Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

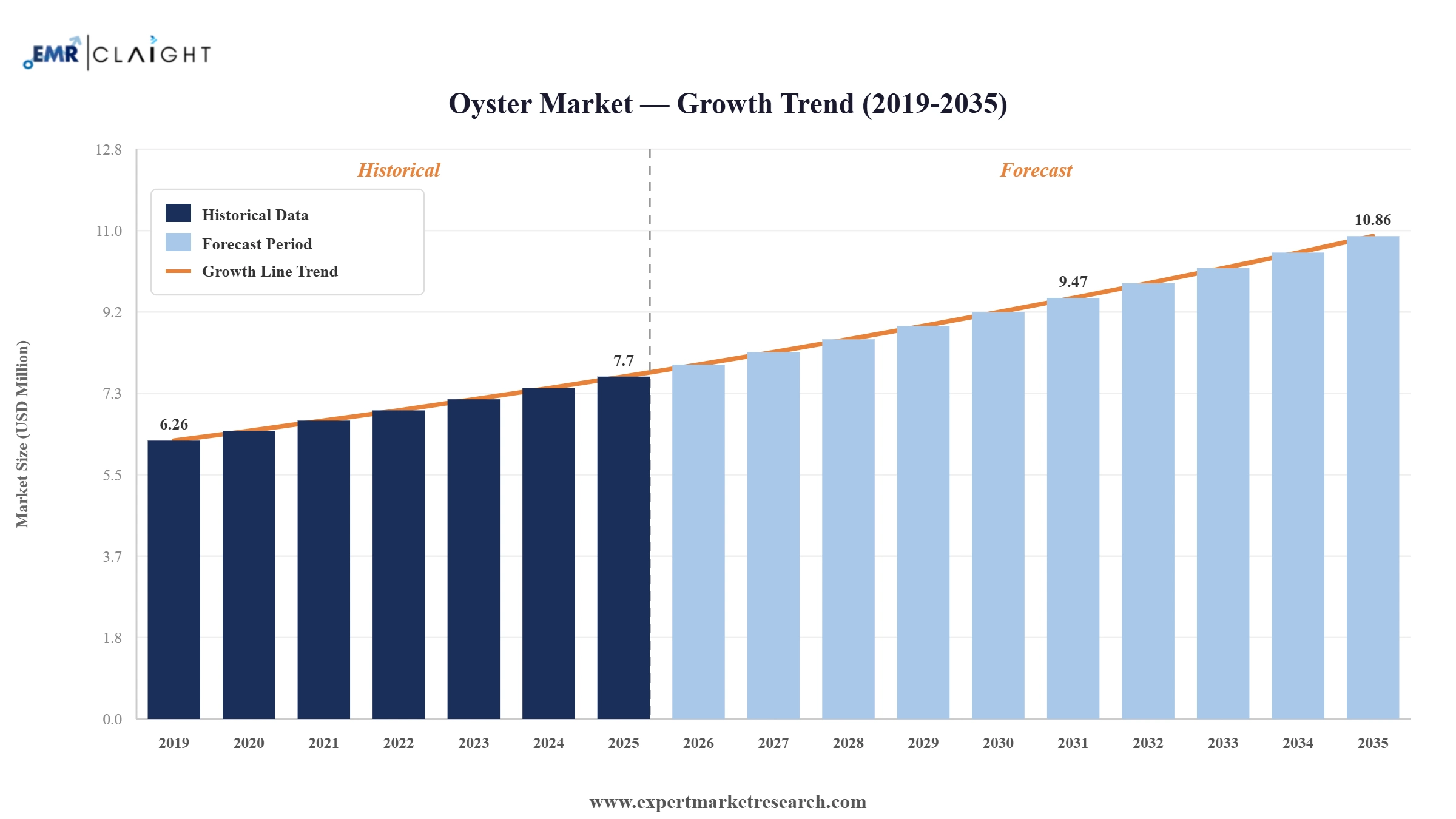

The oyster market was valued at USD 7.70 Million in 2025. The market is expected to grow at a CAGR of 3.50% during the forecast period of 2026-2035 to reach a value of USD 10.86 Million by 2035. Rising seafood consumption and increasing demand for premium aquaculture products are the key factors that are driving the overall growth in the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global oyster market is evolving from a commodity aquaculture product into a premium sustainable protein category with strong health positioning, e-commerce distribution reach, and direct-to-consumer branding. Asia Pacific remains the production and consumption centre of gravity, while North America and Europe are premiumising rapidly through artisan aquaculture, restaurant culture, and online distribution. Sustainability credentials are becoming a primary marketing and competitive differentiator, supported by oysters' unique environmental benefit in improving coastal water quality.

Industry data published in October 2025 confirmed Japan's oyster market is on a sustained growth trajectory, projected to expand from 174.9 thousand tonnes in 2024 to 226.2 thousand tonnes by 2033. Japan's growing preference for premium oysters as a domestic delicacy and restaurant dining staple makes it a key demand driver for global oyster market growth.

A significant hatchery expansion in Albany, Western Australia in September 2025 increased annual oyster spat output to over 40 million, easing supply shortages that had previously constrained new farm development. Taylor Shellfish Company's coordinated North American seed release schedules also supported consistent supply availability for growers across the Pacific Northwest.

NOAA Fisheries confirmed a significant increase in US coastal oyster aquaculture production in May 2025, particularly in the Mid-Atlantic and Pacific Northwest regions. This growth was driven by improved hatchery technology, expanded leasing programmes, and rising consumer demand for premium half-shell oysters, reinforcing the structural supply expansion in the global oyster market.

Reports published in February 2025 confirmed China's oyster import demand had weakened in 2024, creating commercial pressure for France and Ireland whose premium oyster export programmes depend significantly on Chinese premium restaurant and gifting markets. European producers accelerated diversification toward Japanese, Southeast Asian, and North American food service channels.

Oysters' unique environmental credentials, requiring no feed inputs and actively improving coastal water quality, are increasingly used as premium marketing differentiators in the global oyster market. Eco-certifications and sustainability-focused branding are driving 25 to 50% price premiums for certified oyster products in premium retail and food service channels.

E-commerce and direct-to-consumer shipping of live oysters is expanding market access beyond traditional restaurant and retail channels in the global oyster market growth trajectory. East 33 Deliveries in Australia and US-based producers are leveraging cold-chain shipping improvements to reach premium home consumption occasions previously inaccessible for live shellfish products.

Value-added oyster formats including smoked, marinated, and premium canned products are growing faster than fresh oyster categories in global distribution. These formats command 25 to 50% price premiums and are advancing strongly in specialty retail and e-commerce, broadening the global oyster market's consumer reach beyond raw half-shell enthusiasts.

Digital traceability solutions and selective breeding programmes are reshaping oyster producer strategies globally, improving operational efficiency and product quality assurance. Selective breeding initiatives at major hatcheries are increasing disease resistance and growth rates, reducing production costs while improving the consistency of premium-grade oyster output.

NOAA's 2025 data confirms North America's fastest oyster aquaculture growth concentrates in the Mid-Atlantic and Pacific Northwest, where established hatchery infrastructure, strong consumer demand, and supportive state leasing policies are enabling farm expansion. This growth is supporting premium half-shell oyster supply for both domestic restaurant markets and international export.

The Expert Market Research’s report titled “Oyster Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: Pacific Cupped Oyster (Crassostrea gigas) is the dominant oyster type globally, accounting for the majority of commercial aquaculture production across Asia Pacific, Europe, and North America due to its fast growth cycle, climate adaptability, and consumer familiarity. China's vast coastal aquaculture operations primarily cultivate Pacific Cupped Oysters, cementing this variety's market dominance. American Cupped Oyster (Crassostrea virginica) is commercially significant in the United States and is driving the premium half-shell restaurant culture in the East Coast oyster bar ecosystem. Penguin Wing Oyster is primarily cultivated for pearl production and represents a niche but commercially valuable specialty segment.

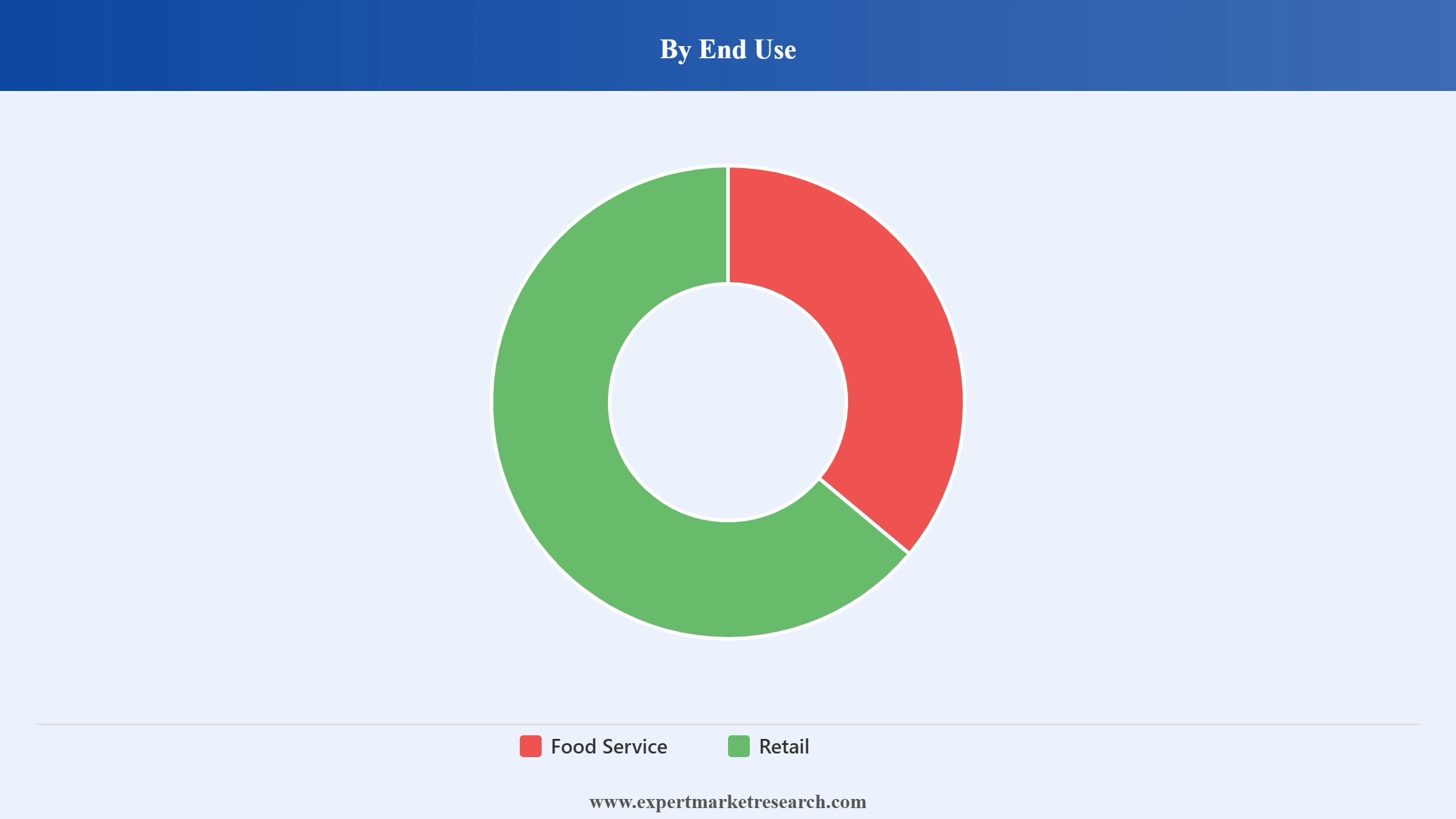

Market Breakup by End Use

Key Insight: Food service is the dominant end-use segment for oysters globally, driven by the premium oyster bar culture in North America and Europe and the oyster restaurant dining tradition in Japan, France, and Australia. Food service enables premium price realisation through half-shell presentation, wine pairing experiences, and the restaurant storytelling around oyster provenance that commands significant consumer willingness to pay. Retail is a growing end-use segment, with supermarkets, specialty seafood outlets, and online platforms expanding access to fresh, frozen, and value-added oyster products for home consumption occasions.

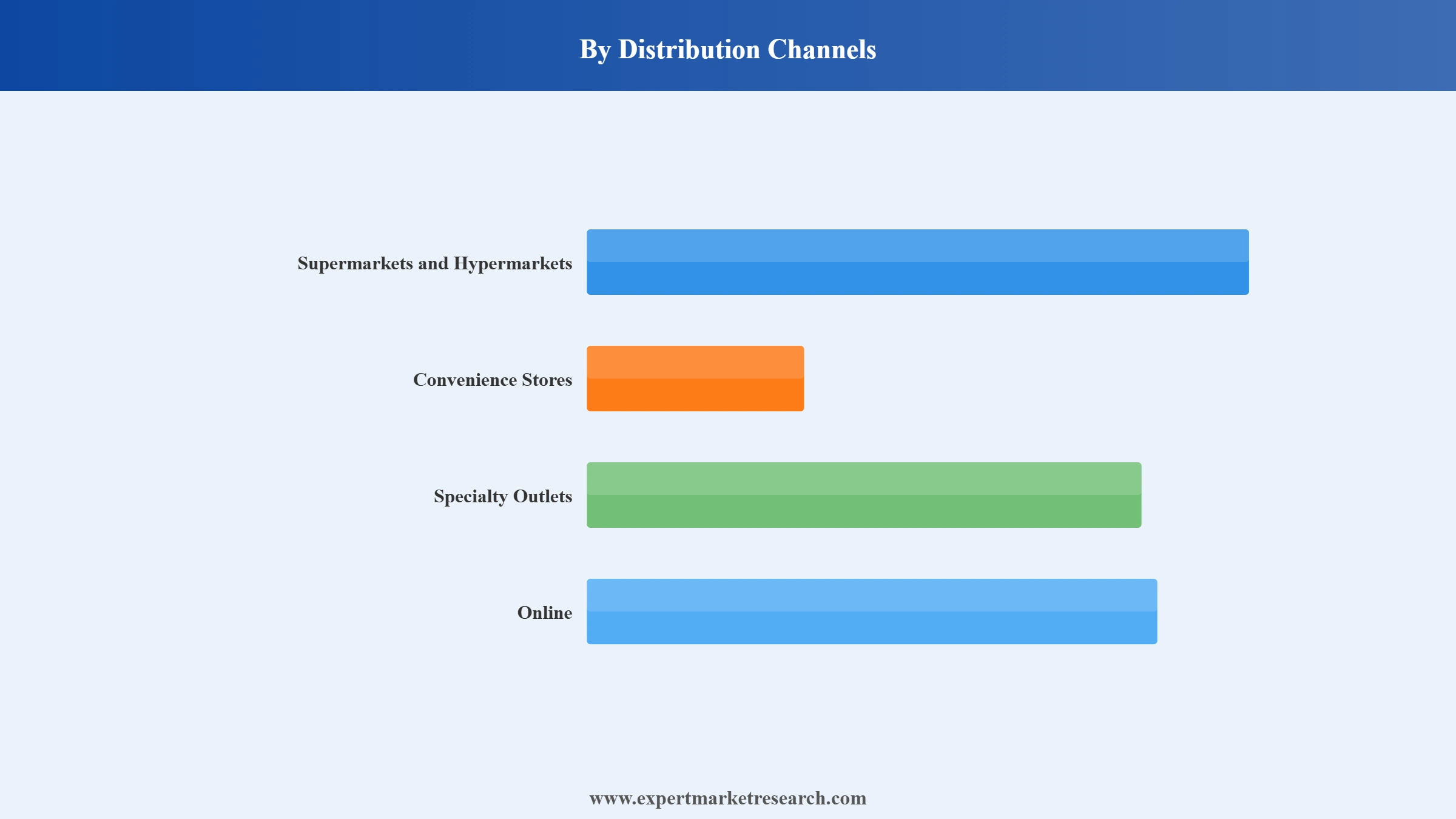

Market Breakup by Distribution Channels

Key Insight: Specialty outlets are the most commercially significant distribution channel for premium oysters globally, encompassing specialist seafood retailers, fishmongers, farmers markets, and premium delicatessens that maintain the cold-chain integrity and product knowledge required to sell live and fresh oysters effectively. Online channels are the fastest-growing distribution segment, driven by improved cold-chain logistics and direct-to-consumer business models adopted by artisan oyster producers in the United States, Australia, and Europe. Supermarkets and hypermarkets are important for processed, canned, and frozen oyster formats that suit self-service purchasing.

Market Breakup by Region

Key Insight: Asia Pacific dominates the global oyster market, commanding approximately 94.9% of global production volume in 2025, anchored by China's vast commercial oyster farming operations along the Fujian, Guangdong, and Shandong coastlines. Japan, South Korea, Vietnam, and Australia are the other significant Asia Pacific producers. Europe is the premium-quality oyster production leader, with France's Marennes-Oleron and Brittany regions producing the world's most sought-after fine de claire and Belon varieties that command exceptional price premiums in global restaurant markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, pacific cupped oyster dominates the market due to commercial aquaculture efficiency and global adaptability

Pacific cupped oyster accounts for the dominant share of global oyster production and commercial aquaculture, driven by its exceptional growth rate, tolerance of a wide range of water temperatures and salinities, and broad consumer acceptance across Asian, European, and North American markets. China's oyster industry, which accounts for the vast majority of global oyster volume, overwhelmingly cultivates Pacific cupped oysters using large-scale longline and raft aquaculture systems. France introduced Pacific cupped oysters in the 1970s following a disease that devastated native flat oyster populations, and Crassostrea gigas now represents approximately 90% of French oyster production and the majority of European commercial output.

American cupped oyster (Crassostrea virginica) is the second most commercially significant oyster type, representing the backbone of the United States East Coast oyster industry. The East Coast's premium half-shell restaurant culture has elevated the American cupped oyster into a high-value artisan product with strong regional identity, with producers in Virginia, Maryland, Massachusetts, and Maine commanding premium prices based on distinct flavour profiles derived from local growing conditions. The East Coast oyster revival has attracted significant investment in new farms, hatcheries, and cold-chain logistics infrastructure through 2025.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, food service accounts for the dominant share due to premium restaurant culture and high value-per-unit realisation

Food service commands the largest share of global oyster end-use revenue, reflecting the premium experience context in which oysters are most effectively marketed and consumed. The raw half-shell oyster bar format in North America and Europe, the oyster as restaurant luxury appetiser in France and Japan, and the oyster hot pot tradition in East Asia all reflect distinct cultural consumption occasions that sustain strong food service demand. Food service channels enable premium prices that significantly exceed retail equivalents, making restaurant distribution the primary commercial priority for premium artisan oyster producers in the global oyster market.

Retail is a growing end-use channel within the global oyster market, expanding through multiple distribution sub-channels. Specialty seafood outlets maintain the cold-chain quality and product knowledge required to sell live oysters at retail, while supermarkets and hypermarkets focus on processed, frozen, smoked, and canned oyster formats that are more accessible for self-service purchase. Online direct-to-consumer retail is the fastest-growing retail sub-channel, with producers like East 33 Deliveries, Hog Island Oyster, and Taylor Shellfish Farms all leveraging improved cold-chain shipping to deliver premium live oysters to residential customers within their respective regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channels, specialty outlets account for the dominant share due to cold-chain and product knowledge requirements for premium live oysters

Specialty outlets represent the most important distribution channel for premium fresh and live oysters in the global oyster market, providing the temperature-controlled storage, rapid turnover, and seafood expertise required to maintain oyster quality and consumer confidence. Specialist fishmongers, premium seafood markets, and delicatessens in Europe and North America serve as the primary retail touchpoints for premium oyster varieties where provenance, species, and growing conditions are central purchasing considerations. France's direct oyster producer sales through regional markets in Brittany and Charente-Maritime exemplify how specialty distribution sustains premium pricing for artisan producers.

Online channels are the fastest-growing distribution segment in the global oyster market, driven by the expansion of cold-chain express delivery capabilities and the growing consumer demand for home consumption of premium seafood. Direct-to-consumer shipping by producers enables farmers to bypass traditional wholesale and retail intermediaries, improving margin retention while building direct relationships with premium consumers. East 33 Deliveries in Australia and US East Coast producers are at the forefront of this distribution model shift, using e-commerce platforms to scale revenue beyond local restaurant markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the global oyster market due to China's unmatched commercial aquaculture scale and production volume

Asia Pacific commands approximately 94.9% of global oyster production volume in 2025, with China's extensive coastal aquaculture operations representing the overwhelming majority of this share. China's Fujian, Guangdong, and Shandong provinces host the world's densest oyster aquaculture infrastructure, leveraging warm coastal waters, favourable tidal conditions, and established supply chains linking farms to domestic wet markets, food processors, and export packaging facilities. Japan's oyster market is on a steady growth trajectory from 174.9 thousand tonnes in 2024 toward 226.2 thousand tonnes by 2033, supported by growing domestic premium consumption.

North America is the fastest-growing premium oyster market in terms of value per unit, driven by the artisan aquaculture movement that has transformed the US East Coast and Pacific Northwest into recognised premium oyster production regions. NOAA Fisheries confirmed significant aquaculture production increases in 2025, particularly across Maryland, Virginia, Massachusetts, and Washington State, supported by improved hatchery technology and strong fine dining and direct-to-consumer demand. Europe maintains its premium production leadership through France's historic oyster appellations and Ireland's Atlantic-influenced oysters, both commanding exceptional price premiums in global restaurant export markets. The Australia and New Zealand hatchery expansion in 2025 also supports long-term supply growth for the Asia Pacific premium segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global oyster market is highly fragmented, with thousands of small and medium-sized aquaculture producers operating alongside a smaller number of commercially scaled producers with multi-farm operations and distribution networks. Taylor Shellfish Farms and Hog Island Oyster Co. are among the most commercially visible premium US producers, while France's Naissain producers and Ireland's Woodstown Bay Shellfish represent European premium supply. East 33 Deliveries in Australia is a notable innovator in direct-to-consumer oyster logistics.

Competition is primarily based on oyster quality, brand provenance storytelling, cold-chain logistics capability, and distribution channel access. The premium segment is increasingly characterised by direct-to-consumer relationships, restaurant exclusivity agreements, and sustainability certification that enable producers to capture higher retail and foodservice prices. The growing value-added product market for smoked, canned, and marinated oyster formats is attracting new commercial entrants seeking to capture premium margins from processed oyster categories in the global oyster market.

Taylor Shellfish Farms is a family-owned aquaculture company founded in 1890 and headquartered in Shelton, Washington, USA. The company is the largest producer of farmed shellfish in the United States, farming oysters, clams, mussels, and geoduck across multiple coastal sites in Washington State and British Columbia. Taylor Shellfish's coordinated seed supply and scheduled spat releases support consistent product availability for growers across the Pacific Northwest region. The company also operates retail oyster bars in Seattle and other Pacific Northwest locations, leveraging its production scale to deliver vertically integrated premium consumer experiences.

Hog Island Oyster Co. was founded in 1983 and is based in Marshall, California. The company farms oysters in Tomales Bay, California, producing premium Pacific and Atlantic oyster varieties under its Sweetwater and Tomales Bay Oyster brands. Hog Island is well known for its sustainable aquaculture practices, farm-to-table ethos, and premium restaurant supply operations across the San Francisco Bay Area and broader California market. The company operates oyster bars at its Marshall farm and at venues in San Francisco and Napa, creating strong direct consumer connections in the global oyster market's premium US segment.

France Naissain and Vendée Naissain are French oyster hatchery organisations supplying oyster spat (juvenile oysters) to farmers across France and European export markets. Located in the Vendée region of western France, these hatcheries are essential infrastructure for France's large commercial oyster farming industry, which produces approximately 90% of its output from Pacific cupped oysters descended from hatchery-reared spat. France's oyster industry exports significant volumes of premium cupped and flat oysters to global restaurant markets and premium retail channels.

East 33 Deliveries Pty Ltd is an Australian oyster producer and distribution company specialising in premium Pacific oysters farmed along Australia's New South Wales coastline. The company is a notable innovator in direct-to-consumer cold-chain oyster delivery, shipping premium live oysters to restaurants and residential customers across Australia and selected export markets. East 33's focus on transparency, provenance, and premium product quality positions it as a leading participant in the global oyster market's fastest-growing direct-to-consumer distribution segment.

Other key players in the market are Ward Oyster Company, Cape Cod Oyster Company, Chatham Shellfish Company, France Naissain and Vendée Naissain, Woodstown Bay Shellfish Ltd., Colville Bay Oyster Co. Ltd., Hoopers Island Oyster Company, Five Star Shellfish Inc., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the global oyster market 2026 with our comprehensive report. Stay ahead with valuable data on aquaculture production trends, premium consumer demand dynamics, and sustainability-driven market growth. Whether you're an oyster producer, seafood distributor, or food service investor, this report gives you the clarity you need. Download your free sample now and discover key opportunities in the global thriving oyster industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 3.50% between 2026 and 2035.

The major market drivers are the growing urban population along with the growing demand for seafood.

The key market trends include the increasing disposable income among people, growing number of health-conscious consumers, and rising popularity of dishes made with oysters.

The various types of oysters in the market include cupped oyster, Pacific cupped oyster, American cupped oyster, and Penguin wing oyster, among others.

The primary end uses in the market for oysters include food service and retail.

The different distribution channels in the market for oysters include supermarkets and hypermarkets, convenience stores, specialty outlets, and online, among others.

The major players in the global oyster market are Ward Oyster Company, Cape Cod Oyster Company, Chatham Shellfish Company, Taylor Shellfish Farms, France Naissain and Vendée Naissain, Woodstown Bay Shellfish Ltd., East 33 Deliveries Pty Ltd, Hog Island Oyster Co., Colville Bay Oyster Co. Ltd., Hoopers Island Oyster Company, and Five Star Shellfish Inc., among others.

In 2025, the oyster market reached an approximate value of USD 7.70 Million.

The market is expected to witness steady growth during the forecast period of 2026-2035 to reach a value of USD 10.86 Million by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channels |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.