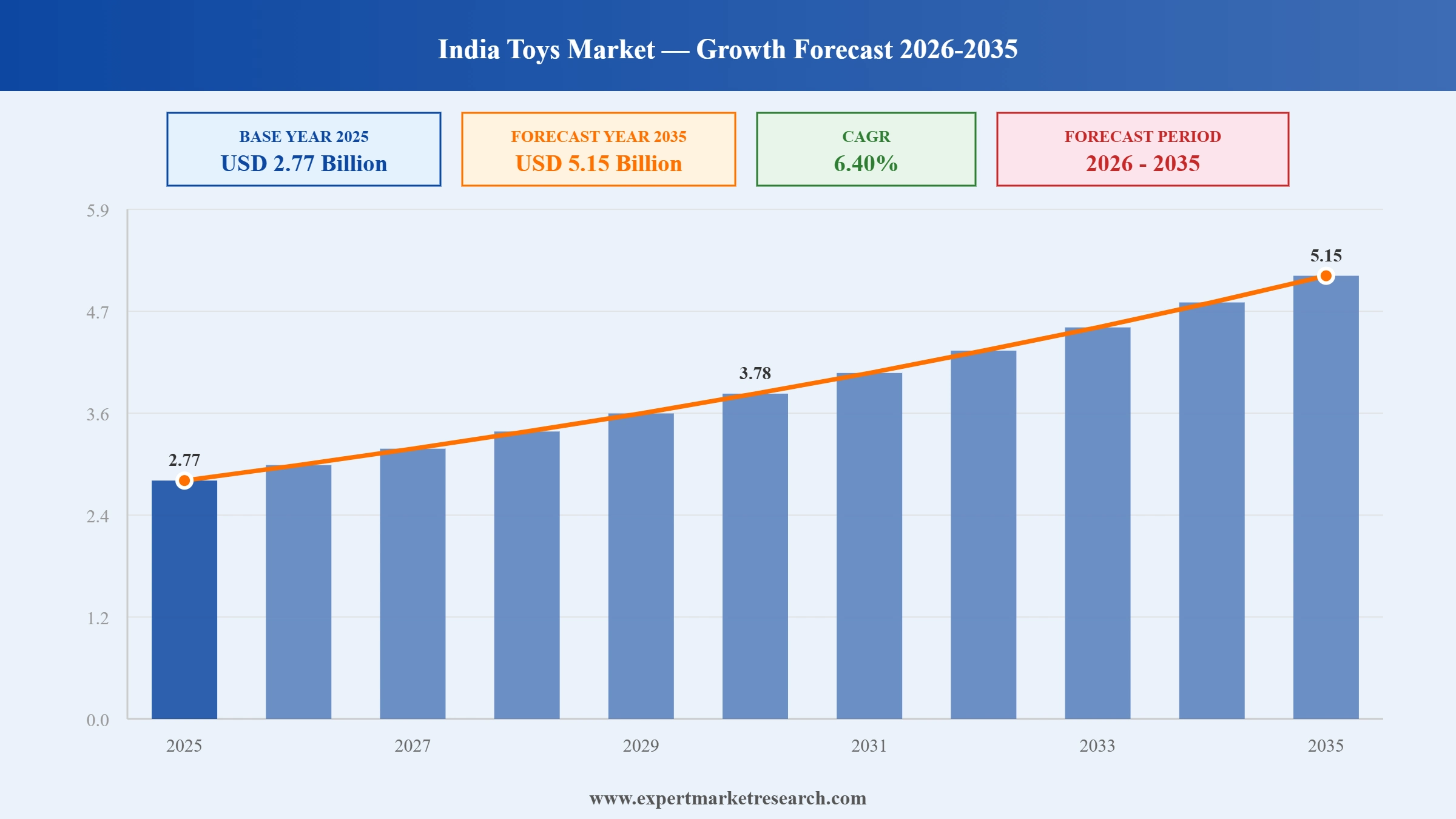

The India Toys Market reached a value of USD 2.77 Billion at 2025 and is projected to expand at a CAGR of around 6.40% during the forecast period of 2026-2035. With rapid growth in demand for STEM-based and educational toys, accelerating online retail penetration into Tier-2 and Tier-3 Indian cities, government policy support through PLI schemes and Quality Control Orders boosting domestic manufacturing, and a large and growing young consumer population, the market is expected to reach USD 5.15 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Toys Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

2.77 |

|

Market Size 2035 |

USD Billion |

5.15 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

6.40% |

|

CAGR 2026-2035 - Market by Region |

South India |

7.5% |

|

CAGR 2026-2035 - Market by Region |

East India |

6.9% |

|

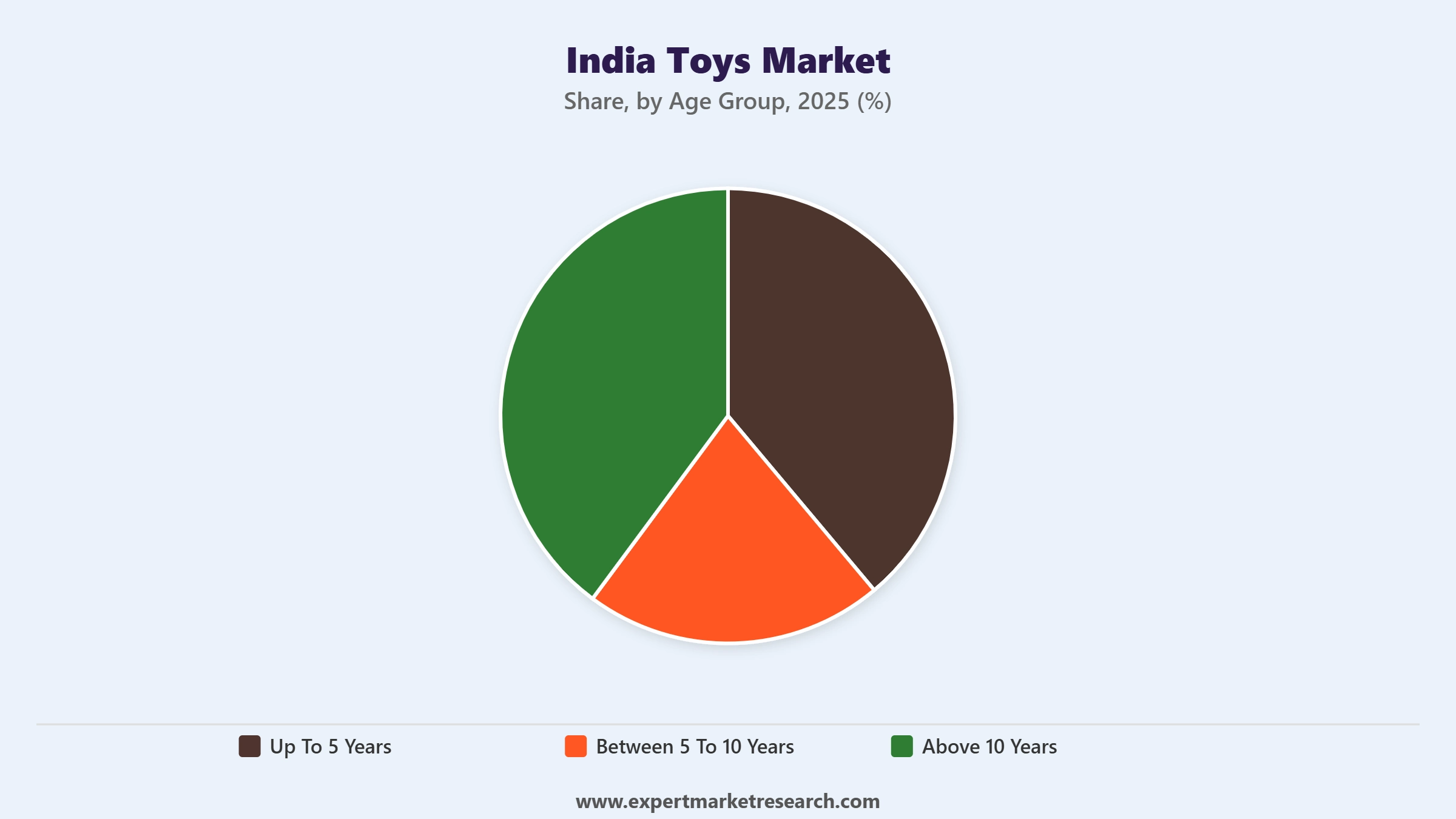

CAGR 2026-2035 - Market by Age Group |

Between 5 To 10 Years |

7.3% |

|

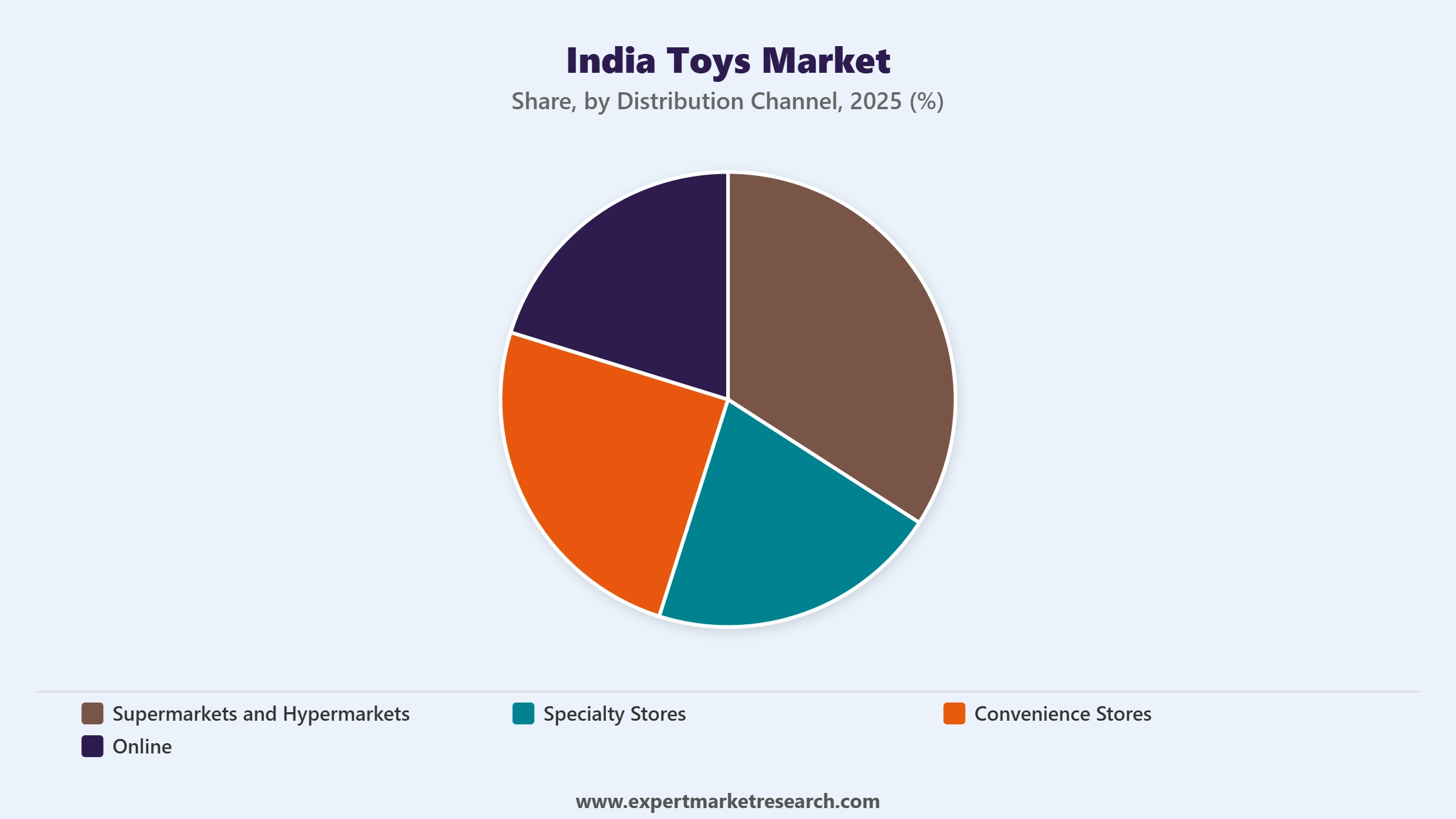

CAGR 2026-2035 - Market by Distribution Channel |

Online |

8.1% |

|

2025 Market Share by Region |

East India |

21.4% |

India's toy market is being reshaped by four structural forces acting simultaneously: a demographic dividend, sustained government policy support for domestic manufacturing, a decisive consumer shift toward educational and technology-enabled play, and the rapid expansion of e-commerce into non-metro markets.

Funskool India, one of the country's most established domestic toy manufacturers, officially entered the electronic toys product category in December 2025, signaling a strategic pivot toward technology-integrated play experiences. The move positions Funskool to compete in the fastest-growing category within the Indian toy industry, where demand for STEM-oriented, app-connected, and interactive electronic toys has been accelerating among parents who prioritise developmental value alongside entertainment. Funskool's entry into the category, backed by its existing manufacturing capabilities, distribution network, and strong brand trust, is expected to intensify competitive dynamics against international players who have historically dominated the premium electronics toy segment in India.

Union Commerce Minister Piyush Goyal confirmed in July 2025 that India's toy exports now reach 153 countries, marking a significant milestone in the country's ambition to establish itself as a global toy manufacturing hub. The expansion of India's toy export footprint reflects the combined impact of Quality Control Orders, increased import duties on finished toys, PLI scheme investments in domestic manufacturing capacity, and active government export promotion. From a domestic market perspective, this internationalisation of Indian toy manufacturers is improving product quality, design capabilities, and safety compliance across the industry, which in turn is strengthening consumer trust in domestically produced toys sold within India, a factor expected to reduce market share of low-quality unorganised sector products through the forecast period.

Mattel entered the construction and building sets toy segment in May 2025 through the launch of its Brick Shop brand, introducing direct competition against LEGO in one of the fastest-growing toy categories globally. The Brick Shop range targets price-sensitive market segments where LEGO's premium price points have historically limited penetration, making it particularly relevant for the Indian market where affordability remains a critical purchase consideration. India's building sets category has been growing steadily alongside parental awareness of the cognitive and engineering skill development benefits associated with construction play. Mattel's entry at a competitive price point is expected to meaningfully expand the addressable consumer base for building sets across both urban and Tier-2 city markets in India.

The LEGO Group announced a multi-year partnership with The Pokémon Company International in March 2025 to co-develop LEGO Pokémon product sets launching from 2026. The partnership is a significant commercial move that taps into the enormous global following of the Pokémon franchise among the 5 to 15 years age cohort, which is one of the most commercially active demographic bands in the India toys market. The collaboration is expected to drive premiumisation of the building sets segment in India, as licensed character-based LEGO sets command higher price points and stronger impulse purchase rates compared to generic construction toy offerings. The launch timeline aligns with LEGO's strategic push to deepen its presence in high-growth Asian markets, including India.

Mattel renewed its multi-year global licensing agreement with Disney for the Toy Story franchise in March 2025, announcing the development of new product lines celebrating Toy Story's 30th anniversary and in anticipation of Toy Story 5. The India market is a growing priority for Mattel's licensed product strategy, as character-driven toy lines have demonstrated strong sell-through rates on both e-commerce platforms and specialty retail stores in the country. The renewed agreement allows Mattel to maintain its portfolio strength in the Action Figures and Dolls categories, where licensed entertainment IP continues to outperform non-licensed alternatives on brand recognition and parent purchasing intent, particularly among children in the 5 to 10 years age group.

Demand for STEM-based educational toys is shifting India's toy product mix away from traditional categories toward building sets, science kits, coding games, and interactive educational charts with measurable developmental outcomes. Edtech platforms bundling interactive toys with learning subscriptions are creating a new hybrid product category particularly popular in Tier-2 and Tier-3 cities, where parents are willing to pay a premium for toys that demonstrably contribute to children's academic readiness and cognitive skills. The e-Toycathon 2025 event hosted by India's Ministry of Electronics and Information Technology further reinforced this shift, encouraging homegrown, eco-friendly electronic toy development and creating visibility for indigenous innovation in the India toys market growth narrative.

India's government has systematically restructured incentives for the toy manufacturing sector to reduce import dependency and build an internationally competitive domestic industry. Import duties on finished toys were raised from 20% to 70% between 2020 and 2023, and a Quality Control Order implemented in 2020 established mandatory safety compliance standards for both domestic manufacturers and importers. These measures have materially reduced toy imports from China while encouraging domestic production investment. The government's National Action Plan for Toys announced in Union Budget 2025-26 further formalises commitment to cluster development and skills upgrading, directly supporting the India toys market outlook for sustained manufacturing-led supply-side expansion through the forecast period.

Online channels have emerged as the dominant distribution format for toys in India, commanding a 38% market share in 2025 and showing strong growth momentum across both premium branded categories and mid-market products. E-commerce platforms including Amazon and Flipkart have dramatically widened product assortment access for consumers in cities where physical specialty toy stores are absent, while the Open Network for Digital Commerce is enabling small indigenous toy sellers to reach national audiences. India's e-commerce market itself is growing at a 19.63% CAGR, according to available market data, providing a powerful infrastructure tailwind for online toy sales India toys market trends that is expected to sustain above-market channel growth through the forecast period.

Environmental consciousness is increasingly shaping toy purchasing decisions among Indian parents, particularly those in the upper-middle income segment in major urban centres. Manufacturers are responding by expanding product lines made from recycled materials, sustainable wood, and non-toxic components, driven by both parental preference and Indian government guidance encouraging reduced plastic use in toy manufacturing. Hasbro launched a new line of eco-friendly toys made from recycled materials in September 2025, signalling that global players are adapting their product strategies to align with India's evolving consumer expectations. This shift is creating a product quality upgrade cycle that benefits premium domestic and international brands over the unorganised, low-cost import sector as India toys market forecast models account for growing sustainability premium acceptance.

The Expert Market Research's report titled "India Toys Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

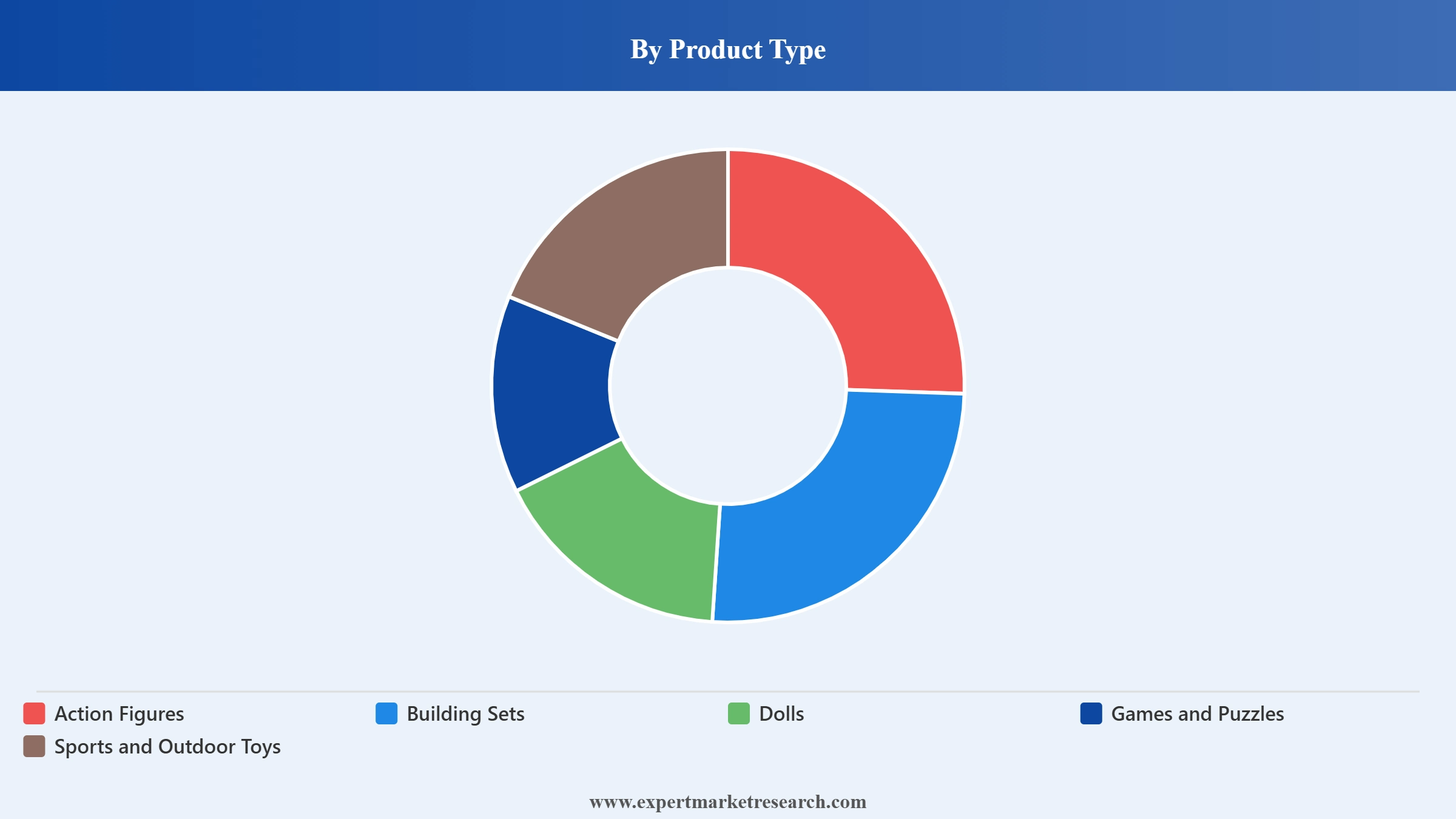

Market Breakup by Type

Key Insight: Games and Puzzles represent the dominant product type within the India Toys Market, supported by their strong adoption in formal educational contexts and institutional B2B sales to schools and edtech platforms. Subscription-based learning kits incorporating branded puzzle and game sets have created a recurring revenue dynamic that sustains category leadership even as digital entertainment competes for children's attention. Action Figures benefit from consistent IP licensing from major entertainment studios, with Disney, Marvel, and Pokemon franchise launches regularly driving sales cycles in this category. Building Sets are the fastest-growing product type, propelled by parental recognition of construction play's cognitive and engineering skill development benefits, and accelerated by international brands including LEGO and Mattel's newly launched Brick Shop range targeting both premium and mass-market price bands. Dolls remain a significant category anchored by both international brands and domestic players, with the sub-segment evolving toward gender-neutral and inclusive design narratives. Sports and Outdoor Toys represent a strong category in semi-urban and rural markets where outdoor play remains the dominant recreational behaviour among children, particularly in the 5 to 10 years age group.

Market Breakup by Age Group

Key Insight: The 5 to 10 Years age group dominates toy purchases in India, coinciding with the critical window for cognitive, social, and emotional development where parental investment in quality educational toys is highest. This age segment has the broadest overlap with school curriculum-aligned toys, STEM kits, and multi-player games, creating high demand intensity and strong willingness to pay premium prices from educated urban parents. The Up To 5 Years segment is driven by safety-conscious parents seeking developmentally appropriate toys from trusted brands with established safety certifications, creating a premium positioning opportunity for brands like Chicco and Funskool with infant and toddler-specific portfolios. The Above 10 Years segment, while smaller in traditional toy purchases, is the fastest-growing area for tech-integrated toys including coding kits, robotics sets, and app-connected interactive play products, reflecting the influence of STEM education priorities and technology familiarity among older children. This segment's overlap with digital platforms also makes it highly responsive to social media-driven toy discovery and peer influence on purchase decisions.

Market Breakup by Distribution Channel

Key Insight: Online has emerged as the leading distribution channel for toys in India, holding approximately 38% market share in 2025, driven by expanding e-commerce platform penetration, convenient home delivery, competitive pricing, and access to wide product assortments that physical stores in Tier-2 and Tier-3 markets cannot replicate. Major platforms including Amazon and Flipkart have transformed toy accessibility, while the Open Network for Digital Commerce is enabling smaller domestic toy makers to reach national buyers. Specialty Stores remain important for premium and branded toys, where knowledgeable staff, product demonstrations, and interactive displays significantly influence purchase decisions. Funskool's specialty retail network and Hamleys India's experience-driven store format are particularly effective in converting high-value toy purchases in metro markets. Supermarkets and Hypermarkets hold a meaningful share through volume-driven promotional placements and impulse purchase opportunities, particularly for lower-price-point categories including puzzles, balls, and basic action figures. Convenience Stores play a supporting role in impulse-driven purchases in urban catchment areas.

Market Breakup by Region

Key Insight: West India, specifically Maharashtra, leads the India Toys Market with approximately 20% market share in 2025, supported by a concentration of major toy manufacturing facilities, robust retail infrastructure, and a large consumer base in Mumbai and Pune. Maharashtra's policy environment has attracted toy manufacturing investment aligned with the PLI scheme, while its highly urbanised consumer base demonstrates strong spending on branded and premium toy categories. North India is the second-largest regional market, anchored by Delhi-NCR's high disposable income base and extensive retail infrastructure across speciality stores, hypermarkets, and online fulfilment. South India is the fastest-growing region, driven by increasing urbanisation in Bengaluru, Hyderabad, and Chennai, rising middle-class incomes, and growing parental emphasis on educational toy investment. East India represents an emerging market with lower current penetration but accelerating growth as e-commerce platforms expand distribution reach into states including West Bengal, Odisha, and Assam, overcoming the historical disadvantage of underdeveloped physical toy retail infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Games and Puzzles hold a strong leadership position within the Product Type segmentation, driven by their entrenched role in India's formal education sector and the rapid expansion of edtech-bundled subscription learning kits that routinely incorporate branded puzzle and game sets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Their high institutional sales volume, repeat purchase behaviour, and measurable developmental outcomes make them the preferred choice for parents and educators alike, particularly across the commercially powerful 5 to 10 years age group that constitutes the market's most active purchasing demographic. Alongside Games and Puzzles, Building Sets are gaining meaningful share through growing awareness of construction play's engineering skill development benefits, amplified by the recent entry of Mattel's Brick Shop brand creating new price tier access points that complement LEGO's premium positioning in the category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online channels dominate the Distribution Channel segmentation with approximately 38% market share in 2025, a position built on e-commerce platform expansion, wide product assortment access, and competitive pricing that physical retail cannot match outside major metro markets. Within the Age Group segmentation, the 5 to 10 Years cohort represents the largest and commercially most valuable consumer segment, driven by parents' investment in educational and developmental toys at the stage of peak cognitive development. West India, led by Maharashtra with approximately 20% of national market share, holds the leading regional position through manufacturing concentration and high consumer spending capacity. South India is the fastest-growing region, drawing increasing toy sales from rising household incomes in major southern cities and growing consumer preference for branded, quality-assured toy products over the unorganised sector alternatives that have historically served these markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the fastest-growing regional market for toys in India, driven by rising urbanisation, expanding middle-class incomes, and an increasingly education-conscious consumer base across Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana. Bengaluru, Hyderabad, and Chennai are the primary urban toy consumption markets within the region, with parents in these cities demonstrating strong willingness to invest in premium educational and STEM-based toy categories. The region's high concentration of technology professionals and exposure to global consumer trends through digital platforms has accelerated consumer interest in international toy brands and technology-integrated play products. South India's toy retail infrastructure, while less developed than the west and north, is rapidly improving through the expansion of online channels, specialty retail formats, and hypermarket toy sections in large format malls across tier-1 and growing tier-2 cities. Government manufacturing investments in Tamil Nadu and Andhra Pradesh are also expanding domestic production capacity within the region, reducing supply-side constraints.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India Toys Market features a moderately fragmented competitive structure, with a mix of established international brands, strong domestic players, and a large unorganised sector providing low-cost alternatives across mass-market price bands. Global players including Mattel, Hasbro, and LEGO dominate the premium segment through brand recognition, licensed IP portfolios, and design innovation, while domestic manufacturers such as Funskool and Ok Play India leverage local manufacturing scale, cost competitiveness, and government PLI eligibility to compete effectively in the mid-market. The competitive environment is shifting toward quality-based differentiation as Quality Control Orders and BIS compliance requirements reduce the competitive advantage of low-cost, low-specification alternatives.

International brands are increasingly investing in localised strategies for India, including character-based licensed products aligned with Bollywood and Indian animation IP, entry-level pricing tiers addressing the mass market, and deeper partnerships with Indian e-commerce platforms for last-mile distribution reach. Domestic manufacturers are responding to technology trends by expanding into electronic and interactive toy categories, as demonstrated by Funskool India's December 2025 entry into electronic toys. Specialty toy retail and e-commerce are the primary competitive battlegrounds, while sustainability-led product innovation is emerging as a differentiator targeting the premium urban parent consumer segment.

Founded in 1945 and headquartered in El Segundo, California, Mattel is one of the world's largest toy manufacturers, operating a broad portfolio of iconic brands including Barbie, Hot Wheels, Fisher-Price, Matchbox, and UNO. In India, Mattel distributes its products through a mix of e-commerce, specialty retail, and hypermarket channels, with strong demand for its action figure, doll, and games categories. In March 2025, Mattel renewed its multi-year global licensing agreement with Disney for the Toy Story franchise, and in May 2025 launched the Brick Shop brand to enter the building sets segment. Mattel's global reach and licensed IP depth give it a durable competitive position in India's premium toy market.

Founded in 1923 and headquartered in Pawtucket, Rhode Island, Hasbro is a leading global toy and game company with a portfolio spanning Monopoly, Nerf, Play-Doh, Transformers, and My Little Pony. Hasbro operates in India through distribution partnerships and direct e-commerce presence, with particular strength in the Games and Puzzles, Action Figures, and Sports and Outdoor categories. In September 2025, Hasbro launched a new line of eco-friendly toys made from recycled materials, aligning its product strategy with growing consumer preference for sustainable products in India's urban markets. Hasbro's diverse portfolio across multiple price points allows it to serve India's broad consumer income spectrum from mass-market to premium.

Founded in 1932 and headquartered in Billund, Denmark, LEGO is the world's most recognised building set brand, with a strong and growing presence in India's toy market. The company's products command premium price points but have demonstrated consistent growth among India's upper-middle-income urban households where parental emphasis on developmental play is strongest. LEGO maintains distribution through specialty stores, major e-commerce platforms, and brand experience stores in select Indian cities. In March 2025, LEGO announced a multi-year collaboration with The Pokémon Company International for LEGO Pokémon sets launching in 2026, extending its licensed IP strategy to attract younger consumers in the 5 to 10 years age group.

Founded in 1987 and headquartered in Chennai, Funskool is India's most established domestic toy manufacturer and one of the few Indian brands operating across games, puzzles, action figures, and infant toys at national scale. The company manufactures and distributes international partner brands in India and operates its own product lines, competing effectively in the mid-market against imported alternatives. Funskool's manufacturing operations in Ranipet, Tamil Nadu, were expanded in 2024 to increase domestic production capacity, and in December 2025 the company officially entered the electronic toys segment, reflecting its strategic response to growing STEM and technology-integrated toy demand. Its pan-India distribution network and government PLI eligibility give it structural cost advantages over fully imported brands.

Other key players in the market are Goliath Games, LLC, Chicco, and Ok Play India Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The India Toys Market is evolving faster than ever, shaped by a young demographic, government-driven manufacturing transformation, and a seismic shift toward educational and technology-integrated play. Our comprehensive analysis of the India Toys Market 2026 gives you the data-driven clarity you need on product innovation trends, distribution channel dynamics, regional growth leaders, and competitive strategy. Whether you are launching a new toy range, entering the Indian market, or assessing investment in domestic manufacturing, this report is your strategic starting point. Download your free sample now and explore the opportunities in India's growing toy industry.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India Toys market reached an approximate value of USD 2.77 Billion.

The market is projected to grow at a CAGR of 6.40% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 5.15 Billion by 2035.

Key strategies include localization of content, integration of STEM and digital technologies, expansion into Tier II/III cities, partnerships with edtech platforms, and sustainable manufacturing aligned with government’s “Make in India” push.

Some of the key trends in the market are rising demand for STEM toys, green products, e-commerce expansion, licensed characters, and local manufacturing supported by the government.

The major regions in the market are North India, South India, East India and West India.

The various types considered in the market report are action figures, building sets, dolls, games and puzzles, and sports and outdoor toys.

The various distribution channels mentioned in the report are supermarkets and hypermarkets, specialty stores, convenience stores, online, etc.

The major players in the market are Mattel, Inc., Hasbro, Inc., LEGO System A/S, Goliath Games, LLC, Funskool Ltd., Chicco, and Ok Play India Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Age Group |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.