Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

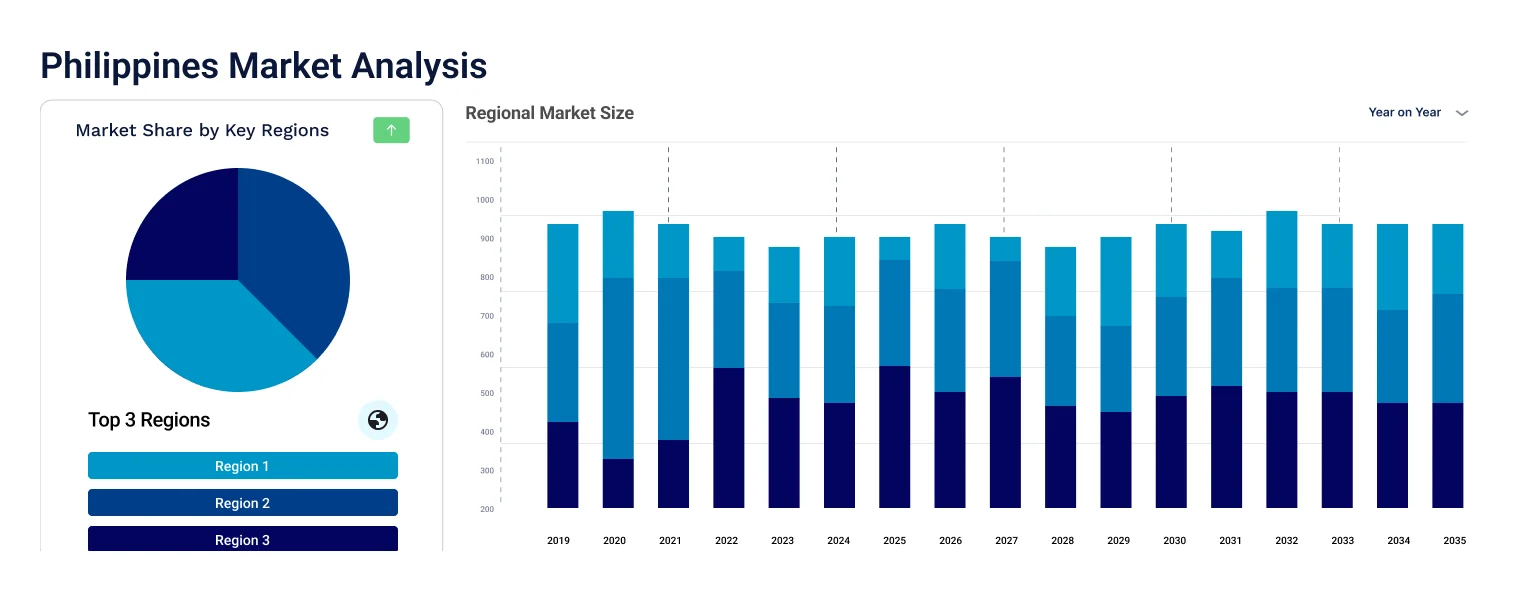

The Philippines clinical diagnostics market was valued at USD 417.54 Million in 2025 and is expected to grow at a CAGR of 7.20%, reaching USD 836.85 Million by 2035. The market growth is driven by rising demand for routine health screenings and advanced diagnostic technologies.

Compound Annual Growth Rate

7.2%

Value in USD Million

2026-2035

Read more about this report - Request a Free Sample

Clinical diagnostics are applied across multiple healthcare domains including infectious disease testing, complete blood count tests, along with liver and renal panels. The rising prevalence of chronic diseases in Philippines has elevated the demand for clinical diagnostics drastically. Being one of the most dynamic economies in the East Asia and Pacific region, Philippines has been witnessing rapid urbanization and an influx of investments to improve the medical sector, bolstering the market growth.

Philippines clinical diagnostics market demand is driven by the increasing improvements and adoption of modern technologies to offer better services to the patients. Philippines laboratories are increasingly adopting automated and digital solutions to streamline workflows and enhance accuracy of results. In addition, rising awareness on early disease detection and implementation of numerous screening programs by public as well as private institutions is expected to drive the market growth in the forecast period.

Investments in Infrastructure Improvement to Drive the Philippines Clinical Diagnostics Market Growth

In March 2023, the Philippines administration approved 123 new infrastructure projects worth USD 163 billion. The major investment was made to enhance the research and medical infrastructure in the country, which specific emphasis on building digital connectivity and facilitating remote consultations and services across the country. It is bound to initiate multiple public-private partnerships and boost the overall economic landscape of the region.

The Philippines clinical diagnostic market share is expected to increase by increasing integration of cutting-edge technologies. In September 2023, the Consul-General of Japan and Surigao city mayor signed an agreement to grant PHP 3.5 million (USD 62k) to establish mobile x-ray system in one of the city hospitals. The investment is a testament to rising government initiatives poised at enhancing the infrastructure and making quality services available at an affordable price.

Rising Prevalence for Artificial Intelligence

In August 2023, Japan International Cooperation Agency (JICA) and the Philippines Department of Health (DOH) collaborated to bring artificial intelligence (AI) Computer Aided Detection (CAD) to allow early tuberculosis diagnosis, and eventually help in disease prevention. The latest technology, when applied on 400 suspected tuberculosis patients, led to successful diagnosis in 382 patients, implying its efficacy to analyze infectious diseases. The technology is expected to be used in the detection of other diseases as well, solidifying artificial intelligence integration, which is one of the major Philippines clinical diagnostic market trends.

Using Advanced Solutions for Better Patient Outcomes

Over the years, the incidence of cardiovascular diseases and cancer has significantly seen an upswing. Lung, breast, colon, rectum, and prostate cancers are some of the most commonly occurring cancers, affecting around 189 in 100,000 Filipinos. As a result, the demand for improved clinical diagnostics has risen. Focused on providing improved solutions to the patients, the healthcare providers and professionals have been continuously working to upscale their services. For instance, the Manila Doctors Hospital (MDH) has adopted several quality services to enhance the quality of services. With a new cancer institute and cardiovascular center, equipped with cardiac catheterization laboratory (cath lab), coronary care unit, cardiac rehab, and heart care services, the hospital has been accredited for medical tourism as well.

Philippines Clinical Diagnostics Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Test

Market Breakup by Product

Market Breakup by End User

Read more about this report - Request a Free Sample

The market growth can be attributed to an influx of investments from government, non-profit organizations as well as international healthcare companies. With easy availability of resources and academic talent, major MedTech companies are setting up new research facilities in the region, which is poised to boost the Philippines clinical diagnostics market growth in the forecast period. In addition, the growing incidence of geriatric population and a heightened focus on preventing infectious diseases is a notable market driver. In addition, other regions such as Baguio City and Central Luzon are also witnessing expedited market growth, owing to increasing infrastructure improvements.

In February 2023, Siemens Healthineers and Unilabs announced EUR 200 million worth collaboration, wherein Unilabs acquired around 400 laboratory analysers to improve their infrastructure and facilitate improved diagnostic services to the consumers. The market has been witnessing a significant boost in merger related activities, with several companies pushing their boundaries to expand their product portfolios. Heightened focus on sustainability and making high-end technology accessible and affordable is a major market trend being adopted by key companies.

The key features of the Philippines clinical diagnostics market report include patent analysis, grants analysis, clinical trials analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players. The major companies in the market are as follows:

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Upto 15% Off

USD

$3099 $2789

$1999 $1799

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is anticipated to grow at a CAGR of 7.20% during the forecast period of 2026-2035, driven by increasing healthcare and research associated investments along with growing prevalence of infectious diseases across the region.

The market demand is driven by the rising emphasis on preventing infectious and fatal chronic diseases via early detection. The increasing integration of modern technologies, such as artificial intelligence and mobile systems, in clinical diagnostics is also fuelling the market demand.

The rising investments focused on improving the healthcare infrastructure is a major market trend. In September 2023, the Consul-General of Japan and Surigao city mayor signed an agreement to grant PHP 3.5 million (USD 62k) to establish mobile x-ray system in one of the city hospitals. Moreover, the government also sanctioned 123 new infrastructure projects worth USD 163 billion.

Based on test, the market is divided into lipid panel, liver panel, renal panel, complete blood count, electrolyte testing, and infectious disease testing, among other tests.

Instruments and reagents, among others are the common technologies available in the market.

Major end users include hospital laboratory, diagnostic laboratory, point of care testing, and others.

Key players involved in the market are Abbott, ARUP Laboratories, OPKO Health, Inc., Bioscientia Healthcare GmbH, Charles River Laboratories, NeoGenomics Laboratories, Genoptix, Inc., Healthscope, The Laboratory Glassware Co., Laboratory Corporation of America Holdings, Fresenius Medical Care AG, and Co. KGaA, QIAGEN, Quest Diagnostics Incorporated, Siemens Healthcare Private Limited, and Tulip Diagnostics (P) Ltd.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Test |

|

| Breakup by Product |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.