Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

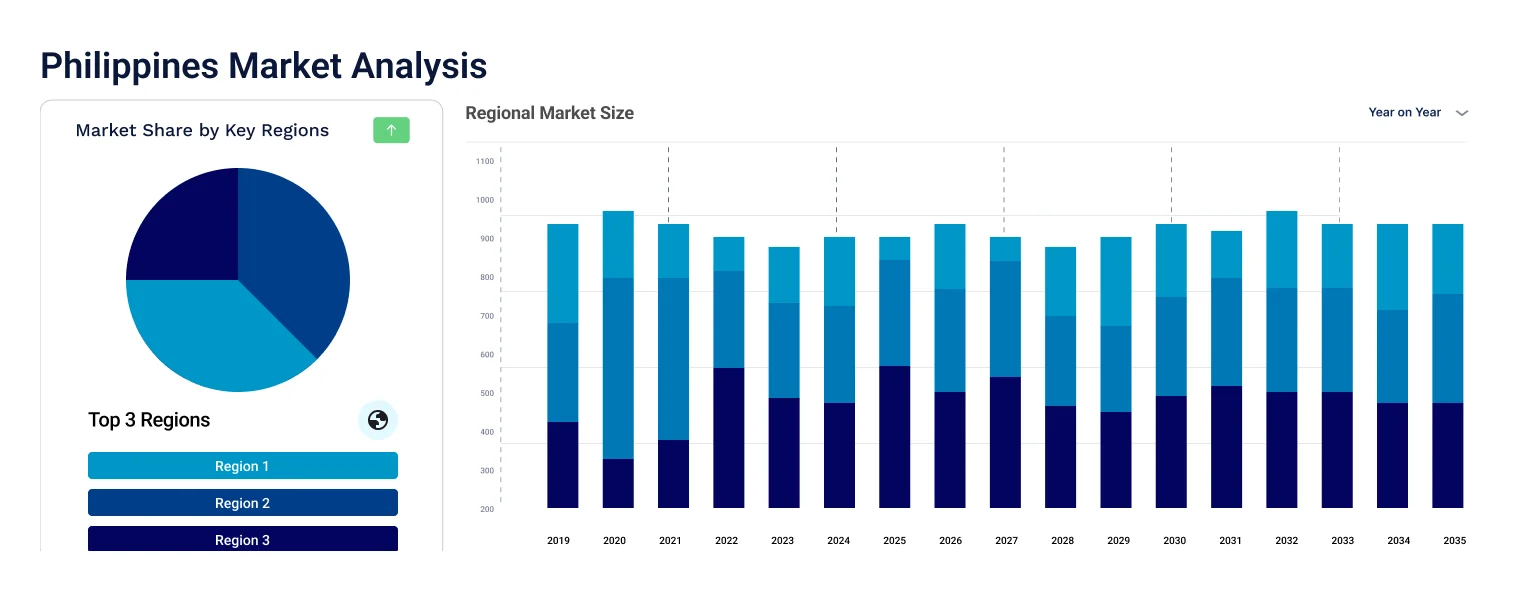

The Philippines semiconductor market size was valued at USD 7.93 Billion in 2025. The industry is expected to grow at a CAGR of 12.10% during the forecast period of 2026-2035 to reach a valuation of USD 24.85 Billion by 2035.

The Philippines Semiconductor Sector received a major capacity boost in April 2026 as Onsemi committed to expanding its operations across Cavite, Tarlac, and Cebu manufacturing plants, where the firm employs over 6,000 workers locally. Cebu Daily News reported that Finance Secretary Frederick Go discussed the expansion with Onsemi CEO Hassane El-Khoury, reinforcing the country's role in supplying foundational power chips for hyperscale data centers and AI infrastructure globally.

According to a Philippine Daily Inquirer article published in March 2026, Bing Viera, chair of the Semiconductor and Electronics Industries in the Philippines Foundation and country head of Amkor Technology, warned that the local Chip Sector risks slipping into stagnation due to its dependence on legacy "Jurassic" technologies. Despite recording USD 49.64 billion in 2025 electronics exports, Philippine facilities are losing higher-value packaging projects to regional peers like Vietnam.

The Philippines semiconductor market is experiencing significant growth, fueled by robust export performance, government initiatives, and diversification of global supply chains. The government of Philippines is improving infrastructure in PEZA (Philippine Economic Zone Authority) zones) to attract more players in the semiconductor and electronics industry. Upgrades include power stability, water supply, and transport connectivity. These economic zones host various key players such as ON Semiconductor, STMicroelectronics, and their expansion increases export competitiveness.

Further, through RCEP (Regional Comprehensive Economic Partnership), the Philippines gains greater access to semiconductor supply chains across Asia-Pacific. Reduced tariffs and simplified trade procedures enable smoother import of raw materials and export of finished chips, enhancing the sector’s integration with regional tech manufacturing hubs like Malaysia and Vietnam.

Government policies have played a key role in promoting the growth of the Philippines semiconductor market. The country has opened up full foreign ownership in renewable energy initiatives, a policy aimed at securing foreign investment and spurring technological development. Further, in September 2024, the American government initiated a workforce development initiative in the Philippines, allocating USD 13.8 million to train Filipinos for the semiconductor sector. More than 6,000 Filipino students will be initially included in this workforce development program This is a component of the International Technology Security and Innovation (ITSI) program under the CHIPS Act, which focuses on securing semiconductor supply chains through the development of skilled workers in partner nations.

Compound Annual Growth Rate

12.1%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Philippines Semiconductor Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

7.93 |

|

Market Size 2035 |

USD Billion |

24.85 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

12.10% |

|

CAGR 2026-2035 - Market by Product Type |

Microprocessors |

13.6% |

|

CAGR 2026-2035 - Market by Application |

Automotive |

13.8% |

As the 2026 ASEAN Chair, the Philippines launched priorities to strengthen regional semiconductor supply chains and digital economy frameworks. The initiative, supported by the Department of Energy and the ASEAN-BAC, focuses on building a resilient regional ecosystem and utilizing the Luzon Economic Corridor to position the country as a high-value manufacturing hub for the Southeast Asian market.

SEIPI President Danilo Lachica reported that while new 25% US tariffs on advanced computing chips pose a risk, the Philippine sector remains resilient by producing critical peripherals and power controllers for AI infrastructure. The industry expects to breach $50 billion in total electronic exports in 2026, driven by sustained demand in automotive components and hyperscale data center technologies.

Executive Secretary Ralph Recto convened the Semiconductor and Electronics Industry Advisory Council (SEIAC) to accelerate the implementation of the national industry roadmap. The administration pledged to maximize incentives under the CREATE MORE Law and address operational bottlenecks, supporting a sector that currently generates approximately ₱3 trillion in annual revenues and accounts for nearly 60% of total exports.

The Department of Trade and Industry (DTI) launched a strategic roadmap targeting $110 billion in annual electronics exports by 2030, with $70 billion specifically from semiconductors. Presented by Secretary Cristina Roque, the plan includes upskilling 128,000 professionals and establishing three national laboratories to transition the industry from assembly toward integrated circuit design and wafer fabrication.

Recognising the semiconductor sector's potential, the Philippine government is actively seeking to bolster its development. Efforts include reaching out to global semiconductor leaders like Texas Instruments to establish local chip fabrication operations. Additionally, the country aims to produce 128,000 engineers for the semiconductor industry, aligning with global demand and enhancing its position in the semiconductor value chain.

The Philippines is leveraging its strategic location and skilled workforce to attract major semiconductor players. The strategic location of the Philippines in Southeast Asia offers proximity to the major semiconductor markets, thus attracting global companies. The country is further preferred for location because of its skilled manpower and government incentives. According to the Semiconductor Industry Association, the Philippines is a key country in the global semiconductor industry, especially in assembly and testing manufacturing.

Demand for electronics used in automotive, telecommunications, and IoT devices is rising globally, creating opportunities for the Philippines semiconductor market. The country is increasingly supplying components for electric vehicles, smartphones, and industrial electronics, expanding beyond traditional consumer devices. The automotive electronics sector in the Philippines has shown significant growth. In May 2024, exports in this category rose by 114.25% year-on-year, from USD 2.29 million to USD 4.90 million. This surge indicates the country's expanding role in supplying components for electric vehicles and advanced automotive systems.

Geopolitical tensions and trade-route realignments are causing multinational companies to diversify their supply chains, which is increasing the demand of the Philippines semiconductor market. Due to its strategic location, English-speaking talent pool, and decades of manufacturing experience, the Philippines is eyed as a potential hub for ATP operations. The Philippines hosts 13 semiconductor ATP facilities, serving as a crucial node in the global supply network. They mainly import integrated circuits from countries such as Taiwan, U.S., and Japan, and export finished goods to Singapore, China, and Japan.

Local firms like Xinyx Design are gaining global clients in chip design, a move beyond traditional assembly. Their recent expansion into Europe shows how Philippine talent is being recognized in more advanced semiconductor roles. This diversification strengthens the country’s presence across the semiconductor value chain. In October 2022, the company inaugurated its European branch at the High Tech Campus in Eindhoven, Netherlands, known as the "Silicon Valley of Europe" to provide engineering services directly to European clients and integrate into the region's semiconductor ecosystem.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research’s report titled “Philippines Semiconductor Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Breakup by Product Type

Key Insight: As per the Philippines semiconductor market analysis, the microprocessors segment occupies a significant share, driven by global shifts toward digital infrastructure, AI integration, and cloud-based services. Microprocessors, integrated circuits that perform logic and control operations in electronic devices are in high demand across computing, mobile, automotive, and industrial sectors. As cloud computing and artificial intelligence adoption increases across Southeast Asia, demand for high-performance processing units has spiked. Philippine-based semiconductor exporters like Texas Instruments Philippines and Analog Devices contribute significantly to global microprocessor assembly and testing.

Breakup by Application

Key Insight: As per the Philippines semiconductor market report, the automotive sector is currently the fastest-growing application segment, driven by the increasing demand for electric vehicles (EVs), advanced driver-assistance systems (ADAS), and connected car technologies. In the first half of 2024, the Land Transportation Office (LTO) reported 10,001 new electrified vehicle registrations, nearly matching the total for all of 2023.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rising Demand for Memory Chips Fuels Growth in Philippines Semiconductor Market

The memory segment of the semiconductor market in Philippines is experiencing notable growth, driven by increasing global demand for data storage solutions in applications like artificial intelligence (AI), cloud computing, and 5G technologies. This surge is prompting local manufacturers to enhance their capabilities in producing memory components, such as DRAM and flash memory, to meet both domestic and international needs.

|

CAGR 2026-2035 - Market by |

Product Type |

| Microprocessors |

13.6% |

| Sensors/MEMS |

12.9% |

| Optoelectronics |

12.4% |

| Memory |

8.5% |

| Analog/RF/Mixed Signal |

XX% |

| Others | XX% |

Optoelectronics, which includes components like LEDs, photodiodes, and image sensors, is another high-growth area. The demand is being driven by increased usage in fiber-optic communication, solar energy systems, and advanced automotive lighting solutions. As the Philippines strengthens its semiconductor export ecosystem, local facilities are becoming more involved in optoelectronic assembly and testing. The rise in smart cities and digital infrastructure investments across Southeast Asia also supports this segment

Consumer Electronics Leading Semiconductor Demand Surge in the Philippines

The consumer electronics segment is currently the fastest-growing application area in the Philippines semiconductor industry. This growth is driven by increasing demand for smartphones, smart home devices, and personal electronics, fueled by rising disposable incomes and digital adoption. In December 2024, consumer electronics exports surged by 168.27% year-on-year, reaching USD 213.55 million, up from USD 79.60 million in December 2023.

The telecommunications sector is witnessing robust growth, fueled by the rollout of 5G networks and the rising demand for high-speed internet connectivity. Semiconductors play a crucial role in enabling faster data transmission and improved network infrastructure. In 2024, Globe Telecom deployed 587 new 5G sites nationwide, achieving 98.69% coverage in the National Capital Region and 96.95% in key cities across the Visayas and Mindanao. This expansion supports over 9 million 5G devices, reflecting the country's increasing reliance on advanced mobile data services.

Key players in the Philippines semiconductor market are actively expanding their manufacturing capacities, modernizing production lines, and investing in automation to meet growing global demand. They are enhancing capabilities in advanced packaging, assembly, and testing processes to stay competitive amid evolving technology requirements. Companies are also localizing supply chains and improving logistics networks to mitigate geopolitical risks and ensure continuity. Emphasis is being placed on compliance with global quality standards and integrating digital solutions, such as data analytics and AI, to improve yield, product performance, and time-to-market.

NVIDIA is a global leader in graphics processing units (GPUs), AI computing, and system-on-a-chip units. Headquartered in California, it drives advancements in gaming, data centers, autonomous vehicles, and AI. Known for its CUDA architecture and cutting-edge chips like the H100, NVIDIA is expanding its reach into semiconductor research and global supply partnerships, including growing interest in Southeast Asia.

Based in the Netherlands, Nexperia specializes in producing discrete, logic, and MOSFET components, with a focus on automotive and industrial applications. It operates manufacturing facilities globally, including in Asia, ensuring high-volume, reliable semiconductor production. Nexperia emphasizes efficiency and miniaturization and plays a key role in power management and connectivity within smartphones, EVs, and consumer electronics.

SFA Semicon Philippines is a subsidiary of SFA Semicon Co., Ltd. of South Korea, engaged in semiconductor packaging and testing services. Located in Clark Freeport Zone, it serves global customers in memory modules and solid-state drives. The company supports high-volume back-end production, primarily for DRAM and NAND products, and continues to expand its local operations and facilities.

ON Semiconductor, now operating as onsemi, is a U.S.-based firm delivering intelligent power and sensing technologies. It supports sectors such as automotive, industrial, and cloud computing with energy-efficient semiconductor solutions. The company has significant manufacturing and R&D operations in Asia, including the Philippines, where it produces analog, discrete, and mixed-signal devices for global distribution.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market are Toshiba Corp., Intel Corporation, Cirtek Holdings Corporation, and Infineon Technologies AG, among others.

Unlock strategic insights with our expertly curated report on the Philippines semiconductor market trends 2025. Download your free sample today to explore the Philippines semiconductor market forecast 2026-2035, key growth drivers, and competitive landscape. Stay ahead with data-driven insights from a trusted source. Ideal for investors, policymakers, and manufacturers eyeing Southeast Asia’s rising electronics hub.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 7.93 Billion.

The market is projected to grow at a CAGR of 12.10% between 2026 and 2035.

Key strategies include export-led growth, government-industry partnerships, foreign investment attraction, talent development through global training, and expanding into high-value segments like chip design, EV components, and advanced packaging and testing services.

The automotive sector exhibits highest growth rate, driven by the increasing demand for electric vehicles (EVs), advanced driver-assistance systems (ADAS), and connected car technologies

The major players in the market are NVIDIA Corporation, NEXPERIA B.V., SFA Semicon Philippines Corporation, ON Semiconductor Corp., Toshiba Corp., Intel Corporation, Cirtek Holdings Corporation, and Infineon Technologies AG, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Application |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.