Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

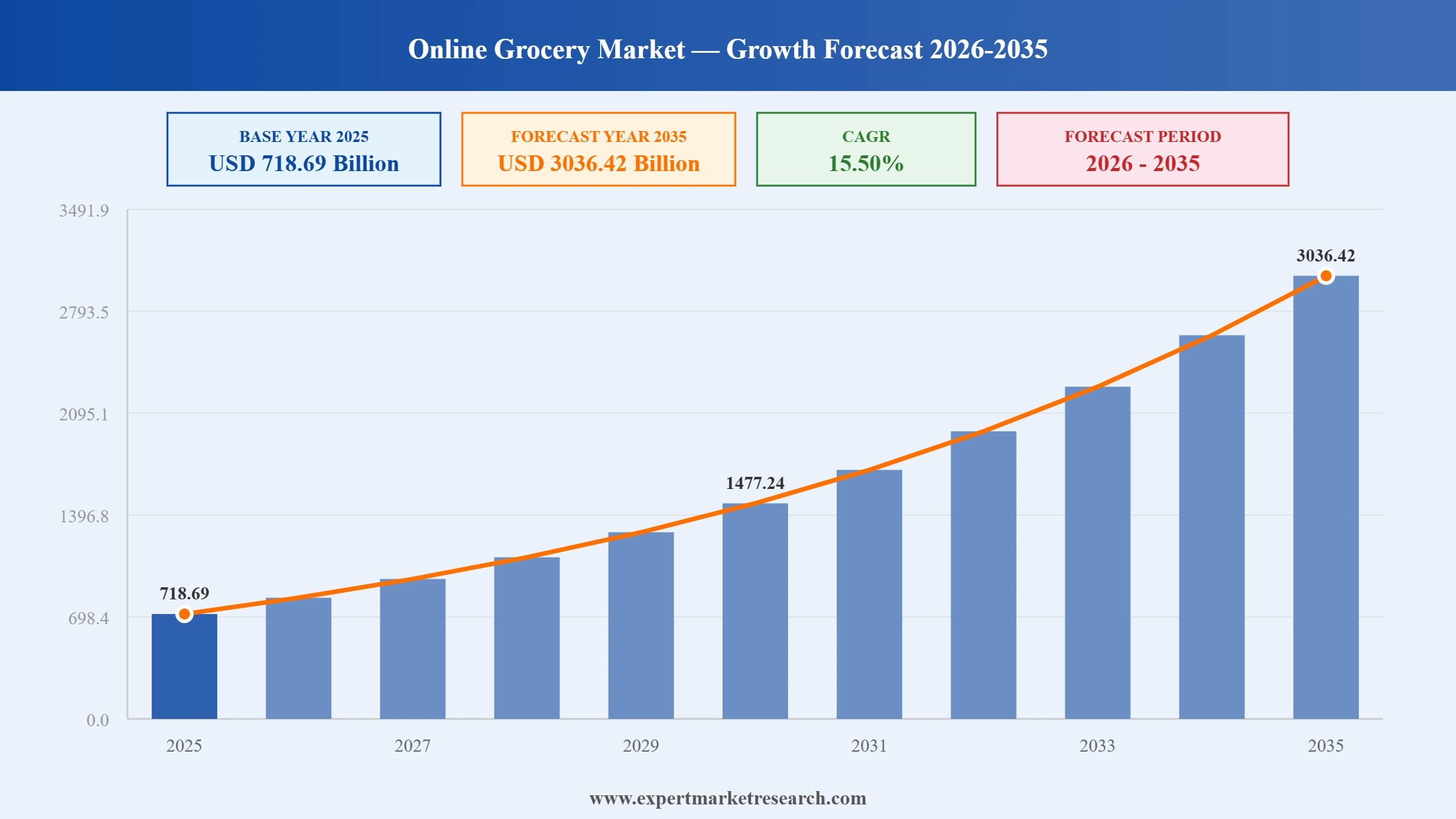

The global online grocery market reached a value of USD 718.69 Billion in 2025 and is projected to grow to USD 3036.42 Billion by 2035, expanding at a CAGR of 15.50% between 2026 and 2035. This trajectory reflects a structural shift in how households source everyday essentials, as digital fulfilment moves from a convenience used occasionally to a default channel for a widening share of grocery spend.

Online grocery refers to the purchase of food, beverages, and household essentials through digital platforms, with orders fulfilled through home delivery, scheduled drop-off, or click-and-collect pickup. What began as a niche service concentrated in dense urban centres has matured into a mainstream retail channel spanning fresh produce, dairy, packaged goods, meat and seafood, and pantry staples. The category now sits at the intersection of food retail, e-commerce, and last-mile logistics, and its growth is being shaped by changing consumer routines, deepening smartphone penetration, and continuous investment in fulfilment infrastructure.

The market’s expansion is broad rather than concentrated. Demand is rising across developed economies, where convenience and time-savings drive repeat usage, and across emerging markets, where first-time digital grocery buyers are entering the category in large numbers as connectivity and digital payments spread. The result is a market that is simultaneously scaling in value and diversifying in format, from full-basket weekly shops to rapid top-up orders delivered within minutes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Several trends are actively reshaping the online grocery landscape. The most visible is the rise of quick commerce, in which orders are fulfilled from hyper-local dark stores within very short delivery windows. This format has redefined consumer expectations around immediacy and has pulled top-up and impulse grocery spend online. Closely related is the build-out of micro-fulfilment centres, which place automated or semi-automated picking close to demand to raise throughput and lower per-order cost.

Personalisation is a second defining trend. Platforms increasingly use behavioural data to tailor recommendations, surface relevant promotions, and pre-populate baskets, shortening the shopping journey and lifting basket size. Artificial intelligence is being applied across demand forecasting, inventory management, dynamic delivery routing, and substitution logic for out-of-stock items, improving both the consumer experience and operational efficiency.

A third trend is the blurring of channels. Click-and-collect and curbside pickup bridge the physical and digital store, giving consumers the assortment and trust of a familiar retailer with the convenience of online ordering. Sustainability is also rising up the agenda, with attention to packaging reduction, route optimisation to cut delivery emissions, and reduction of fresh-food waste through better demand prediction. Together, these innovations are widening the addressable market and raising the baseline expectation for speed, reliability, and experience.

The primary driver is the durable change in consumer behaviour. Convenience, time-savings, and the ability to shop at any hour have made digital grocery a fixture of household routines, and the behaviour has proven sticky across demographics. Rising smartphone penetration and the maturation of digital payments have removed friction at both ends of the transaction, making it easy to discover, order, and pay.

Infrastructure investment is a second driver. The expansion of dark stores, micro-fulfilment, and cold-chain logistics has solved the operational problems that once constrained online grocery, particularly in fresh categories. As fulfilment networks densify, delivery becomes faster and cheaper, which expands the market into new geographies and customer segments. Retailer and platform competition is a third driver, pushing continuous improvement in assortment, speed, and loyalty propositions, all of which compound demand. Underlying these is broad urbanisation and the growth of time-pressed, dual-income, and younger households for whom digital convenience is a default expectation rather than a novelty.

The online grocery market is segmented by product type, platform, purchase type, and region. This structure reflects how demand is generated, how consumers transact, and where growth is concentrated.

Market Breakup by Product Type

By product type, the market spans Fresh Produce, Breakfast and Dairy, Snacks and Beverages, Meat and Seafood, Staples and Cooking Essentials, and Others. Staples and packaged categories were the earliest to migrate online because they are shelf-stable, predictable, and easy to fulfil. The more significant recent shift has been the movement of fresh and perishable categories, including fruits, vegetables, dairy, and meat and seafood, into the digital basket. Reliable cold-chain handling and improved quality assurance have built the consumer trust needed for these high-frequency, high-margin categories to scale online, and they are now central to platform differentiation.

Market Breakup by Platform

By platform, the market divides into Web-Based and App-Based channels. Web-based ordering remains relevant for desktop planning of larger, full-basket shops, while app-based ordering has become the engine of frequency and retention. Applications support push-driven re-engagement, location-aware delivery, saved preferences, and rapid reordering, all of which lift order frequency and lifetime value. The app channel is also where the fastest fulfilment formats, including on-demand and rapid delivery, are most heavily concentrated.

Market Breakup by Purchase Type

By purchase type, the market is split between One-Time and Subscription purchases. One-time orders capture spontaneous and need-based demand, including rapid top-up shopping. Subscription models, by contrast, lock in recurring revenue and predictable demand, whether through membership programmes that bundle free or discounted delivery or through scheduled replenishment of regularly consumed items. Subscriptions are strategically important because they raise retention, smooth fulfilment planning, and improve the economics of last-mile delivery.

Market Breakup by Region

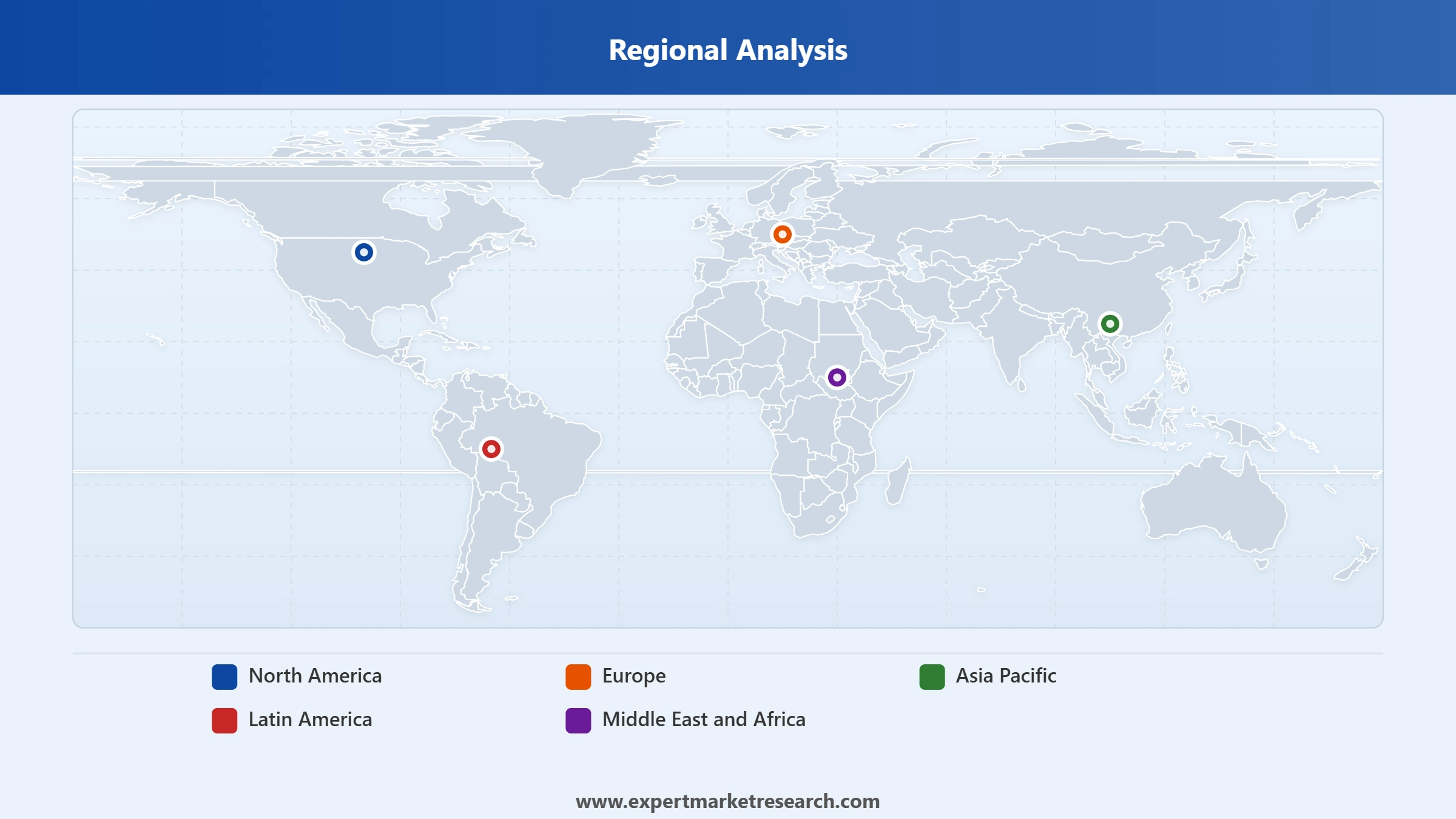

By region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Each region sits at a different point on the adoption curve, from highly penetrated, convenience-led markets to fast-emerging markets where first-time digital grocery buyers are driving rapid expansion. Regional dynamics are examined in detail later in this report.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The competitive landscape is dynamic and varies markedly by geography. Incumbent grocery retailers compete on assortment depth, supplier relationships, and the ability to use existing stores as fulfilment hubs. Global e-commerce operators leverage logistics scale, technology, and large existing customer bases to integrate grocery into wider retail offerings. Rapid-delivery and pure-play specialists compete primarily on speed, convenience, and hyper-local fulfilment density.

Competition increasingly turns on fulfilment capability and customer retention rather than on price alone. Investment in automation, delivery-network density, data-driven personalisation, and loyalty or subscription programmes is where leading players differentiate. Partnerships across retail, logistics, and technology are common, as operators seek to combine assortment, speed, and reach without building every capability in-house. The report profiles the strategies, positioning, and capabilities of the major participants shaping the global market.

Amazon.com Inc. was founded in 1994 and is headquartered in Seattle, Washington, United States. The company operates one of the world's largest e-commerce and digital ecosystems, with its grocery business spanning Amazon Fresh, Whole Foods Market, and rapid-delivery formats. Amazon is recognised for combining vast logistics scale, technology-led fulfilment, and Prime membership integration to serve grocery customers across full-basket and on-demand shopping needs.

Walmart Inc. was founded in 1962 and is headquartered in Bentonville, Arkansas, United States. As the world's largest retailer by revenue, the company has built a leading online grocery operation underpinned by its extensive store network, which doubles as a fulfilment base for delivery and pickup. Walmart is recognised for its omni-channel model, strong private-label assortment, and continued investment in last-mile innovation, including automation and membership-driven convenience.

The Kroger Co. was founded in 1883 and is headquartered in Cincinnati, Ohio, United States. One of the largest grocery retailers in North America, Kroger has expanded its digital business through delivery, curbside pickup, and automated fulfilment centres. The company is recognised for its data-driven personalisation, loyalty programme strength, and growing retail-media network, which together support higher basket sizes and improved customer retention online.

Costco Wholesale Corporation was founded in 1983 and is headquartered in Issaquah, Washington, United States. Operating a membership-based warehouse club model, Costco has extended its grocery reach into online ordering, same-day delivery, and bulk e-commerce fulfilment. The company is recognised for its high-volume, value-focused assortment and loyal membership base, which provide a durable foundation for sustained growth in digital grocery.

Target Corporation was founded in 1902 and is headquartered in Minneapolis, Minnesota, United States. A leading general merchandise and grocery retailer, Target supports its online grocery business through same-day delivery and pickup services powered by its store-as-fulfilment-hub strategy. The company is recognised for its strong brand positioning, curated assortment, and integration of digital convenience with an established physical retail footprint.

Other key players in the global online grocery market include Tesco Plc, JD.com, Inc., FreshDirect, LLC, Albertsons Companies, Inc., and Maplebear Inc. (Instacart). These companies compete across diverse fulfilment models, investing in last-mile delivery, dark stores, loyalty and subscription programmes, and AI-driven personalisation to strengthen their positions, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

North America is a highly developed online grocery market characterised by high convenience expectations, strong subscription adoption, and mature click-and-collect infrastructure. Within the region, the United States is the dominant market, where a combination of established retailer fulfilment networks, widespread membership programmes, and rapid-delivery entrants has driven deep penetration. US demand is anchored in full-basket weekly shopping complemented by a fast-growing layer of on-demand and top-up ordering, and the market continues to expand as fulfilment density improves and assortment widens across fresh and prepared categories.

Europe is a mature and competitive region with strong adoption in densely populated markets and a notable role for click-and-collect alongside home delivery. Consumer attention to product quality, freshness, and sustainability is pronounced, and operators differentiate through assortment, private-label strength, and environmentally conscious fulfilment. Penetration varies across the continent, leaving meaningful room for further growth in markets that are earlier on the adoption curve.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the most dynamic region and a primary engine of global growth. Large populations, rapid urbanisation, high smartphone penetration, and the swift uptake of digital payments have created fertile conditions for online grocery, particularly through app-based and rapid-delivery formats. The region has been a pioneer of quick commerce and hyper-local fulfilment, and the continued entry of first-time digital grocery buyers across its major economies positions it for sustained, high-rate expansion through the forecast period.

Latin America is an emerging, fast-growing market where rising connectivity, smartphone adoption, and digital-payment uptake are bringing new consumers into the category. Growth is concentrated in major urban centres, where delivery economics are most favourable, and the region presents significant headroom as fulfilment networks extend and consumer trust in digital grocery deepens.

The Middle East and Africa region is at an earlier stage of adoption but is expanding steadily, led by urban demand in higher-income markets and supported by growing digital infrastructure. Quick commerce and app-based ordering are gaining traction in dense urban centres, and the region offers long-term growth potential as connectivity, payments, and logistics capabilities mature.

The online grocery market faces a set of operational challenges that bear directly on profitability. Last-mile delivery remains the costliest and most complex part of the value chain, and serving fresh and perishable categories adds the burden of cold-chain integrity, careful handling, and tight delivery windows. Order accuracy, substitution management, and maintaining produce quality from pick to doorstep continue to test even well-resourced operators, and any failure on these fronts erodes the consumer trust on which repeat usage depends. Sustaining service quality while scaling into lower-density areas, where delivery economics are weaker, is a persistent challenge that defines the difference between platforms that scale profitably and those that do not.

Alongside these challenges sit structural restraints that temper the pace of expansion. Thin fulfilment margins and high delivery and infrastructure costs constrain profitability, and many operators continue to balance growth against the path to sustainable unit economics. Adoption is uneven across regions, held back in places by limited connectivity, lower digital-payment maturity, or entrenched preferences for in-store selection of fresh goods. Consumer sensitivity to delivery fees, minimum-order thresholds, and product freshness can suppress order frequency, while logistical limitations in rural and low-density markets restrict the geographic reach of the category. These restraints do not reverse the growth trajectory, but they shape where and how quickly it is realised.

The opportunities, however, are substantial and are what carry the market toward its forecast for 2035. Vast headroom remains in under-penetrated emerging markets, where rising connectivity, digital payments, and a young, urbanising population are bringing first-time digital grocery buyers into the category at scale. Subscription and membership models offer a clear route to higher retention and more predictable demand, while automation and AI-driven fulfilment promise the cost reductions needed to make delivery durably profitable. Quick commerce, private-label expansion, premium and specialty assortments, and the integration of grocery into broader retail and loyalty ecosystems each open new revenue streams. For retailers, investors, and new entrants weighing where to commit, the balance of manageable risk against sustained growth makes a detailed, evidence-based reading of this market essential, and the full report sets out that evidence in depth.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global online grocery market reached a value of USD 718.69 Billion in 2025, reflecting the channel’s shift from an occasional convenience to a mainstream way of buying everyday groceries across both developed and emerging markets.

The market is estimated to grow at a CAGR of 15.50% between 2026 and 2035.

The market stood at USD 718.69 Billion in 2025 and is projected to reach USD 3036.42 Billion by 2035, growing at a CAGR of 15.50% over the 2026 to 2035 forecast period.

Key drivers include durable shifts in consumer behaviour toward convenience, rising smartphone and digital-payment penetration, heavy investment in dark stores and cold-chain logistics, and intense competition that continually improves speed and assortment.

Major trends include quick commerce and hyper-local fulfilment, micro-fulfilment automation, AI-driven personalisation and routing, the blurring of online and in-store through click-and-collect, and a growing focus on sustainability.

The report covers North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, with Asia Pacific positioned as the fastest-growing region and North America among the most mature.

By platform, the market is split into web-based and app-based channels. By purchase type, it is divided into one-time and subscription purchases, with subscriptions playing a growing role in retention and predictable demand.

Different purchase types are one-time and subscription.

The market features established grocery retailers, large e-commerce platforms, and rapid-delivery specialists, with leadership in each geography shaped by fulfilment density, delivery speed, assortment, and the strength of loyalty and subscription programmes.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Platform |

|

| Breakup by Purchase Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.