Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

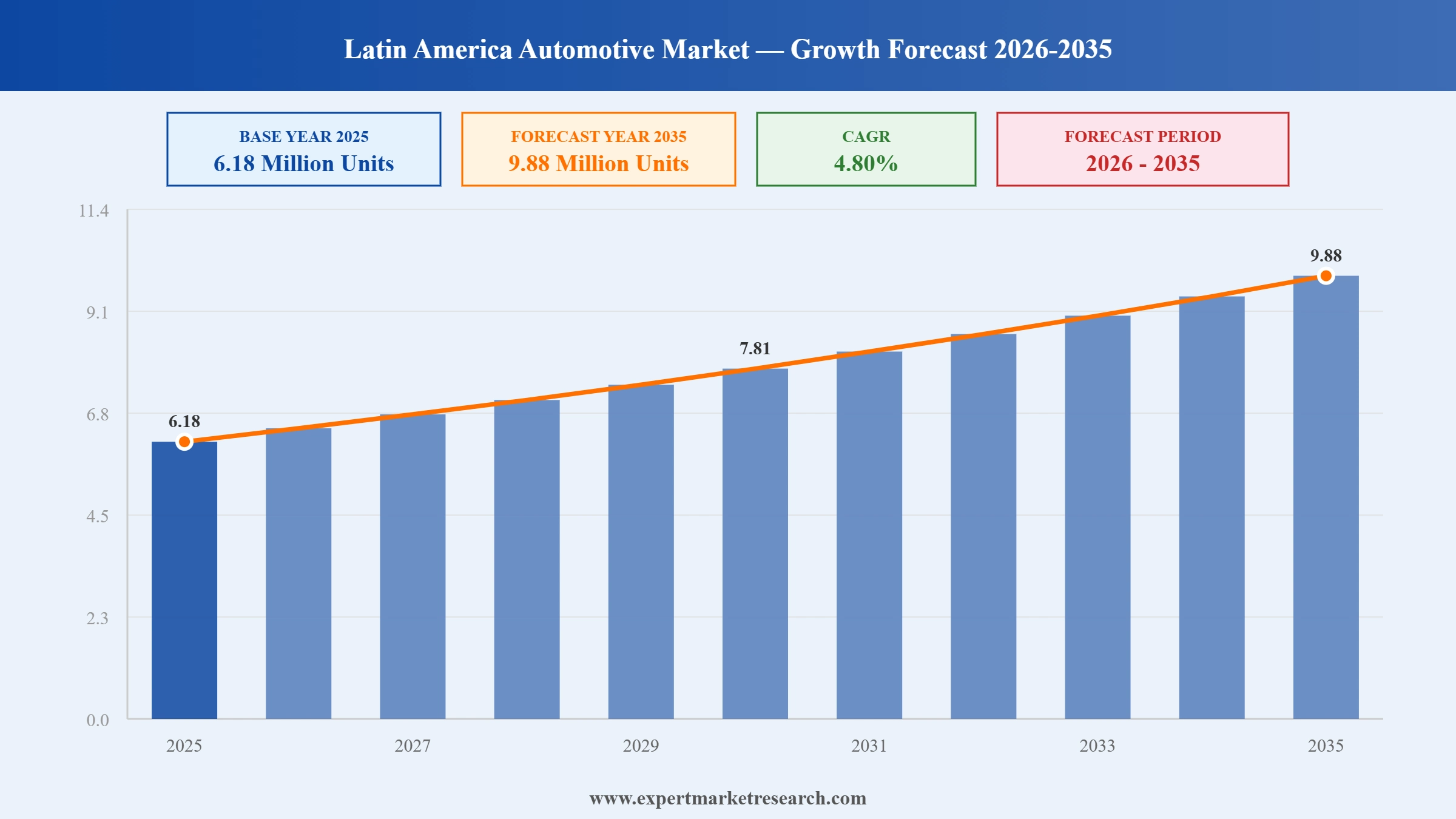

The Latin America Automotive Market reached a volume of 6.18 Million Units at 2025 and is projected to expand at a CAGR of around 4.80% during the forecast period of 2026-2035. With rising middle-class incomes driving passenger car demand across Brazil and Mexico, accelerating adoption of hybrid and electric vehicles supported by regional incentive programmes, a wave of record manufacturing investments from global and Chinese automakers building local production capacity, and expanding ride-hailing and shared mobility services creating fleet demand, the market is expected to reach 9.88 Million Units by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Latin America Automotive Market Report Summary |

Description |

Value |

|

Base Year |

Million Units |

2025 |

|

Historical Period |

Million Units |

2019-2025 |

|

Forecast Period |

Million Units |

2026-2035 |

|

Market Size 2025 |

Million Units |

6.18 |

|

Market Size 2035 |

Million Units |

9.88 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

4.80% |

|

CAGR 2026-2035- Market by Country |

Mexico |

5.5% |

|

CAGR 2026-2035 - Market by Country |

Brazil |

4.6% |

|

CAGR 2026-2035 - Market by Vehicle Type |

Passenger Vehicle |

5.3% |

|

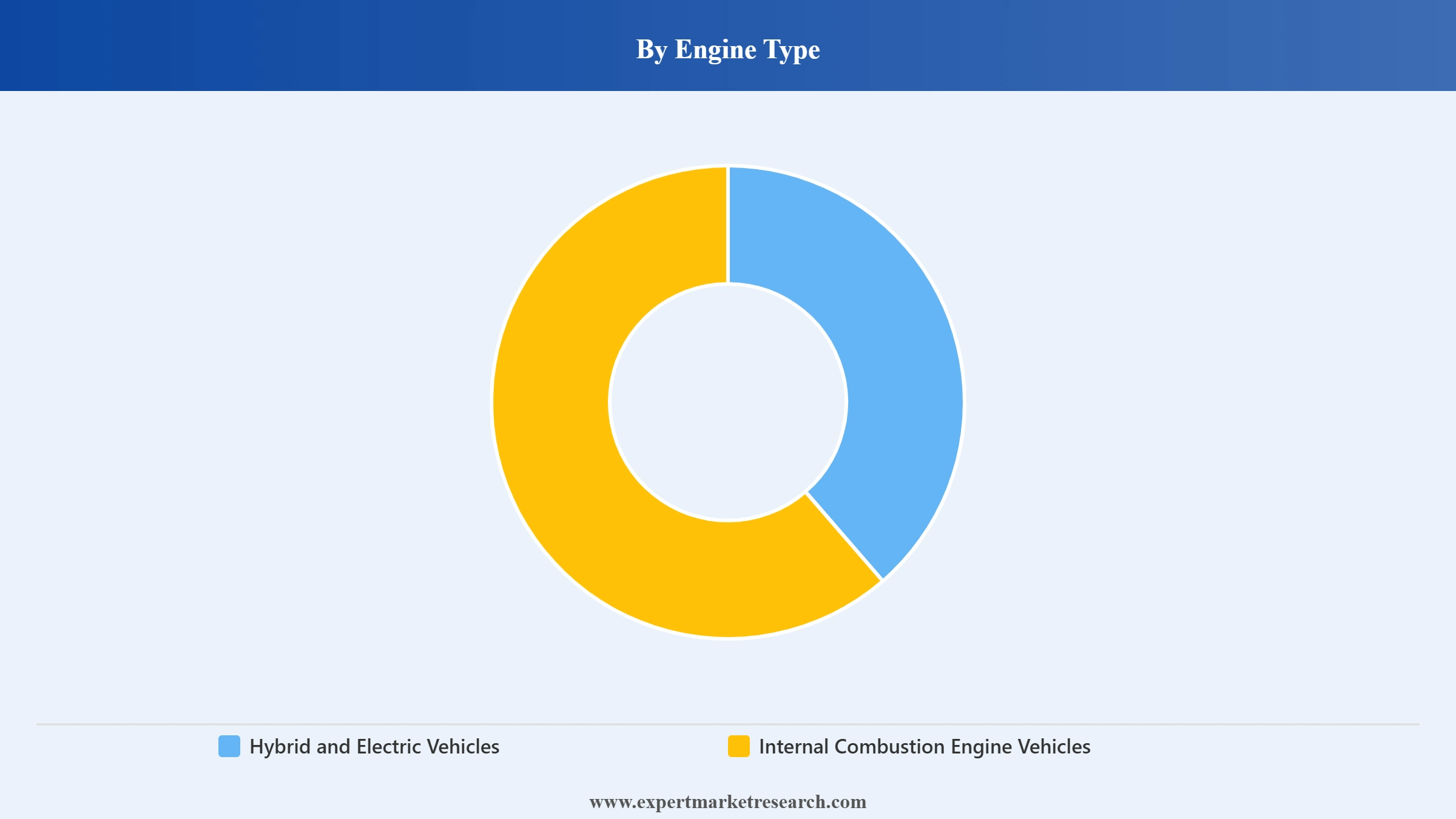

CAGR 2026-2035 - Market by Engine Type |

Hybrid and Electric Vehicles |

7.2% |

|

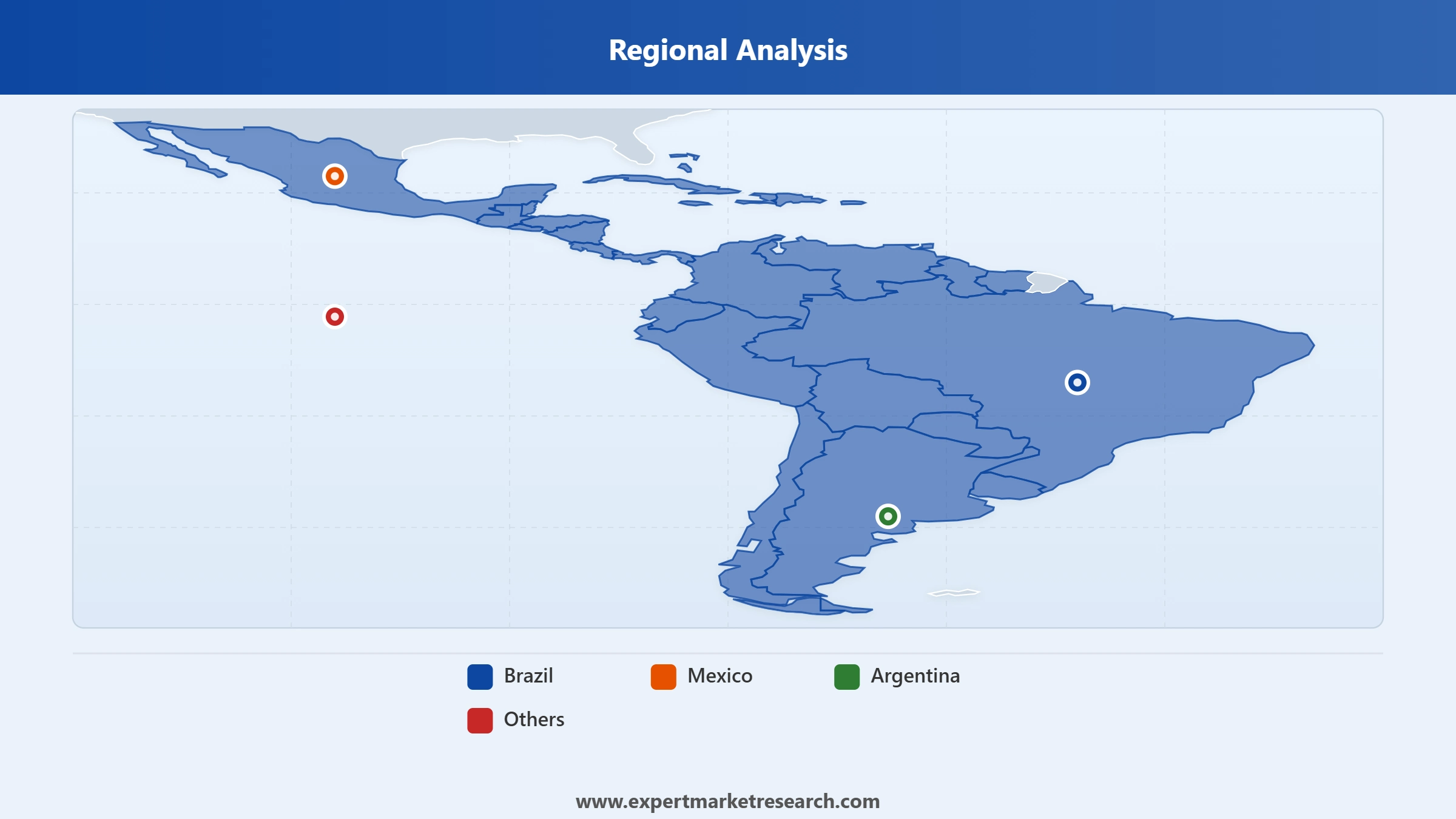

Market Share by Country 2025 |

Brazil |

36.6% |

The key trends in the Latin America automotive market include demand for hybrid vehicles, regional sourcing of auto components, production, and digitalization.

In August 2025, General Motors and Hyundai Motor Company revealed plans to jointly develop five new vehicle models specifically targeting the Central and South American market, with a combined production target of 800,000 annual units by 2028. The collaboration represents a significant shared-cost development strategy designed to accelerate product cadence while reducing the per-model investment risk for both companies. The models are planned to leverage localised platforms that comply with Mercosur tariff preferences and regional regulatory norms, reflecting the broader industry trend toward region-specific vehicle architectures in Latin America's growing but cost-sensitive market.

In July 2025, BYD formally commenced passenger car production at its newly established manufacturing facility in Bahia state, Brazil, following a total investment of approximately BRL 5.5 billion (approximately USD 1 billion). The plant marks BYD's transition from an importer to a domestic producer in Latin America's largest automotive market, which is a move that positions the company to benefit from local content incentives and avoid import tariffs. The launch builds on BYD's dominant position in the region's EV segment, where the brand holds approximately 70% market share, and signals the company's long-term commitment to manufacturing in Brazil as a hub for regional supply.

In April 2025, Volkswagen AG allocated approximately USD 580 million toward the development of the next-generation Amarok pickup truck at its Pacheco facility in Argentina. The investment underscores Volkswagen's continued commitment to local manufacturing in Argentina despite the country's challenging macroeconomic environment, and reflects the strategic importance of the pickup truck segment in the Latin American commercial vehicle landscape. The Amarok has historically been one of Volkswagen's best-selling models in the region, and the Pacheco facility investment ensures ongoing domestic production with the potential for regional export to other Latin American markets.

In January 2025, the Mexican government announced the launch of Olinia, the nation's first domestically founded electric vehicle manufacturer. Olinia was established with the strategic objective of producing affordable electric mini-vehicles designed specifically to address the urban mobility challenges of Mexican cities, combining sustainable transportation with practical suitability for congested urban environments. The launch reflects Mexico's ambition to develop its own electric mobility ecosystem alongside its established role as a major global vehicle exporter, and adds a new domestic player to a sector previously dominated entirely by international automotive brands and their local assembly operations.

In March 2024, Stellantis announced its largest-ever investment plan for Brazil and the South American region, committing EUR 5.6 billion (approximately BRL 30 billion) over the period from 2025 to 2030. The plan, described as the single biggest investment in the history of the Brazilian and South American automotive industry, targets the development and launch of close to 40 new vehicle offerings and focuses specifically on decarbonising the company's regional mobility portfolio. The investment encompasses production facility upgrades, new electric and hybrid model introductions, and supply chain localisation, reinforcing Brazil's position as the central hub for Stellantis's Latin American manufacturing and product strategy.

Latin America is experiencing a notable shift in consumer powertrain preferences, with hybrid vehicles and locally adapted flex-fuel models capturing increasing attention across Brazil, Colombia, and Chile. Government tax incentives and tightening emissions regulations are lowering the cost premium for hybrid models, bringing them within reach of middle-class buyers who have historically favoured affordable ICE vehicles. Toyota's Corolla Hybrid has gained meaningful market share in Brazil and Colombia as a result. The hybrid and electric vehicle segment is forecast to grow at a CAGR of 7.2% over the forecast period per Expert Market Research, significantly outpacing the overall market. The Latin America automotive market growth in the electric and hybrid segment is further supported by Brazil's E30 flex-fuel mandate and Chile's EV incentive programme.

Chinese automotive brands, led by BYD but also including Dongfeng, JAC, and Great Wall, are fundamentally reshaping the competitive dynamics of the Latin American automotive market. Chinese OEMs compete aggressively on feature richness and price, offering technology-laden models at price points that pressure established Japanese, European, and American brands to revise their product and pricing strategies. BYD retains approximately 70% of the region's nascent EV market and began passenger car production in Brazil in July 2025, transitioning from importer to local manufacturer. In December 2024, Dongfeng formally entered the Mexican car market with over ten models. This competitive shift is accelerating EV penetration, intensifying price competition across all segments, and forcing incumbent automakers to accelerate their localisation strategies.

Global automakers are increasingly prioritising localised vehicle production in Latin America as a strategic response to rising import tariffs, currency volatility, and the Mercosur framework's preference for regionally manufactured content. Brazil and Mexico have emerged as the primary manufacturing hubs, with companies like Volkswagen, Ford, Toyota, and Stellantis operating significant assembly plants that produce models specifically adapted for local consumer preferences and regulatory conditions. In 2024, Stellantis committed EUR 5.6 billion to South American operations through 2030, focused on decarbonising its regional portfolio and introducing nearly 40 new offerings. Volkswagen's USD 580 million investment in the Pacheco facility in Argentina and BYD's Bahia plant operationalisation both reflect the same strategic logic.

Ride-hailing services operated by Uber, DiDi, and Cabify are experiencing strong growth across Mexico, Brazil, and Argentina, creating a structurally different category of fleet vehicle demand within the Latin America automotive market. Commercial fleet operators and ride-hailing platforms typically prioritise durability, fuel efficiency, and low maintenance costs over consumer-oriented premium features, which is reshaping the product specifications that automakers need to offer for fleet contracts. Vehicle subscription models are also gaining traction in Brazil, where over 30 companies now compete in the space. These services are expected to spread across the region as awareness increases and prices become more accessible, creating an additional non-traditional sales channel for automakers alongside the conventional dealership model.

The Expert Market Research's report titled “Latin America Automotive Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Vehicle Type

Market Breakup by Engine Type

Market Breakup by Propulsion Type

Market Breakup by Class

Market Breakup by Country

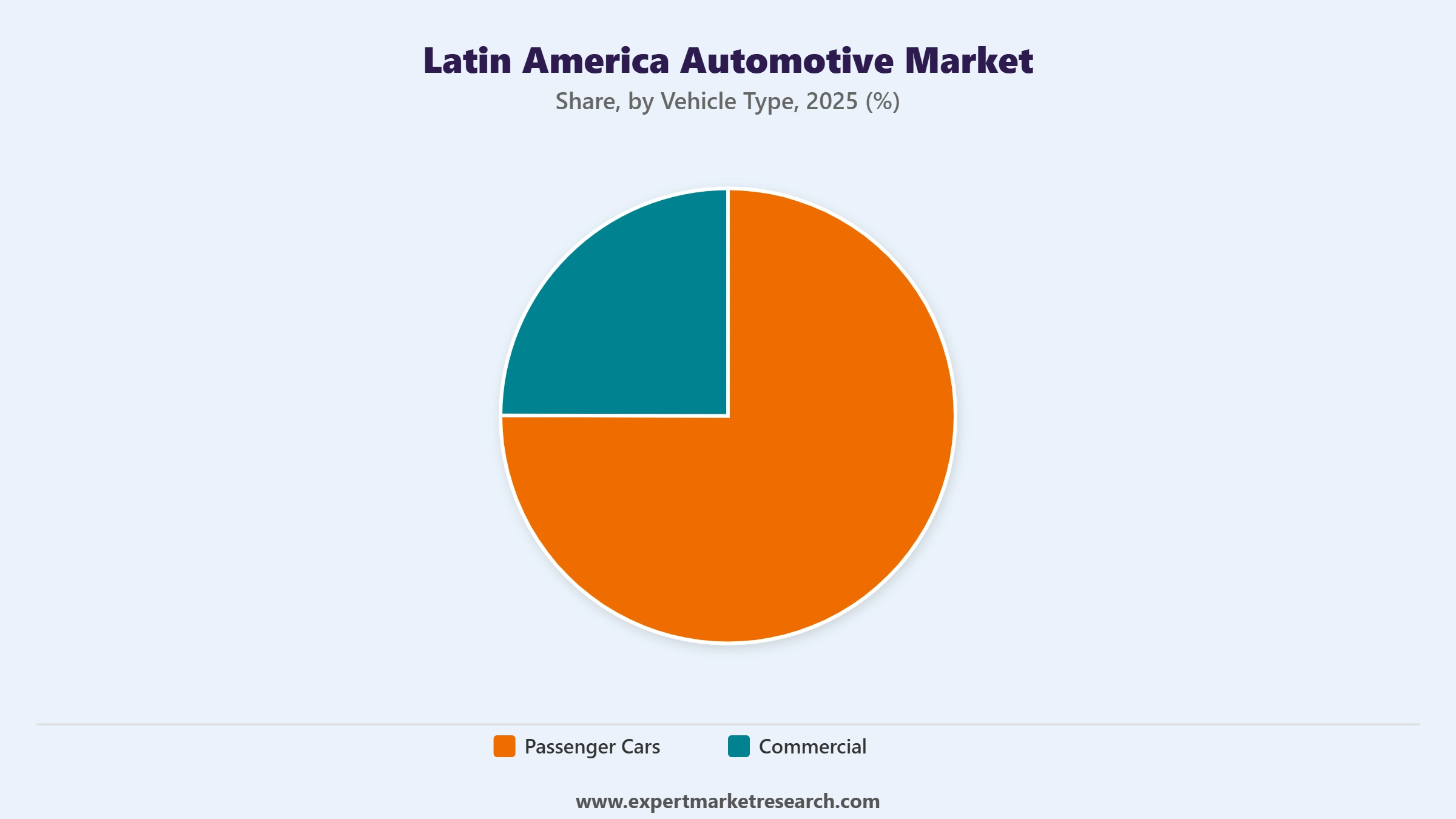

By Vehicle Type: Passenger cars hold the leading market share in the Latin America automotive market by vehicle type, driven by the growing aspirations of the middle-class consumer base across Brazil, Mexico, and Colombia. The SUV sub-segment has been the most dynamic within passenger cars, with Chinese OEMs introducing sub-compact crossovers at prices competitive with traditional hatchbacks, which has shifted buyer preference toward taller vehicles with perceived safety advantages and higher ground clearance. Hatchbacks and sedans retain relevance in urban markets where compactness and fuel efficiency are priorities. In the commercial vehicle category, light commercial vehicles hold the largest share, sustained by the expansion of last-mile delivery infrastructure driven by e-commerce growth across Brazil and Mexico. Heavy trucks and buses serve the mining, agriculture, and intercity transport sectors, maintaining steady demand as infrastructure investment in the region continues.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Engine Type: Internal combustion engine vehicles hold the dominant share of the Latin America automotive market by engine type, accounting for the vast majority of total units sold across the region. Brazil's flex-fuel vehicle platform, where sugarcane ethanol is blended with petrol, is a key structural driver of ICE vehicle persistence in the region's largest market. However, the Hybrid and Electric Vehicle segment is the fastest-growing engine type, expanding at a CAGR of 7.2% over the forecast period as government incentives, Chinese EV market entry, and rising environmental awareness shift consumer and regulatory preferences. Chile has been the regional leader in EV adoption relative to market size, recording over 90% growth in EV sales in 2023, driven by national electrification strategies and favourable import policies. Colombia and Costa Rica are also expanding their EV passenger vehicle sales shares, reflecting a broader regional momentum toward electrification.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Brazil is the largest and most strategically important market in the Latin America automotive sector, accounting for approximately 36.6% of regional vehicle sales volume in 2024. The country's automotive ecosystem is distinctive globally for its flex-fuel vehicle platform, where ethanol blends power vehicles alongside conventional petrol, giving consumers a hedge against fuel price volatility. Brazil's main OEM production hubs in Sao Paulo state host assembly facilities operated by Volkswagen, Stellantis, Toyota, Ford, and General Motors, collectively making Brazil one of the top vehicle-producing nations in the world. Stellantis's commitment of EUR 5.6 billion over 2025-2030 and BYD's Bahia plant operationalisation in July 2025 demonstrate sustained investment confidence in Brazil's long-term growth potential. Brazil's economy expanded 3.4% in 2024 with an unemployment rate of 6.5%, creating supportive conditions for vehicle purchases, though elevated borrowing rates are adding pressure on affordability.

Mexico is the second-largest market and is projected to grow at the fastest pace of all major country markets, with a CAGR of 5.5% over the forecast period per Expert Market Research. Mexico's automotive importance extends well beyond domestic consumption: the country is one of the world's top ten vehicle producers, manufacturing over 3.3 million units in 2023, more than 80% of which are exported to the United States and Canada under the USMCA framework. Mexico's deep integration into North American supply chains gives it a structural advantage as nearshoring trends accelerate, with more global manufacturers establishing or expanding production in the country. Domestically, the launch of Olinia in January 2025, Mexico's first indigenous EV manufacturer, signals the country's ambition to build a national EV brand alongside its role as a global export manufacturing hub. Chinese automakers, including Dongfeng's December 2024 market entry with over ten models, are intensifying competition in the local market and accelerating product diversification.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Latin America automotive market is home to a well-established competitive landscape dominated by global Japanese, European, and American automakers with decades of local manufacturing presence, which are now facing increasing competitive pressure from Chinese OEMs that are entering with cost-effective, feature-rich models. The market structure is moderately consolidated at the top, with Toyota, Volkswagen, General Motors, and Stellantis commanding the largest combined shares, but is fragmenting as Chinese brands and new domestic players build market presence.

Competitive priorities centre on localised production, product portfolio adaptation to regional consumer preferences, expansion of hybrid and EV offerings in response to government incentives and emissions regulations, and pricing strategies that address the cost sensitivity of Latin America's predominantly economy-segment buyer base. Alliance formation and joint development agreements, such as the GM-Hyundai collaboration announced in August 2025, are emerging as a response to the cost pressure of maintaining competitive product cadences in a region with multiple distinct national markets.

Founded in 1937 and headquartered in Toyota City, Aichi, Japan, Toyota Motor Corporation is one of the most entrenched and consistently high-performing automotive brands in Latin America. Toyota maintains significant production, distribution, and service operations across Brazil and Mexico, with the Corolla Hybrid gaining strong market share in Brazil and Colombia as hybrid adoption accelerates. The company's strategy in Latin America emphasises a combination of locally relevant models, sustainability initiatives, and supply chain partnerships that align with regional government incentive programmes. Toyota's hybrid-flex SUV initiative, which blends its hybrid technology with Brazil's existing ethanol infrastructure, represents a regionally tailored innovation not replicated in other global markets.

Founded in 1937 and headquartered in Wolfsburg, Germany, Volkswagen AG is among the most dominant automotive brands in Latin America, particularly in Brazil and Argentina, where its legacy of local manufacturing and brand recognition spans multiple generations of consumers. Volkswagen operates major assembly plants in Brazil and Argentina, producing models specifically adapted to local tastes and regulatory requirements. The company's April 2025 USD 580 million investment in the Pacheco, Argentina facility for the next-generation Amarok pickup illustrates its ongoing commitment to the region. Volkswagen is also navigating the competitive pressure from Chinese OEMs by expanding its own electric and hybrid offerings, maintaining its product portfolio's relevance across both economy and premium segments.

Founded in 1908 and headquartered in Detroit, Michigan, General Motors operates across Latin America primarily through its Chevrolet brand, which has historically been one of the most recognised automotive names in the region. GM maintains manufacturing operations in Brazil, where it produces compact and mid-size models tailored to local consumer preferences. In August 2025, General Motors announced a joint development agreement with Hyundai to co-develop five vehicle models targeting Central and South America, targeting 800,000 annual units by 2028, reflecting a strategy of cost-sharing and product acceleration in response to competitive pressures. The company is actively expanding its hybrid and electric vehicle offerings in Latin America to comply with tightening emissions standards and capitalise on growing consumer interest in electrified powertrains.

Founded in 1967 and headquartered in Seoul, South Korea, Hyundai Motor Company has established a growing and competitive presence in Latin America across multiple vehicle categories, from compact passenger cars to SUVs and commercial vehicles. Hyundai competes strongly in the economy and mid-segment passenger car categories and has been expanding its hybrid and electric vehicle lineup in the region in line with its global electrification strategy. The company's August 2025 co-development agreement with General Motors to produce five models for Central and South America marks a significant strategic move, creating a collaborative platform that is expected to enhance product competitiveness and reduce per-unit development costs for both brands in the region's evolving market.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Latin America's automotive sector is on a trajectory of sustained growth, but navigating it successfully requires a clear-eyed understanding of country-level dynamics, competitive intensity, and the accelerating shift toward electrification. Our comprehensive 2026 market report puts the data, the trends, and the strategic perspective at your fingertips. Whether you are an OEM, a supplier, a distributor, or an investor evaluating the region, this report is your guide to acting with clarity. Download your free sample today and take the first step toward understanding Latin America's fast-moving automotive landscape.

Upto 15% Off

USD

$5499 $4949

$3499 $3149

$6999 $5949

$8324 $7075

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Latin America automotive market reached an approximate volume of 6.18 Million Units.

The market is projected to grow at a CAGR of 4.80% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a volume of around 9.88 Million Units by 2035.

The major drivers of the market are rapid urbanization, internal and external trade agreements, and industrial growth across construction, mining, and agricultural sectors.

The key trends of the market include demand for hybrid vehicles, regional sourcing of auto components, production, and digitalization.

The major countries in the market are Brazil, Mexico, Argentina, and others.

The various engine types considered in the market report are hybrid and electric vehicles, and internal combustion engine vehicles.

The various propulsion types considered in the market report are BEV, HEV and PHEV, CNG, diesel, and gasoline.

The classes considered in the market report are economy and luxury.

The major players in the market are Toyota Motor Corp., Volkswagen AG, Nissan Motor Co. Ltd., Hyundai Motor Company, Kia Corporation, Suzuki Motor Corp., General Motors Company (Chevrolet), Honda Motor Co. Ltd., BMW AG, Ford Motor Company, AB Volvo, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Vehicle Type |

|

| Breakup by Engine Type |

|

| Breakup by Propulsion Type |

|

| Breakup by Class |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Datasheet

One User

USD 3,499

USD 3,149

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,324

USD 7,075

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.