Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The Philippines Personal Accessories Market reached a value of USD 2.65 Billion at 2025 and is projected to expand at a CAGR of around 8.60% during the forecast period of 2026-2035. With rapid wearable technology adoption among health-conscious urban consumers, surging social commerce and influencer-driven demand, expanding e-commerce accessibility across the Philippine archipelago, and a growing appetite for culturally rooted and sustainably produced accessories, the market is expected to reach USD 6.05 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Personal Accessories Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

2.65 |

|

Market Size 2035 |

USD Billion |

6.05 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

8.60% |

|

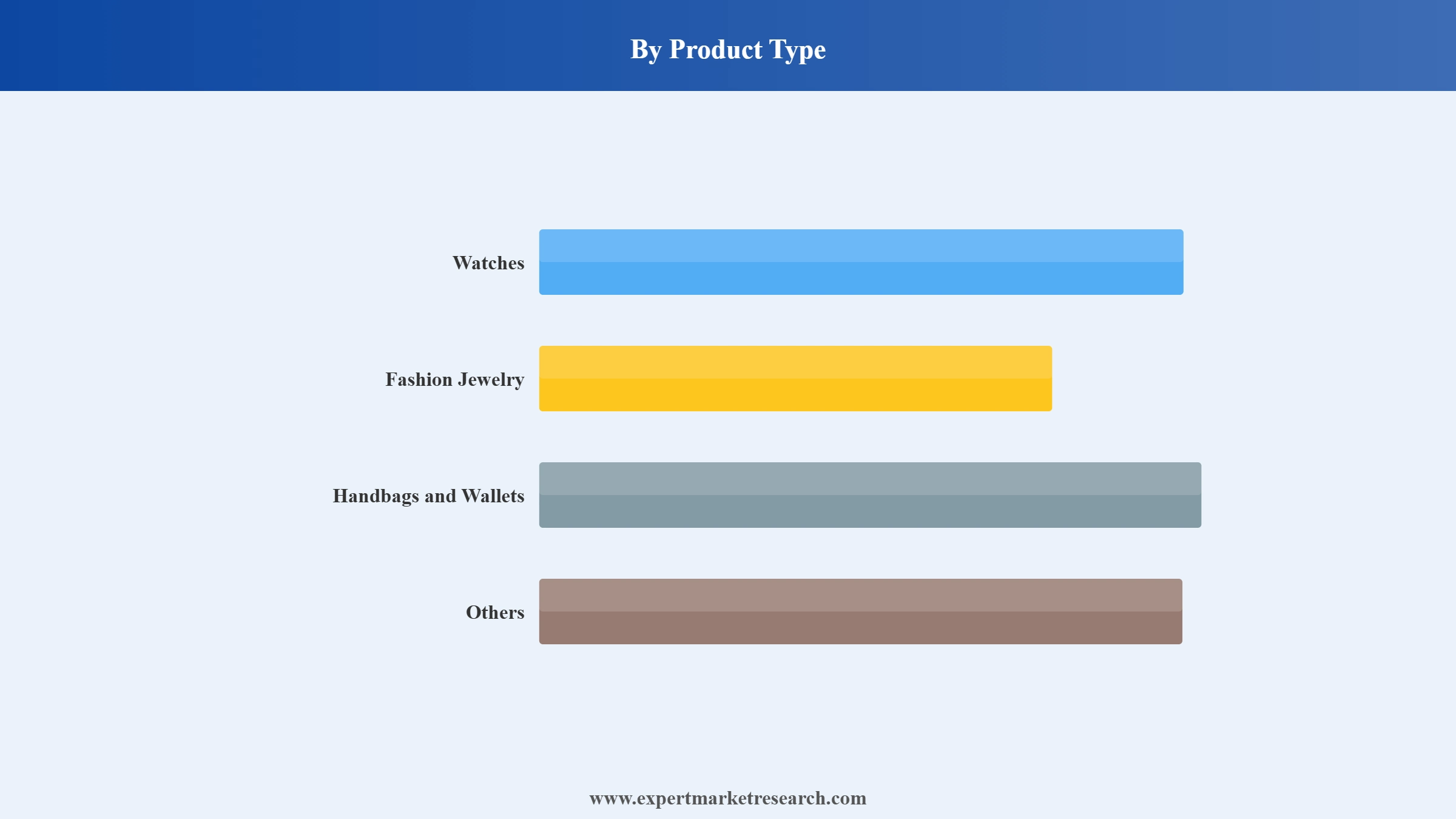

CAGR 2026-2035 - Market by Product Type |

Handbags and Wallets |

9.5% |

|

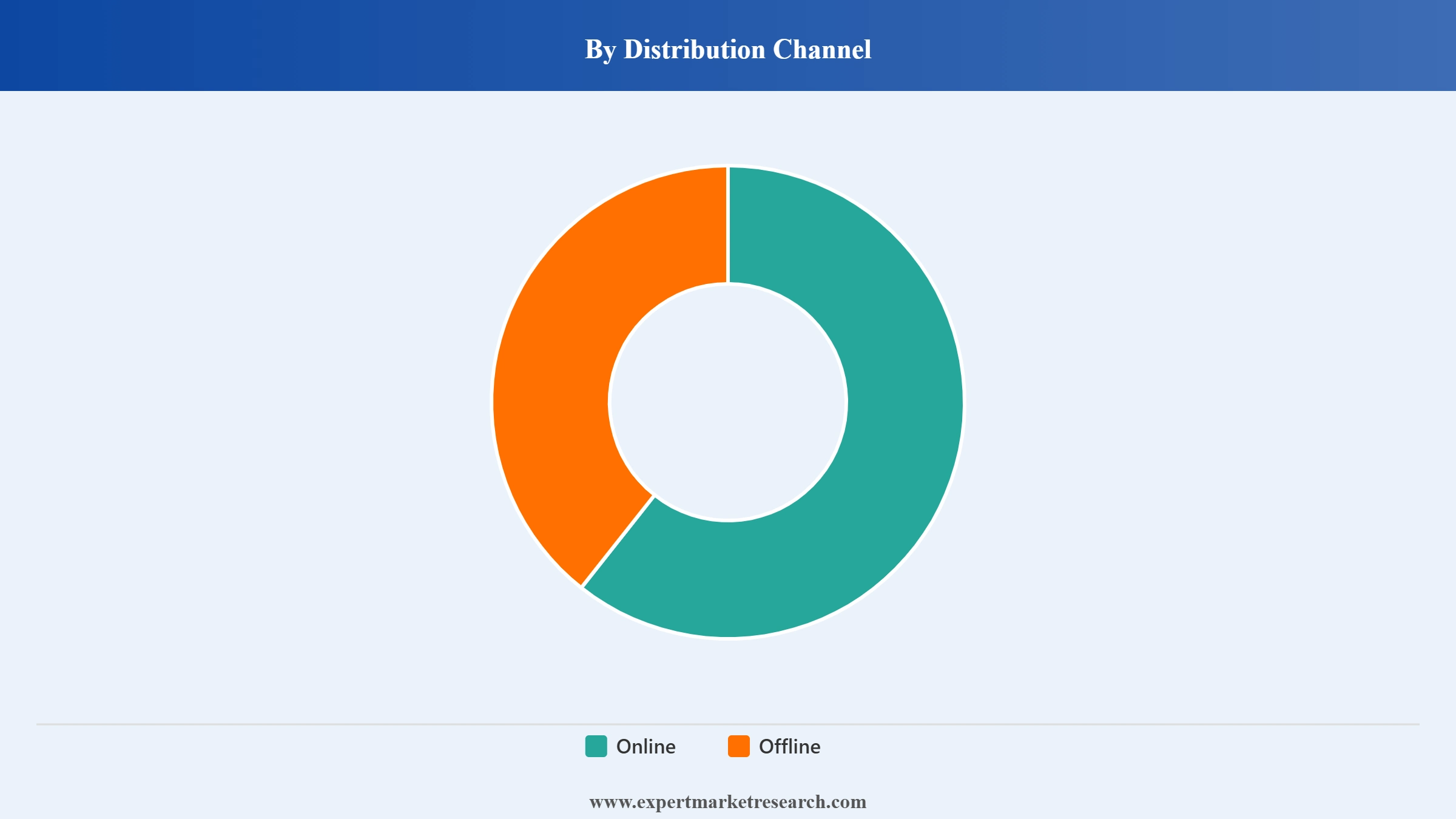

CAGR 2026-2035 - Market by Distribution Channel |

Online |

12.3% |

The Philippines personal accessories market is being reshaped by the meeting point of technology, lifestyle shifts, and cultural identity. These four trends are driving the market's trajectory through the forecast period.

In June 2025, French contemporary fashion label Sandro opened its first boutique in the Philippines at Greenbelt 5 in Manila, as part of its Southeast Asian expansion strategy. Founded in 1984 by Evelyne Chetrite, Sandro offers a curated range of ready-to-wear apparel, accessories, and footwear that blends minimalist sophistication with trend-forward design. The Manila opening adds to a growing roster of international fashion label entries into the Philippines, reflecting the increasing confidence of global brands in the country's expanding affluent consumer base and its maturing premium retail infrastructure in key lifestyle malls.

In May 2025, Garmin unveiled the Forerunner 570 and Forerunner 970, its latest GPS running and triathlon smartwatches featuring the brand's brightest AMOLED screens, built-in speakers and microphones, Garmin Triathlon Coach training plans, and advanced mental health and recovery tracking capabilities. The launch is directly relevant to the Philippines market, where health consciousness among urban and fitness-oriented consumers is accelerating demand for premium wearable accessories. Garmin's local strategy in the Philippines includes developing mental wellness smartwatch features in partnership with technology universities and clinics, deepening the brand's relevance among health-aware consumers in Metro Manila and key regional cities.

In May 2025, PUMA launched an immersive H-Street brand experience event in Seoul, commemorating the release of its new H-Street sneaker with a VIP opening featuring BLACKPINK's Rosé and other regional artists. The event highlighted the growing influence of K-pop culture and street fashion on Filipino consumer preferences, where PUMA maintains a strong presence through its PUMA Sports Philippines operations. Events of this nature directly amplify social media conversation and drive demand for branded accessories including bags, caps, and lifestyle footwear among Philippine millennials and Gen Z who closely follow regional pop culture trends.

In December 2024, Swedish watch brand Daniel Wellington made its official debut in the Philippines, expanding its Southeast Asian retail footprint to include one of the region's most digitally active and fashion-forward consumer markets. Known for its minimalist, gender-neutral watch designs and sporty sling bags developed in collaboration with regional artists, Daniel Wellington's Philippine launch targets the growing urban consumer base that values understated, versatile accessories with a strong social media identity. The entry reinforces the Philippines as a priority destination for mid-premium global accessories brands seeking a young, brand-conscious audience.

In February 2024, the Philippine government, through the Tatak Pinoy Act, introduced tax incentives and targeted support programs for local brands producing accessories using sustainable materials, aiming to promote innovation and competitiveness in the domestic personal accessories industry. The policy has encouraged local fashion accessory brands and artisan producers to accelerate investment in eco-friendly materials such as plant-based leather and upcycled textiles. This initiative supports the DTI's Go Lokal! program, which has already facilitated collaborations between fashion houses and Filipino artisans, giving rise to accessories featuring indigenous weaves from the Cordillera region and Mindanao-sourced pearls that are gaining international recognition.

The line between a timepiece and a health device has all but vanished in the Philippines. Smartwatches from Garmin, Apple, and Huawei that track heart rate, blood oxygen, mental wellness indicators, and sleep cycles are now positioned as must-have lifestyle accessories rather than purely utilitarian gadgets. Garmin's February 2025 launches, which included mental health tracking features developed in partnership with Philippine technology institutions, illustrate how brands are localizing product innovation to match the country's growing interest in holistic health. The Department of Information and Communications Technology is also encouraging wearable technology adoption, particularly in Metro Manila and Cebu, accelerating Philippines personal accessories market growth by expanding the addressable consumer base well beyond fashion-first buyers into health and fitness communities.

The Philippines ranks among the world's most active social media markets, with over 84.4 million social media users as of early 2024 and a January 2025 estimate of 90.8 million user identities, representing 78% of the entire population. This digital intensity has made Instagram, TikTok, and Facebook critical sales and discovery channels for personal accessories. Brands including PUMA, Nike, and Lacoste actively engage Filipino consumers through regional artist partnerships and K-pop-adjacent collaborations, building cultural relevance alongside commercial reach. Social commerce features embedded within Shopee and Lazada have further shortened the distance between inspiration and purchase, with influencer-tagged accessories generating measurable spikes in basket conversion rates, particularly among the 18 to 35 demographic that drives a disproportionate share of market growth.

Filipino consumers are increasingly gravitating toward accessories that carry cultural meaning alongside commercial appeal. Government-backed initiatives such as the DTI's Go Lokal! program are facilitating collaborations between global fashion houses and local artisans, producing accessories featuring Cordillera-inspired weaves, Mindanao pearl jewelry, and indigenous textile detailing that distinguish the Philippines in the broader Southeast Asian accessories market. At the same time, sustainability has become a genuine purchase criterion, particularly among Gen Z buyers, driving demand for accessories made from upcycled ocean plastic, plant-based leather, and traceable natural materials. Fashion jewelry brands including Tropiko now publish material traceability information, and the Tatak Pinoy Act, introduced in February 2024, provides tax incentives specifically targeting sustainable domestic accessories producers.

Online retail has become the fastest-growing distribution channel for personal accessories in the Philippines, with the segment projected to expand at a CAGR of approximately 12.3%. Lazada and Shopee dominate the digital accessories marketplace, providing brand-owned storefronts, flash sales, and in-app social commerce features that are reshaping purchasing behavior across both metro and provincial markets. Apple's Philippines online store has introduced 3D try-on options and AI-driven styling suggestions tailored for local consumer preferences, reflecting the broader industry trend toward immersive digital retail. In 2025, the market for personal accessories saw retail value grow 7%, outpacing volume growth of 2%, indicating a clear consumer shift toward higher-value purchases, a trend that online platforms are capturing by improving curation and premium product discovery tools.

The Expert Market Research's report titled "Philippines Personal Accessories Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Watches occupy a significant share of the Philippines personal accessories market, driven by the rapid convergence of technology and fashion through smartwatches from Apple, Garmin, and Huawei, alongside the continued demand for traditional timepieces from brands like Seiko and Diesel. The smartwatch sub-category is expanding particularly rapidly as health-conscious urban Filipinos treat their wrist devices as both fitness companions and style statements. Fashion Jewelry is one of the most dynamic product segments, fueled by social media influence, influencer-led brand launches, and the growing popularity of customizable, culturally rooted jewelry pieces. Handbags and Wallets is the fastest-growing product segment at a projected 9.5% CAGR, driven by urbanization, rising travel, growing corporate sector employment, and a shift toward branded functional bags for both professional and leisure use.

Market Breakup by End User

Key Insight: Female buyers represent the dominant end user segment in the Philippines personal accessories market, accounting for a majority of purchases across watches, fashion jewelry, handbags, and fashion-forward lifestyle accessories. Rising female workforce participation rates in the Philippines, combined with strong social media engagement and a culturally ingrained affinity for accessories as self-expression, sustain this segment's dominance. Female consumers are also the primary adopters of e-commerce for accessory purchases, making the segment particularly important for brand investment in digital and influencer marketing. The Male segment is growing at a healthy pace, particularly in the smartwatch and sports bag sub-categories, driven by increasing health awareness and the athleisure trend among Filipino men, with brands like Garmin, Adidas, and Nike specifically targeting this demographic through fitness-linked marketing.

Market Breakup by Distribution Channel

Key Insight: Offline retail remains the largest distribution channel in terms of current market share, with premium malls including Greenbelt in Makati, SM Mall of Asia, and Rockwell Center in Pasig serving as anchor venues for global accessories brands. Major brand boutiques and department store concessions drive significant offline transactions, particularly for higher-price-point watches, handbags, and branded jewelry. The Online channel, growing at a projected 12.3% CAGR, is the clear leader in growth momentum. Platforms including Shopee and Lazada have become primary discovery and purchase channels for fashion jewelry, mid-range bags, and sports accessories, while brand-owned digital stores from Apple, Nike, and Adidas offer curated premium experiences. The Philippines' high mobile internet penetration rate and social commerce integration within major platforms are accelerating the shift of mid-market accessory purchases from offline to digital channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the product type segmentation, Watches and Handbags and Wallets command the most significant portions of market value. Watches benefit from dual demand: traditional timepieces continue to hold status in gift-giving and professional contexts, while the smartwatch segment is expanding rapidly as health-tracking capabilities draw in a younger, tech-aware consumer base. Brands including Apple, Garmin, and Seiko serve distinct price tiers within this segment, giving retailers and online platforms wide optionality in positioning and margin management. Handbags and Wallets, growing at 9.5% CAGR, is increasingly shaped by functional demand including travel bags, crossbody bags, and professional laptop bags, all of which benefit from both the expansion of domestic tourism and growing corporate sector employment in Metro Manila and regional business hubs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the distribution channel segmentation, Offline currently holds the larger revenue share, with the Philippines' strong mall culture supporting high brand visibility and foot traffic in premium retail destinations. However, the Online channel is growing at more than double the rate of offline, and its trajectory is steeper than in most comparable Southeast Asian markets. This is partly because the Philippines has one of the world's highest social media engagement rates, with social commerce driving seamless discovery-to-purchase journeys for accessories priced in the mid-market range. Brands investing in 3D virtual try-ons, AI-based styling, and live-stream shopping events are seeing above-average digital conversion rates, and this channel is expected to significantly narrow the gap with offline over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Philippines personal accessories market is served by a mix of global sports and lifestyle brands, premium watch manufacturers, and international fashion labels, all of which have deepened their physical and digital presence in the country in recent years. Competition is driven by brand recognition, product innovation, social media engagement, and the ability to reach consumers across both premium retail environments and high-traffic e-commerce platforms. The market is structured around a clear price segmentation, with premium and aspirational brands like Apple, Garmin, Seiko, and Diesel serving the upper tier, mid-market brands including Adidas, Nike, PUMA, and Lacoste dominating volume transactions, and local and digital-native brands growing within the accessible fashion jewelry and functional bag categories.

Brands that combine product innovation with culturally relevant local marketing are winning outsized consumer attention. Partnerships with Filipino influencers, K-pop-adjacent brand ambassadors, and local artisans are emerging as core competitive strategies alongside investment in digital retail capabilities such as AR try-on tools and AI-powered styling recommendations. Market entrants from France, Sweden, and other fashion-forward markets are increasingly viewing the Philippines as a Southeast Asian priority due to its young demographics, high social media usage, and growing retail infrastructure in lifestyle malls.

Adidas AG, founded in 1949 and headquartered in Herzogenaurach, Germany, is one of the world's leading sportswear and accessories brands with a strong presence across the Philippines. Its accessories portfolio includes bags, backpacks, caps, sports watches, and branded lifestyle items that appeal to both fitness-oriented and fashion-forward Filipino consumers. Adidas Philippines leverages its partnerships with global sports franchises, including Juventus, and collaborates with local retailers and e-commerce platforms to maintain broad market access across Metro Manila and regional cities.

PUMA SE, founded in 1948 and headquartered in Herzogenaurach, Germany, maintains a vibrant presence in the Philippines through its PUMA Sports Philippines operations. The brand's accessories portfolio spans sports bags, caps, wallets, and lifestyle items positioned at the intersection of athletic performance and street fashion. PUMA's H-Street campaign in May 2025, featuring K-pop artist Rosé, exemplifies its strategy of using regional pop culture to drive accessories demand among the Philippines' socially active youth demographic, with strong sell-through rates observed on digital platforms following brand event activations.

Garmin Ltd., founded in 1989 and headquartered in Olathe, Kansas, is a leading wearable technology and GPS products company with growing relevance in the Philippines accessories market. Its Forerunner, Fenix, and Vivoactive smartwatch lines serve health-conscious urban Filipinos who treat precision tracking and fitness coaching as essential lifestyle features. Garmin is strengthening its Philippines footprint through partnerships with local technology universities and clinics to develop market-relevant mental wellness features, positioning the brand at the intersection of health technology and premium personal accessories.

Apple Inc., founded in 1976 and headquartered in Cupertino, California, is the dominant premium player in the Philippines wearable accessories segment through its Apple Watch lineup. In the Philippines, Apple's online store has rolled out 3D try-on experiences and AI-driven styling suggestions calibrated to local consumer tastes, making digital purchasing of its accessories more intuitive and personalized. Apple Watch's combination of health monitoring, connectivity, and premium brand positioning has made it the aspirational wearable accessory for Philippines' growing affluent and upper-middle-class urban consumer segment.

Other key players include Nike Inc., Seiko Group Corporation, Argos Watches Corporation, Diesel SpA, SUYEN CORPORATION (Aldo Corp.), Lacoste S.A., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The Philippines personal accessories market is growing fast, and the brands that are winning are those that understand the local consumer deeply. Our 2026 report gives you the full picture, from category-level forecasts to company strategies and emerging segment opportunities. Whether you are planning a market entry, optimizing a product range, or evaluating a retail investment, this report equips you with the insight you need to move with confidence. Download your free sample today and discover what is driving the Philippines' thriving accessories sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Philippines personal accessories market reached an approximate value of USD 2.65 Billion.

The market is projected to grow at a CAGR of 8.60% between 2026 and 2035.

The key players in the market include Adidas AG, PUMA SE, Garmin Ltd., Apple Inc., Nike Inc., Seiko Group Corporation, Argos Watches Corporation, Diesel SpA, SUYEN CORPORATION (Aldo Corp.), and Lacoste S.A., among others.

Key strategies driving the market include leveraging hyper-local design cues, adopting immersive online tech, and collaborating with Filipino artisans to personalize accessories.

The handbags and wallets segment is gaining massive traction and anticipated to expand with a 9.5% CAGR through 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.