Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

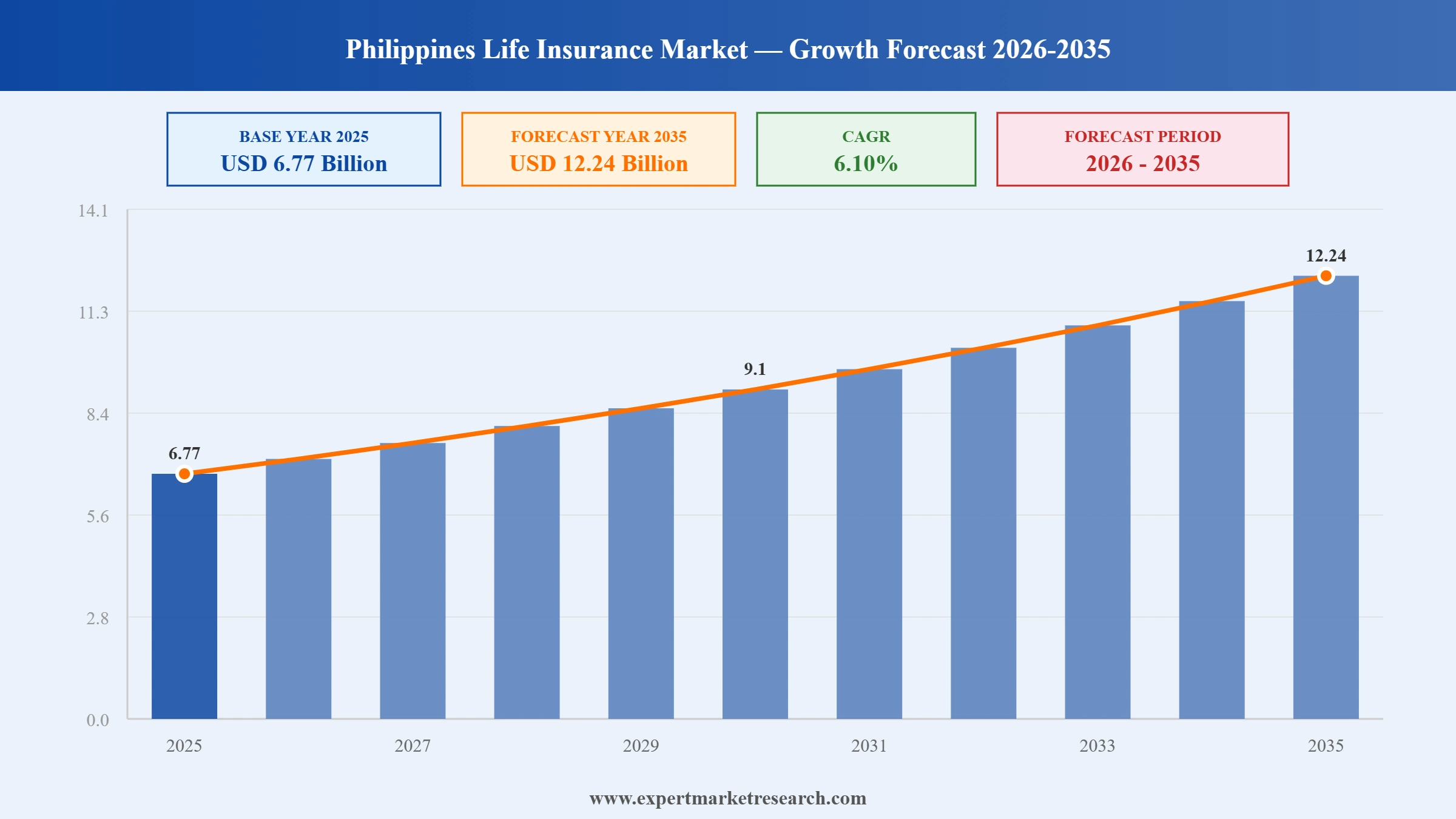

The Philippines Life Insurance Market reached a value of USD 6.77 Billion at 2025 and is projected to expand at a CAGR of around 6.10% during the forecast period of 2026-2035. With rising financial literacy driving demand for individual life policies, the rapid expansion of bancassurance and digital channels broadening market reach, growing adoption of investment-linked and ESG-focused products among younger Filipinos, and the government's continued push for OFW protection coverage, the market is expected to reach USD 12.24 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Life Insurance Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

6.77 |

|

Market Size 2035 |

USD Billion |

12.24 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

6.10% |

|

CAGR 2026-2035 - Market by Demographic |

Adults |

6.5% |

|

CAGR 2026-2035 - Market by Distribution Channel |

Direct Sales |

7.2% |

The key trends of the Philippines life insurance market include digital innovations, microinsurance growth, personalized products, and health integration.

The Philippines life insurance sector posted a landmark performance in 2025, with total life insurance premium income reaching PHP 403.21 billion, a 14.54% year-on-year increase from PHP 352.02 billion in 2024, according to data from the Insurance Commission. Life insurance retained its dominant position, accounting for 80.77% of the total PHP 499.23 billion in combined industry premiums. Sun Life Philippines led by total assets at PHP 344.49 billion, followed by AIA Philippines at PHP 251.49 billion, with Pru Life UK topping new business annual premium equivalent rankings at PHP 10.05 billion. The results confirm that demand for life coverage among Filipino households is accelerating ahead of broader economic growth, with net income across the sector also rising sharply.

Singlife Philippines launched new mobile payment capabilities in September 2025, including annual premium payment options with potential savings and QR code-based transaction support, significantly enhancing the accessibility and convenience of its digital insurance platform for Filipino policyholders. The launch reflects the growing emphasis on frictionless digital experiences in the Philippines life insurance market, where consumers increasingly expect the same level of transactional convenience they receive from banking and e-commerce platforms. Singlife's mobile-first strategy aligns with broader industry shifts as insurers compete to reduce payment friction and improve premium collection efficiency in an increasingly digital consumer environment.

FWD Life Philippines achieved a significant milestone in 2025, ascending to third place in the new business annual premium equivalent (NBAPE) rankings with PHP 9.03 billion, a sharp improvement from its fourth-place standing in 2024 at PHP 7.74 billion. FWD Life's rapid advance reflects the competitive strength of its digital-first approach to life insurance distribution, including its Tapp mobile application that allows policyholders to manage their coverage, make payments, and file claims entirely through a smartphone interface. The insurer's consistent investment in simplified product design and user-friendly digital tools has successfully attracted a younger, tech-savvy consumer base in the Philippines, making FWD one of the fastest-growing life insurance companies in the market.

Pru Life UK maintained its leading position in the Philippines' new business annual premium equivalent (NBAPE) rankings in 2024 with PHP 9.83 billion, sustaining its competitive advantage over Sun Life Philippines at PHP 8.96 billion. Pru Life UK's continued leadership reflects the enduring appeal of its investment-linked life insurance products, which combine savings and protection components into flexible, customizable policies suited to Filipino consumers seeking both financial security and capital growth. The company's sustained investment in agent training, digital tools for advisors, and product innovation across health, term, and unit-linked categories reinforces its long-term competitive positioning in the Philippines market.

The Insurance Commission of the Philippines confirmed in early 2024 that insurance penetration was improving progressively, supported in part by regulatory mandates and government-backed programs extending life insurance coverage to Overseas Filipino Workers (OFWs) across key labor markets. This initiative aimed to bridge the coverage gap for the approximately 10 million OFWs who face elevated personal and financial risks working abroad, many of whom had previously lacked structured insurance protection. The expanded coverage mandate contributed to new policy issuances across both individual and group segments, supporting premium income growth that outpaced GDP growth and helping push overall industry penetration from 1.67% in 2024 toward the 2% target.

Digital technology has become the central battleground for competitive differentiation in the Philippines life insurance market, with leading insurers investing heavily in AI-driven underwriting, mobile policy management platforms, and data analytics capabilities to improve both customer acquisition and retention. The Insurance Commission's data showing a 14.54% premium income growth in 2025 reflects, in part, the efficiency gains that digital distribution has delivered, particularly in reaching consumers who would previously have had no easy access to insurance agents. FWD Life's Tapp mobile application, which allows end-to-end policy management including claims filing, exemplifies how digital-first platforms are reshaping consumer expectations. In September 2025, Singlife Philippines extended this trend further by introducing QR-based premium payment features, making ongoing policy maintenance simpler and more convenient for its policyholders.

Bancassurance has emerged as one of the most effective channels for broadening life insurance penetration in the Philippines, as insurers leverage the extensive branch networks and established customer trust of Philippine banks to distribute life policies at scale. Key partnerships include AIA Philippines with the Bank of the Philippine Islands (BPI-AIA), BDO Unibank through BDO Life, and Allianz PNB Life's longstanding tie-up with Philippine National Bank. These arrangements give insurance products visibility in banking environments where millions of Filipinos regularly transact, creating natural cross-selling opportunities among consumers who are already engaged with financial services. Sun Life Philippines was the largest life insurer by assets in 2025 at PHP 344.49 billion, reflecting the effectiveness of its multi-channel strategy that combines dedicated advisors, online platforms, and bancassurance partnerships to sustain premium growth.

Microinsurance is gaining meaningful ground in the Philippines as both commercial insurers and non-profit mutual benefit associations develop affordable, low-premium life products targeted at informal workers, farmers, fisherfolk, and gig economy participants who have traditionally been excluded from mainstream insurance. The gig economy and self-employed population represent one of the most significant untapped segments for the Philippines life insurance market, given the absence of employer-sponsored group coverage for this growing labor cohort. The Insurance Commission's financial inclusion programs have supported product approvals for simplified microinsurance products, and several InsurTech firms are partnering with cooperatives and microfinance institutions to distribute these policies through digital channels. Out-of-pocket health expenses constituted 44.4% of total health spending in the Philippines in 2023 according to the Philippine Statistics Authority, a figure that powerfully illustrates the protection gap that microinsurance is working to address.

Investment-linked life insurance policies that incorporate environmental, social, and governance (ESG) criteria are gaining traction among younger Filipino consumers who want their financial planning to reflect their values. These products combine life coverage with investment components channeled into ESG-screened fund portfolios, appealing to millennials and Gen Z professionals who are increasingly interested in sustainable finance. Leading insurers including Sun Life Philippines, Pru Life UK, and AXA Philippines have expanded their investment-linked product ranges to include ESG fund options, responding to growing demand for policies that deliver both financial protection and impact-aligned investment returns. The broad adoption of variable unit-linked insurance plans in the Philippines, which allow policyholders to direct premium savings into equity and fixed-income funds, provides a natural platform for embedding ESG options without requiring entirely new policy structures.

The EMR’s report titled “Philippines Life Insurance Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

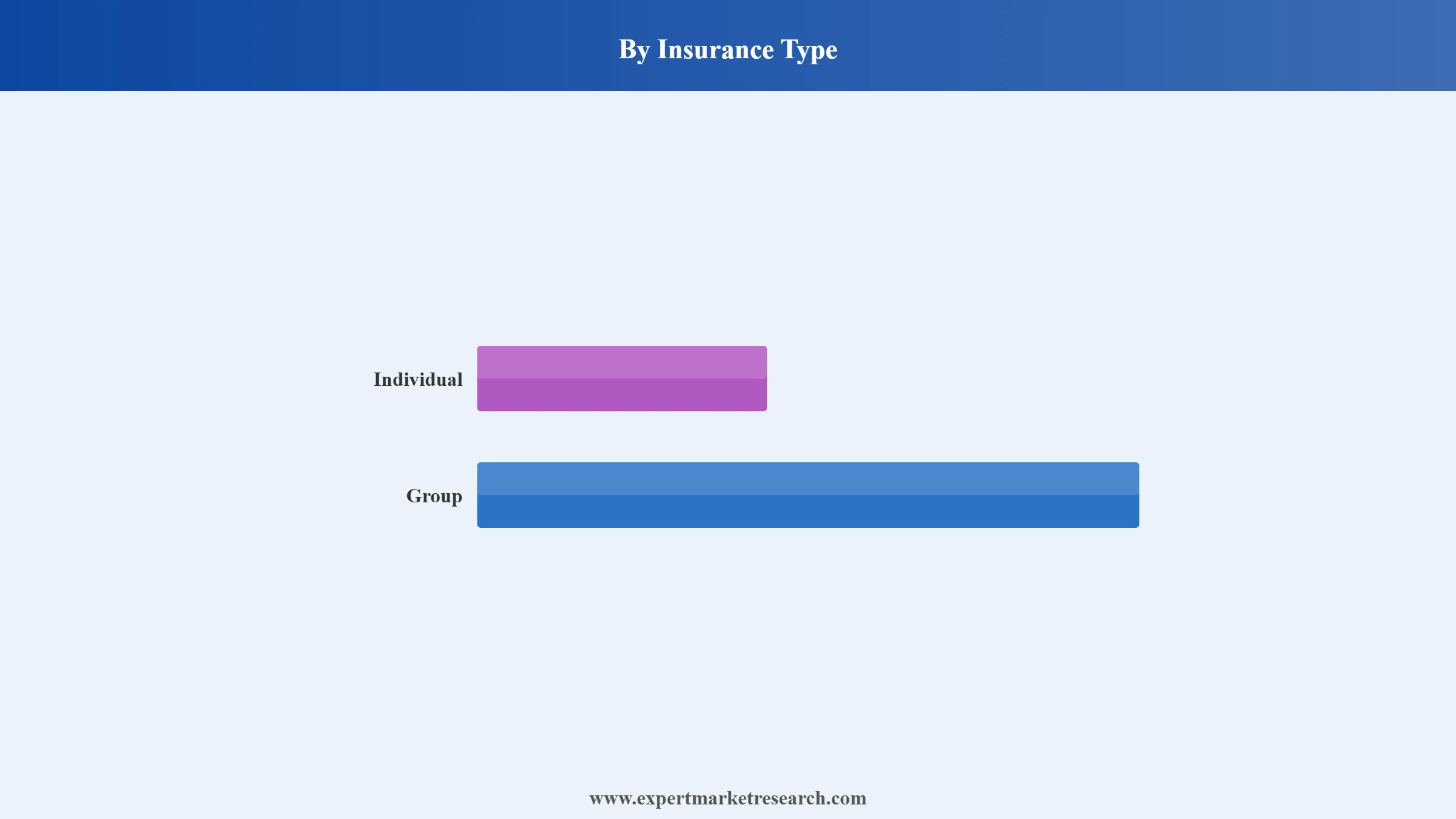

Market Breakup by Insurance Type

Key Insight: Individual life insurance policies dominate the Philippines life insurance market by premium volume, reflecting the country's growing culture of personal financial planning and the widespread adoption of investment-linked policies among working-age Filipinos. Variable unit-linked (VUL) plans, which combine life coverage with equity fund investments, are particularly popular among middle-class consumers seeking dual protection and wealth-building benefits. Term life insurance is gaining appeal among cost-conscious buyers and younger first-time policyholders who prioritize affordable pure protection without an investment component. Group life insurance, while smaller in overall premium share, is growing through employer benefit packages, cooperative group plans, and microinsurance programs targeting informal workers and OFW communities. Pru Life UK's PHP 10.05 billion new business annual premium equivalent in 2025 underscores the strong individual policy demand sustained by its advisor network and product portfolio.

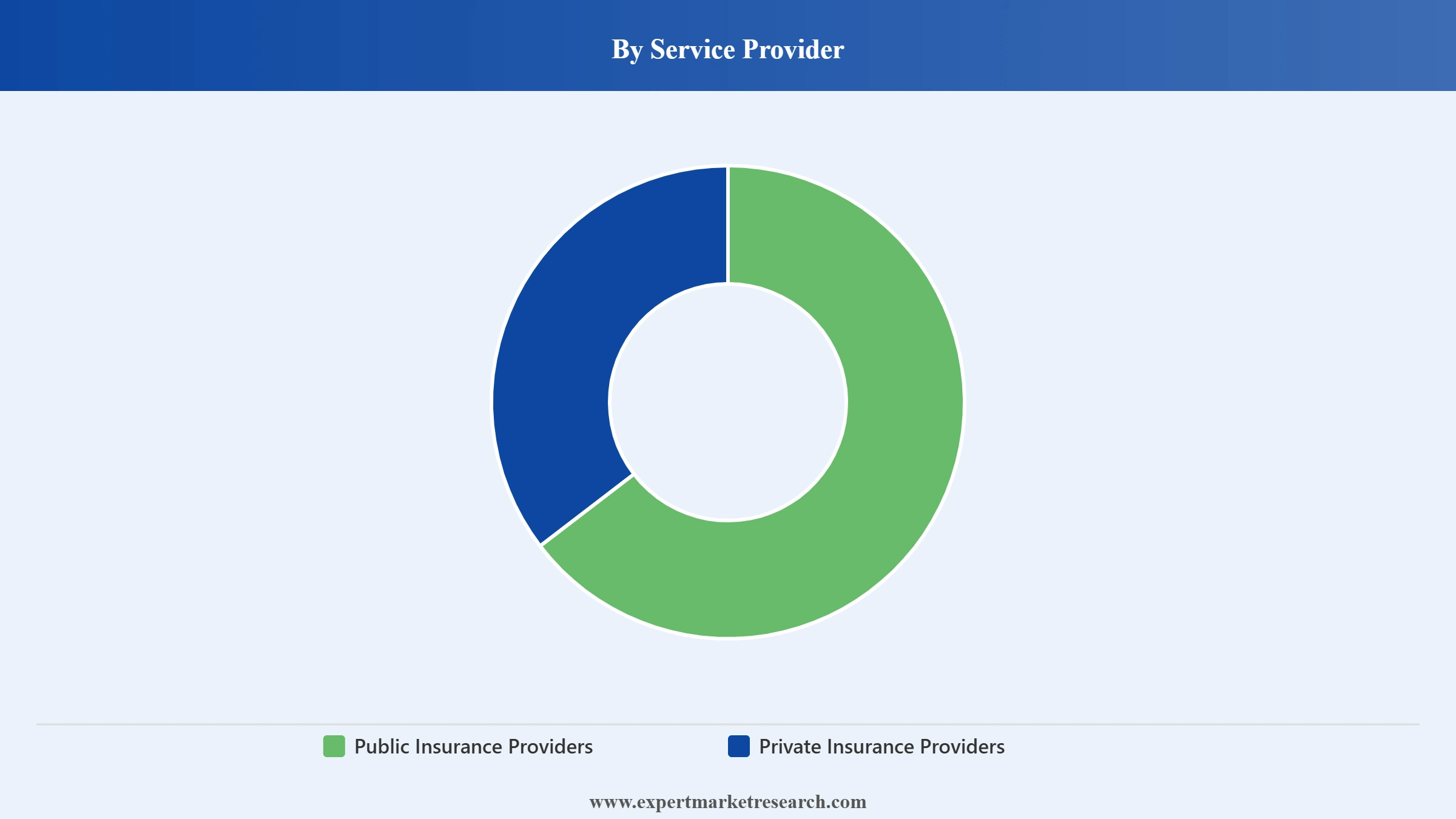

Market Breakup by Service Provider

Key Insight: Private insurance providers dominate the Philippines life insurance market, accounting for the significant majority of premium income across individual and group segments. The market's top performers by premium and new business metrics - including Pru Life UK, FWD Life, Sun Life Philippines, AXA Philippines, and Allianz PNB Life - are all private entities operating with international backing. Public insurance providers, including government-sponsored programs under the Social Security System (SSS) and the Government Service Insurance System (GSIS), provide baseline life cover and retirement benefits for formal sector workers, but their premium and coverage scope is structurally distinct from the commercial market. The private sector's competitive intensity drives product innovation, digital investment, and distribution network expansion, while public providers anchor the social protection floor for employed Filipinos in both public and private sectors.

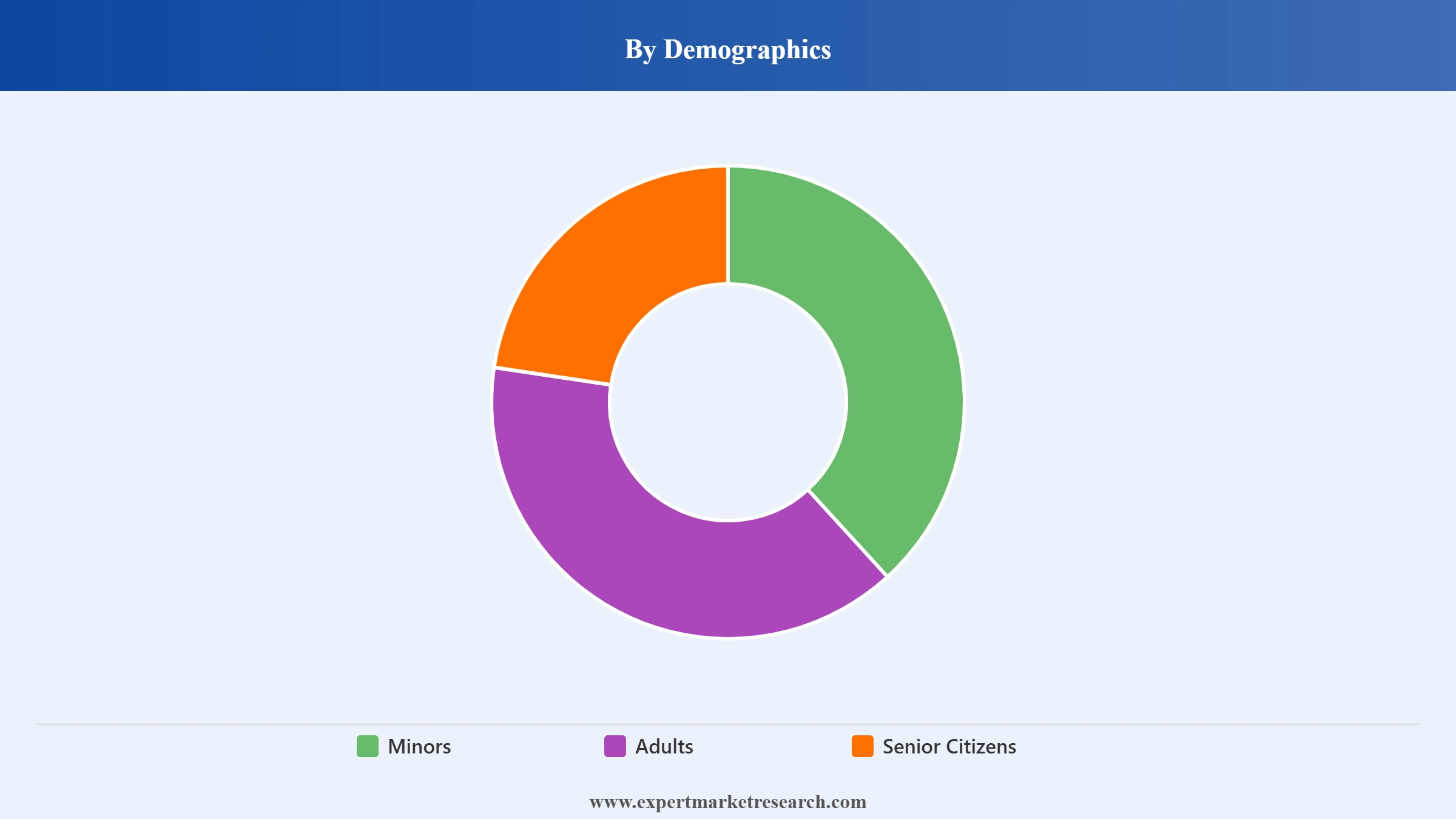

Market Breakup by Demographics

Key Insight: Adults constitute the largest demographic segment in the Philippines life insurance market, driven by working-age consumers seeking protection, investment-linked savings, and retirement planning products. The adults segment is projected to expand at a CAGR of 6.5% over the forecast period, reflecting rising financial literacy and improving wage levels among the country's growing professional class. Policies for minors represent a fast-growing niche, with parents increasingly seeking early-stage education savings plans and juvenile life policies that lock in lower premium rates and provide long-term financial foundations for their children. Senior citizens are an emerging segment as life expectancy improves and concerns around healthcare costs and retirement income security grow, with insurers developing targeted products including long-term care coverage and retirement annuities for this cohort.

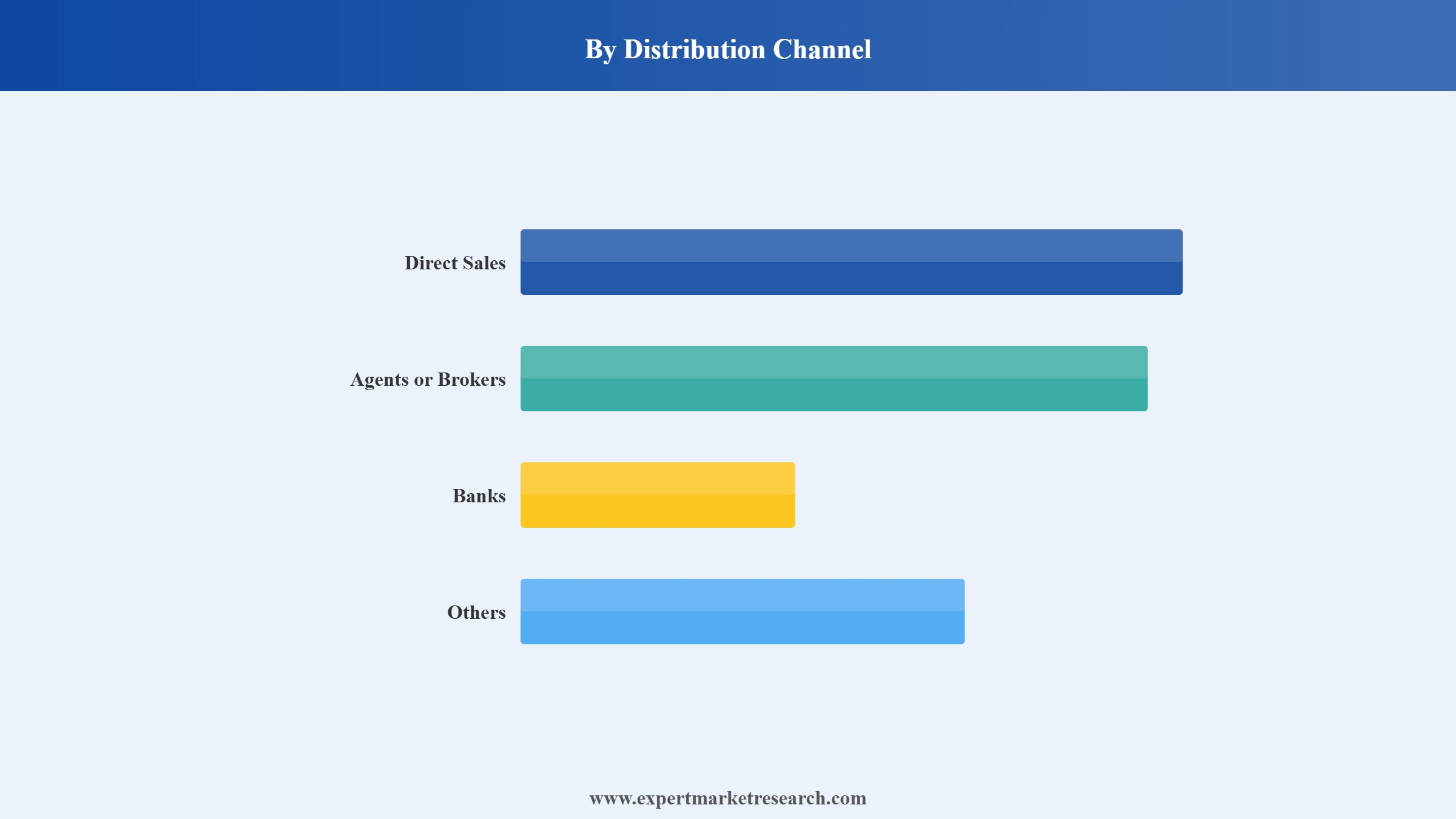

Market Breakup by Distribution Channel

Key Insight: Agents or Brokers remain the dominant distribution channel for life insurance in the Philippines, owing to the complexity of product comparisons, the trust-dependent nature of insurance purchases, and the preference among Filipino consumers for face-to-face financial guidance from professional advisors. Leading insurers including Pru Life UK, Sun Life Philippines, and AXA Philippines each maintain large, well-trained agent networks as their primary growth engines. Banks represent the fastest-growing channel through bancassurance arrangements that embed life insurance product offerings within banking relationships, with partnerships such as AIA-BPI, BDO Life, and Allianz PNB Life generating substantial premium inflows. Direct sales through digital platforms are accelerating as mobile apps and online comparison tools lower the barrier to first-time policy purchase, particularly among younger consumers comfortable transacting entirely through digital channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Insurance Type

Individual life insurance policies account for the dominant share of the Philippines life insurance market by premium volume, with investment-linked variable unit-linked plans representing the most commercially significant individual product type. The depth of consumer engagement with VUL plans reflects the dual appeal of life coverage and investment returns in a single product structure, well-suited to a young, aspirational Filipino middle class that values both financial protection and wealth accumulation. In 2025, Pru Life UK led all insurers in new business annual premium equivalent at PHP 10.05 billion, with the majority of its production driven by individual VUL sales through its extensive advisor network. Term life insurance is gaining share as a secondary individual product among cost-sensitive consumers and younger first-time insurance buyers. Group policies, while smaller in premium share, are growing through bancassurance and employer benefit channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Service Provider

Private insurance providers hold the dominant market share in the Philippines life insurance sector by a significant margin, with the combined premium income of private commercial insurers far exceeding the contribution of government-linked public providers. The Insurance Commission's 2025 data confirms the competitive strength of private players, with Sun Life Philippines topping life insurers by total assets at PHP 344.49 billion and Pru Life UK leading new business generation at PHP 10.05 billion NBAPE. FWD Life's emergence as the third-ranked insurer by new business premium, with PHP 9.03 billion in 2025, demonstrates how private sector agility and digital-first strategy can rapidly shift competitive position even in a market dominated by decades-old incumbents.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Demographics

The Adults demographic segment holds the largest share of the Philippines life insurance market and is also the primary driver of premium growth in both the individual and group insurance categories. The segment's projected CAGR of 6.5% reflects sustained demand from working-age Filipinos who are entering formal insurance for the first time or upgrading from basic term policies to investment-linked products. The Minors segment is growing as Filipino parents prioritize early financial planning through juvenile policies, while the Senior Citizens segment is attracting new product development attention from insurers building retirement annuity and long-term care offerings for an ageing demographic cohort.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Agents or Brokers account for the largest share of premium income in the Philippines life insurance market, underscoring the relationship-driven nature of insurance sales in a market where consumer education and trust are prerequisites for purchase. The Banks channel, while holding a smaller share, is the fastest-growing route to market, reflecting the successful scaling of bancassurance partnerships between major Philippine banks and leading insurers. Institutions such as BDO Life, BPI-AIA, and Allianz PNB Life have demonstrated that embedding life insurance within banking relationships generates high-quality, long-tenure customers who are already financially active and more receptive to protection and savings conversations. The Digital/Direct sales channel remains small but is growing as tech-savvy consumers, particularly in Metro Manila, seek self-directed policy purchase experiences.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The National Capital Region (NCR), encompassing Metro Manila and its adjacent urban areas, functions as the undisputed core of the Philippines life insurance market. The region's high concentration of corporate offices generating group insurance demand, its large base of employed professionals seeking individual coverage, and the density of bank branches enabling bancassurance distribution all combine to make NCR the primary revenue engine for every major life insurer operating in the country. Sun Life Philippines, the largest life insurer by total assets at PHP 344.49 billion, maintains its national headquarters and most of its advisor concentration in the NCR. AXA Philippines and Allianz PNB Life similarly prioritize Metro Manila for flagship product launches, high-value client events, and financial literacy campaigns. Insurance penetration in the NCR is the highest in the country and continues to improve as rising incomes and post-pandemic awareness of financial vulnerability sustain demand. Digital insurance platforms are particularly effective in Metro Manila, where smartphone penetration and trust in online transactions are highest among Philippine regions.

Luzon beyond the NCR, Visayas, and Mindanao collectively represent the largest structural growth opportunity in the Philippines life insurance market for the forecast period. These regions are characterized by significantly lower insurance penetration rates compared to Metro Manila, but are experiencing above-average income growth, urbanization, and increased exposure to financial literacy programs through government and insurer outreach initiatives. Bancassurance partnerships are the most effective mechanism for reaching provincial consumers, as major Philippine banks including BDO and BPI maintain extensive branch networks in secondary cities such as Cebu, Davao, Iloilo, and Cagayan de Oro. Microinsurance providers and cooperative-linked mutual benefit associations serve rural communities in Mindanao and Visayas that fall below the minimum income threshold for most commercial policies. The government's OFW insurance mandate is particularly impactful in regions with high overseas labor migration rates, creating a new insurance demand pool among families receiving remittances in provincial areas.

The Philippines life insurance sector is concentrated among a core group of well-capitalized domestic and international players, with Pru Life UK, Sun Life Philippines, FWD Life Philippines, Allianz PNB Life, and AXA Philippines consistently dominating new business and premium income rankings. The market is intensely competitive at the top, with close rivalry between Pru Life UK and Sun Life for new business leadership and FWD Life rapidly closing the gap through its digital distribution model. International insurance groups with deep local operating experience hold a structural advantage through established advisor networks, strong brand recognition, and multi-product relationships built over decades.

The competitive frontier is being reshaped by digital-first players and bancassurance partnerships. FWD Life's mobile-first Tapp platform and Singlife's digital premium payment features represent a growing expectation among Filipino consumers for frictionless, smartphone-based policy management. Bancassurance is shifting competitive dynamics by enabling insurers to scale distribution through banking partners without proportionally expanding agent headcounts. ESG-aligned product innovation and microinsurance development are emerging as differentiation vectors for reaching previously underserved consumer segments, as insurers compete not only on premium pricing but also on the breadth of populations they can serve effectively.

Pru Life UK, the Philippine subsidiary of London-headquartered Prudential plc (founded 1848), is the consistent leader in new business annual premium equivalent in the Philippines market. In 2025, Pru Life UK topped NBAPE rankings at PHP 10.05 billion, reflecting its dominant advisor network and the strong consumer appeal of its investment-linked and health-bundled life insurance products. The company has been recognized as International Life Insurer of the Year for three consecutive years and maintains a comprehensive product portfolio spanning term insurance, health coverage, accident protection, and unit-linked savings plans. Its disciplined focus on agent quality, digital advisor tools, and product flexibility makes it the benchmark for life insurance distribution excellence in the Philippines.

Sun Life Philippines, affiliated with Sun Life Assurance Company of Canada (founded 1865), is the largest life insurer in the Philippines by total assets, which stood at PHP 344.49 billion in 2025, and by net income at PHP 10.22 billion in the same year. The company has held the top asset position for four consecutive years and combines a well-regarded advisor force with strong financial literacy programs, investment-linked product depth, and an expanding digital capability for online policy applications and client servicing. Sun Life's long-standing reputation for financial stability and its commitment to consumer education make it the preferred insurer for Filipinos seeking trusted long-term financial protection and retirement savings.

Allianz PNB Life Insurance Inc. is a joint venture between global insurance giant Allianz SE (founded in Germany in 1890) and Philippine National Bank, bringing together international insurance expertise with a well-established local banking distribution network. The company ranked fourth by total assets in 2025 at PHP 168.459 billion and fourth by premium income at PHP 37.66 billion, reflecting the effectiveness of its bancassurance model in generating large premium volumes through PNB's branch network across the Philippines. Allianz PNB Life's product range covers life coverage, health benefits, and retirement and investment solutions, all marketed to PNB customers and independent prospects through financial advisors and bank channel staff.

AXA Philippines Life and General Insurance Corp. is the Philippine operating unit of the global AXA Group, which is one of the world's largest insurance and asset management organizations. With total assets of PHP 185.68 billion in 2025 and premium income of PHP 31.498 billion, AXA Philippines holds a strong third-tier position in the country's life insurance competitive landscape. AXA distributes life, health, income protection, and investment products through its strategic partnership with Metrobank and PSBank, making its policies accessible to millions of banking customers across the Philippines. AXA's focus on high-net-worth clients, comprehensive financial planning services, and innovative product structures has earned it a strong reputation in the premium urban insurance segment.

Other key players in the market are BDO Unibank, Inc., FWD Life Insurance Corporation, The Insular Life Assurance Company, Ltd., The Manufacturers Life Insurance Company, AIA Group Limited, Sun Life Grepa Financial, Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead in the Philippines Life Insurance Market with our comprehensive 2026 research report. From detailed segmentation across insurance types and demographic groups to competitive intelligence on Pru Life UK, Sun Life, AXA, and FWD Life, our report equips you with everything you need to make confident strategic decisions. Whether you are an insurer expanding into new channels, an investor assessing market potential, or a regulator benchmarking industry performance, this report delivers the depth of insight you need. Download your free sample today and start unlocking opportunities in the Philippines' thriving Life Insurance industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Philippines life insurance market reached an approximate value of USD 6.77 Billion.

The market is projected to grow at a CAGR of 6.10% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 12.24 Billion by 2035.

The major drivers of the market are the growing interest in ESG-focused investment-linked insurance policies, demand for insurance policies denominated in stable currencies, and regulations on Overseas Filipino Workers.

The key trends of the market include digital innovations, microinsurance growth, personalized products, and health integration.

The various insurance types considered in the market report are individual and group.

The various service providers considered in the market report are public insurance providers and private insurance providers.

The demographics considered in the Philippines life insurance market report are minors, adults, and senior citizens.

The major players in the market are Pru Life UK and Prudential pl, Sun Life Assurance Company of Canada, Allianz PNB Life Insurance Inc., AXA Group, BDO Unibank, Inc., FWD Life Insurance Corporation, The Insular Life Assurance Company, Ltd., The Manufacturers Life Insurance Company, AIA Group Limited, and Sun Life Grepa Financial, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Insurance Type |

|

| Breakup by Service Provider |

|

| Breakup by Demographics |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.