Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The North America third-party logistics (3PL) market was valued at USD 394.90 Billion in 2025. The industry is expected to grow at a CAGR of 5.10% during the forecast period of 2026-2035 to reach a value of USD 649.40 Billion by 2035. The market growth is attributed to the strategic consolidation and portfolio realignment of logistics providers.

Leading firms are acquiring companies to leverage scale, service lines, and market reach, as well as divesting non-core businesses to concentrate on niche, high-margin services. For example, RXO, a company, in June 2024, acquired the Coyote Logistics company from UPS in a deal valued a staggering USD 1.025 billion. This positioned RXO as one of the biggest freight brokage service providers in North America. Again, the deal by UPS to sell the Coyote Logistics company highlights the trend of divesting and concentrating on the core parcel and premium logistics service offerings. This also shows that the trend in the industry aligns as 3PL companies balance the portfolio and align M&As and divestitures to optimize the delivery of operational efficiency and service specializations amidst the dynamic logistics industry.

Base Year

Historical Period

Forecast Period

In 2023, the e-commerce sector in the United States represented 22.0% of total retail sales.

As of 2023, there were 761,474 people working in the 3PL and 4PL logistics industry in the US.

3PL companies are significantly adopting a wide range of technology solutions, particularly AGVs (automated guided vehicles).

Compound Annual Growth Rate

5.1%

Value in USD Billion

2026-2035

*this image is indicative*

The increasing need for healthcare, biologic, and temperature-sensitive products is leading to the expansion of these distribution networks by 3PL companies. EVERSANA established a new distribution facility in Memphis, Tennessee, in April 2025, with cold storage and AI-powered warehouse management systems in their 358,000-square-foot facility. Not only is this essential for enhancing storage and distribution of pharmaceuticals, but it again establishes third-party logistics companies as vital links for healthcare distribution in the market and as catalysts in terms of their niche services.

3PL companies are polishing their service portfolios by introducing reverse logistics services and value additions to effectively deal with the returns aspect. In October 2025, DHL Supply Chain has come up with the “ReTurn Network” for the North American region, providing multi-client reverse logistics solutions to the retail and manufacturing sectors. By this, 3PLs minimize costs associated with their day-to-day business activities and satisfy the customers, hence fueling the North American 3PL market.

The 3PL companies are increasing their warehousing networks to accommodate sector-driven requirements and optimize deliveries. As of September 2024, BroadRange Logistics expanded its networks to 10.5 million sq. ft. in seven states across the United States to serve the solar industry supply chain. The development will optimize flexibility and customer service for 3PL to capitalize on growth within the sector and adapt to a dynamic logistics environment.

Temperature-controlled storage and international distribution of such items are very important, and in May 2024, CJ Logistics America expanded its cold storage facility near Kansas City, improving capabilities for such items. As such, these improvements have boosted the North American 3PL market, which is registering growth through such capabilities and improved services offered by these different infrastructure services.

Companies such as 3PL providers are also leveraging and exploring technology solutions that will improve shipment visibility and operational collaboration. Trimble began the launch of Transporeon Visibility, its shipment visibility solution, in the North American market in September 2024. The adoption and integration of such technologies enable 3PL companies to improve the efficiency and resilience of the supply chains and improve the transparent nature of their services, which increases market growth and cements innovation as a market differentiator.

The EMR’s report titled “North America Third-Party Logistics (3PL) Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Service

Key Insights: The North America 3PL industry is made up of Dedicated Contract Carriage (DCC), Domestic Transportation Management (DTM), International Transportation Management (ITM), Warehousing and Distribution, and Value Added Logistic Services (VALs). DCC solutions, offered by J. B. Hunt and Ryder, help manage specific fleets, and BlueGrace Logistics further develops DTM solutions integrated with TMS to better manage freight within America. The development of ITM is fueled by companies such as Evans Transportation, increasing their offices across borders into Laredo, Texas. The purchase of Inmar Supply Chain Solutions by DHL Supply Chain improves their reverse logistics/return capabilities. The primary warehouse and distribution company, GXO Logistics, provides order fulfillment, kitting, and e-commerce logistics solutions across North America.

Market Breakup by Transport

Key Insights: The transport segments in the 3PL environment in North America are Railways, Roadways, Waterways, and Airways. J.B. Hunt Corporation enables intermodal transportation by forming collaborative ventures with railways, which connects well with trucking infrastructure, while Union Pacific is developing Mainline Texas Industrial Park, which is expected to help railways-served distribution centers. Roadways are still the most prominent, with Ryder and FedEx Logistics transporting shipments through long road routes. Waterways are accessed by DP World Logistics, which uses port-centric distribution, while Airways are accessed by Kuehne+Nagel for expedited, high-value shipments.

Market Breakup by End Use

Key Insights: In terms of end-use, the North America third party logistics market caters to sectors such as retail, healthcare, manufacturing, automotive, and others. Retail is benefitted using 3PL companies such as GoBolt, which offers its customers e-commerce warehousing and last-mile delivery operations across Canada and the United States. The logistics of the healthcare industry have been extended with the announcement of the UPS acquisition agreement to purchase Andlauer Healthcare Group, improving the cold chain distribution infrastructure. Manufacturing and Automotive industries use the services of AIT Worldwide Logistics and Kuehne+Nagel logistics companies to handle the transportation of parts, finished products, and sequencing operations.

Market Breakup by Region

Key Insights: Regionally speaking, the North America 3PL market consists of the United States of America and Canada. As far as the United States is concerned, the expansion of warehousing and tech-enabled fulfillment offerings by the likes of Ryder, J.B. Hunt, and DHL Supply Chain will continue to support e-commerce and industrial distributions. International freight between the United States and Mexico will be improved by Evans Transportation's opening of a new office in Laredo. In the Canadian marketplace, the likes of GoBolt and UPS Supply Chain Solutions will be expanding their offerings in the areas of fulfillment and cold chain facilities.

By service, dedicated contract carriage (DCC) is in high demand

Based on service, the dedicated contract carriage market is dominated by DCC, which is in huge demand. Notably, the main driving factor behind the growth of DCC is the growing need for specialized fleet solutions catering to the large volume of national shippers, who need specific capacity and reliability in logistics solutions. Logistical leaders, including the likes of Ryder and J.B. Hunt, are heavily invested in better fleet technology and customized routing solutions aimed at reducing delivery times and ensuring on-time delivery. Partnerships between network carriers and middle-mile logistics solutions have also led to improved delivery reliability, contributing to DCC becoming the popular model of logistics solutions.

Warehouse and distribution services are quickly evolving as third-party logistics companies react to the challenges of e-commerce, the need to create a distribution network that enables services across multiple channels, and the desire to place inventory close to the end consumer. For instance, in May 2025, DHL Supply Chain acquired an e-commerce and retail logistics company that operates in the United States, IDS Fulfillment, adding over 1.3 million square feet of warehouse space across major markets in the country catering to small and midsized customers' distribution requirements.

By transport, roadways show notable growth

Road remains the foremost method of operation for the 3PL industry in North America due to its flexibility and ability to handle point to point delivery services. Organizations such as XPO Logistics and Total Quality Logistics (TQL) continue to invest in and benefit from the use of advanced telematics solutions within their trucking fleets and real-time routing solutions in order to optimize efficiency and utilization of the trucking capacities on long haul and regional trucking networks. Advances in investments in trucking optimization solutions continue to help the 3PL industry handle a higher number of loads with reduced miles of empty trucks due to growing trucking demands brought about by e-commerce and JIT delivery needs.

Air cargo is a significant part of third-party logistics markets in North America. Air freight transport is driving growth in higher value or time-critical cargo transport, particularly in verticals like consumer electronics, biopharmaceuticals, and express packages. Companies in this space are working to develop air freight transport management systems, which enable better visibility and time-efficient transport over global trade lanes. For example, Flexport's steady growth of their freight forwarding and customs brokerage services, owing to investment by leading venture capitalists like Shopify ($260MM invested), highlights just how air and global solutions are being meshed with innovative use of technology and process redesign for time-efficient and reliable transportation and delivery to high value, time-critical clients.

By end use, retail generates significant revenue

Retail is one of the prime use types in the 3PL market, because of omnichannel distribution, peak season delivery, and return management. The 3PL industry is witnessing innovation in terms of integrated fulfillment networks and scalable warehousing solutions to meet retail fluctuations. For instance, the recent expansion of GoBolt in the United States and Canada in terms of warehousing, order fulfillment, and last-mile delivery helps to improve retail logistics for e-commerce sellers for faster delivery. Such initiatives will help retailers to effectively send order fulfillment to a platform-driven scalable logistics solution, in turn, directly leveraging customer demand.

The healthcare industry is a major driver of growth in the 3PL industry due to the strict regulations of temperature controlled, traceability, and healthcare regulations. The healthcare logistics infrastructure is also being developed by 3PL companies for pharmaceutical and temperature sensitive healthcare goods transportation. For instance, in April 2025, UPS committed to acquiring the Andlauer Healthcare Group for USD 1.6 billion, a move geared at acquiring a stronger cold chain logistics network in Canada and offering precise healthcare supply chain services to clients in North America.

In the United States, the factors contributing to the growth of the 3PL market include well-developed infrastructure, advanced e-commerce demand, and extensive logistics capabilities. The 3PL companies have been leveraging the digitalization trend and collaborations to optimize their offerings on domestic routes. An example of this is the collaboration between Yamaha Motor Manufacturing Corporation and DHL Supply Chain, which exemplifies the United States Manufacturing-led approach to increase their internal distribution capabilities and expedite delivery performance.

The logistics infrastructure of Canada is supportive of cross border movements and fulfillment services, which is further reinforced by trans-national expansions and adoption of services. The 2025 expansion by Evans Transportation in the Laredo, Texas region, which is supportive of Mexico-United States cross border logistics, is just one of the instances which indicate Canadian based carriers' extension of regional networks of service delivery, which is likely to optimize international connectivity on behalf of Canadian and United States-based clients.

Market players operating in the North America 3PL market are also expanding their service offerings and geographic reach in response to growing demands in e-commerce, healthcare, and temperature-controlled logistics. Companies such as Ryder, J. B. Hunt, and DHL Supply Chain are focusing on warehouse expansion and development of cold storage facilities and AI-powered warehouse management systems to optimize logistics and improve relationships with clients.

To remain competitive, 3PL operators are increasingly looking at collaborations, acquisition strategies, and technology integration. Kuehne+Nagel and Nippon Express are looking at digital freight platforms and intermodal solutions, and there are acquisition strategies such as Kenco’s entry into Canada to enhance border logistics. This will help them scale their operations and provide visibility to their supply chain and add to their strength in a dynamic North American logistics landscape.

Deustsche Post AG is a globally operating company which after the brand name DHL is known as one of the biggest service providers in the logistics and supply chain management industry. The company was founded in 1969 and its main office is located in Bonn, Germany. Deustsche Post provides express, freight, supply chain, and e, commerce logistics services to the whole world as a one, stop solution.

Schenker AG is a worldwide logistics and freight forwarding company, which can trace its roots to 1872 and has its headquarter facilities in Essen, Germany. The Company engages in the business of land transportation, air freight, ocean freight, contract logistics, supply chain management, and various other activities, which are closely related to each other, and different routes.

CH Robinson Worldwide Inc. is one of the pioneer third, party logistics companies. It was established in 1905, and it is headquartered in Eden Prairie, Minnesota, United States. The company concentrates on freight brokerage, multimodal transportation, and tech, based logistics solutions.

United Parcel Service, Inc. is a leader on the world market in package delivery and supply chain solutions. It was founded in 1907 and is headquartered in Atlanta, Georgia, United States of America. They offer logistics, express, freight, and contract logistics solutions to customers from all over the world.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other players in the market include FedEx Corp, Nippon Express Holdings Inc., J B Hunt Transport Services Inc., Kuehne + Nagel International AG, Ryder System Inc., Hub Group Inc., CEVA Logistics S.A., and others.

Explore the latest trends shaping the North America Third-Party Logistics (3PL) Market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on North America third-party logistics (3PL) market trends 2026.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

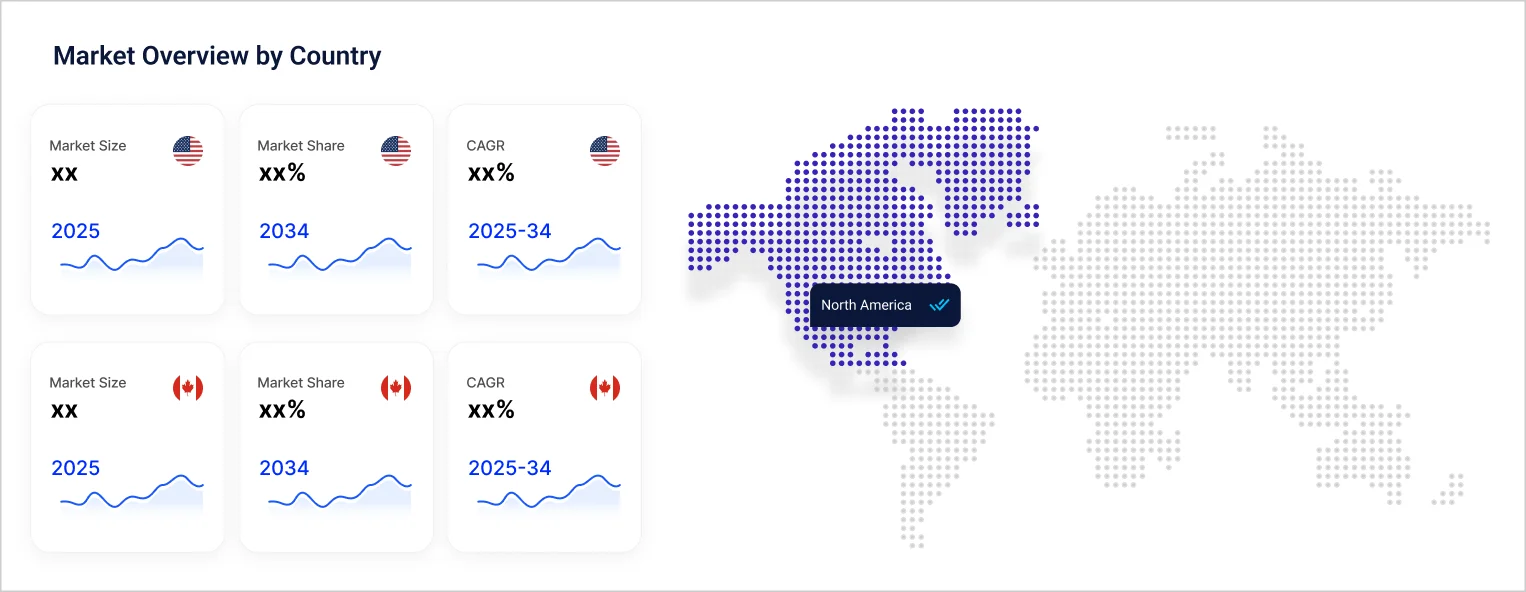

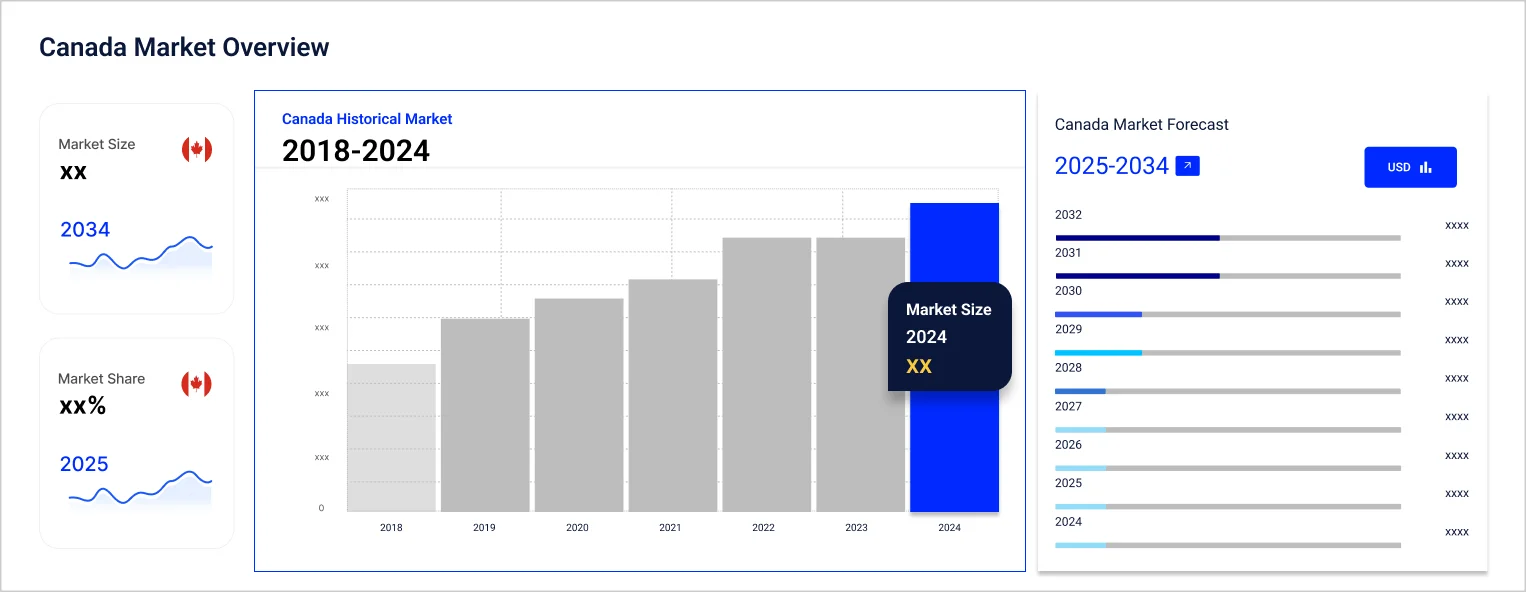

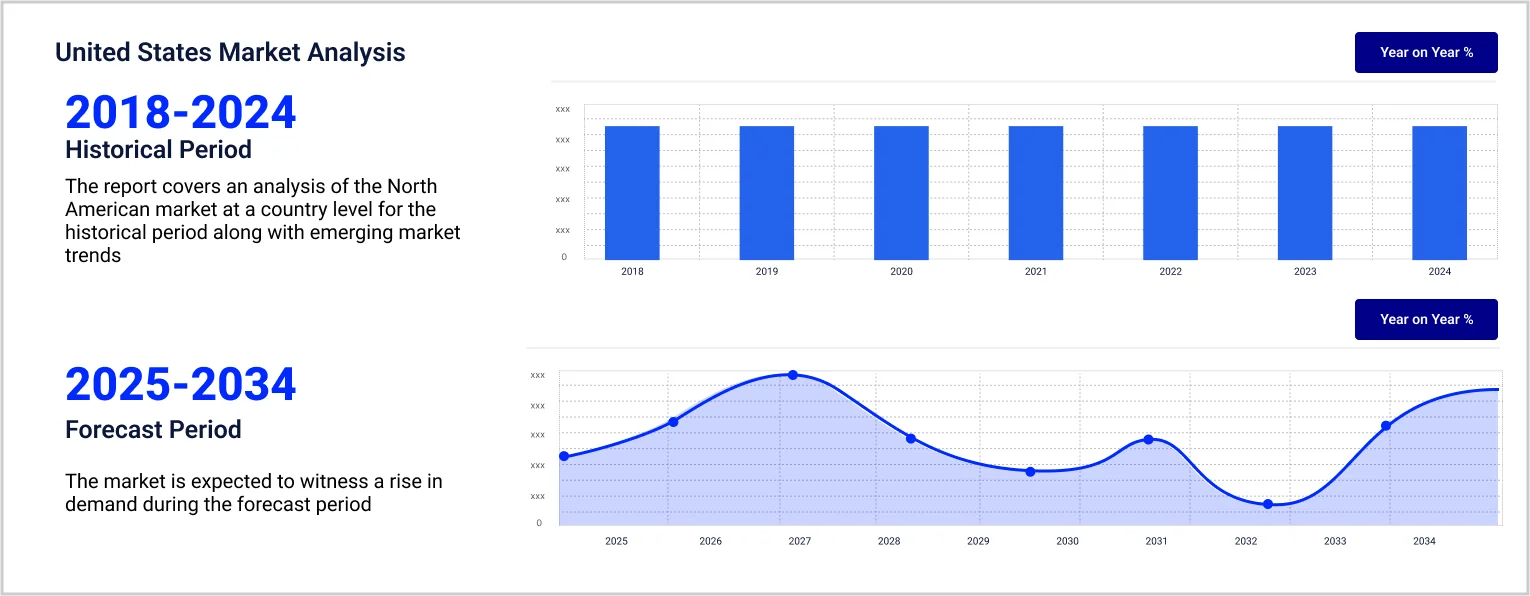

In 2025, North America third-party logistics (3PL) the market reached an approximate value of USD 394.90 Billion.

The market is projected to grow at a CAGR of 5.10% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of USD 649.40 Billion by 2035.

The United States and Canada are the countries covered in the market report.

Railways, roadways, waterways, and airways are the major transportation methods in the market.

The major classifications based on service include dedicated contract carriage (DCC), domestic transportation management (DTM), international transportation management (ITM), warehousing and distribution, and value-added logistic services (VALs).

The major end uses of third-party logistics include retail, healthcare, manufacturing, automotive, and others.

The key players in the market include Deutsche Post AG (DHL), Schenker AG, C.H. Robinson Worldwide Inc, United Parcel Service, Inc, FedEx Corp, Nippon Express Holdings Inc, J.B. Hunt Transport Services Inc, Kuehne + Nagel International AG, Ryder System Inc, Hub Group Inc, CEVA Logistics S.A., and others.

Key strategies driving the market include acquisitions and partnerships, digital platform adoption, warehouse automation, cold chain expansion, and development of value added logistics services.

Major challenges that the North America third-party logistics (3PL) market faces include high operating costs, labor shortages, capacity fluctuations, regulatory complexity, and technology investment requirements.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Service |

|

| Breakup by Transport |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share