Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

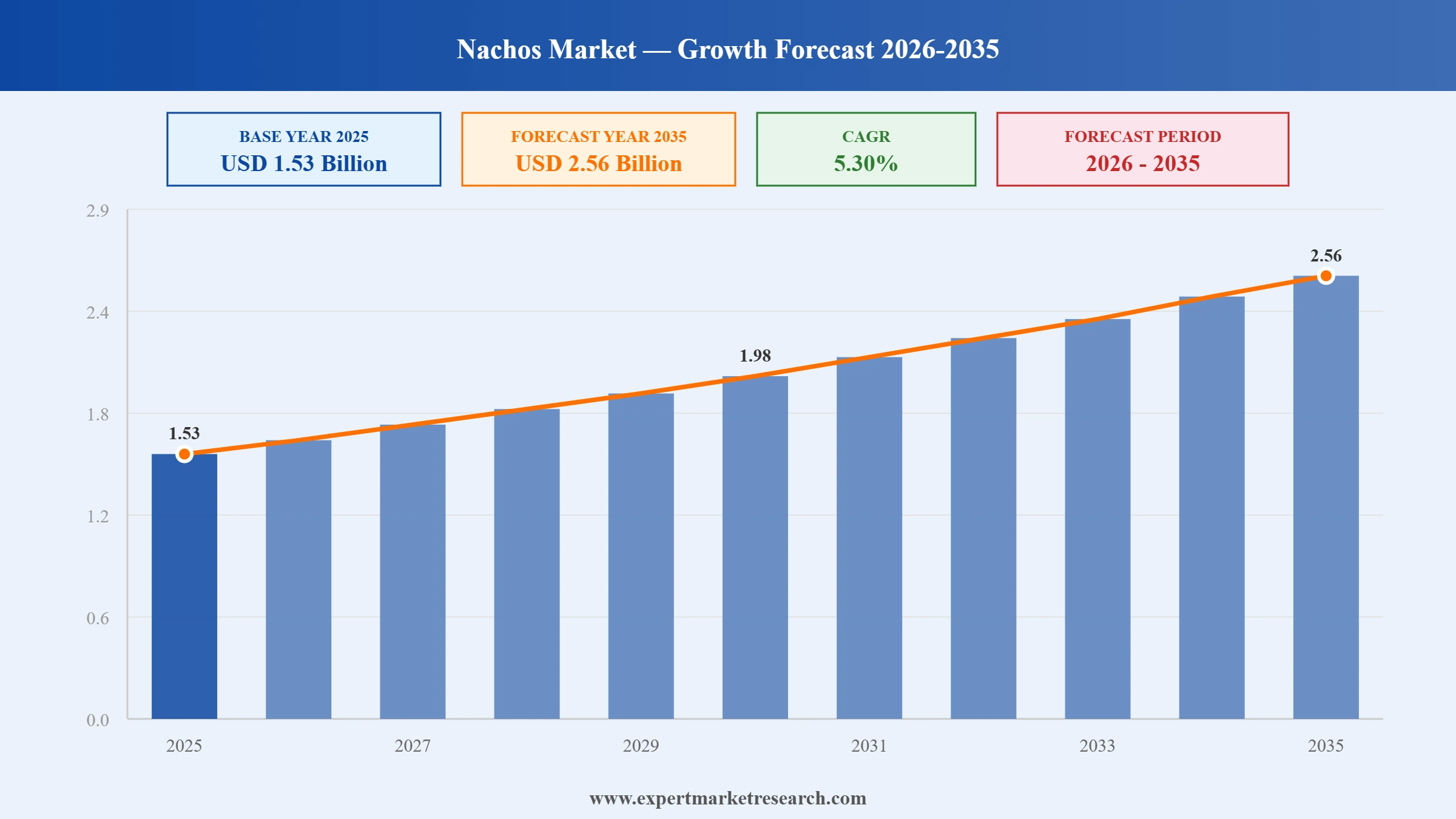

The Nachos Market reached a value of USD 1.53 Billion at 2025 and is projected to expand at a CAGR of around 5.30% during the forecast period of 2026-2035. With the rising global popularity of Mexican-style snacking culture, growing consumer appetite for bold flavours and convenient ready-to-eat options, accelerating online snack retail, and an expanding foodservice footprint across emerging markets, the market is expected to reach USD 2.56 Billion by 2035.

According to Yahoo Lifestyle, MASA's beef tallow tortilla chips are gaining traction among US consumers seeking premium, whole-ingredient snacking options for nachos and dipping. The Hatch Chile and Cobanero varieties are leading viral demand. This premiumization trend is pushing legacy tortilla chip brands to reformulate with traditional fats and clean-label ingredients, reshaping nacho purchasing behavior across grocery and specialty retail channels.

As reported by NACS, PepsiCo rolled out Doritos Protein tortilla chips in early March, offering 10 grams of protein per serving in Nacho Cheese and Cool Ranch flavors. The launch marks a major entry into the functional snack category, expanding the nachos base. The move is expected to widen the addressable market and pressure competitors to innovate across protein-enhanced tortilla chip formats.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Nachos Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 1.53 |

| Market Size 2035 | USD Billion | 2.56 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.30% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.9% |

| CAGR 2026-2035 - Market by Country | India | 6.0% |

| CAGR 2026-2035 - Market by Country | China | 5.7% |

| CAGR 2026-2035 - Market by Type | Baked | 5.8% |

| CAGR 2026-2035 - Market by Distribution Channel | Online Channels | 9.6% |

| Market Share by Country 2025 | Italy | 2.4% |

Growing demand for innovative snacks; the rising appeal of meat flavours; the surging popularity of Mexican snacks; and the increasing use of AI are the major factors favouring the nachos market growth.

In March 2026, PepsiCo launched Doritos Protein, a high-protein version of its iconic tortilla-style chips, extending one of the world's most recognised nacho chip brands into the rapidly growing better-for-you snacking category. Each one-ounce serving of Doritos Protein delivers 10 grams of protein, with a single-serve bag providing 17 grams. The launch directly targets health-conscious consumers who want the bold flavour and snack experience associated with Doritos but with added nutritional functionality. PepsiCo also announced a parallel collaboration with Jack Link's, rolling out Doritos-branded jerky and meat stick products in the United States. The move reflects a broader strategic push by PepsiCo to capture the growing functional snacking segment without abandoning the flavour-forward positioning that made Doritos a market leader.

At the National Association of Convenience Stores Expo in November 2025, Frito-Lay, a division of PepsiCo, unveiled the Jack Link's x Doritos Nacho Cheese collaboration, introducing the classic nacho cheese flavour into both a jerky format and meat sticks product. The product fusion bridges the tortilla snack and protein snack categories, targeting consumers who seek on-the-go high-protein options with the familiar bold flavour profile of Doritos Nacho Cheese. Frito-Lay also announced at the same event the permanent addition of Doritos Blazin' Buffalo and Ranch chips to its lineup, reflecting the company's strategy of converting fan-favourite limited-edition products into core range items based on sustained consumer demand and strong repeat purchase performance.

In 2025, Beanitos launched a subscription-box service offering limited-edition nacho kits, achieving an online repeat purchase rate of approximately 18% within the first quarter of launch. The initiative reflects two converging trends in the nachos market: the rapid growth of the online channel as a preferred shopping route for snack products, and the rising consumer interest in curated, premium snacking experiences that go beyond off-the-shelf tortilla chip bags. Subscription-based models are particularly suited to the nachos category because of the natural pairing potential between chips, dips, and specialty toppings. Beanitos' success in the early months of the programme underscores the revenue potential of direct-to-consumer models for nacho brands willing to invest in digital commerce and community-building strategies.

In the first half of 2024, Tia Lupita, a sustainable tortilla chip and nacho brand, joined PepsiCo's Greenhouse Accelerator Programme, which connects emerging sustainable food brands with Frito-Lay's operational expertise and distribution infrastructure. Through the programme, Tia Lupita worked on revamping its chip portfolio, retaining its best-performing Sea Salt and Salsa Verde varieties with improved formulations while launching a new Sea Salt and Lime flavour made with real lime juice. The company also focused on expanding its distribution into additional retail channels. The development illustrates how major snack conglomerates are actively supporting better-for-you and sustainability-focused brands within the tortilla chip and nachos space as consumer appetite for cleaner alternatives grows.

In 2024, Late July Snacks expanded its tortilla chip and nachos portfolio with the launch of Hawaiian Habanero, a bold new flavour combining sweet pineapple with habanero heat. The product exemplifies the broader flavour innovation trend shaping the nachos and tortilla chip category, where manufacturers are increasingly experimenting with unexpected flavour combinations to capture consumer interest and drive repeat purchases beyond traditional cheese and salsa profiles. Late July, known for its organic and non-GMO product positioning, targeted health-conscious snack consumers who also seek adventurous flavour experiences. The launch reflects how the better-for-you segment within nachos is no longer just about reducing calories or fat but is equally focused on delivering a premium, exciting taste experience.

Flavour innovation is the single most powerful growth driver in the global nachos market today. Consumer interest in bold, unexpected, and globally inspired flavour combinations is at an all-time high, with manufacturers racing to introduce limited-edition and permanent range extensions that generate excitement and reward repeat shoppers. Spicy, smoky, tangy, and fusion flavours are particularly popular, attracting younger demographics who consume nachos as part of a broader adventurous snacking lifestyle. In 2024, tortilla chip manufacturers including Late July Snacks launched flavours such as Hawaiian Habanero, which combined sweet pineapple with habanero heat, and PepsiCo's Tia Lupita brand introduced improved Sea Salt and real lime juice-infused variants. Both launches were cited by industry analysts as examples of how nachos market growth is increasingly driven by flavour-led product differentiation.

Health-conscious snacking is fundamentally altering product development strategies in the nachos market. Baked formulations, organic ingredients, protein-enhanced variants, gluten-free options, and reduced-sodium profiles are moving from niche positioning to mainstream shelf presence. Consumers no longer accept that indulgence and nutrition are mutually exclusive, particularly in snacking. In March 2026, PepsiCo launched Doritos Protein, a product that delivers 10 grams of protein per serving in the familiar tortilla chip format. The launch is a direct response to growing demand from health-active consumers who want snack foods that contribute to their nutritional goals, signalling that the era of purely indulgence-led nachos marketing is giving way to a more functionality-focused product narrative in the category.

The HoReCa channel (hotels, restaurants, and cafes) plays a central role in driving nachos consumption globally, particularly in North America where nachos are a standard menu item at sports bars, movie theatres, casual dining chains, and quick-service restaurants. The category's suitability for sharing occasions and its compatibility with diverse toppings and dip formats make it a natural fit for on-premise foodservice. Brands are leveraging foodservice as a brand-building channel, introducing signature nacho formats that drive brand awareness and encourage off-premise retail purchases. In November 2025, Frito-Lay's collaboration with Jack Link's to launch Doritos-flavoured jerky and meat sticks at the NACS Expo illustrated how snack brands are extending their nacho-adjacent flavour identities across multiple foodservice-compatible formats to reinforce consumer engagement across purchase occasions.

The online distribution channel for nachos is growing at a CAGR of 9.6% over the forecast period, significantly outpacing all other channels. E-commerce platforms are reshaping how consumers discover, sample, and repurchase nachos and related snack products, with digital-first brands and subscription box services generating high levels of customer loyalty and repeat purchase rates. Online channels also allow niche and premium brands to compete effectively against established mass-market players without the capital-intensive shelf placement requirements of traditional retail. In 2025, Beanitos launched a subscription-based nacho kit service that achieved an 18% repeat purchase rate within its first quarter, demonstrating the commercial viability of direct-to-consumer models in the nachos segment and the growing preference of a key consumer demographic for curated home snacking experiences.

The EMR’s report titled “Global Nachos Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

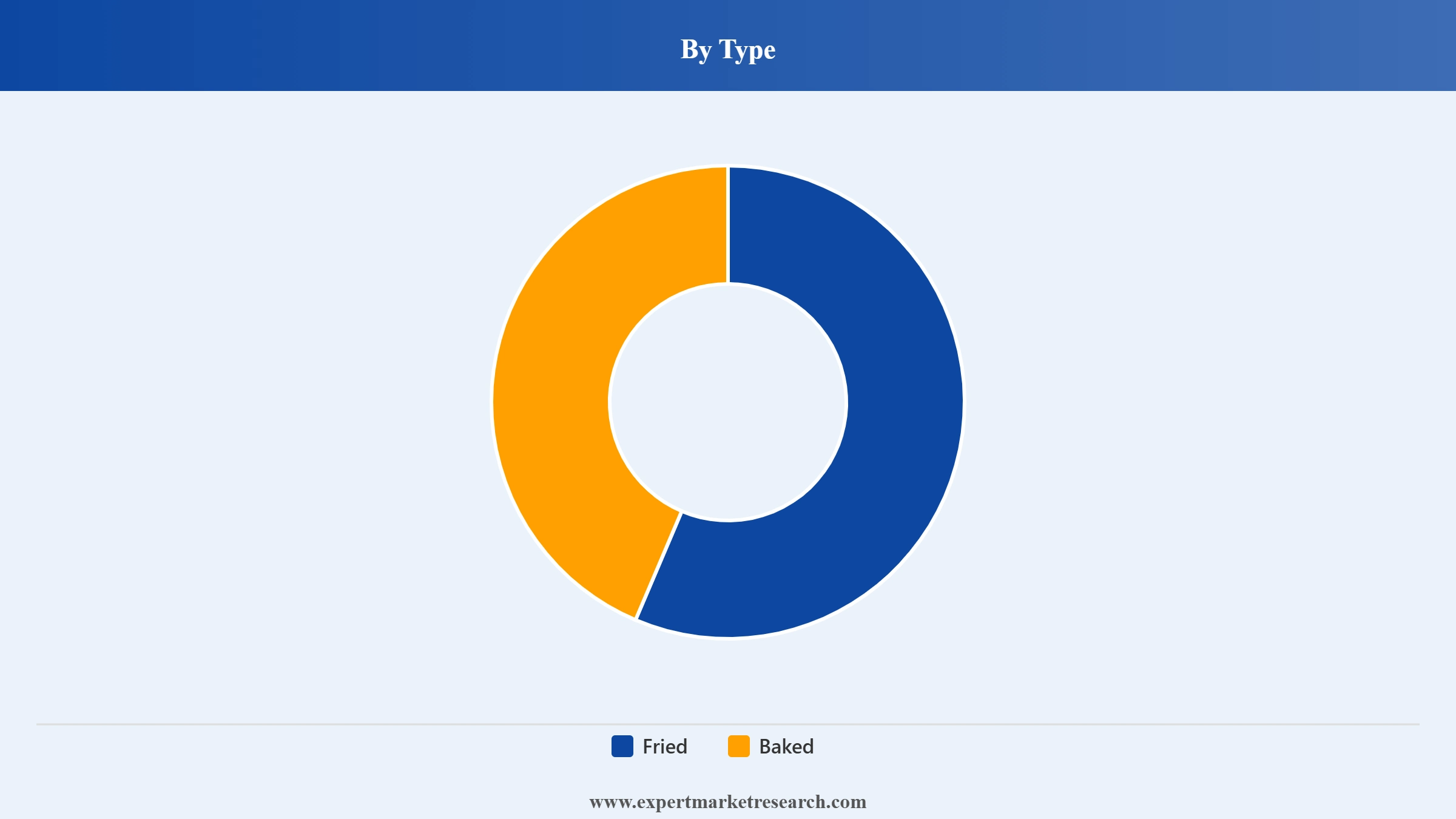

Breakup by Type

Key Insight: Baked nachos hold the dominant share within the Type segmentation, accounting for the majority of global market revenue as health-conscious consumer trends shift purchasing behaviour away from traditional fried formats. Baked formulations offer a lower fat and calorie profile while preserving the crunchy texture and bold flavour experience that define the nachos eating occasion, making them appealing to both long-standing nachos consumers and newer health-aware entrants to the category. Fried nachos retain a significant consumer base, particularly within the foodservice and restaurant channel, where the traditional fried nacho experience remains synonymous with the authentic Mexican-style snack occasion. The Others category includes premium and artisanal nacho formats, including grain-free, gluten-free, and vegetable-based tortilla chip variants that are growing in niche health and specialty retail channels.

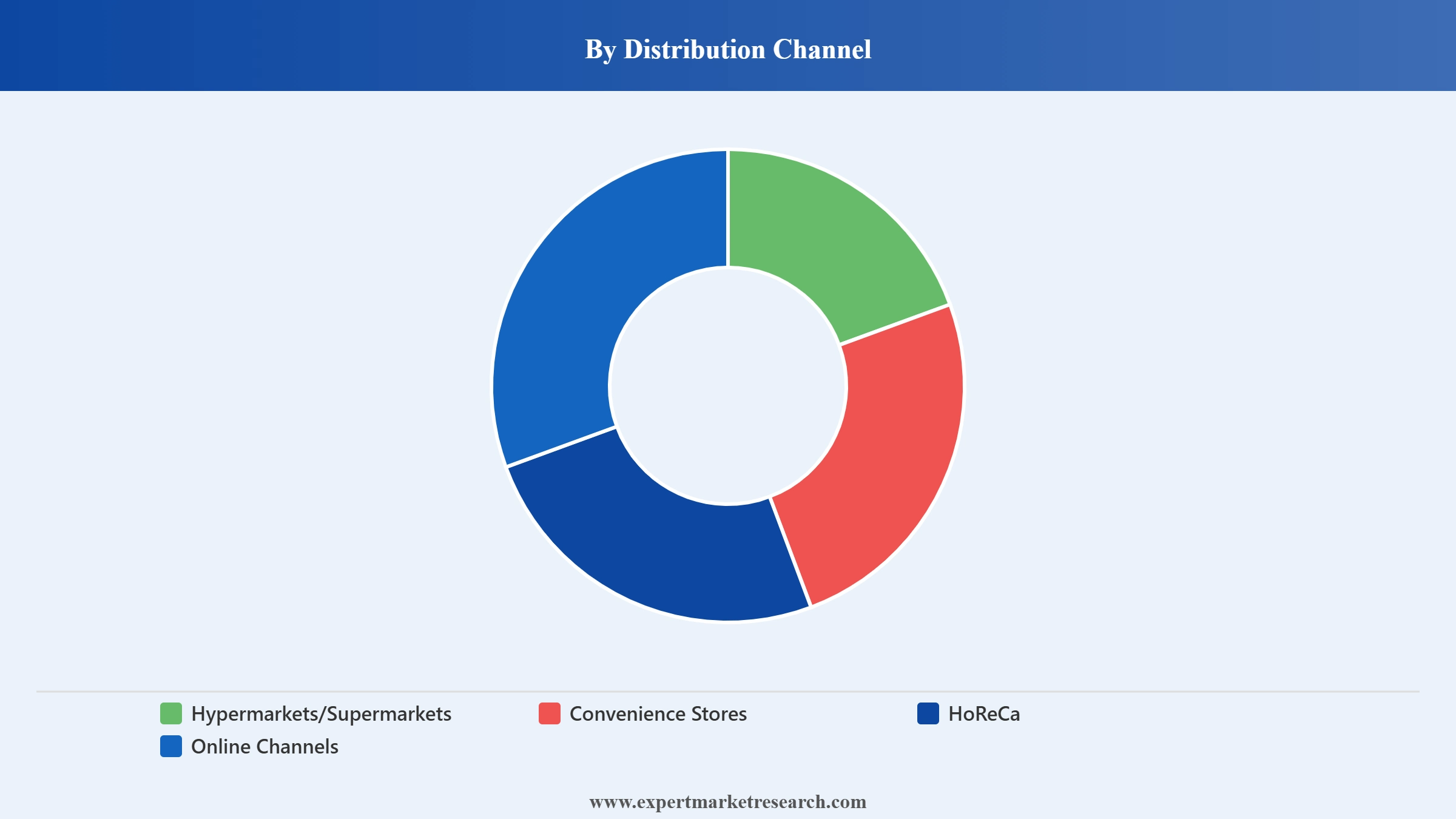

Breakup by Distribution Channel

Key Insight: Hypermarkets and Supermarkets are the dominant distribution channel for nachos globally, accounting for the largest share of retail sales due to their high footfall, broad product range, and promotional shelf-space advantages that established nachos brands leverage effectively. Online Channels are the fastest-growing route to market at a CAGR of 9.6%, fuelled by e-commerce platform expansion, subscription snack delivery services, and the growing preference of digitally active consumers for home snacking discovery and direct-to-consumer brand relationships. HoReCa is a strategically important channel, driving both volume consumption at social and entertainment occasions and acting as a key brand visibility platform for leading nachos producers. Convenience stores serve time-pressed urban consumers seeking immediate snack options, reinforcing the on-the-go consumption positioning that is central to nachos' broader category appeal.

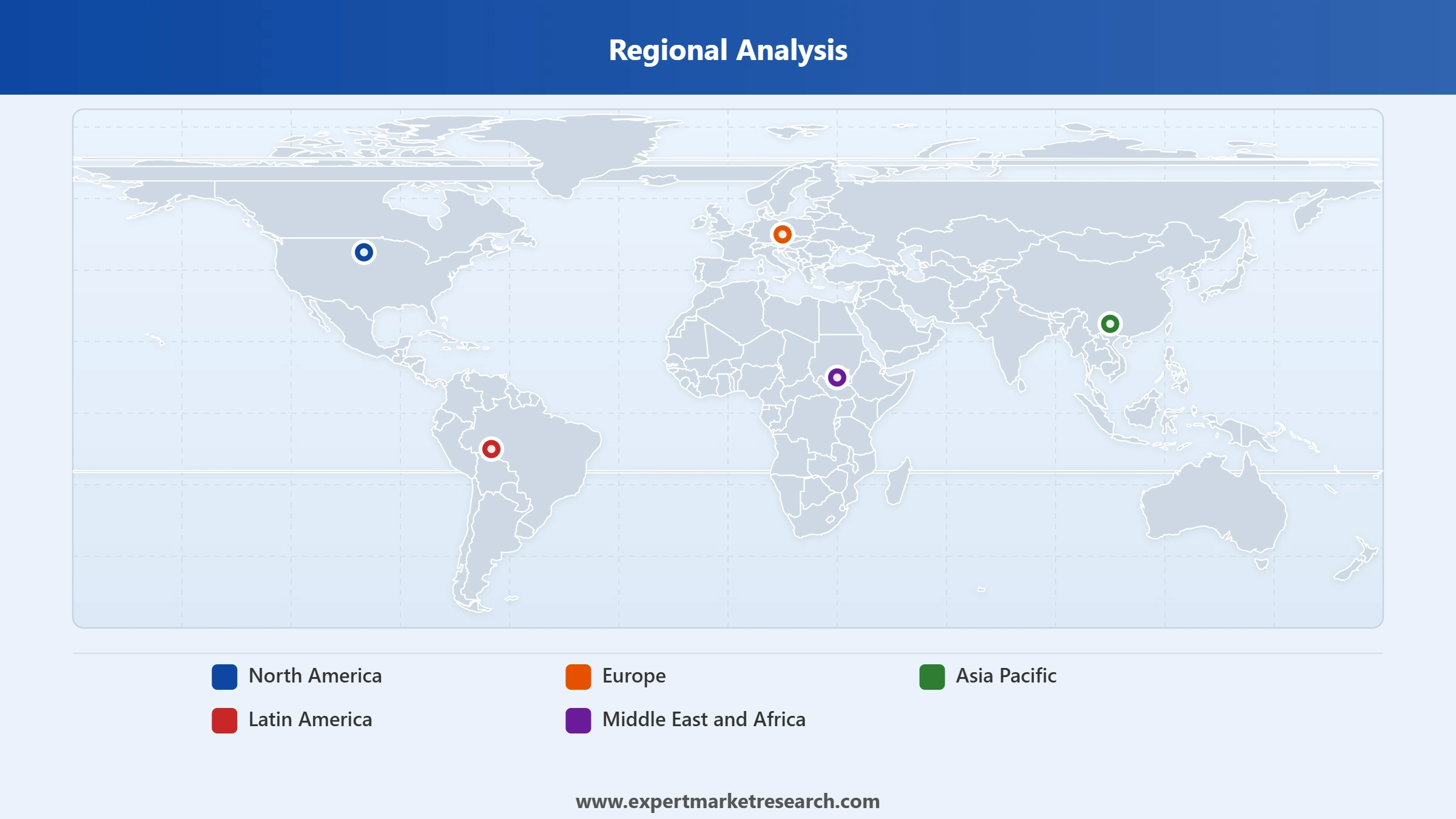

Breakup by Region

Key Insight: North America is the largest and most mature nachos market globally, commanding the dominant share of total market revenue. The region's deep-rooted Tex-Mex culinary culture, established quick-service restaurant ecosystem, and high per-capita snack consumption sustain strong baseline demand. Asia Pacific is the fastest-growing region at a CAGR of 5.9%, with rapid urbanisation, rising disposable incomes, and growing exposure to Western snack formats driving nachos adoption in China, India, Japan, and ASEAN markets. Latin America is growing at a CAGR of 5.7%, benefiting from the category's authentic Mexican cultural roots which resonate strongly with local consumer tastes. Europe represents a moderate growth market, with the UK, Germany, and France showing strongest demand driven by the rising popularity of international cuisines and the expanding casual dining culture. Middle East and Africa present an emerging opportunity as young, urban-focused consumer bases in markets like Saudi Arabia, UAE, and South Africa grow increasingly receptive to Western snack formats.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Type segmentation, Baked nachos command the dominant share of the global nachos market, reflecting the accelerating structural shift toward health-conscious snacking choices that is reshaping product preferences in virtually every packaged food category. Consumers who snack regularly are increasingly factoring nutritional profiles into their purchase decisions, and baked nachos answer this need without asking consumers to sacrifice the crunchy texture and bold flavour experience that makes nachos a consistently satisfying snack occasion. The dominance of baked formats is particularly pronounced in North America and Europe, where health awareness is most developed, while fried formats retain stronger representation in HoReCa and foodservice settings across Latin America and Asia Pacific where the traditional nacho-eating experience remains prevalent. Major brands including Frito-Lay, Gruma, and General Mills have all responded to this demand by expanding their baked and better-for-you product lines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Distribution Channel segmentation, Hypermarkets and Supermarkets hold the largest revenue share of the global nachos market, driven by their unmatched consumer reach, competitive promotional mechanics, and the established in-store snack aisle positioning of the leading nachos brands. The impulse purchase dynamic in large-format grocery retail is particularly well-suited to nachos, which consumers frequently add to shopping baskets without pre-planning. Online Channels, while still a smaller share of total revenue, are growing at a CAGR of 9.6% and represent the most disruptive shift in nachos distribution. The online channel is particularly effective for premium, specialty, and better-for-you nacho brands that lack the shelf placement resources to compete with dominant brands in physical retail but can build direct consumer relationships through digital platforms, social media marketing, and subscription models. The HoReCa channel holds a structurally important position, particularly for the Fried nacho format, which is most commonly served in restaurants, bars, and entertainment venues.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the undisputed leader in the global nachos market, accounting for the largest regional revenue share and establishing the cultural and commercial template that other global markets are progressively following. The United States alone represents the most significant portion of North American demand, with nachos embedded in the national snacking culture as a fixture at sporting events, cinema concessions, casual dining restaurants, sports bars, and home entertainment occasions. The US market is characterised by intense competition among established brands such as Frito-Lay's Doritos and Tostitos, private-label tortilla chips, and a growing segment of premium and better-for-you brands including Late July Snacks, Beanitos, and Tia Lupita that are capturing demand from health-conscious consumers. Canada also contributes meaningfully to regional revenue, with a snacking culture closely aligned to the United States. Product innovation in North America is the primary global engine driving nachos market development, with new flavour launches, functional formulations, and collaborative products from this region frequently setting trends that eventually reach European and Asian markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing regional nachos market, expanding at a CAGR of 5.9% over the forecast period, supported by rapid urbanisation, rising household incomes, and growing exposure to Western food culture through social media, streaming content, and the expansion of international quick-service restaurant chains. China and India are the most significant growth contributors, with China's nascent but fast-developing affinity for salty snacks and India's deeply embedded tradition of bold-flavoured savoury snacking creating fertile ground for nachos adoption. Japan and South Korea, while more established markets, continue to grow through premiumisation and the introduction of globally inspired flavour profiles. ASEAN markets including Indonesia, Vietnam, Thailand, and the Philippines are emerging as high-potential frontiers for nachos distribution as urban middle-class populations expand and modern retail infrastructure including both brick-and-mortar supermarkets and e-commerce platforms extends its reach. International brands are actively investing in these markets through partnerships with regional distributors and entry into local foodservice chains.

The global nachos market is led by a concentrated group of multinational snack food companies with the brand equity, distribution scale, and product development resources to compete effectively across multiple geographies and retail formats. PepsiCo, through its Frito-Lay division, commands the most significant market position globally, with brands such as Doritos and Tostitos among the most widely recognised tortilla chip and nachos products in the world. Gruma Corporation, the world's largest tortilla manufacturer, holds a structurally important position through its Mission Foods and Guerrero brands, while General Mills and Utz Quality Foods maintain competitive presence in specific regional markets and consumer segments.

The competitive landscape is evolving as better-for-you and premium brands gain traction at the expense of traditional mass-market fried nacho formats. Smaller independent brands specialising in organic, gluten-free, grain-free, and protein-enhanced nachos are growing faster than the overall category, attracting investment from both private equity and strategic acquirers seeking exposure to health-driven snacking trends. The integration of digital commerce and subscription-based delivery models is further opening competitive space for niche brands that can build direct consumer relationships online, reducing their dependence on traditional retail shelf space.

Founded in 1965 and headquartered in Purchase, New York, PepsiCo is one of the world's largest food and beverage companies. Through its Frito-Lay division, PepsiCo commands the dominant global position in the tortilla chip and nachos market with brands including Doritos, Tostitos, and Lay's. Operating across more than 200 countries, PepsiCo combines unmatched distribution reach with continuous product innovation, as evidenced by the March 2026 launch of Doritos Protein and the Jack Link's collaboration. Its Greenhouse Accelerator programme also reflects a strategic commitment to incubating the next generation of snack brands.

Founded in 1949 and headquartered in Monterrey, Mexico, Gruma Corporation is the world's largest tortilla manufacturer and a foundational player in the global nachos supply chain. The company operates globally through its Mission Foods, Guerrero, Maseca, and GRUMA brands, producing tortillas, tortilla chips, and related corn-based products that serve both retail and foodservice markets. With manufacturing facilities across the Americas, Europe, Asia, and Oceania, Gruma provides the foundational ingredient base for the global nachos category and also competes directly in packaged tortilla chip retail segments across key markets.

Founded in 1856 and headquartered in Golden Valley, Minnesota, USA, General Mills is a diversified global food company with a relevant presence in the nachos and snack segment through its snack bar portfolio and corn-based product ranges. The company operates across more than 100 countries, leveraging a well-established manufacturing and distribution infrastructure to serve global retail and foodservice customers. General Mills has made ongoing investments in better-for-you snack formulations, aligning its product development pipeline with the health-conscious consumer trend that is reshaping the nachos and tortilla chip category across developed markets.

Founded in 1921 and headquartered in Hanover, Pennsylvania, USA, Utz Quality Foods is one of the leading independent snack manufacturers in the United States with a strong presence in the tortilla chip and nachos segment. The company's portfolio includes a range of tortilla chips and nacho-style snacks sold under the Utz, On the Border, and other brand names. Utz primarily serves the North American market, leveraging its regional manufacturing strength, deep retailer relationships, and well-established brand recognition among East Coast US consumers. The company has invested in expanding its distribution footprint and broadening its better-for-you snack offerings.

Other key players in the market are Campbell Soup Company, Xochitl Inc., The Hain Celestial Group Inc., Nature's Path Foods Inc., Greendot Health Foods Pvt., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The global nachos category is evolving rapidly, with health-conscious reformulations, bold flavour innovation, and digital commerce fundamentally reshaping how consumers discover, purchase, and engage with nachos brands worldwide. Our comprehensive Global Nachos Market report for 2026 provides the data-driven clarity you need to navigate this dynamic landscape. Whether you are a snack manufacturer seeking market entry intelligence, a retailer optimising your snack category mix, or an investor evaluating growth opportunities in the food and beverage sector, this report delivers the insights that matter. Download your free sample today and explore the key opportunities defining the future of nachos globally.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 1.53 Billion.

The market is projected to grow at a CAGR of 5.30% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 2.56 Billion by 2035.

The different regions considered in the market report include North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The major market trends are the rising appeal of meat flavours, the rising popularity of Mexican snacks, and the increasing use of AI.

The different types of nachos include baked and fried, among others.

The different distribution channels for nachos in the market are hypermarkets/supermarkets, convenience stores, HoReCa, and online channels, among others.

Key players in the market are PepsiCo Inc., Gruma Corporation, General Mills, Inc., Utz Quality Foods, LLC, Campbell Soup Company, Xochitl Inc., The Hain Celestial Group, Inc., Nature’s Path Foods, Inc., Greendot Health Foods Pvt. Ltd., and Haldiram Products Private Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.