Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

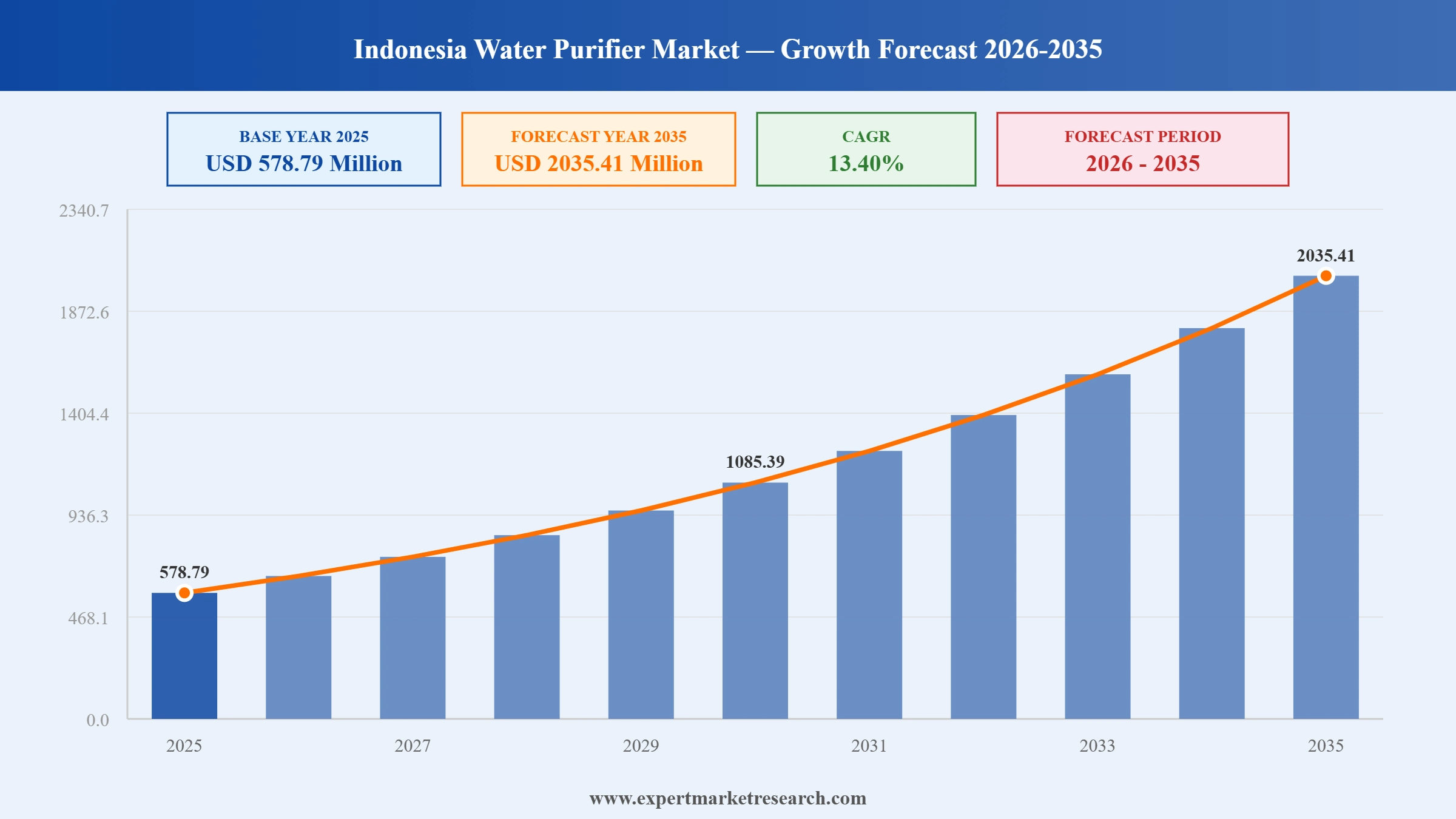

The Indonesia Water Purifier Market reached a value of USD 578.79 Million at 2025 and is projected to expand at a CAGR of around 13.40% during the forecast period of 2026-2035. With Indonesia's worsening water contamination crisis, mounting government investment in national clean water supply infrastructure, rising household health awareness, and expanding product availability through digital and physical retail channels, the market is expected to reach USD 2035.41 Million by 2035.

Indonesia is targeting 24 million new household piped water connections by 2029, effectively doubling current coverage and extending safe water access to approximately 93 million additional people under its National Long-Term Development Plan 2025-2045. As reported by Water & Wastewater Asia, this large-scale infrastructure push is driving increased reliance on point-of-use purification solutions, creating substantial growth opportunities across Indonesia's residential water purifier market.

Indonesia's Ministry of Public Works has been actively implementing its 2026 water infrastructure programme, covering pipeline network expansion, irrigation systems, and clean water facility development across the archipelago. According to Xinhua, Indonesia's coordinating minister confirmed that national water policy is being realigned to accelerate investment and expand clean water access nationwide, a shift directly increasing demand for residential and commercial water purification systems.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Indonesia Water Purifier Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

578.79 |

|

Market Size 2035 |

USD Million |

2035.41 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

13.40% |

|

CAGR 2026-2035 - Market by Technology |

UV |

15.2% |

|

CAGR 2026-2035 - Market by End Users |

Residential |

15.6% |

Indonesia's water purifier market is being driven by a fundamental and worsening public health challenge: access to safe drinking water in a country of 270 million people, 60% of whose rivers are polluted. As health awareness rises, technology advances, and both government and private investment scale up, this market is expanding rapidly across residential, commercial, and industrial end users.

ANGEL, a globally leading water purification technology company, announced its entry into the Indonesian market in June 2025, signalling growing international interest in one of Southeast Asia's fastest-growing water purifier markets. The entry adds competitive intensity to the market at a time when consumer demand for advanced purification systems is accelerating in line with urbanisation and rising health awareness. ANGEL's expansion strategy in the region was further reinforced in July 2025 when it partnered with Thailand's Mazuma and HomePro to co-develop innovative water purifiers and enhance service standards across Southeast Asia, demonstrating a regional platform approach to building market presence.

Coway launched its Villaem III water purifier in Indonesia in February 2025, featuring an advanced five-stage filtration system with automatic UV sterilisation every 12 hours. The product addresses one of the most common household water safety concerns in Indonesian urban areas, specifically the risk of microbial contamination in supplies that are physically clean but biologically unsafe. The Villaem III launch represents a broader trend of multinational water purifier brands bringing technology-led premium products into the Indonesian market as rising urban incomes allow a growing segment of households to invest in higher-end home water safety solutions.

Almar Water Solutions and Moya Indonesia formed a joint entity, Obor Infrastructure, in July 2024, designed to provide more than 425,000 cubic meters of treated water daily to urban and industrial zones across Greater Jakarta. This large-scale water services partnership reflects growing private-sector investment in Indonesia's water infrastructure, partly complementing government efforts to expand safe water access in and around the nation's most densely populated urban corridor. The development underscores the industrial water treatment opportunity in Indonesia, where water-intensive industries and tightening environmental discharge norms are driving demand for reliable, outsourced water supply and treatment solutions.

Panasonic Corporation launched an improved model of its Water Purification System in Indonesia in April 2024, designed to remove iron contaminants from well water using the company's proprietary technology. The upgraded model eliminates the need for additional pressure valves for water pressures up to 0.6 MPa and has a 50% smaller footprint than its predecessor, making it more compatible with the wide range of pump types and installation environments found across Indonesian homes. In August 2024, Panasonic followed with the launch of a complementary Water Softener, reinforcing its ambition to build a complete water solutions ecosystem for Indonesian households reliant on well water.

The Indonesian government allocated IDR 17 trillion in 2024 to improve water supply infrastructure under the National Clean Water Supply Programme, directing funds toward both rural and urban areas that lack reliable access to safe drinking water. The initiative is part of the government's goal to ensure 80% of the population has clean water access by 2025. While the public investment is focused on supply-side infrastructure, it creates complementary demand for household purification systems as consumers who gain access to piped water still require purification products to ensure the safety of that supply, given the persistent contamination challenges affecting water quality at the point of delivery.

Indonesia faces a chronic and intensifying water quality crisis that is generating sustained, non-cyclical demand for water purification systems across all end-user segments. The national water quality index stood at 54.78 in 2024, significantly below the national target. As per Ministry data, approximately 60% of Indonesia's rivers are polluted from domestic sewage, industrial effluents, and plastic waste, with the Citarum River, a major water source for Greater Jakarta, ranking among the world's most toxic waterways, contaminated by lead and mercury. The Indonesia water purifier market growth is directly tied to this structural crisis, as urban households increasingly recognise that access to piped water does not equate to safe drinking water, particularly in cities like Jakarta where sewerage coverage is only around 12%.

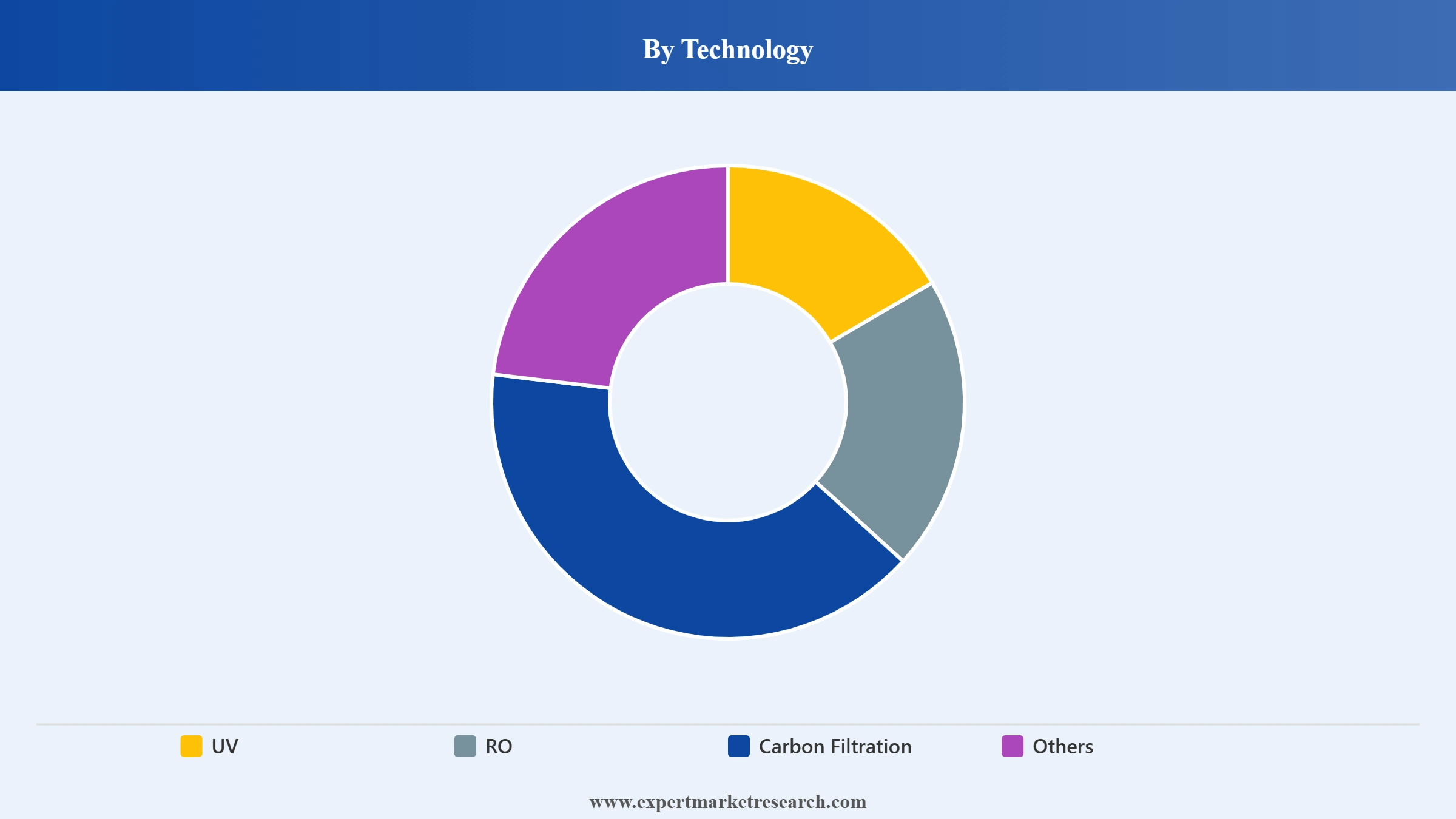

UV-based water purifiers are the leading technology segment in Indonesia and are growing at 15.2% CAGR, reflecting their strong appeal among urban households where the primary water safety concern is microbial rather than chemical contamination. UV purifiers offer a chemical-free, energy-efficient approach to disinfection that is particularly valued in households with young children or immunocompromised members who face elevated health risks from waterborne pathogens. In February 2025, Coway's Villaem III launch in Indonesia, featuring automatic UV sterilisation every 12 hours, illustrated the direction in which product innovation is moving: combining multi-stage filtration with UV disinfection in user-friendly, aesthetically designed units that appeal to the growing urban middle-class consumer.

Indonesia's rapid industrial expansion is creating a parallel demand surge for water purification in commercial and industrial settings alongside the better-known residential market. Water-intensive industries including food and beverage, textiles, pharmaceuticals, and electronics manufacturing require consistently high-quality process water, while increasingly stringent environmental regulations on industrial discharge are compelling businesses to invest in water treatment infrastructure. In July 2024, the formation of the Obor Infrastructure joint venture between Almar Water Solutions and Moya Indonesia to deliver 425,000 cubic meters of treated water daily to Greater Jakarta's urban and industrial zones illustrated the scale of commercial water services investment being deployed to meet industrial demand, and signalled growing private-sector confidence in long-term industrial water treatment as a business opportunity in Indonesia.

Government-led infrastructure investment is directly shaping Indonesia's water purifier market growth by progressively expanding the population's access to piped water while simultaneously raising awareness of water quality issues that household purifiers are positioned to address. The 2024 allocation of IDR 17 trillion under the National Clean Water Supply Programme and the awarding of the Jakarta Wastewater Management Master Plan contract in July 2024 are two concrete expressions of this policy commitment. As more households gain access to piped municipal water, the addressable market for point-of-use water purifiers expands, because consumers who transition from well or surface water to municipal supply often discover that piped water carries its own quality concerns, from chlorination byproducts to distribution pipe contamination, motivating an upgrade to household water purification.

The Expert Market Research's report titled "Indonesia Water Purifier Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Technology

Key Insight: The UV segment holds the largest revenue share in Indonesia's water purifier market, reflecting its strong fit with urban water quality challenges where microbial contamination is the primary concern. UV systems are increasingly preferred in Indonesian cities for their chemical-free operation, ease of maintenance, and effectiveness against bacteria and viruses. RO systems are gaining traction in areas where groundwater contains high levels of total dissolved solids, heavy metals, and industrial pollutants, particularly in peri-urban and industrial zones. Carbon filtration is the fastest-growing technology at a projected CAGR of 14.6%, serving households seeking taste and odour improvement or using it as a pre-filtration layer in multi-stage systems. Gravity-based and ceramic filters in the "others" category address rural demand where electricity access and consistent water pressure cannot be assumed.

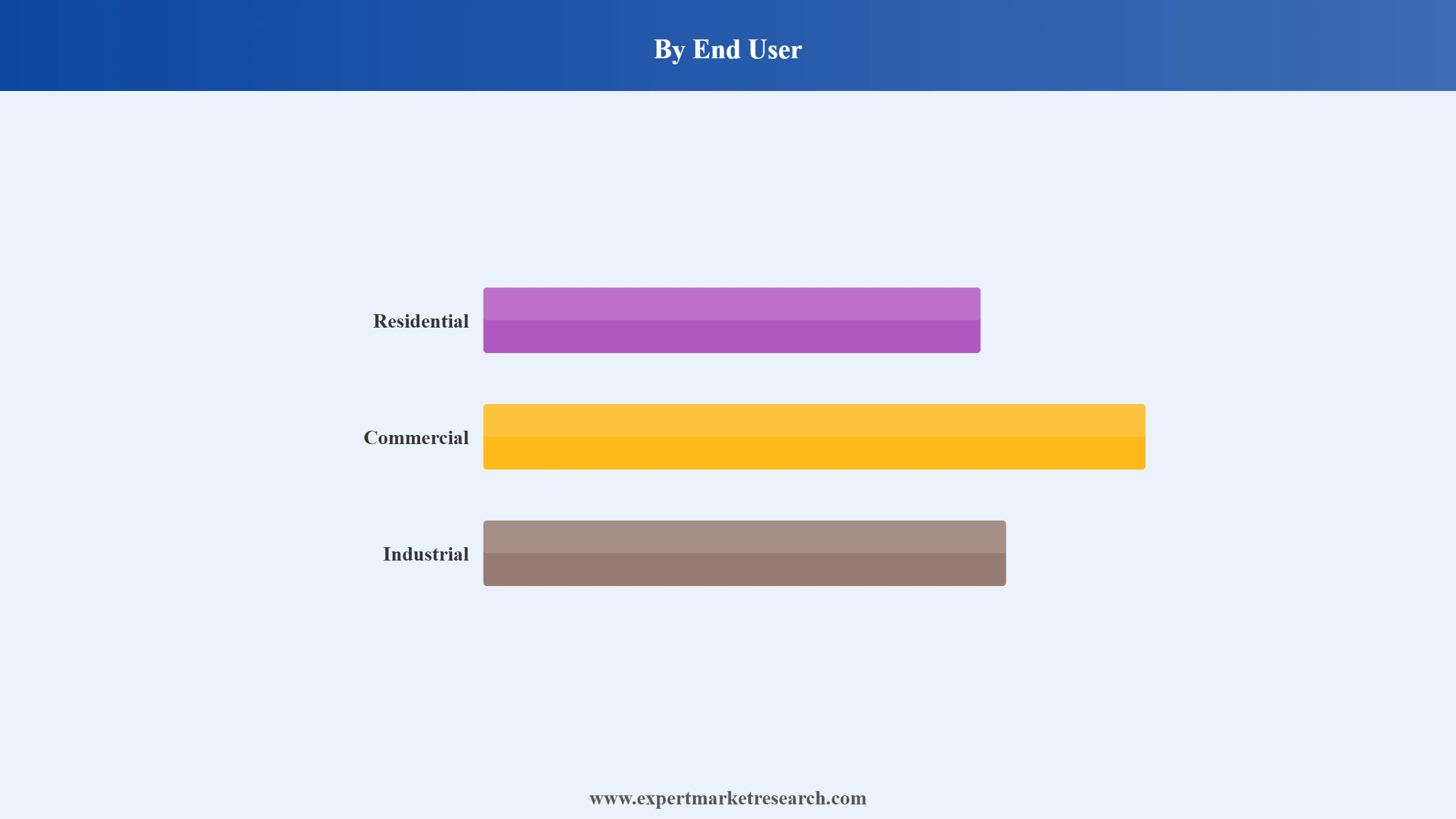

Market Breakup by End-User

Key Insight: Residential end users dominate the Indonesia water purifier market by volume and are growing at 15.6% CAGR, driven by rising consumer health awareness, deteriorating municipal water quality, and the growing middle class seeking reliable home-based water safety solutions. Commercial end users, including hotels, restaurants, schools, and healthcare facilities, represent a growing segment as businesses increasingly prioritise water quality for both regulatory compliance and customer satisfaction. The industrial end user segment is growing at the fastest pace, driven by Indonesia's expanding manufacturing base in food and beverage, textiles, and electronics, where high-quality process water is an operational necessity, and by tightening environmental discharge regulations compelling industrial operators to invest in on-site water treatment infrastructure.

Market Breakup by Distribution Channel

Key Insight: The offline distribution channel remains dominant in Indonesia's water purifier market, with electronics retailers, specialised appliance stores, and authorised dealers playing a critical role in building consumer trust, providing product demonstrations, and managing the installation and after-sales service relationships that high-consideration purchases like water purifiers require. Online distribution is growing rapidly, particularly in urban centres including Jakarta, Surabaya, and Bandung, where smartphone penetration is high and e-commerce platforms like Tokopedia and Shopee offer competitive pricing, product variety, and doorstep delivery. The water purifier online sales increase of 18% in 2024 across Indonesian e-commerce platforms reflects how effectively digital channels are reaching the younger, tech-savvy urban consumer segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Technology: UV purifiers hold the dominant share in Indonesia's water purifier market by technology, built on their effectiveness against bacterial and viral contamination in the urban water systems that serve the majority of Indonesia's purchasing population. The segment's strong CAGR of 15.2% is reinforced by continuous product innovation from brands like Coway, with its Villaem III launch in February 2025 exemplifying how manufacturers are packaging UV disinfection within multi-stage, consumer-friendly systems. RO purifiers hold a strong secondary share, particularly in high-TDS water environments, while Carbon Filtration is the fastest-growing technology as affordable, entry-level options for taste and odour improvement attract first-time purifier buyers in both urban and semi-urban markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

End User: Residential end users account for the dominant share by volume in Indonesia's water purifier market, reflecting the universal need for safe drinking water at the household level and the direct relationship between rising health awareness and residential purifier adoption. The industrial segment, while smaller in unit terms, is growing at the fastest pace in value terms as large-scale water treatment contracts for industrial zones create high-value demand that individual consumer products cannot match. Almar Water Solutions and Moya Indonesia's July 2024 formation of the Obor Infrastructure joint venture illustrates how the industrial water services segment is attracting capital and partnership investment at a scale well beyond the residential market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Indonesia occupies a critical position in the Asia Pacific water purifier landscape, not only because of its massive population of over 270 million but also because of the severity of its water quality challenges relative to its peers in the region. While markets like Japan and Australia deal primarily with the fine-tuning of already treated municipal water, Indonesia faces a more fundamental problem: a large share of its water sources are compromised at origin, with 60% of rivers polluted by industrial effluents, domestic sewage, and agricultural runoff. The Citarum River, Greater Jakarta's primary water source, is classified as one of the most toxic rivers in the world, contaminated by heavy metals. This elevated starting problem means that demand for water purification is not a lifestyle preference in Indonesia but a genuine public health necessity, creating a market with far greater structural depth than markets where water quality is already broadly acceptable.

Urban centres, particularly the Greater Jakarta metropolitan area, represent the highest-density demand markets within Indonesia, combining high contamination risk, relatively high household incomes, and access to modern retail channels that support water purifier adoption. The government's July 2024 award of the Jakarta Wastewater Management Master Plan contract to the KWJ joint venture signals long-term public commitment to improving water infrastructure in the capital region, which over time should improve baseline water quality while simultaneously raising consumer awareness of waterborne health risks. Second-tier cities like Surabaya, Bandung, and Medan are emerging as increasingly important demand markets as the urban middle class expands beyond Java's megacities, and as e-commerce platforms extend the reach of branded purification products to consumers who previously had limited access to formal retail.

Indonesia's water purifier market is served by a competitive mix of global technology leaders, European water treatment specialists, purpose-driven social enterprises, and locally embedded Indonesian companies, each occupying a distinct segment of the market and serving different consumer profiles and use cases. Global brands like 3M and Panasonic compete on technical sophistication and reliability in the urban premium and mid-market segments, while Nazava addresses the underserved rural low-income population through affordable gravity-based filtration, and BWT Indonesia targets premium residential and commercial buyers with European-standard water treatment technology.

Competition is intensifying with the entry of new players like ANGEL in 2025 and rising product innovation from Korean and Asian brands like Coway. Key competitive differentiators include filtration technology performance, product certification and safety credentials, installation and after-sales service capabilities, distribution reach into Tier 2 and Tier 3 cities, and price-performance positioning. E-commerce is emerging as a new competitive battleground where brands that can build digital presence, manage reviews, and offer platform-native purchasing journeys are gaining disproportionate reach among younger urban consumers.

Founded in 1902 and headquartered in Maplewood, Minnesota, United States, 3M is a diversified industrial conglomerate with major operations in healthcare, consumer safety, and industrial solutions. In Indonesia, 3M offers advanced water filtration systems targeting residential and commercial segments, leveraging its global R&D capabilities to deliver high-efficiency, certified purification technologies. The company's brand recognition and quality credentials make it a trusted choice for urban households and institutional buyers willing to pay a premium for reliability. 3M's strength lies in combining globally tested filtration media with a service and support infrastructure that reassures buyers in a market where post-purchase maintenance is a key purchase consideration.

Nazava is a social enterprise founded in 2009 and co-headquartered in Indonesia and the Netherlands, focused on providing affordable gravity-based ceramic water filtration solutions for low-income and off-grid communities across Indonesia and beyond. Its mission of bringing safe drinking water to populations without reliable electricity or consistent water pressure fills a gap that premium tech-based brands cannot effectively address. In 2023, Nazava partnered with Indonesia's Ministry of Public Works and Housing to enter the national procurement catalogue, and distributed approximately 500 water filters to schools serving over 80,000 students. Nazava's model of combining affordability, social impact, and government partnership gives it a unique and defensible market position in rural and semi-urban Indonesia.

Founded in 1918 and headquartered in Osaka, Japan, Panasonic Corporation is one of Asia's most recognised electronics and home appliances companies. In Indonesia, Panasonic has built a focused water solutions business through iterative product launches tailored to the specific challenges of Indonesian households, particularly those reliant on well water. The April 2024 launch of its improved Water Purification System, designed for higher-pressure pump compatibility and a reduced footprint, followed by the August 2024 Water Softener launch, demonstrates Panasonic's strategy of building a complete home water treatment ecosystem rather than competing on individual products alone. Its established service network and brand trust in Indonesia give it a meaningful advantage in the considered-purchase water purifier segment.

BWT (Best Water Technology) is a leading European water technology company, established in 1990 and headquartered in Mondsee, Austria, operating in Indonesia through local subsidiaries. BWT competes in the premium residential, hospitality, and industrial water treatment segments, emphasising sustainability, water softening, and mineral management in its product positioning. The company's European heritage and certification credentials make it a preferred choice for high-end urban consumers, international hotels, and industrial operations that prioritise water quality standards aligned with European benchmarks. BWT's sustainability-led messaging resonates well in Indonesia's growing ESG-aware corporate segment, where companies are increasingly factoring water quality into their operations management.

Other key players in the market are PT Penguin Indonesia, PT Indotech Energy Persada, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Indonesia's water purifier market is one of the most compelling growth stories in Southeast Asia, driven by a genuine and worsening public health need that is unlikely to diminish over the forecast horizon. Whether you are a water purifier manufacturer assessing your Southeast Asia strategy, a private equity investor evaluating the sector's fundamentals, or a distributor seeking a clearer view of which technologies and channels are winning, our 2026 to 2035 report delivers the comprehensive intelligence you need. From UV technology dynamics to the industrial water treatment opportunity, the full market picture is here. Download your free sample today and begin your deep dive into one of Asia Pacific's most important water purification markets.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Indonesia water purifier market reached an approximate value of USD 578.79 Million.

The market is projected to grow at a CAGR of 13.40% between 2026 and 2035.

The key players in the market include 3M Company, Panasonic Corporation, Nazava Water Filter, BWT Indonesia, PT Penguin Indonesia, and PT Indotech Energy Persada, among others.

Key strategies driving the market include product innovation (UV/RO/Carbon filters), tech-transfer partnerships, expansion into underserved regions, and e-commerce integration.

The residential segment is dominating the market, driven by rising public awareness about waterborne diseases, poor municipal water quality, and growing adoption of RO/UV systems for safe drinking water at home.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.