Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

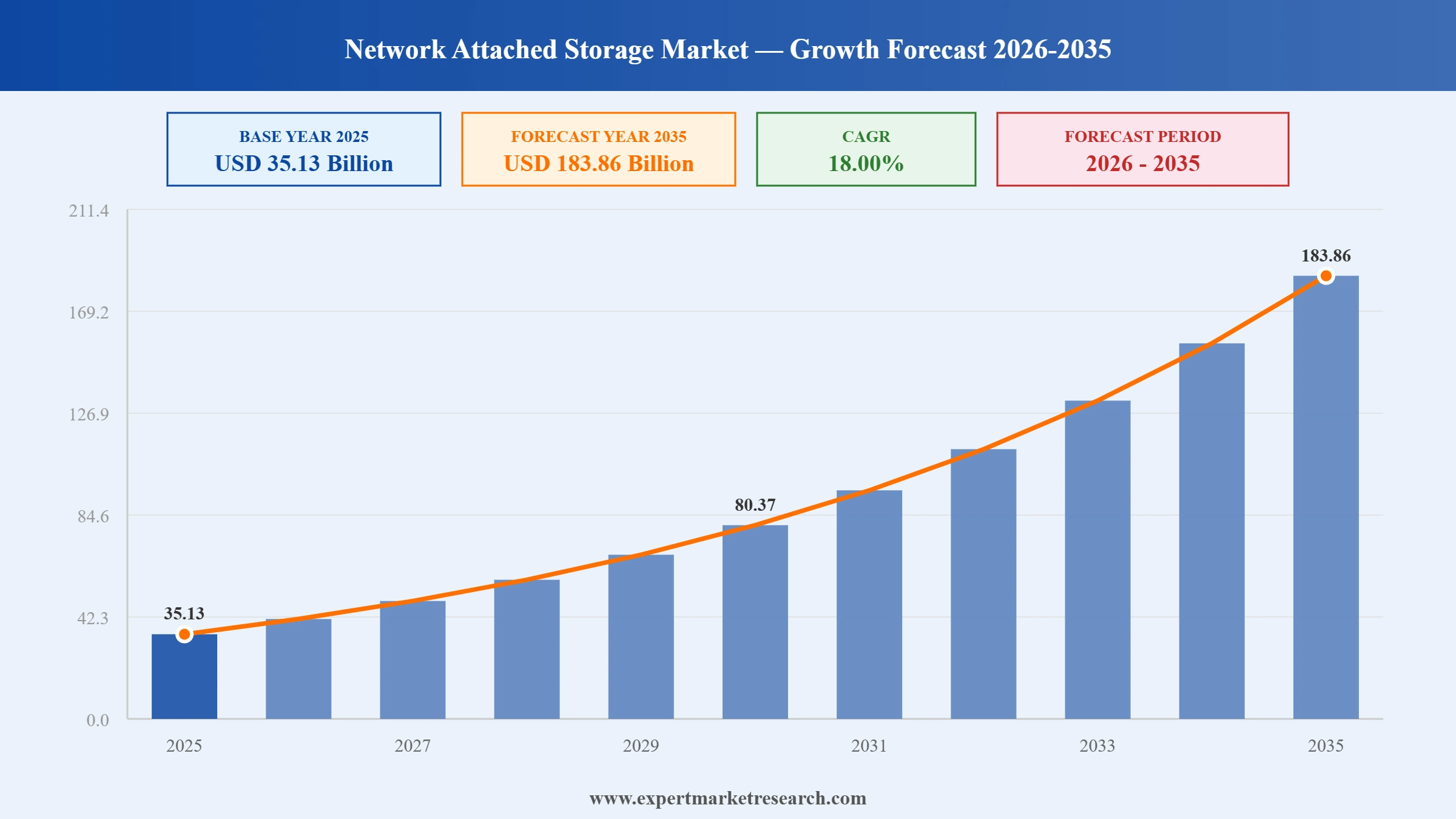

The global network attached storage market was valued at USD 35.13 Billion in 2025 and is projected to reach USD 183.86 Billion by 2035, growing at a CAGR of 18.00% over the forecast period 2026-2035, according to Expert Market Research. This robust growth trajectory reflects the structural acceleration of enterprise data generation, the expansion of AI and machine learning workloads requiring high-throughput centralised storage, the mainstreaming of hybrid cloud architectures in which on-premises NAS serves as the performance and data sovereignty layer, and the deepening penetration of consumer NAS devices as personal cloud alternatives gain mainstream adoption across home and prosumer user segments.

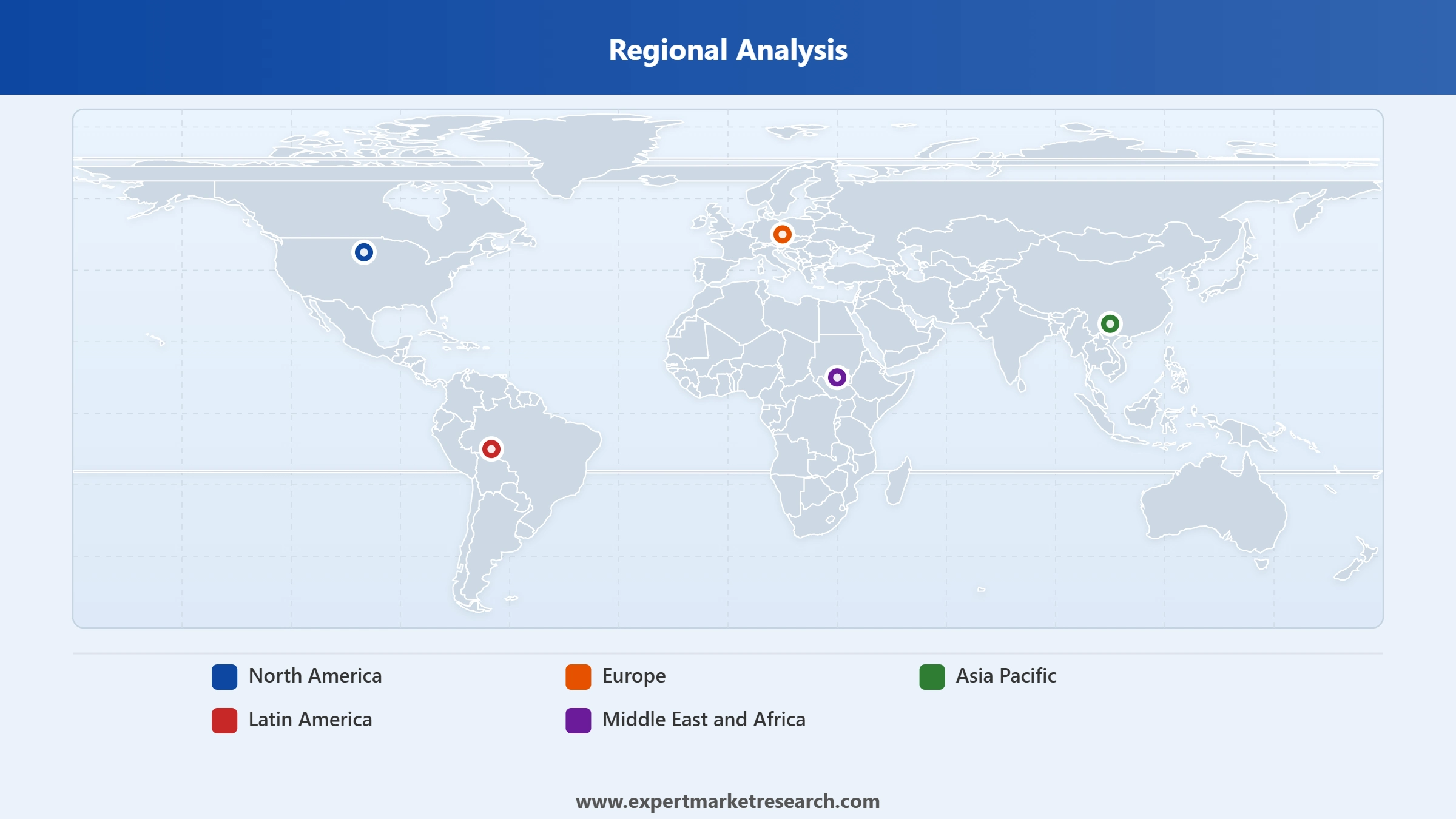

North America held the largest regional share in the network attached storage market in 2025. Scale-out NAS, the fastest-growing architecture segment, is projected to register a CAGR of approximately 17.50% over the forecast period, driven by enterprise demand for horizontally scalable storage for big data, AI, and distributed cloud workloads. The mid-size enterprise segment organisations with fewer than 1,000 employees held a dominant share of enterprise NAS procurement in 2025, reflecting the growing accessibility of sophisticated NAS technology to organisations below the large enterprise tier.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Network Attached Storage Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 35.13 |

| Market Size 2035 | USD Billion | 183.86 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 18.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 20.7% |

| CAGR 2026-2035 - Market by Country | India | 23.8% |

| CAGR 2026-2035 - Market by Country | China | 19.9% |

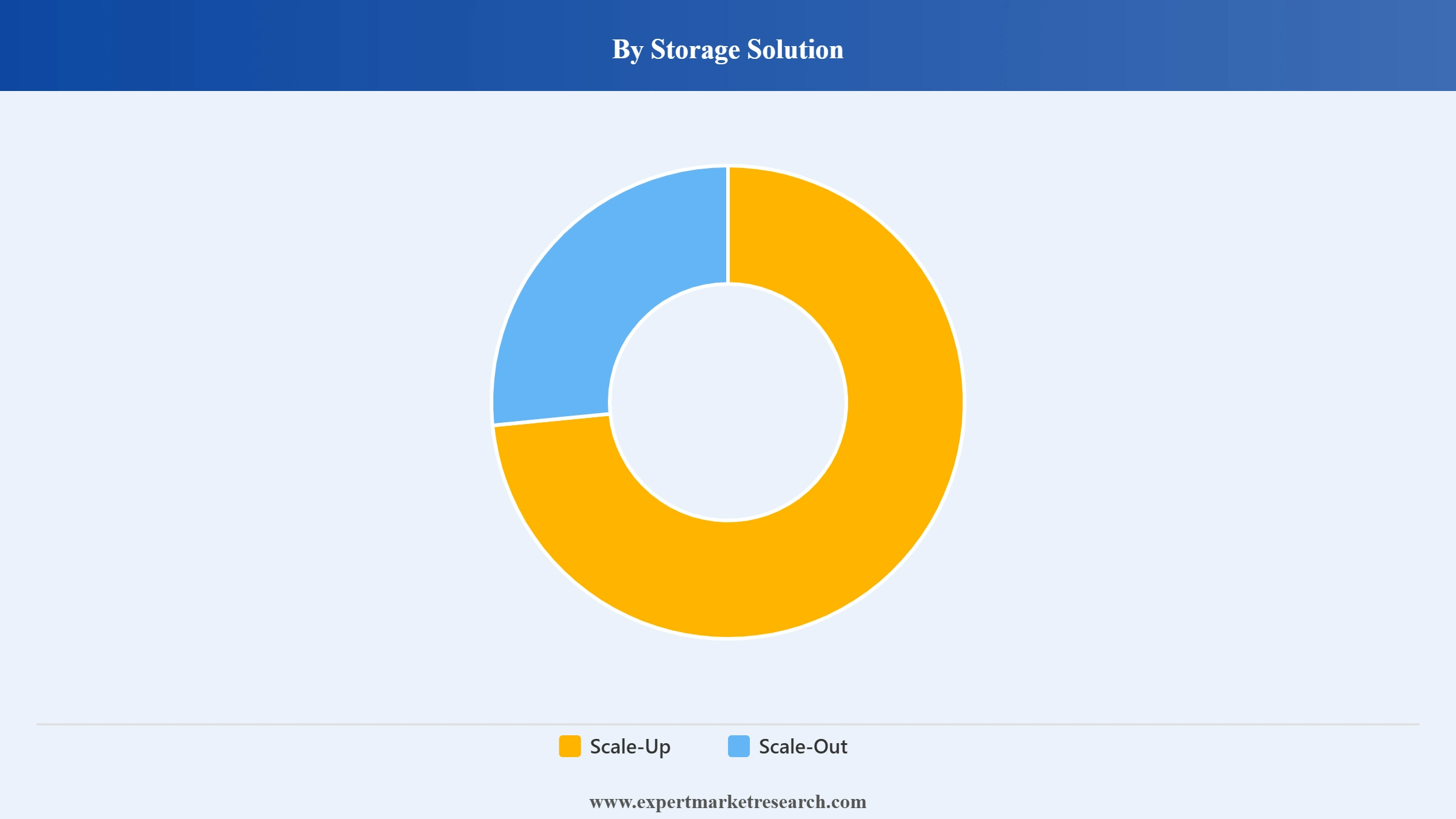

| CAGR 2026-2035 - Market by Storage Solution | Scale-Out | 19.8% |

| CAGR 2026-2035 - Market by End-Use Industry | Banking, Financial Services, and Insurance (BFSI) | 20.5% |

| Market Share by Country 2025 | UK | 3.6% |

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The fundamental driver of the global NAS market is the structural and accelerating growth of data generation across every enterprise function and consumer activity. The volume of data created, captured, copied, and consumed globally is growing at a pace that outstrips the practical and economic ability of organisations to move workloads entirely to public cloud object storage. Files generated by AI inference pipelines, high-resolution video production, medical imaging systems, industrial IoT sensor networks, and genomic research each require the combination of high-throughput sequential access, low-latency random read performance, and multi-user concurrent access that NAS architectures deliver more efficiently than object storage for file-intensive workloads.

The structural expansion of distributed and hybrid work models has increased enterprise demand for centralised, network-accessible file storage that serves geographically dispersed team members with consistent access to shared data. The National Association of Home Builders reported in July 2025 that the telework rate stood at 21.6% in April 2025, with approximately 34.3 million Americans working from home at least part of the time a sustained level that requires organisations to invest in storage infrastructure accessible over wide-area networks. NAS systems integrated with VPN access, remote synchronisation, and hybrid cloud caching serve distributed teams with on-premises performance and data security without the ongoing bandwidth costs and latency of cloud-primary storage models.

Artificial intelligence and machine learning workloads are creating an entirely new NAS demand category that did not meaningfully exist before 2022. Training large language models and computer vision systems requires access to petabyte-scale datasets at throughput rates that public cloud object storage cannot serve without prohibitive cost. High-performance NAS systems with NVMe flash tier, 10GbE or 100GbE connectivity, and GPU server integration are increasingly deployed as the storage layer for on-premises AI training clusters. QNAP's March 2026 release of the TS-h1077AFU, a 10-bay all-flash NAS with AMD Ryzen PRO 7000 processors, exemplifies the product innovation investment being made by NAS manufacturers to specifically serve AI-adjacent workloads requiring high IOPS and low-latency storage access.

Hybrid cloud storage in which enterprise NAS serves as the primary performance tier while integrating with public cloud storage for tiering, backup, and disaster recovery has become the dominant enterprise storage architecture. NAS vendors are competing on the quality and depth of their cloud integration, with Synology's Wasabi partnership formalised in 2026 and QNAP's multi-cloud integration framework representing the commercial direction of enterprise NAS development. Cloud NAS dedicated NAS instances deployed in public cloud environments is the fastest-growing application segment, driven by the need for cloud-native file storage that serves remote and distributed workloads without the management overhead of object storage.

Ransomware attacks targeting enterprise file storage have made data protection capability a primary NAS procurement criterion across all enterprise size tiers. Modern enterprise NAS platforms offer autonomous ransomware detection using anomaly detection algorithms, immutable snapshot technology that prevents encrypted rollback, air-gapped backup protocols, and multi-factor authentication for administrative access. Data compliance requirements under GDPR, HIPAA, SOC 2, and industry-specific frameworks are driving NAS deployments that offer certified encryption, audit logging, and data residency controls that public cloud storage cannot consistently provide across all regulated jurisdictions. Synology's ISO/IEC 27001 certification in May 2026 reflects the commercial importance of formal security credentialing in enterprise NAS procurement decisions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Scale-out NAS storage systems that expand capacity and performance by adding nodes to an existing cluster rather than by upgrading individual nodes is the fastest-growing architecture segment within the NAS market, projected at the highest CAGR through the forecast period. Scale-out architectures are inherently suited to AI training datasets, media and entertainment production workflows, genomic research data lakes, and enterprise collaboration environments where both storage volume and access performance must grow without disrupting running workloads. The ability to add storage nodes without downtime, combined with global namespace management that presents the entire cluster as a single file system to connected applications, makes scale-out NAS the preferred architecture for organisations managing the fastest-growing data categories.

NAS manufacturers are embedding artificial intelligence and machine learning directly into storage operating system firmware to enable predictive maintenance, automated data tiering, intelligent caching, and ransomware behavioural detection without requiring external management tools. Synology's AI Advisor DSM feature, launched in its 2026 platform update, exemplifies the commercial direction of firmware-integrated intelligence across the NAS market. AI-driven data tiering automatically migrates data between NVMe, HDD, and cloud tiers based on access frequency, recency, and predicted future access patterns, reducing storage costs while maintaining performance for active datasets. Ransomware detection algorithms trained on normal file access patterns can identify and quarantine anomalous bulk encryption events before significant data loss occurs.

Consumer NAS devices serve home users' requirements for centralised personal media storage, automated photo and video backup, multi-device file synchronisation, remote access to personal data without dependency on commercial cloud subscriptions, and private network video recording for home surveillance cameras. Synology's BeeStation product line, reviewed in April 2026 across the technology press, targets first-time NAS buyers who want personal cloud functionality without the configuration complexity of traditional multi-bay NAS systems. The growing awareness of cloud subscription costs and data privacy concerns among home users is expanding the addressable consumer NAS market beyond early adopters and prosumers.

All-flash NAS systems using NVMe U.2 and PCIe storage interfaces are displacing HDD-based and hybrid NAS at the high-performance tier of the enterprise market, driven by the latency requirements of AI inference, real-time media editing, and database workloads that SATA HDD latency cannot serve. QNAP's TS-h1290FX all-flash NAS with AMD EPYC 7002 processors and the March 2026 TS-h1077AFU represent the commercial progression of all-flash NAS from specialist scientific computing tool to mainstream enterprise storage product. NVMe-based NAS systems deliver read/write performance comparable to direct-attached storage while retaining the shared access, management, and data protection capabilities of network storage architecture.

Multi-speed Ethernet connectivity has become a standard feature across the NAS market, driven by the growing mismatch between storage media performance and network bandwidth available in typical office and data centre environments. The mainstreaming of 2.5GbE across the midrange consumer and SMB NAS segment with Synology's Plus series and QNAP's mid-tier models adopting 2.5GbE as the baseline connectivity standard has meaningfully increased data transfer performance for video editing, backup, and file-sharing workloads.

The global network attached storage market faces compounding challenges as the competitive landscape intensifies and the technology requirements of enterprise buyers escalate. The primary challenge facing NAS vendors is the commoditisation pressure applied by cloud hyperscalers: Amazon S3, Azure Blob Storage, and Google Cloud Storage offer object storage at declining per-GB costs with effectively unlimited scalability, creating a continuous pricing pressure against on-premises NAS in the capacity storage tier for cold and warm data. Cybersecurity complexity is an escalating challenge while NAS manufacturers are embedding ransomware protection capabilities into firmware, the sophistication of attacks targeting file storage is also increasing, requiring ongoing security investment that smaller NAS vendors may struggle to sustain at the pace required. The NAS market also faces a skills gap challenge: deploying and managing enterprise-grade scale-out NAS requires storage administration expertise that is in short supply, particularly among mid-size enterprises that represent the dominant procurement segment. Integration complexity with heterogeneous cloud and on-premises environments creates deployment friction that delays purchasing decisions and implementation timelines.

Several structural dynamics constrain the pace of NAS market expansion in specific segments and geographies. The capital expenditure nature of on-premises NAS procurement requiring upfront hardware investment compared to the opex consumption model of cloud storage creates adoption barriers for organisations with constrained capital budgets or strong financial preferences for operating expenditure. This dynamic is particularly pronounced in emerging markets where enterprise technology budgets are expanding but the cultural and financial preference for cloud-first procurement is simultaneously entrenching. Drive lock-in practices by major NAS manufacturers most notably Synology's M.2 NVMe pool restriction to proprietary drives create ecosystem dependency risks that generate buyer hesitation and competitive opportunities for vendors with more open compatibility policies. The consumer NAS segment faces the specific restraint of technical complexity: a significant portion of potential home users who would benefit from consumer NAS functionality are deterred by the perceived difficulty of initial setup and ongoing management relative to turnkey cloud storage subscriptions.

The global NAS market presents substantial and growing opportunity across every segment and geography. The scale-out NAS segment is positioned to capture disproportionate revenue growth as AI training clusters, media production facilities, and enterprise data lake deployments scale their storage requirements beyond what scale-up architectures can economically serve. The consumer NAS sub-market represents a structurally underpenetrated opportunity: as cloud subscription costs and data privacy awareness increase among non-technical home users, vendors that successfully simplify the consumer NAS onboarding experience will access a significantly larger addressable market than currently served. Emerging market data centre investment particularly in India, Southeast Asia, and the Gulf Cooperation Council region is creating greenfield NAS deployment opportunities where infrastructure builds from a near-zero base with modern hybrid and all-flash architectures specified from inception. The integration of AI-driven storage management into NAS firmware is creating new software-as-a-service revenue streams for NAS manufacturers that have traditionally monetised through hardware sales, improving the long-term revenue quality and customer retention of leading vendors. Explore the complete 2026–2035 investment opportunity analysis within the Expert Market Research Network Attached Storage Market Report.

The EMR’s report titled “Network Attached Storage Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Storage Solution

Scale-Up NAS commands the dominant revenue share at approximately 50% of the global NAS market, reflecting its widespread adoption across enterprises that require vertically scalable, centrally managed storage with predictable expansion through additional drive capacity within existing enclosures. Scale-up NAS serves structured and unstructured data workloads with moderate to high performance requirements and benefits from mature management tooling and extensive drive compatibility ecosystems.

Scale-Out NAS is the fastest-growing segment, projected at a CAGR of approximately 17.50%, driven by enterprise demand for horizontally scalable storage for big data analytics, AI/ML datasets, cloud-native applications, and distributed workloads that exceed the maximum capacity of individual scale-up nodes.

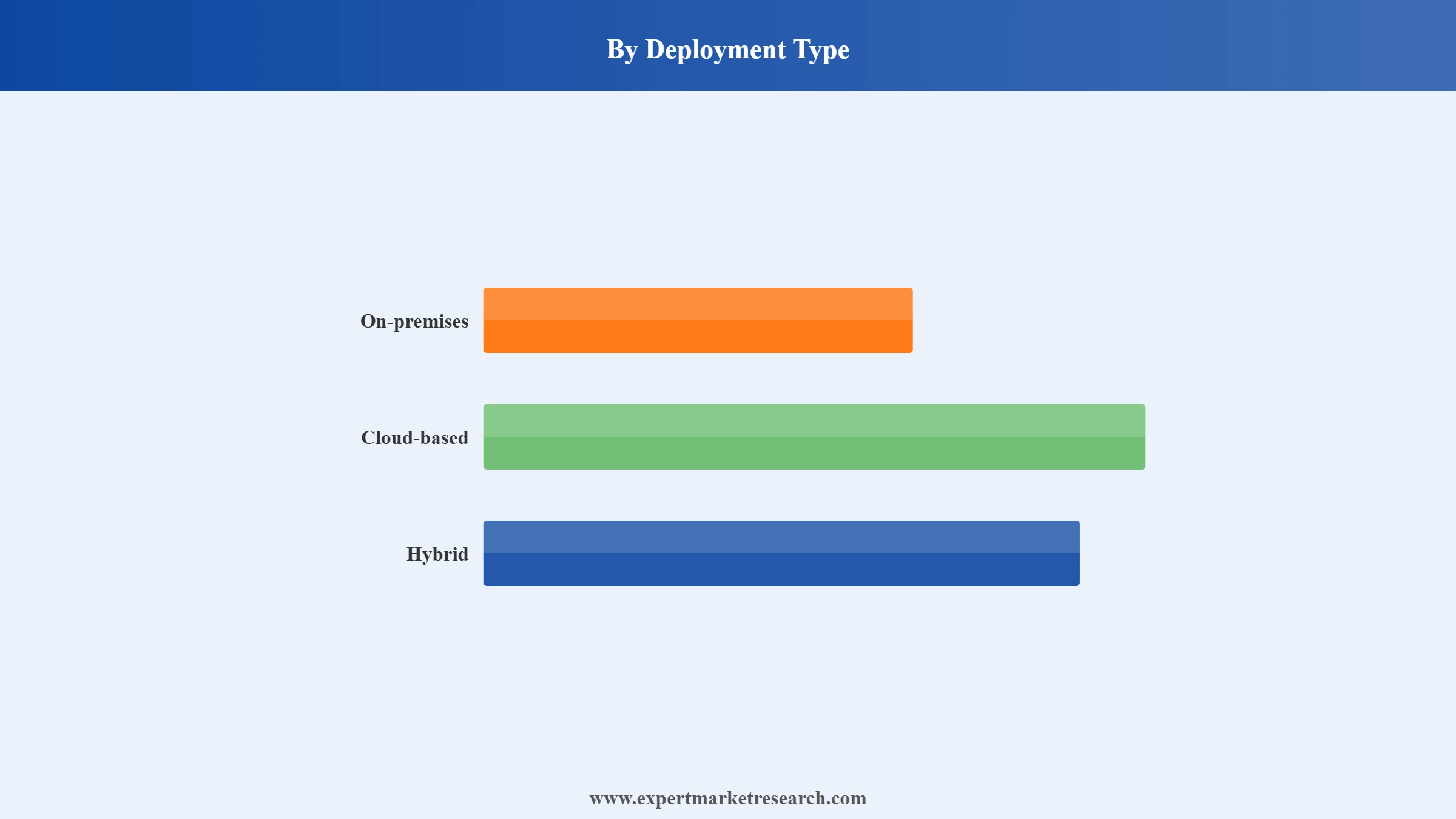

Market Breakup by Deployment Type

On-premises NAS deployment holds the dominant revenue share in the global market, with hardware and storage software physically installed within the organisation's own infrastructure for complete data sovereignty and lowest-latency access. This model is favoured by regulated industries operating under GDPR, HIPAA, and PCI-DSS frameworks that impose data residency obligations, and by AI training, media production, and video surveillance workloads where cloud latency is operationally prohibitive.

Cloud-based NAS is the fastest-growing deployment model, delivering file-level storage as a managed service through platforms including Amazon Elastic File System, Azure Files, and Google Cloud Filestore without requiring on-premises hardware. This model suits cloud-native applications, geographically distributed development teams, and organisations with variable storage demand that benefits from the operational expenditure consumption model and provider-managed maintenance.

Hybrid NAS integrates on-premises performance-tier storage with public cloud capacity tiers within a unified management architecture, automatically migrating data between local and cloud storage based on access frequency, cost policy, and compliance requirements. Synology Hybrid Share, QNAP Hybrid Backup Sync, and comparable vendor platforms illustrate the market-wide convergence toward unified on-premises and cloud storage management that is making hybrid deployment the preferred enterprise architecture through the forecast period.

Market Breakup by End-Use Industry

BFSI is among the largest NAS end-use verticals, driven by high transaction data volumes, SOX, PCI-DSS, and Basel III compliance obligations requiring immutable and auditable storage, and persistent ransomware threats targeting financial data assets. The sector demands high-availability encrypted NAS with comprehensive access logging and zero-tolerance reliability standards.

Retailers deploy NAS for centralised product imagery libraries, e-commerce digital asset management, supply chain data exchange, and omnichannel transaction archiving across physical, online, and marketplace sales channels. The growth of personalisation analytics is expanding retail data storage requirements as organisations consolidate customer behaviour and inventory data for real-time decision support.

Telecom carriers and IT services companies are the highest-volume enterprise NAS buyers, deploying network storage for virtualised service delivery infrastructure, software development file sharing, network performance data, and operations support system storage at scale. High-availability active-active replication architectures across multiple data centre locations are standard requirements in this segment.

Healthcare drives NAS adoption through the exponential growth of DICOM-format medical imaging data from CT, MRI, PET, and ultrasound systems, alongside electronic health records, genomic sequencing pipelines, and clinical AI workloads requiring HIPAA-compliant high-throughput local storage. A single modern imaging department can generate multiple petabytes of cumulative study data requiring long-term accessible archival infrastructure.

Others end-use sectors include energy sector deploys NAS for geophysical survey datasets, SCADA data streams, and drone inspection imagery across field and plant environments. Educational institutions use scale-out NAS for HPC research clusters running genomics, climate modelling, and open science data repositories. Media and entertainment relies on high-throughput all-flash NAS for 4K/8K video production, visual effects rendering, and broadcast playout serving multiple simultaneous users. Additional sectors include government, defence, legal services, and manufacturing each deploying NAS for secure document management, classified data storage, matter file archiving, and CAD/CAM collaboration respectively.

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America leads the global NAS market by revenue share, anchored by the United States as the world's largest enterprise technology market. US enterprise NAS demand is sustained by AI workload storage requirements, hybrid cloud adoption across financial services, healthcare, and media, and a sustained remote work infrastructure investment cycle. Scale-out NAS investment is particularly concentrated in US hyperscale-adjacent enterprise environments.

United States The US NAS market is characterised by deep enterprise adoption of multi-vendor hybrid storage architectures integrating on-premises NAS with AWS, Azure, and Google Cloud through cloud tiering and backup integration.

Europe's NAS market is shaped by GDPR data residency requirements that sustain enterprise on-premises storage investment, combined with strong AI and media production industries in Germany, France, and the United Kingdom driving all-flash NAS adoption.

Germany's NAS market is anchored by manufacturing sector Industry 4.0 data requirements, the country's strong mid-size enterprise (Mittelstand) technology investment culture, and the automotive and engineering industries' requirement for high-performance collaborative file storage.

Asia Pacific is the fastest-growing regional NAS market, driven by data centre expansion in China, India, Japan, South Korea, and Southeast Asia, combined with government data localisation mandates that sustain on-premises NAS investment.

Japan's NAS market is anchored by the country's advanced manufacturing sector, media and entertainment production industry, and enterprise technology investment culture. Buffalo Technology, a Japan-headquartered NAS vendor, contributes to Japan's strong domestic market presence. Hitachi Vantara's enterprise storage division also anchors significant Japan-based NAS deployment.

The Middle East represents a growing NAS market anchored by GCC data centre investment programmes. Saudi Arabia's Vision 2030 digital infrastructure development, including the NEOM cognitive city project, is generating substantial enterprise NAS procurement demand. The UAE's Smart Dubai initiative and technology sector expansion in Abu Dhabi are contributing to regional enterprise storage growth.

Brazil and Mexico lead Latin American NAS adoption, with financial services, media, and government sectors driving enterprise NAS deployments.

The comprehensive Expert Market Research Report provides an in-depth assessment of the market based on the Porter's five forces model along with giving a SWOT analysis. The report gives a detailed analysis of the following key players in the global network attached storage market, covering their competitive landscape and the latest developments like mergers, acquisitions, investments, and expansion plans. The global NAS market is moderately concentrated at the enterprise tier, with established leaders including NetApp, Dell Technologies, and Hewlett Packard Enterprise commanding enterprise data centre deployments, while Synology and QNAP dominate the SMB and mid-enterprise segment. Netgear holds an estimated 14% global NAS market share and Synology approximately 11%, with the remainder distributed across Dell EMC, NetApp, Western Digital, Seagate, and regional specialists. Key players include Synology Inc., QNAP Systems Inc., Western Digital Corporation, NetApp Inc., Dell Technologies Inc., Hewlett Packard Enterprise, Seagate Technology Holdings plc, NETGEAR Inc., Hitachi Vantara LLC, and Buffalo Americas Inc.

Buffalo Americas is a prominent supplier of trustworthy, secure, and easy-to-use data storage solutions with exceptional pre-and post-sales service. It creates high-quality networking and storage, among other technological solutions that make life easier and provide a good return on investment. It offers solutions for small to medium-sized businesses.

Synology Inc. Synology (Taiwan) is the world's leading NAS vendor by unit share in the SMB and enterprise mid-tier segments, managing approximately 350 exabytes of data across 260,000+ businesses globally. In May 2026, Synology launched three new enterprise RackStation models (RS6426xs+, RS4826xs+, RS3626xs), achieved ISO/IEC 27001 certification, deployed the PAS7700 active-active NVMe enterprise platform, and formalised a Wasabi cloud partnership, while receiving recognition as a Gartner Strong Performer in Backup and Data Protection Solutions.

QNAP (Taiwan) is a leading NAS manufacturer serving the prosumer through enterprise segments with hardware-forward products emphasising PCIe expandability, AMD and Intel processor options, and QuTS hero ZFS-based operating system for critical data environments. QNAP's March 2026 release of the TS-h1077AFU 10-bay all-flash NAS with AMD Ryzen PRO 7000 processors demonstrates its commitment to performance-tier enterprise storage innovation.

Western Digital (US) is among the largest storage technology companies globally, serving the NAS market through its WD Red and WD Red Pro hard drive lines optimised for 24/7 NAS workloads and its My Cloud NAS product line for home and small business users. Western Digital was named to the 2026 S&P Dow Jones Best in Class Index North America, reflecting its corporate sustainability standing within the storage industry.

NetApp (US) is a leading enterprise storage and data services company, providing scale-out NAS, unified storage, and cloud data management solutions deployed in large enterprise data centres and hybrid cloud environments globally. NetApp's ONTAP operating system serves as the enterprise storage platform for customers requiring high-availability, multi-protocol storage serving both SAN and NAS workloads simultaneously.

Seagate Technology Holdings plc Seagate (US/Ireland) supplies NAS-optimised hard drives including the IronWolf and IronWolf Pro series designed for 24/7 multi-drive NAS operation and has developed NAS system partnerships with QNAP and other vendors to deliver integrated enterprise storage solutions.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global NAS market is projected to grow at a CAGR of 18.00% between 2026 and 2035, according to Expert Market Research.

The global NAS market was valued at USD 35.13 Billion in 2025, according to Expert Market Research.

The key network attached storage market trends include the growing digitalisation, increase in remote working, storage and sharing of multimedia, and backups of various devices.

The numerous end-use industries of network attached storage include banking, financial services, and insurance (BFSI), consumer goods and retail, telecommunications and IT, healthcare, energy, education and research, and media and entertainment, among others.

Network attached storage (NAS) is a file-level storage architecture that creates a centralised storage for multiple users across devices.

Key players include Synology Inc., QNAP Systems Inc., Western Digital Corporation, NetApp Inc., Dell Technologies Inc., Hewlett Packard Enterprise, Seagate Technology Holdings plc, NETGEAR Inc., Hitachi Vantara LLC, and Buffalo Americas Inc., among others profiled in the Expert Market Research NAS Market Report.

The market is projected to reach USD 183.86 Billion by 2035 by 2035, growing at a CAGR of 18.00% through the forecast period 2026–2035.

The consumer NAS market encompasses personal cloud devices enabling home users to store, back up, and remotely access media libraries and personal files without dependency on commercial cloud subscriptions.

Key NAS market share holders include Netgear (approximately 14% global share), Synology (approximately 11%), with NetApp, Dell EMC, Western Digital, QNAP, and Seagate collectively holding significant enterprise and SMB segment positions. Full manufacturer share analysis is available in the Expert Market Research NAS Market Report.

Scale-out NAS is the fastest-growing segment, projected at approximately 17.50% CAGR, driven by enterprise demand for horizontally scalable storage for AI training, big data analytics, media production, and distributed cloud workloads.

North America leads the global NAS market by revenue share, with the United States as the largest national market. Asia Pacific is the fastest-growing regional market, driven by data centre expansion in China, India, Japan, and Southeast Asia.

Key drivers include exponential enterprise data growth, AI and machine learning workload storage requirements, hybrid cloud architecture adoption integrating on-premises NAS with cloud tiers, remote and distributed workforce file access infrastructure investment, and ransomware protection and data compliance requirements.

Scale-out NAS allows storage expansion by adding nodes to an existing cluster without disrupting operations, making it ideal for AI, big data, cloud, and distributed workloads.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Storage Solution |

|

| Breakup by Deployment Type |

|

| Breakup by End-Use Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.