Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

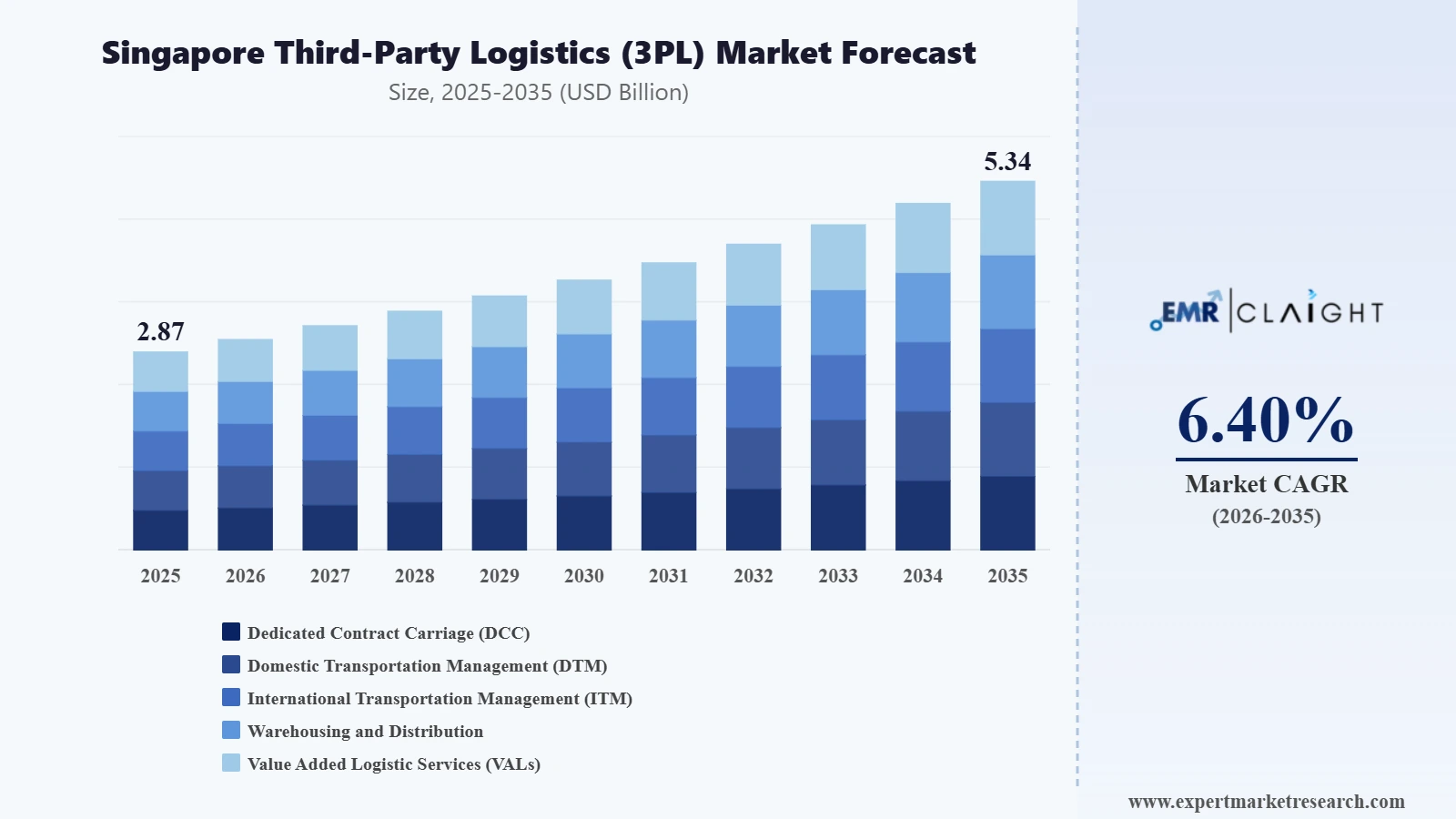

The Singapore third-party logistics (3PL) market size reached approximately USD 2.87 Billion in 2025. The market is projected to grow at a CAGR of 6.40% between 2026 and 2035, reaching a value of around USD 5.34 Billion by 2035.

Singapore has a presence of 3.51 million e-commerce users.

Singapore logistics chain node is connected to more than 600 ports worldwide, representing a high-frequency supply chain.

As of Q1/2022, Singapore had the presence of 121.5 million sq ft of warehouse space in the country, of which 97% was held by the private sector and 3% by the public sector.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Singapore’s strategic location as a central trading hub, presence of state-of-the-art infrastructure, and business-friendly environment are transforming the country into a robust logistics market. Moreover, the country’s third-party logistics (3PL) providers are playing a key role in supporting its reputation as a regional business hub. The presence of a tech-savvy population, with internet penetration over 95% and a growing young demographic, is contributing to the expansion of the e-commerce sector. This is further leading to the Singapore third-party logistics (3PL) market expansion, as e-commerce companies outsource their logistics operations to 3PL providers.

Singapore is witnessing an increase in cross-border trade, creating opportunities for 3PL companies to provide value-added services such as customs clearance and freight forwarding. From January to March 2024, Singapore Changi Airport registered 475,000 tonnes of airfreight throughput, representing an increase of 14% compared to the same period in 2023. Air freight provides the quickest shipping times, with efficient safety and security, thereby increasing its adoption.

It is estimated that by 2028, the online retail share will grow to 25.6%, as Singaporean customers are increasingly turning towards online channels for shopping purposes. The significant shift in consumer behaviour is pushing businesses to adopt a robust e-commerce strategy, further contributing to the Singapore third-party logistics (3PL) market growth.

"Singapore Third-Party Logistics (3PL) Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Service

Market Breakup by Transport

Market Breakup by End Use

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Major 3PL companies in the country are offering a variety of services with advanced technologies, ensuring efficient and reliable operation

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market reached approximately USD 2.87 Billion in 2025.

The market is projected to grow at a CAGR of 6.40% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 5.34 Billion by 2035.

The factors driving the market growth are increasing penetration of the internet, rising e-commerce, and rapid technological advancements, among others.

The major transportation methods include railways, roadways, waterways, and airways.

The major end uses are retail, healthcare, manufacturing, automotive, and others.

The various services include dedicated contract carriage (DCC), domestic transportation management (DTM), international transportation management (ITM), warehousing and distribution, and value added logistic services (VALs).

The major players in the market are CWT Pte. Limited, Singapore Post Ltd., Schenker AG, Kuehne + Nagel International AG, Deutsche Post AG (DHL), YCH Group Pte. Ltd, CEVA Logistics S.A, Nippon Express Holdings Inc, Toll Holdings Limited, and GEODIS S.A. (Keppel Logistics), among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Service |

|

| Breakup by Transport |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.