Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

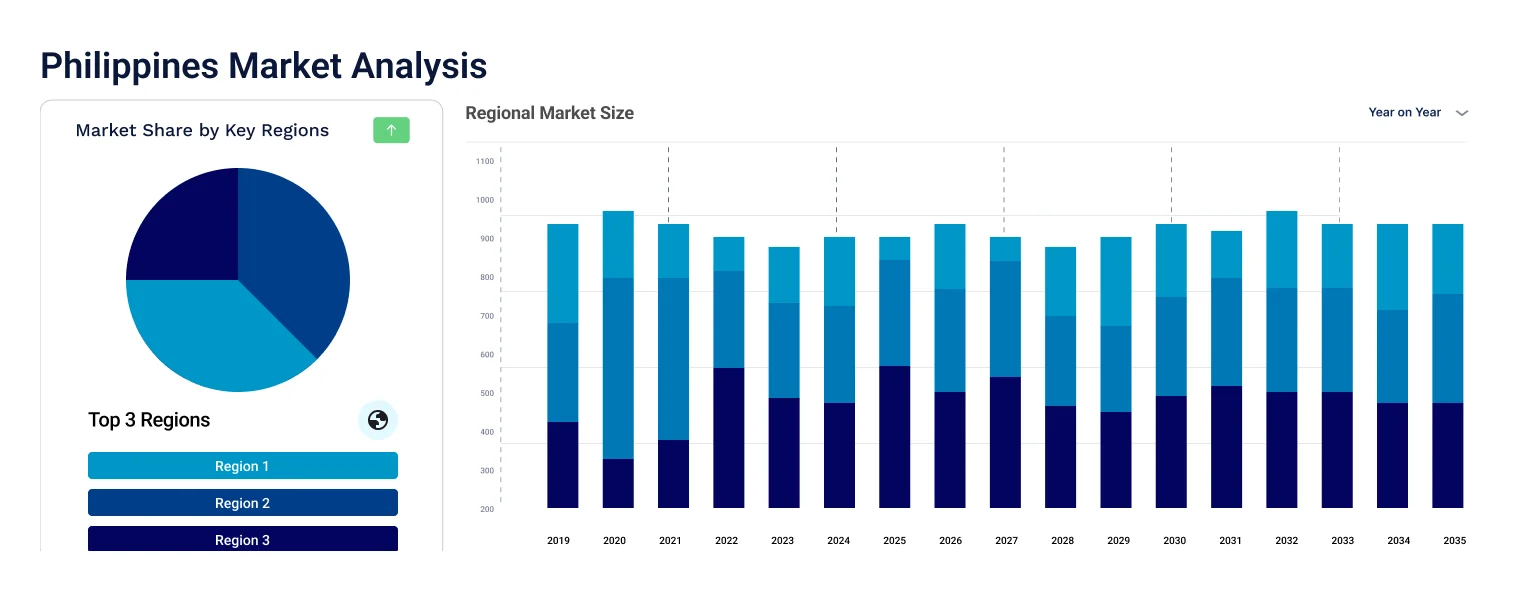

The Philippines OTC pharmaceutical market was valued at USD 1.57 Billion in 2025 and is expected to grow at a CAGR of 5.17%, reaching USD 2.60 Billion by 2035. The market growth is fueled by increasing self-medication trends and wider availability of over-the-counter drugs.

The Philippines presents a compelling growth environment for over-the-counter pharmaceuticals, shaped by a young and growing population of over 115 million people and a healthcare system where self-medication is deeply embedded in everyday life. According to the Philippine Statistics Authority, a significant portion of the population particularly in rural and semi-urban areas relies on OTC drugs as a first line of response due to limited access to formal healthcare facilities. This widespread self-care behaviour, combined with the rapid expansion of retail pharmacy chains across provincial towns and cities, is steadily broadening the Philippines OTC pharmaceutical market's consumer base beyond Metro Manila.

Rising health awareness following the COVID-19 pandemic has also left a lasting imprint on consumer behaviour in the Philippines. More Filipinos are now proactively managing common conditions from pain relief and fever to vitamins and digestive health without waiting for a doctor's consultation. The Department of Health's ongoing initiatives to improve medicine accessibility and the Food and Drug Administration Philippines' streamlined OTC drug registration framework are further supporting market growth by ensuring a wider, safer range of products reaches consumers across the country.

The Philippines OTC pharmaceutical market is on a firm and consistent growth path over the next decade, underpinned by strong structural drivers rather than short-term trends. A large, young population, an expanding middle class, and steadily improving retail pharmacy infrastructure across both urban and provincial areas are collectively ensuring that demand for over-the-counter medicines remains on a reliable upward trajectory.

The projected CAGR places the Philippines among the more consistently growing OTC pharmaceutical markets in Southeast Asia. The World Bank's data on rising household consumption expenditure in the Philippines, combined with the government's Universal Health Care Act pushing greater health awareness at the grassroots level, suggests this growth is structurally supported, making it a market with genuine long-term commercial relevance for manufacturers, distributors, and retail investors alike.

Compound Annual Growth Rate

5.17%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

With a large population base, rising health awareness, and access to healthcare services, the demand for OTC pharmaceuticals is experiencing significant surge across Philippines. The Filipino government has made medical sector a priority area of development with an allocation of PHP 296.3 billion in its annual budget. A substantial portion of this budget (around PHP 29.1 billion ), is earmarked for the purchase and distribution of a wide range of pharmaceuticals, including drugs, medicines, vaccines, as well as medical and dental supplies, to government health facilities across the country. As a result, Philippines OTC pharmaceutical market share is poised to witness a notable rise in the forecast period.

The OTC drug application across multiple domains including pain relief, allergy treatment, as well as wellness also fuels the market growth. The expansion of drugstores and pharmacies along with rising prevalence for e-commerce is one of the major market trends. In addition, increasing incidence of drugs approvals by regulatory authorities and efforts to improve the healthcare infrastructure and services to aid better outcomes for the population are expected to impact the market value positively in coming years.

Surge in Partnerships to Drive Philippines OTC Pharmaceutical Market Growth

In January 2024, STADA Philippines Inc., appointed Zuellig Pharma, a pioneering healthcare solution provider to distribute their products across Philippines. The alliance is expected to promote over the counter (OTC) drugs and consumer brands such as FERN-C vitamin C range and the Oilatum skincare line in the region. It will also allow easy access to ophthalmology, antibiotics, and cardiovascular medications, which can be helpful to decrease the rising prevalence of cardiac arrest associated deaths.

Increasing Integration of Artificial Intelligence to Expedite Drug Development Process

Philippines OTC pharmaceutical market demand is driven by increased efforts to improve the efficacy and quality of drugs. Researchers have been deploying the latest technologies such as machine learning and artificial intelligence to improve efficiency and bring precise solutions to the consumers. In June 2023, BioMed X and Sanofi launched a joint research venture to leverage artificial intelligence aided drug development. Titled as the “Next Generation Virtual Patient Engine for Clinical Translation of Drug Candidates” (VPE) project, it plans to develop a computational platform that predicts the efficacy of first or best-in-class drug candidates. Following the global trend, Philippines has also been witnessing infrastructure specific improvements to integrate all modern facilities in their research laboratories, which is anticipated to fuel the market value the forecast period.

Rising Prevalence for Digital Solutions

Philippines OTC pharmaceutical market size has increased with the continuous economic growth and rising disposable income levels as more people can afford and procure OTC drugs easily. With the sudden COVID-19 outbreak, the demand and application of digital services gained a massive momentum. Consequently, the preference for e-commerce platforms witnessed a surge, owing to variety of facilities such as contactless deliveries along with an array of options to choose from.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Philippines OTC Pharmaceutical Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Market Breakup by Distribution Channel

Market Breakup by Formulation Type

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Manila, holding a massive portion of educated and urban population, leads the regional market share. With greater access to healthcare services and typically higher disposable incomes, the OTC pharmaceutical consumption is higher in the region. In addition, the presence of supermarkets, convenience stores and other modern retail channels aids an additional opportunity for OTC pharmaceutical organizations.

Popular tourist spots such as Boracay, Palawan, and Cebu, are poised to hold to a substantial Philippines OTC pharmaceutical market share in forecast period. The growth can be attributed to increased tourist footfall, leading to higher demand for common medications such as motion sickness medication, sunburn relief and insect repellents.

With rising emphasis on developing improved alternatives for the masses, rural and remote areas are also witnessing expedited infrastructure developments. The government along with key healthcare providers are taking critical steps to bridge the gap and provide access to better healthcare facilities.

In November 2023, Lloyd Laboratories (a Filipino firm) and United States based DifGen Pharmaceutical signed a USD 20 million worth partnership to boost the local production of pharmaceuticals in the country. The alliance can be marked as a vital step towards the promotion of a robust local pharmaceutical and healthcare industry. It is also indicative of the current market trend which focuses on increased merger and acquisition activities.

The key features of the Philippines OTC pharmaceutical market report include patent analysis, grants analysis, clinical trials analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players. The major companies in the market are as follows:

Johnson & Johnson is one of the most widely recognised consumer healthcare companies operating in the Philippines, with a strong portfolio of OTC products spanning pain relief, skin care, and baby care categories. The company benefits from decades of brand trust built across Filipino households, making its products a default choice in pharmacies and supermarkets nationwide. Its global research capabilities and localised marketing approach have helped it maintain consistent relevance in the competitive Philippine OTC landscape.

GlaxoSmithKline has a well-established presence in the Philippines OTC pharmaceutical market, offering a broad range of consumer health products including vitamins, oral care, and respiratory relief formulations. The company's strong distribution partnerships with major pharmacy chains ensure reliable product availability across Metro Manila and key provincial markets. GSK's ongoing global shift toward consumer healthcare as a standalone focus area signals continued investment in markets like the Philippines where OTC demand is steadily rising.

Bayer AG brings a diverse OTC product portfolio to the Philippines, covering pain management, nutritional supplements, and dermatological care categories that see high repeat purchase volumes among Filipino consumers. The company's established local presence and trusted brand equity across multiple generations of Filipino families give it a durable competitive position. Bayer's commitment to consumer health innovation continues to drive new product introductions tailored to the specific health needs of Southeast Asian markets.

Pfizer participates in the Philippines OTC pharmaceutical space through its consumer health product lines, leveraging its globally recognised brand reputation to drive consumer confidence at the point of purchase. The company's extensive regulatory expertise and established relationships with the Food and Drug Administration Philippines facilitate efficient product registration and market access. Pfizer's focus on vitamins, supplements, and wellness products aligns well with the post-pandemic health consciousness that continues to shape Filipino consumer behaviour.

Sanofi has built a meaningful presence in the Philippines OTC market through its consumer healthcare division, offering products across allergy relief, pain management, and nutritional supplementation categories. The company's strategic focus on self-care solutions resonates strongly with the Philippines' deeply embedded self-medication culture, where consumers proactively manage common health conditions without formal medical consultation. Sanofi's investment in consumer education and pharmacy-level engagement further strengthens its brand visibility across the country.

Novartis contributes to the Philippines OTC pharmaceutical market through its established consumer health brands, focusing on high-quality formulations that address everyday health concerns faced by Filipino consumers. The company's global clinical expertise translates into products that meet both international quality standards and local regulatory requirements set by the Food and Drug Administration Philippines. Its strategic presence in key retail pharmacy networks ensures broad market accessibility across the archipelago.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players active in the Philippines OTC pharmaceutical market include Procter & Gamble, Reckitt Benckiser Group plc, Takeda Pharmaceutical Company Limited, Boehringer Ingelheim, Sun Pharmaceutical Industries Ltd., Perrigo Company plc, Teva Pharmaceutical Industries Ltd., Mylan N.V. (now part of Viatris Inc.), and Cipla Limited, each contributing to the market through their respective OTC product portfolios and distribution strengths across the country.

Upto 15% Off

USD

$3099 $2789

$1999 $1799

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is anticipated to grow at a CAGR of 5.17% during the forecast period of 2026-2035, driven by the rising demand for convenient and affordable medications for common health concerns across the region.

The market demand is driven by the increasing preference for self-medication, rising disposable income and infrastructure improvements leading to expansion of drugstores and pharmacies across the region.

Increasing mergers to provide enhanced solutions to the consumers is a major market trend. In January 2024, STADA Philippines Inc., appointed Zuellig Pharma, distribute over the counter (OTC) drugs along with ophthalmology, antibiotics, and cardiovascular medications across the country.

Based on product types, the market is divided into pain relievers, anti-allergic, gastrointestinal drugs, vitamins and minerals, cough and cold remedies and others.

Tablets, liquids, ointments, and sprays are common formulations available in the market.

Major distribution channels include retail pharmacies, online pharmacies, drug stores and others.

Key players involved in the market are Johnson & Johnson, GlaxoSmithKline, Bayer AG, Pfizer Inc., Sanofi, Novartis International AG, Procter & Gamble, Reckitt Benckiser Group plc, Takeda Pharmaceutical Company Limited, Boehringer Ingelheim, Sun Pharmaceutical Industries Ltd., Perrigo Company plc, Teva Pharmaceutical Industries Ltd., Mylan N.V. (now part of Viatris Inc.), and Cipla Limited.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Formulation Type |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.