Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

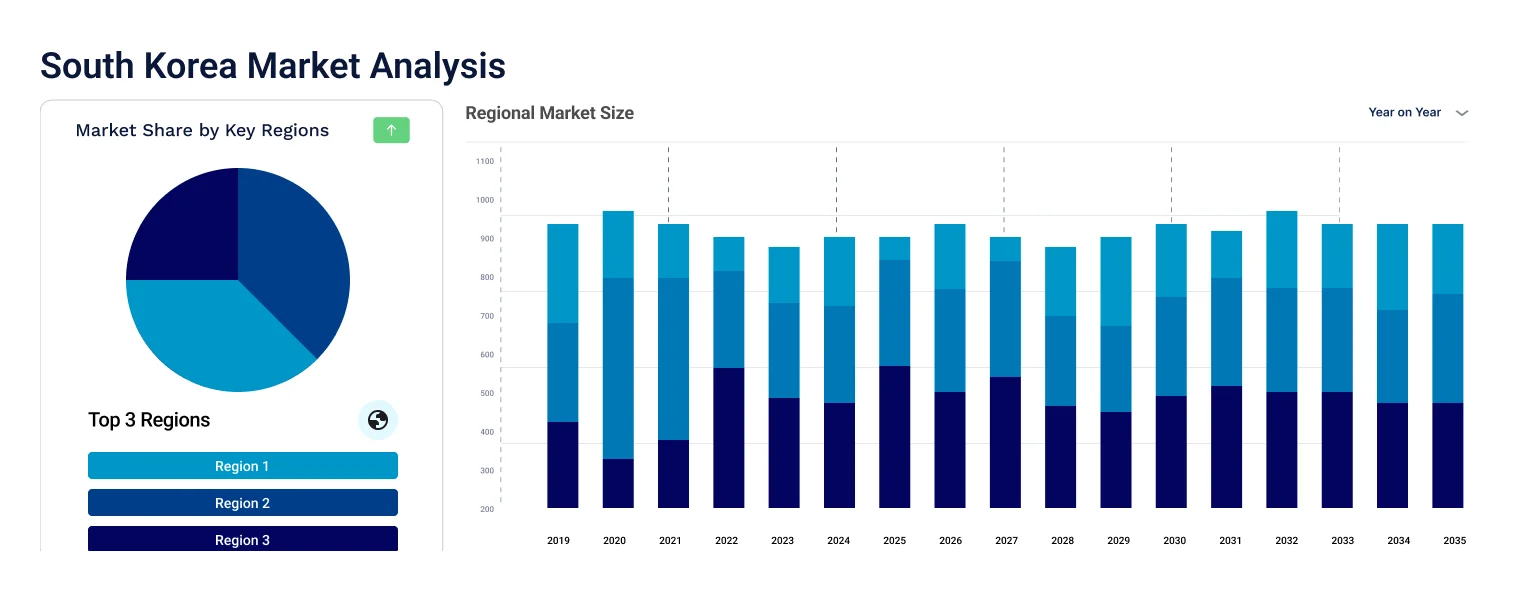

The South Korea battery recycling market attained a value of USD 214.62 Million in 2025 and is projected to expand at a CAGR of 6.00% through 2035. The market is further expected to achieve USD 384.35 Million by 2035. Rising geopolitical risks around critical minerals are pushing Korean battery makers to secure recycled materials domestically, accelerating investment in battery recycling infrastructure and long-term supplier partnerships.

The pressure from tougher environmental regulations in South Korea is compelling battery producers to develop end-of-life battery management plans. To be in compliance, suppliers realize that there must be documented recovery rates, approved recyclers, and traceability of materials. Meanwhile, the rising scale of EV cell production has led to a sharp increase in manufacturing scrap, including electrode trims and rejected cells, impacting the overall South Korea battery recycling market growth. The combination of regulatory pressure and available scrap materials is pushing recycling firms to expand capacity ahead of schedule.

The increasing capacity of recycling companies to recycle nickel, cobalt, and lithium from used batteries indicates that recycling companies are moving from pilot-scale recovery to industrial-scale recovery. For example, in December 2023, SungEel HiTech, a South Korean company, further expanded its hydrometallurgical recycling plant in Gunsan, increasing the country’s domestic closed-loop battery recycling capacity.

The South Korea battery recycling market is further moving from the waste management sector to a strategic materials sector. Recycling companies are integrating their businesses with battery manufacturers to gain long-term supply contracts. Companies are also focusing on developing sophisticated separation technologies to enhance the purity of recovered materials and lower the cost of refining. For example, SK Innovation announced that its independently developed lithium iron phosphate (LFP) battery recycling technology was published in Separation and Purification Techno in December 2025. Such developments benefit local cathode manufacturers, who want to minimize their reliance on imported raw materials. The government’s circular economy initiatives are also promoting this development, which will encourage increased recycling rates and traceability throughout the battery life cycle.

Compound Annual Growth Rate

6%

Value in USD Million

2026-2035

Livium partnered with a South Korean firm to explore solar and battery recycling, targeting material recovery efficiency and localized processing infrastructure. Other recyclers can leverage this South Korea battery recycling market opportunity to collaborate with regional partners to localize collection, processing, and compliance-driven recycling services.

South Korea inaugurated its largest research center to accelerate innovation across energy storage, recycling technologies, and next-generation battery materials development. Technology providers can thus pilot recycling innovations through government-backed research ecosystems and fast-track commercialization partnerships.

LG Energy Solution established a recycling joint venture with Derichebourg, strengthening closed-loop battery material recovery across electric vehicle supply chains. Component suppliers can leverage such developments in the South Korea battery recycling market and integrate into closed-loop systems by offering sorting, pre-processing, or secondary material refinement services.

Emerson automated a leading EV lithium-ion battery recycling facility, improving process efficiency and real-time operational visibility. Such developments encourage automation, AI, and industrial software firms to position solutions for efficiency, traceability, and regulatory compliance upgrades.

Closed-loop recycling systems are becoming standard requirements in the South Korea battery recycling market dynamics. Recycling firms are signing direct supply agreements with battery cell manufacturers to recycle metals into new cathode materials. This has enhanced the risk of raw material supply and ESG disclosure. Public institutions are working together on traceability projects to track the recycled materials. Firms are working on technology solutions to track material traceability. In January 2026, Noveon Magnetics, Kangwon Energy Co., Ltd., and LG Electronics Co., Ltd announced a strategic agreement to advance closed-loop recycling of rare earth permanent magnets, leveraging Noveon's proprietary Magnet-to-Magnet technology.

Hydrometallurgical recycling methods are becoming popular compared to pyrometallurgical recycling methods. These methods allow for a higher rate of recovery with less energy consumption. Korean recyclers are also enhancing the leaching and solvent extraction methods to improve lithium and nickel recovery. Technological developments are reducing waste residues and production costs. For example, IS Dongseo’s Korean facility became capable of processing about 7,500 tons of waste batteries per year, since January 2022. Government-funded R&D projects are helping in pilot optimization. This South Korea battery recycling market trend is helpful for the recyclers to meet more stringent environmental regulations while producing high-grade materials for direct cathode recycling.

Scrap from battery manufacturing is proving to be a significant source of feedstock. The non-functional battery cells and electrodes from gigafactories are a constant source of input volume with known chemistry. Companies are establishing dedicated lines for pre-consumer waste recycling. This will ensure minimal risks of contamination and maximize the processing volume, accelerating the overall South Korea battery recycling market value. Companies that manufacture batteries are poised to benefit from optimal recycling cycle times and yield management. In August 2023, EV battery recycler Aqua Metals entered into a strategic partnership with South Korean battery materials company Yulho.

The South Korean government is tightening its circular economy policies for battery materials. Export restrictions are also being implemented for battery waste, so that valuable resources remain in the country. This is also affecting investment and capacity expansion. According to the South Korea battery recycling market analysis, the number of waste electric vehicle batteries in Korea is expected to surge from 2,058 in 2024 to about 20,000 by 2029. Hence, this compliance-driven demand is becoming a stable source of revenue for the recycling industry.

Major chemical and energy companies are venturing into the battery recycling business through acquisitions and joint ventures. These companies bring in investment, processing expertise, and integration capabilities. Their entry is hastening commercialization and improving cost structures. For instance, United States-based Ascend Elements partnered with South Korea-based SK ecoplant and its e-waste recycling subsidiary, in September 2023, redefining trends in the South Korea battery recycling market.

The EMR’s report titled “South Korea Battery Recycling Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Material

Key Insight: Material recovery approaches are influenced by value concentration and compliance needs. Metals lead the South Korea battery recycling market growth because of reuse value and stable downstream markets. Electrolytes are emerging as important materials because of the need for stricter waste management. Plastics and other materials have become secondary, with a focus on disposal and reuse. Emphasis on the material type is based on the recyclers’ need to balance profitability with compliance needs while catering to battery makers looking for full-service recyclers rather than material processors.

Market Breakup by Recycling Process

Key Insight: Breakup of the South Korea battery recycling market based on the recycling process of lithium-ion batteries indicates the maturity of technology and the variety of feedstocks. Hydrometallurgy is increasingly being preferred over lithium-ion batteries because of the higher recovery rate and lower energy intensity. Pyrometallurgy is still applicable for mixed and contaminated materials.

Market Breakup by Processing State

Key Insight: Processing priorities in the South Korea battery recycling market are increasingly becoming lifecycle driven. Material extraction dominates because recovered metals can be directly reused in cathode manufacturing, supporting supply security and margin stability. Second-life applications are expanding their shares as diagnostic tools improve accuracy around residual capacity and safety performance. In September 2025, Stellantis announced that the company is advancing its activities in the field of High Voltage Batteries Repurposing, also known as Second Life Batteries. Reuse delays full recycling while creating interim value for storage and backup systems.

Market Breakup by Chemistry

Key Insight: Lithium-based chemistries continue to contribute to the South Korea battery recycling market revenue due to the scale of electric vehicles. Nickel-based chemistries are also growing popular with the development of cathode materials and higher energy density. Lead-acid chemistries continue to be a stable market due to the established collection infrastructure and predictable industrial demand. In November 2025, researchers developed an eco-friendly recycling technology that extracts 99% pure nickel and cobalt from waste batteries. Other chemistries are used in niche markets where the economics of recycling are less important than regulatory requirements.

Market Breakup by Source

Key Insight: Source dynamics in South Korea battery recycling market are defined by scale and consistency. Automotive batteries lead due to volume concentration and structured collection systems. Industrial batteries provide stable growth supported by ESS and backup power replacement cycles. Consumer electronics remain fragmented, creating logistical and sorting challenges. Recycling efficiency depends on collection reliability and chemistry uniformity. Recyclers are prioritizing sources that support predictable output and contract-based supply.

By material, metals account for the dominant share due to strong reuse demand from cathode makers

Metals emerge to be the most crucial material in the South Korea battery recycling market. Recyclers target nickel, cobalt, lithium, and manganese due to their direct entry into the country’s cathode production lines. Battery manufacturers find the use of recycled metals advantageous to minimize risks associated with importation and price fluctuations. Recyclers are improving their separation technologies to produce higher-quality materials for battery applications instead of producing concentrates.

Electrolyte recycling is gaining traction as the South Korea battery recycling market shifts from metal-focused business models. The increasing amount of EV scrap waste is pushing the industry to adopt safer and more efficient treatment technologies. Korean recyclers are investing in solvent recovery, neutralization, and containment technologies to minimize the costs associated with the disposal of hazardous materials. Umicore and HS Hyosung Advanced Materials also partnered to industrialize silicon-anode materials for EV batteries in November 2025. Although direct revenue generation is still low, electrolyte recycling enhances plant efficiency and compliance with regulations.

By recycling process, hydrometallurgy registers the dominant market share due to higher recovery efficiency standards

Hydrometallurgy is the most prominent battery recycling method in South Korea because of its efficiency in terms of high recovery rates and purity of materials. Chemical leaching and solvent extraction enable the selective extraction of cathode-grade lithium, nickel, and cobalt. This method is preferred by recyclers for lithium-ion batteries because it requires lower energy input compared to other thermal methods. Continuous improvements in reagent and filtration process optimization are enhancing economic viability. This method also complies with environmental regulations, making it more scalable.

The lead-acid battery recycling category is further growing its share in the South Korea battery recycling market as a result of process improvements. The category is upgrading smelting technology, pollution control, and material processing to comply with more stringent environmental regulations. In November 2025, lead-acid battery regeneration company, REPOWERTEK unveiled its groundbreaking fifth-generation "PRIME Series" regenerator, along with an innovative industrial workshop and platform business model. Further, industrial and backup power batteries offer a constant supply of materials to the recycling industry.

By processing state, material extraction dominates the market due to direct integration into battery supply chains

Material extraction dominates the South Korea battery recycling market scope as recyclers focus on reclaiming battery-grade inputs. This stage generates the highest commercial value by supplying metals back into cathode manufacturing. Companies are investing in automated dismantling, shredding, and refining systems to improve yield consistency. In September 2025, Telescope’s proprietary ReCRFT process achieved >99.9% pure Li2CO3 from battery recycling brines. Extraction-focused facilities benefit from long-term agreements with battery producers seeking stable recycled inputs. This segment supports national goals for raw material security and circular economy development.

Second-life battery processing is also contributing to the South Korea battery recycling market revenue as EV batteries retire with usable capacity. Companies are assessing modules for energy storage, backup power, and industrial applications. Repackaging extends asset life and delays material extraction. Korean recyclers are partnering with utilities and ESS developers to deploy refurbished systems. Improved diagnostics are increasing confidence in second-life performance. While margins vary, this segment supports sustainability objectives and reduces immediate recycling pressure.

Lithium-based chemistry dominates recycling due to EV battery volume concentration

Lithium-based batteries represent the dominant chemistry category boosting the overall South Korea battery recycling market penetration as electric vehicle adoption accelerates across the nation. Recyclers are optimizing hydrometallurgical processes for NCM and NCA chemistries to improve lithium, nickel, and cobalt recovery efficiency. This segment attracts the highest capital investment because recovered materials are directly reintegrated into domestic cell and cathode manufacturing. Process innovation focuses on impurity control, yield stabilization, and consistent output quality. For instance, Lithion Technologies recycles lithium-ion batteries in a sustainable way to create a greener future, since June 2024.

Nickel-based battery chemistries are being recognized as the fastest-growing focus area for recyclers with the development of high nickel cathode materials. Recycling companies are optimizing the separation and purification processes to efficiently process higher levels of nickel without affecting the yields. This category is also benefiting from the battery industry’s drive for higher energy density and longer ranges. Improved nickel recovery has a profound effect on revenue per ton and improves the economics of recycling.

By source, automotive batteries capture the maximum market share due to predictable collection and scale economics

Automotive batteries dominate feedstock availability in the South Korea battery recycling market due to accelerating electric vehicle adoption and rising manufacturing scrap volumes. Recyclers align capacity planning with automaker production schedules to manage consistent inflows. Predictable chemistry profiles improve processing efficiency and yield stability. Long-term supply agreements with automotive OEMs support investment planning and facility expansion. This segment also benefits from centralized collection systems and regulatory traceability requirements. In July 2025, Carmaker Toyota Tsusho announced a strategic partnership with South Korean lithium-ion battery maker LG Energy Solution to establish a new joint venture focused on recycling electric vehicle (EV) batteries in the United States.

Industrial batteries are a new source segment that is growing at a fast rate due to the installation of ESS and the need for backup power. Telecommunications networks, data centers, and manufacturing plants provide a constant source of replacement business. Recycling companies find this source segment appealing because of the predictable chemistry and manageable size.

The industry is becoming more structurally competitive and consolidated. Leading South Korea battery recycling market players are ensuring long-term supply of key materials. Recycling companies are upgrading hydrometallurgical processes, automating, and implementing traceability to ensure sufficient cathode material quality. Chemical and metal producers are entering the industry through joint ventures, which bring scale and processing knowledge. The industry is seeing a shift in competitive differentiation from volume processing to recovery rate, purity, and contract reliability.

The most lucrative opportunities exist in closed-loop recycling contracts, high-nickel material recovery, and second-life battery use for energy storage systems. South Korea battery recycling companies that match recycling capacity with battery production cycles have better negotiation power and utilization stability. The ability to comply with regulations is also emerging as a competitive strength. Those companies with the strongest technology, feedstock, and downstream integration are better equipped to protect margins and grow sustainably as the recycling industry evolves from waste management to a strategic materials business.

Established in 2020 and headquartered in Seoul, South Korea, LG Corp., through LG Energy Solution, is embedding battery recycling into its broader cell manufacturing strategy. The company is prioritizing recovery of nickel, cobalt, and lithium from production scrap and end-of-life batteries. Recovered materials are directed back into cathode supply chains to reduce import exposure.

Founded in 1970 and headquartered in Yongin, South Korea, Samsung SDI positions battery recycling as a core element of its premium cell strategy. The company is forming recycling partnerships to secure material traceability and recycled content for high-performance batteries.

Established in 2000 and headquartered in Gunsan, South Korea, SungEel HiTech is a specialized battery recycling company focused on hydrometallurgical processing. The firm concentrates on recovering lithium, nickel, cobalt, and manganese from lithium-ion batteries. SungEel HiTech supplies recovered materials to domestic and international battery manufacturers.

Founded in 1949 and headquartered in Seoul, South Korea, Young Poong brings decades of metallurgical expertise into battery recycling operations. The company focuses on recovering valuable metals through industrial-scale processing systems. Young Poong leverages existing smelting, refining, and materials handling capabilities to improve recycling efficiency.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include SK Ecoplant Co. Ltd., COSMO & Company Inc., Korea Zinc Inc., JaeYoungTech. Ltd., and Green Li-ion Pte Ltd., among others.

Unlock the latest insights with our South Korea battery recycling market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

South Korea Circular Economy And Sustainability Policy

South Korea Electronic Waste Management Industry

South Korea Battery Materials Recovery Technologies

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 214.62 Million.

The market is projected to grow at a CAGR of 6.00% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of around USD 384.35 Million by 2035.

Stakeholders are securing long-term feedstock contracts, upgrading recovery technologies, integrating traceability systems, forming strategic joint ventures, and expanding second-life applications to strengthening supply resilience and profitability.

The key trends aiding the market expansion include the establishment of battery recycling units by companies, technological innovations, and increasing environmental concerns.

The different recycling processes are hydrometallurgy, pyrometallurgy, lithium-ion battery recycling process, and lead-acid battery recycling process.

The major segments based on battery chemistry are lead-acid battery, nickel based, and lithium based, among others.

The key players in the market include LG Corp. (LG Energy Solution Ltd.), Samsung SDI Co. Ltd., SungEel Hitech Co. Ltd., Young Poong Co., Ltd., SK Ecoplant Co. Ltd., COSMO & Company Inc., Korea Zinc Inc., JaeYoungTech. Ltd., and Green Li-ion Pte Ltd., among others.

Feedstock variability, high capital requirements, evolving environmental regulations, technology scale-up risks, and margin sensitivity to metal price fluctuations continue challenging recyclers seeking long-term profitability and operational stability.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material |

|

| Breakup by Recycling Process |

|

| Breakup by Processing State |

|

| Breakup by Chemistry |

|

| Breakup by Source |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.