Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global software-defined data center market attained a value of USD 96.74 Billion in 2025 and is projected to expand at a CAGR of 31.20% through 2035. The market is further expected to achieve USD 1461.99 Billion by 2035. The adoption of AI-native infrastructure orchestration platforms by enterprises is driving up the uptake of software-defined data centers, which facilitate automation of workload balancing, energy efficiency, cybersecurity, and management of hybrid cloud environments.

Through April 2026, hyperscale and enterprise operators continued retooling software-defined data center estates to accommodate generative AI workloads, with a focus on virtualised GPU pooling, software-defined networking and zero-trust segmentation. The Wall Street Journal reported that AI capacity expansion is now the single largest driver of SDDC software spend.

Microsoft continued the rollout of software-defined networking on Azure Local powered by Azure Arc through early 2026, introducing cloud-driven network security groups and centralised hybrid network management. The release, detailed on Microsoft's official Azure blog, reflects accelerating convergence between on-premises SDDC and public cloud control planes.

The global software-defined data center market is currently undergoing rapid transformations, as firms are moving beyond traditional virtualization and embracing full-fledged policy-driven infrastructure ecosystems. For example, in May 2026, Broadcom launched VMware Cloud Foundation 9.1, enhancing secure, cost-efficient private cloud infrastructure to include AI workload orchestration and private cloud automation solutions for hyperscale companies. This release was aimed at serving financial institutions and telecom companies operating hybrid workloads with stringent latency requirements.

Additionally, structural modernization processes within enterprise IT infrastructure continue to transform the software-defined data center market dynamics. Prominent companies are increasingly turning to composable infrastructure, which unifies storage, networking, and computing resources using software. Leading vendors like Cisco Systems Inc. and Nutanix Inc. are making substantial investments in cloud-native orchestration systems that enable the operation of Kubernetes-based applications and distributed edge solutions. Firms in the financial services industry, healthcare, and semiconductors are actively adopting software-defined infrastructures to boost resilience against cyberattacks. For example, in April 2026, Axiado highlighted AI-driven hardware security innovations, funding growth, platform management solutions, and cybersecurity advancements for infrastructure.

Demand for autonomous infrastructure management is emerging as a key driving factor of growth in the software-defined data center market. Enterprises are adopting AI-enabled orchestration platforms to automate the allocation of workloads, manage network congestion, and mitigate downtime risks. Meanwhile, growing cybersecurity threats are making organizations adopt software-driven infrastructure solutions with inherent micro-segmentation and zero trust technologies. For example, in April 2025, Hewlett Packard Enterprise introduced automated threat detection and infrastructure observability features into its GreenLake cloud platform. Furthermore, increasing investment in edge computing by telecom operators and manufacturers is driving the demand for software-managed data center infrastructures.

Compound Annual Growth Rate

31.2%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Blackstone collaborated with Google to set up cloud-based computing systems that will be focused on AI-related computing needs using TPUs. Innovations such as these offer possibilities for other players to develop their own cloud-based computing systems oriented towards AI workloads and software-defined networking capabilities for business computing needs.

Tata Communications developed connectivity solutions based on self-healing networks to enable improvements in software-defined interconnectivity and better multi-data center connectivity management. Innovations such as these can help competing companies in the software-defined data center market build software-defined connectivity platforms with automated orchestration capabilities and cloud routing.

Schneider Electric launched solutions for high density AI and accelerated computing, providing support in energy efficient, scalable, and software-driven infrastructure modernization. Such developments make it possible for other companies to pay attention to sustainable cooling, power efficiency, and intelligent infrastructure management for hyperscale computing.

Dell Technologies offered new innovations in data centers for faster and secure private clouds with increased workload agility, automation, and software-defined enterprise computing. Such software-defined data center market developments inspire other firms to improve hybrid cloud security, resource automation, and software-defined private infrastructure.

Infrastructure management based on AI is radically transforming the software-defined data center market amid challenges that enterprises are facing due to increasingly complex workloads and energy-intensive applications. Enterprises are employing machine learning-powered orchestration technologies to forecast traffic peaks, provision resources effectively, and prevent any disruptions. In May 2026, Dell and NVIDIA advanced enterprise compute, integrating AI infrastructure, data platforms, and agentic AI scalability. There are also governmental efforts toward modernization of advanced infrastructure. For instance, in March 2026, the European Commission increased investments in energy-efficient cloud and edge computing infrastructure as part of its digital transformation programs, thus motivating enterprises to upgrade their legacy infrastructures.

Requirements for data localization and digital sovereignty are creating a strong impetus in the software-defined data center market. Governments and regulated industries are increasingly insisting on having more control over sensitive enterprise and citizens' data and are pushing cloud providers to create localized software-defined cloud infrastructures. For instance, in June 2023, Oracle launched sovereign EU cloud regions in Germany and Spain, strengthening data privacy, compliance, and regional control. Regulatory authorities across Germany, France, and India are strengthening compliance obligations regarding data residency and cybersecurity auditing.

The ongoing edge computing ecosystem growth presents new business opportunities in the software-defined data center market. Telcos, logistic companies, and industrial manufacturing firms are investing in decentralizing their IT infrastructures. For example, in March 2025, Schneider Electric launched Modicon Edge I/O NTS, enabling flexible data aggregation, cybersecurity, interoperability, and industrial automation efficiency. The International Telecommunication Union also reports an upsurge in the number of 5G subscriptions across the world, hence the need for low-latency infrastructure deployment methods is surging.

Growing sustainability pressures are influencing enterprise infrastructures' procurement decisions in the software-defined data center market. Businesses are under pressure to reduce carbon footprint, power utilization effectiveness, and environmental reporting standards. The International Energy Agency reports that the demand for computing resources from artificial intelligence could significantly increase global electricity consumption from data centers in the next ten years. As an effective initiative, in December 2024, Lenovo Group Limited unveiled its liquid-cooled infrastructure solutions that incorporate software-defined management software to minimize energy consumption related to cooling of high-performance data centers.

A hybrid and multi-cloud approach is becoming critical for enterprise digital transformation efforts, thus creating significant demand within the global industry. Modern enterprises are demanding workload portability between their private clouds, public hyperscale clouds, and edge computing infrastructures without affecting governance or visibility. Demonstrating this trend in the software-defined data center market, in May 2025, IBM expanded hybrid AI capabilities, helping enterprises deploy AI agents, improve integration, and scale secure data-driven automation.

The Expert Market Research's report titled “Global Software-Defined Data Center Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

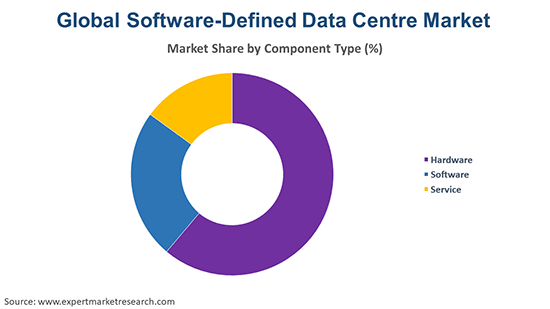

Market Breakup by Component Type

Key Insight: Software components maintain relevance in the software-defined data center market owing to the need by companies to adopt orchestration platforms, virtualization software, and automation frameworks that enhance their infrastructure flexibility and visibility. The market observes a steady demand for hardware as firms seek to upgrade their servers, networking gear, and storage that is optimized for cloud-native applications and AI. Service providers are becoming increasingly important as firms increasingly realize the need to consult in regard to deployment, security integration, infrastructure migration, and managed services. Distributed cloud ecosystem adoption is also characterized by a need for long-term operational support in terms of maintaining consistency in infrastructure and performance optimization. Aligning with such trends, in May 2026, HPE launched unified private clouds and data platforms, improving AI readiness, resilience, workload modernization, and operational efficiency.

Market Breakup by Deployment Type

Key Insight: Software defined computing represents the dominant category in the software-defined data center market as enterprises prefer the flexibility in compute virtualization and centralized workload management. Software-defined storage is constantly growing as organizations seek scalability in data management, quick data retrieval processes, and easier backup management for AI and analytics solutions. Moreover, there is a growing adoption of software-defined networking driven by demands for programmability in traffic management, cyber security segmentation, and low latency.

Market Breakup by Company Size

Key Insight: Large enterprises continue to lead the software-defined data center market revenue growth owing to the need to orchestrate their highly sophisticated digital infrastructure and optimize workloads and cybersecurity through automation. They are interested in scalable virtualization platforms and intelligence in infrastructure visibility. For example, in May 2026, SAP unveiled Autonomous Enterprise, integrating business AI, automation, governance, and agent-driven enterprise workflow transformation. On the other hand, small and medium enterprises are gravitating towards software-defined data centers due to the availability of cloud-based subscription services that make it easier to adopt and manage infrastructure.

Market Breakup by End Use

Key Insight: The government and the defense sector make use of software-defined infrastructure for secure data handling and automation of mission-critical workloads, accelerating demand in the software-defined data center market. For example, in April 2026, Viasat launched Tactical Mission Fabric, enabling resilient edge-to-cloud connectivity, AI-driven analytics, secure orchestration, and mission continuity. Financial organizations require low-latency infrastructure for regulatory compliance and real-time transaction processing. The healthcare industry is using scalable virtualization technology for telemedicine, artificial intelligence diagnostics, and record management. Schools and universities are continuously updating their digital learning infrastructure using cloud-based orchestration platforms. Retailers are becoming dependent on software-defined infrastructure for omnichannel commerce and predictive analytics.

Market Breakup by Region

Key Insight: The North American region is leading the software-defined data center market growth due to its robust investments in hyperscale clouds, high adoption rate of enterprise virtualization, and innovative infrastructures. The European region is prioritizing sovereign cloud implementations, sustainability-based infrastructure innovations, and cyber security framework implementations. The Asia Pacific region is experiencing fast growth owing to rapid implementation of cloud transformations, digital connectivity, and artificial intelligence infrastructure implementations by governments and enterprises. In the Latin American region, there is an increased demand for virtualization platforms that can support telecommunication infrastructural advancements and fintech development. On the other hand, the Middle East and Africa region is steadily growing due to smart city projects, digital government projects, and cloud infrastructure ecosystems implementations. In April 2026, Volt formed a Dubai joint venture to build AI-ready data centers, expanding scalable digital infrastructure capacity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By component, the software segment dominates the market owing to increasing infrastructure virtualization and automation acceptance

Software holds the largest share of the software-defined data center market as businesses prefer software solutions that offer centralized orchestration, intelligent workloads, and programmable infrastructure. Companies from the banking sector, telecommunication industry, and healthcare providers are opting for software solutions that facilitate the virtualization of applications, artificial intelligence-based monitoring tools, and cloud-based management systems. The demand for software solutions which can integrate hybrid cloud environments with cybersecurity automation is rising steadily. As a result, in May 2026, Elastx expanded cloud infrastructure using Lightbits software-defined storage, improving scalability, resilience, cost efficiency, and hardware flexibility.

Services emerge to be the fastest-growing segment as businesses need professional services related to consulting, deployment, integration, and management of software-defined solutions. Enterprises shifting from traditional infrastructure to software-defined infrastructure lack the technical expertise to handle orchestration framework, virtualization layer, and automated networking. Hence, service providers are offering lifecycle management, cybersecurity assessment, and migration services for hybrid cloud transformation.

By deployment type, software defined computing dominates the market due to rising enterprise virtualization requirements

Software defined computing dominates the software-defined data center market as businesses seek to virtualize computing resources for scalable digital operations and AI-powered applications. Businesses are focusing on centralized compute resource management, automated provision, and workload balancing functionalities to enhance their operational efficiencies. The highest demand for software-defined computing is driven by hyperscale cloud providers and financial services organizations managing fluctuating workloads across hybrid environments. Vendors are developing more advanced software for processing optimization, virtualization management, and AI-based infrastructure scheduling solutions.

Automation and orchestration represent the most rapidly growing deployment area in the software-defined data center market due to the rising demand for autonomous infrastructure management. Businesses that deploy multi-cloud and edge computing strategies need advanced orchestration systems that can automate workload distribution, policy implementation, and infrastructure monitoring in geographically distributed infrastructures. Businesses are leveraging AI-driven orchestration platforms to foresee performance constraints and increase resiliency of their infrastructure. For example, Teleste and Polystar partnered to launch AI-driven cable automation, improving predictive operations, analytics, efficiency, and network reliability in May 2026.

By company size, large enterprises account for the largest market share owing to complex hybrid infrastructure modernization investments

Large-scale businesses lead the software-defined data center market growth due to the surging need for scalability, virtualization, and cybersecurity management in their highly distributed infrastructure environments. Financial services firms, telecom operators, and large-scale manufacturers are allocating resources into centralized infrastructure orchestration for the execution of artificial intelligence workloads, cloud migration projects, and digital transformation programs. They also focus on workload balancing, infrastructure analytics, and compliance monitoring.

Small and medium-sized businesses are embracing the software-defined data center technology with notable enthusiasm owing to the increasing availability of cloud-based infrastructure platforms. Small businesses and medium-sized enterprises need scalable IT infrastructure that will enable them to run remote operations, e-commerce sites, and cybersecurity strategies without heavy investments. Vendors are developing subscription-based orchestration platforms, managed virtualization, and automation solutions for SMEs. In May 2026, Enphase unveiled AI data center, battery, and EV charging roadmap, expanding energy storage and intelligent power infrastructure.

By end use, the IT and telecom sector dominates the market due to accelerating cloud infrastructure deployments

The IT and Telecom sector is expected to lead the software-defined data center market growth dynamics owing to the need for extremely scalable infrastructure that supports cloud computing, 5G network rollout, and intelligent digital services. Telecommunication companies are now depending on software-defined networking and automation tools to cope with increasing traffic volumes and distributed edge computing environments. Technology players are also making substantial investments in virtualization solutions, cloud-native infrastructure management platforms, and autonomous monitoring technologies. For example, in May 2026, RTX’s Raytheon advanced software-defined radar capabilities, improving naval flexibility, multi-mission performance, and spectrum-sharing efficiency.

The healthcare industry represents the fastest growing end-user application segment due to increased digital transformation of healthcare operations, medical devices, and cloud-based patient management solutions. The adoption of software-defined infrastructure among hospitals and healthcare organizations can be attributed to the requirement for enhanced data availability, security, and real-time analysis capabilities. The growth of AI-powered diagnostic systems, telehealth platforms, and EHR applications is also fueling demand for virtualization and workload automation technologies.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America secures the leading share of the global market owing to strong hyperscale cloud infrastructure investments

The North American region is dominating the software-defined data center market owing to its robust hyperscale cloud ecosystem, advanced digital infrastructure, and significant adoption by enterprises of AI-based technologies. Large-scale technology players and colocation providers are spending significantly on software-defined networking, autonomous infrastructure management, and hybrid cloud orchestration solutions. Increasing emphasis by enterprises in the financial services industry, healthcare sector, and telecom industry on scalable virtualization platforms and security-centric infrastructure modernization is becoming evident. In March 2025, Vertiv launched software enhancing power and thermal chain visibility, improving control, efficiency, and hyperscale data center resilience.

The Asia Pacific region is expected to become the fastest-growing software-defined data center market owing to the increasing adoption by enterprises and governments of cloud computing, digital infrastructure, and AI-based modernization strategies. Telecom players, e-commerce firms, and banks in India, China, Japan, and Southeast Asia are investing significantly on scalable software-defined platforms. For example, in February 2026, STT GDC launched a 45 MW AI-ready Chennai facility, expanding hyperscale capacity and strengthening India’s data infrastructure.

The market is becoming highly competitive as vendors direct their efforts on developing AI-driven infrastructure automation solutions, sovereign clouds, and edge-friendly virtualization platforms. Leading software-defined data center market players are focusing on telecom, BFSI, and healthcare segments, where there is increasing demand for intelligent workload management and resilient security solutions. Predictive analytics for infrastructure, AI-driven data centers using liquid cooling, and autonomous network management systems are some technologies that providers are currently concentrating on.

The collaboration between cloud service providers, semiconductor companies, and infrastructure software vendors is also increasing. Several software-defined data center companies are discovering new business prospects in hybrid cloud migration services, distributed edge infrastructure, and carbon-aware workload management platforms. Many companies are now developing industry-specific orchestration software designed for industries that require data localization and compliance management. Subscription-based infrastructure services and AI-based observability software are also helping vendors increase their recurring revenue.

The International Business Machines Corporation was incorporated in 1911 and has its headquarters in Armonk, New York, United States. The company operates in the area of hybrid cloud infrastructure, AI-enabled automation, and the integration of Red Hat OpenShift in software-defined infrastructure. IBM is increasingly concentrating on regulated industries with the use of advanced orchestration, automation in cybersecurity, and observability solutions for multi-cloud and enterprise virtualization.

Dell Technologies Inc. was incorporated in 1984 and has its headquarters in Round Rock, Texas, United States. The company offers integrated solutions of software-defined infrastructure that are specifically designed for AI workloads, private clouds, and edge infrastructures. The company is focusing on liquid cooling, automated lifecycle management, and hybrid cloud orchestration.

Microsoft Corporation was formed in 1975 and operates from Redmond, Washington, United States. It serves the software-defined data center sector with Azure Stack, intelligent cloud orchestration services, and infrastructure monitoring using artificial intelligence technology. Microsoft concentrates more on hybrid cloud interoperability, cybersecurity robustness, and low-latency edge infrastructure solutions for enterprise digital transformation initiatives.

HUAWEI Technologies Co., Ltd. was founded in the year 1987 and operates from Shenzhen, China. This company provides AI-driven cloud infrastructure services, software-defined network architectures, and intelligent data center management software. Huawei is working to build modular infrastructure ecosystems, advanced energy-efficient cooling solutions, and automation software solutions that serve telecom operators, governments, and hyperscale enterprises.

Other key players in the market include Oracle Corporation, Hewlett Packard Enterprise Co, Nutanix, Inc., and Red Hat, Inc., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our software-defined data center market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is expected to grow at a CAGR of 31.20% between 2026 and 2035.

The major drivers expected to aid the market growth are the growing penetration of consumer electronics, rising disposable incomes, advent of IoT and growing demand for cloud based technologies, increased establishment of data centers, and development of software-defined data center solutions.

The key trends guiding the growth of the market include the increased investments by the companies to develop enhanced 5G facilities and the growing research and development activities.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Hardware, software, and service are the leading component types of the product in the market.

Software defined computing, software defined storage, software defined data center networking, and automation and orchestration are the major deployment types of the product in the market.

The significant segments based on company size include small and medium enterprises and large enterprises.

Banking, financial services and insurance, IT and telecom, government and defence, healthcare, education, retail, and manufacturing, among others, represent the significant end use segments of the product in the market.

The major players in the market are International Business Machines Corporation, Dell Technologies Inc., Microsoft Corporation, HUAWEI Technologies Co., Ltd., Oracle Corporation, Hewlett Packard Enterprise Co, Nutanix, Inc., and Red Hat, Inc., among others.

In 2025, the market reached an approximate value of USD 96.74 Billion.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component Type |

|

| Breakup by Deployment Type |

|

| Breakup by Company Size |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.