Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

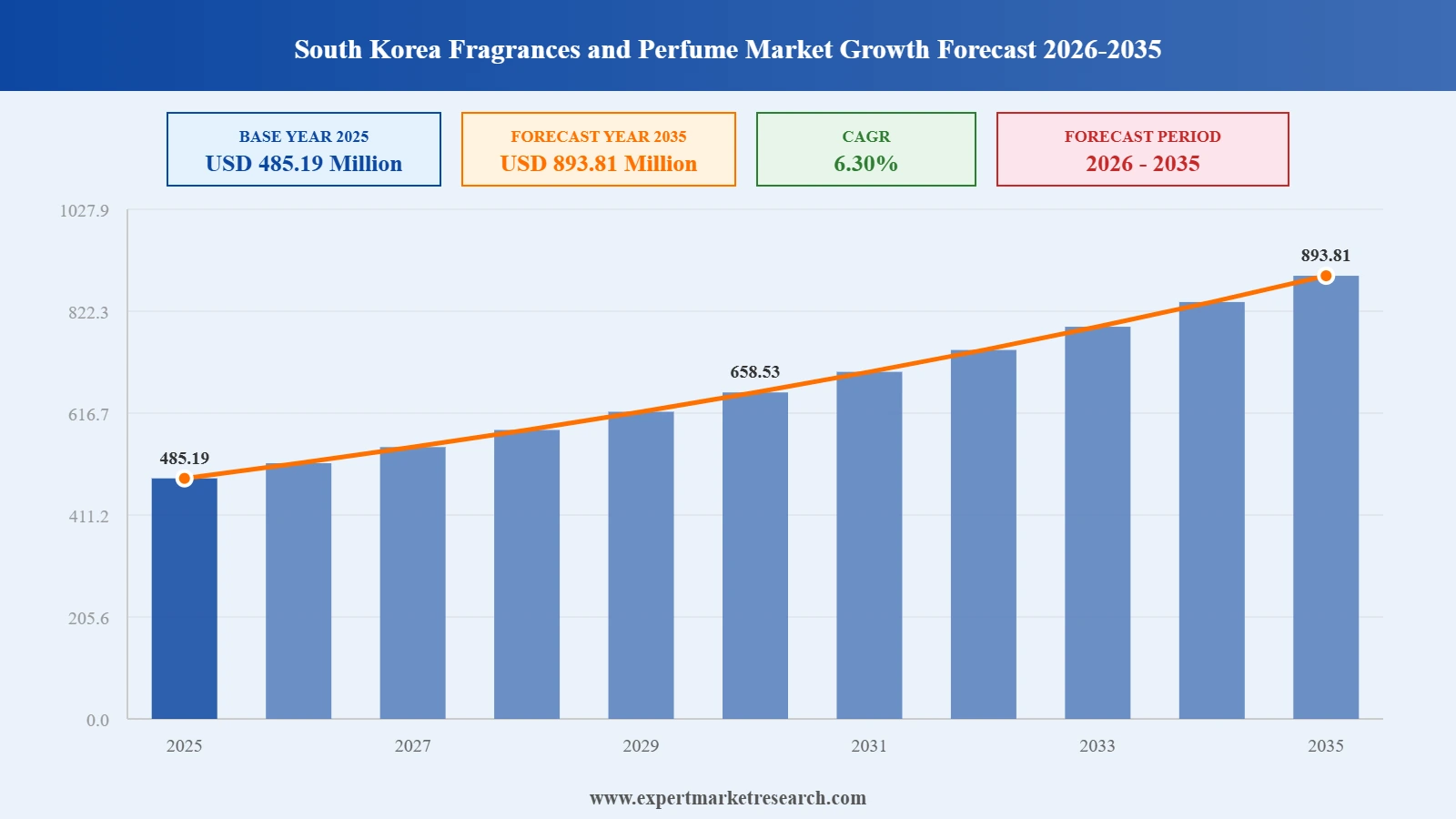

The South Korea fragrances and perfume market reached a value of USD 485.19 Million at 2025 and is projected to expand at a CAGR of around 6.30% during the forecast period of 2026-2035. With growing demand for niche and artisanal fragrances, rising influence of K-beauty on scent preferences, expanding online and duty-free retail channels, and increasing adoption of premium and eco-friendly perfume products, the market is expected to reach USD 893.81 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| South Korea Fragrances and Perfume Market Report Summary | Description | Value |

| Base Year | USD Million | 2025 |

| Historical Period | USD Million | 2019-2025 |

| Forecast Period | USD Million | 2026-2035 |

| Market Size 2025 | USD Million | 485.19 |

| Market Size 2035 | USD Million | 893.81 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 6.30% |

| CAGR 2026-2035 - Market by Consumer Group | Women | 6.6% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 6.5% |

The South Korea fragrances and perfume market is undergoing a significant structural shift, with niche and artisanal brands reshaping consumer expectations around scent identity. The convergence of K-beauty influence, premiumisation, and digital retail innovation is redefining how fragrances are discovered, purchased, and experienced in the country. These changes are creating new growth pathways for both established global houses and homegrown Korean labels.

Spanish luxury brand Loewe Perfumes opened its first global flagship perfume store in Seoul's Seongsu-dong district in January 2026. The store reflects growing international brand interest in the South Korea fragrances and perfume market, leveraging the country's cultural cachet and its rising reputation as a global fragrance destination.

In October 2025, The Estee Lauder Companies inaugurated its Fragrance Atelier within La Maison des Parfums in Paris. The facility serves as a global innovation hub for brands including Jo Malone London and Tom Ford, using AI-enabled creation processes to accelerate scent development, with implications for prestige fragrance offerings in South Korea.

Shinsegae Duty Free expanded its premium fragrance portfolio with the debut of Korean niche brand Borntostandout at its Myeong-dong flagship in May 2025. The launch included a pop-up activation on the store's Iconic Zone floor, blending K-culture storytelling with high-end fragrance retail to attract both domestic and international travellers.

Seoul-based niche perfume brand Borntostandout raised Series A capital in February 2025, led by Touch Capital with participation from L'Oreal's venture fund BOLD. The investment will support the brand's global offline expansion, particularly across Europe and the United States, reinforcing the rising stature of Korean-origin fragrance labels.

South Korea's fragrance exports reached a record USD 6.52 million in January 2026, the highest monthly total since records started in 1988 according to the Korea International Trade Association. The country also posted its first perfume trade surplus with the United States in 28 years, signalling sustained momentum in South Korea fragrances and perfume market growth.

K-perfume sales at Lotte Department Store grew more than 35% year-on-year in 2024, reflecting strong demand among millennial and Gen Z consumers who favour individualistic, story-driven scents. The retailer plans to position domestic fragrance brands as a key content category, further strengthening the South Korea fragrances and perfume market landscape.

In early 2026, Spanish beauty conglomerate Puig and The Estee Lauder Companies entered discussions about a potential business combination. If completed, the merger could create a luxury beauty group valued at approximately USD 40 billion, consolidating a powerful South Korea fragrances and perfume portfolio spanning brands like Byredo, Jo Malone, and Tom Ford.

In May 2025, YSL Beauty launched its LIBRE L'Eau Nue scent, targeting consumers who prefer lighter, sun-inspired fragrance formats. The release aligns with the growing preference for everyday luxury scents in the South Korea fragrances and perfume market, where mood-driven and seasonal offerings continue to gain traction among younger buyers.

Kolmar Korea presented eight proprietary fragrances at Cosmoprof Asia in Hong Kong in late 2025, featuring city-inspired scents such as Seoul Foresto and Jeju Breeze crafted from local ingredients. The collection attracted interest from Russian and Vietnamese companies, with export contracts in development, enhancing the global reach of the South Korea fragrances and perfume industry.

The report of Expert Market Research's titled "South Korea Fragrances and Perfume Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

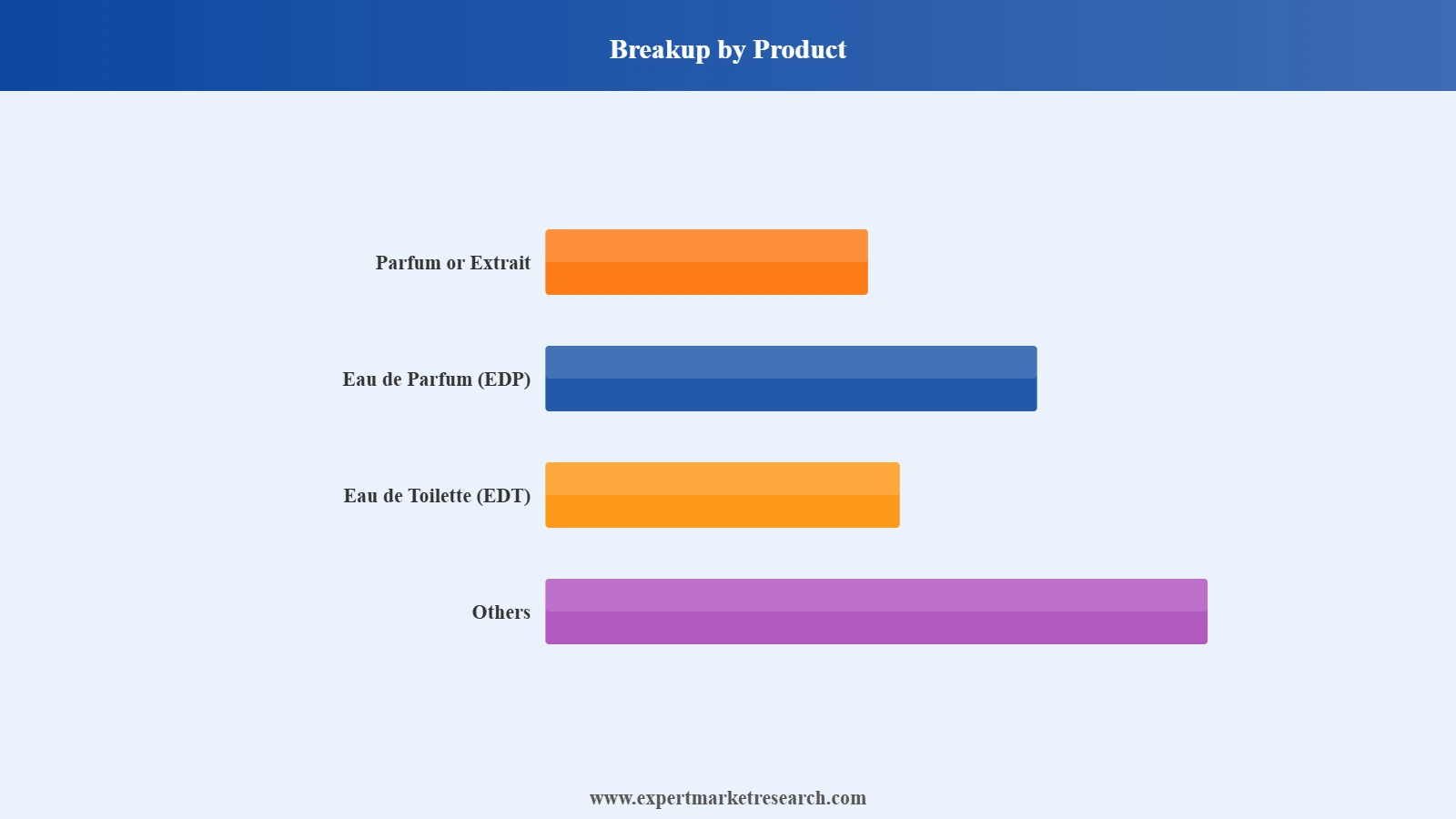

Market Breakup by Product

Key Insight: Eau de Parfum (EDP) anchors the majority of the demand in the South Korea fragrances and perfume market because it balances longevity, sillage, and value that suit both daily routines and luxury gifting occasions. Korean consumers increasingly prioritise scent performance, which positions EDP as the concentration of choice across department stores, online platforms, and duty-free outlets. Parfum or Extrait is experiencing rapid growth as well, particularly among shoppers drawn to exclusivity and artisanal craftsmanship, while Eau de Toilette remains a popular entry-level option for casual and cost-conscious consumers. Other formats, including body mists and hair perfumes, are expanding as personalisation and layering trends gain momentum.

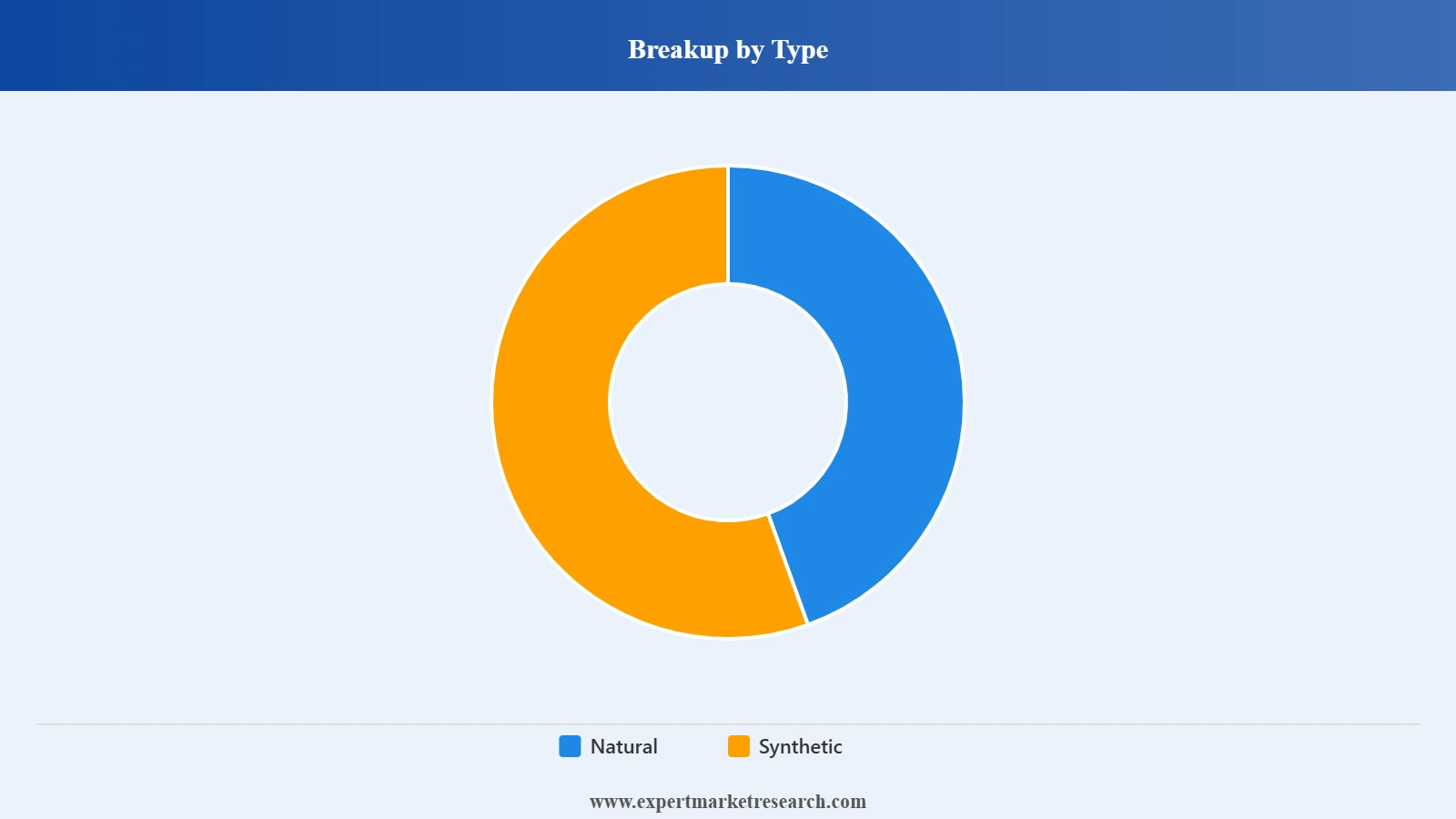

Market Breakup by Type

Key Insight: Natural fragrances hold the dominant share of the South Korea fragrances and perfume market, supported by a strong consumer preference for clean, transparent, and eco-conscious beauty products. The K-beauty ethos of ingredient purity extends naturally into fragrance purchasing decisions, with Korean buyers showing a willingness to pay more for formulations that feature botanicals, essential oils, and sustainably sourced materials. Several domestic brands, including Nonfiction and Tamburins, have built their identity around naturally derived and vegan-friendly scent profiles. Synthetic fragrances continue to play a significant role, especially in the mass and mid-tier product segments, where cost efficiency and creative versatility in scent composition remain important. Advances in green chemistry are narrowing the distinction between natural and synthetic, with many brands adopting blended approaches.

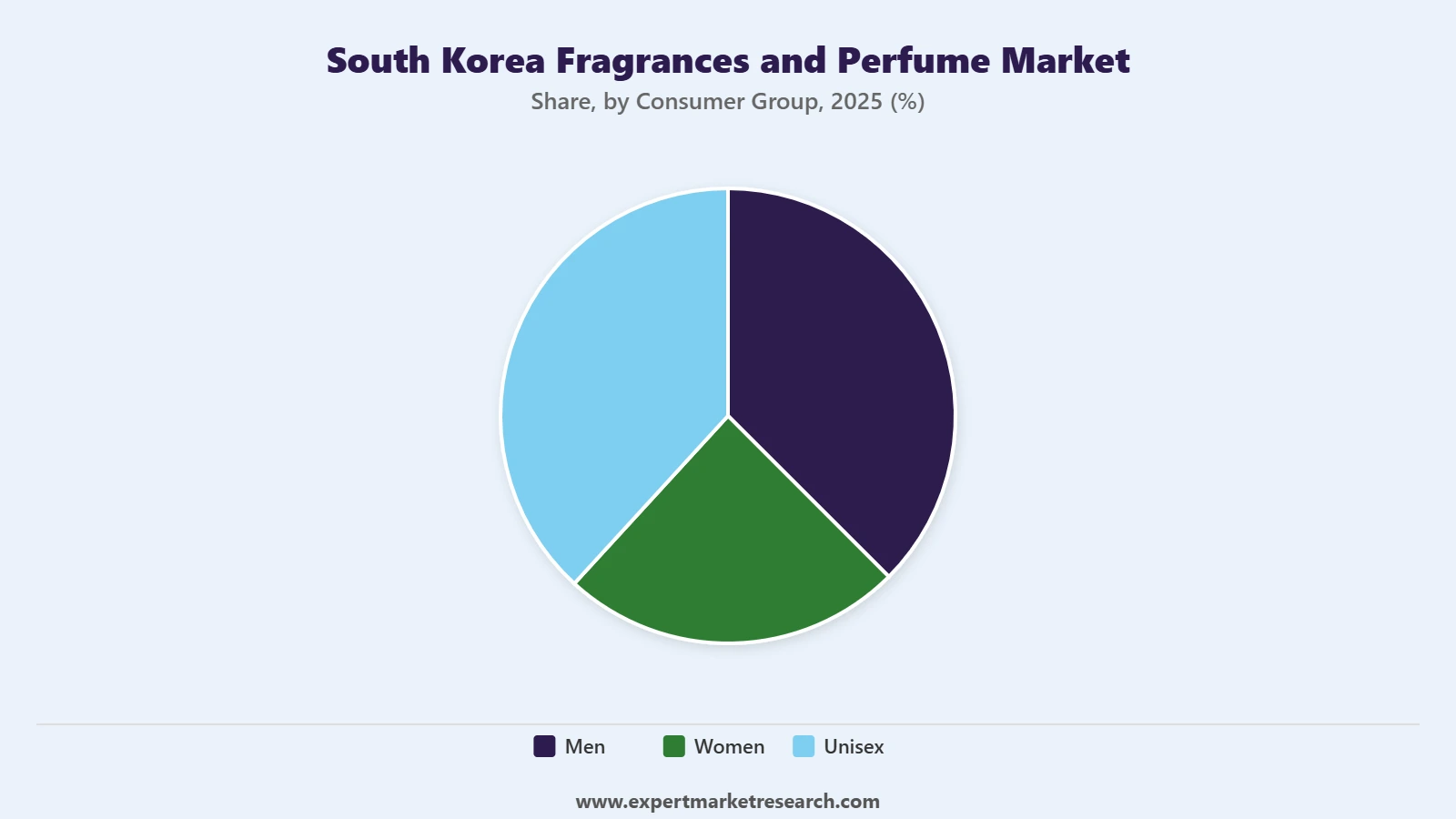

Market Breakup by Consumer Group

Key Insight: Women continue to represent the largest consumer group in the South Korea fragrances and perfume market, driven by longstanding beauty rituals and increasing incorporation of fragrance into daily self-care routines. A growing number of female consumers are exploring niche and luxury perfumes, seeking scents that align with their personal identity. However, the men's segment is gaining meaningful traction as personal grooming becomes more culturally normalised among South Korean males, supported by celebrity endorsements and social media influence. The unisex category is one of the fastest-growing segments, reflecting a generational shift among Gen Z and millennial consumers who prefer gender-neutral scents. Clean, woody, and musky profiles that transcend traditional gender boundaries are particularly popular in this segment.

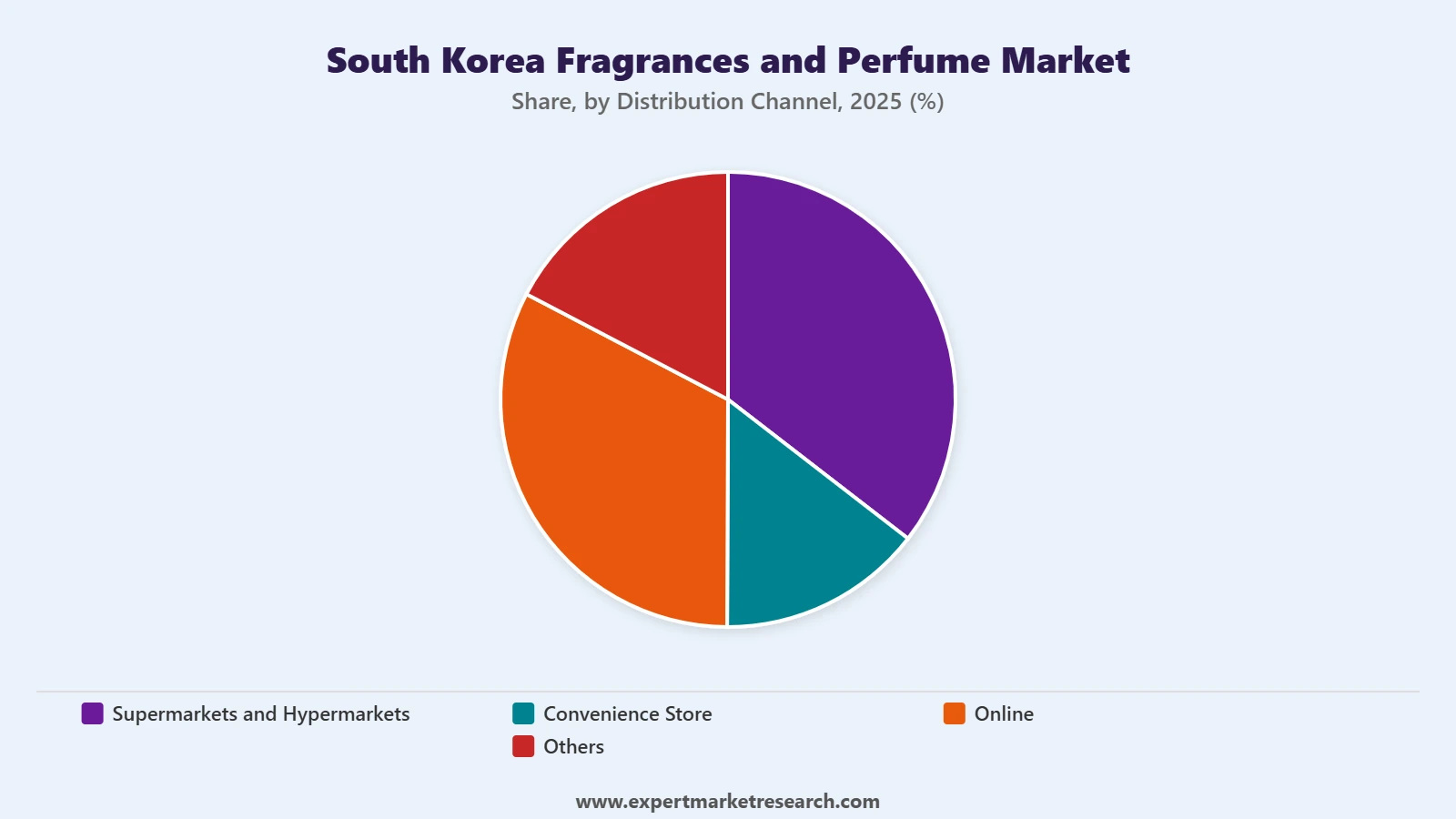

Market Breakup by Distribution Channel

Key Insight: Supermarkets and hypermarkets remain a key distribution channel in the South Korea fragrances and perfume market, particularly for mass-market and everyday scent products that benefit from high foot traffic and impulse purchasing. However, the online channel is the fastest-growing segment, driven by Korea's highly connected digital ecosystem, where platforms like Olive Young, Coupang, and Naver Shopping offer curated fragrance discovery experiences. Online sampling programmes, AI-powered scent recommendation tools, and influencer-driven product reviews are reshaping how consumers discover and purchase fragrances. Convenience stores cater to quick, affordable fragrance options and body mists, while the Others category includes department store counters, duty-free shops, pop-up stores, and brand-operated boutiques that serve as experiential touchpoints for premium and niche perfume brands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product, Eau de Parfum (EDP) dominates the market due to its ideal balance of longevity, performance, and premium value

Eau de Parfum leads the South Korea fragrances and perfume market primarily because it meets the Korean consumer's expectation for scents that last throughout the day without being overpowering. Department stores such as Lotte, Shinsegae, and Hyundai dedicate significant floor space to EDP offerings from international houses like Chanel, Dior, and Jo Malone, reflecting the category's commercial importance. The format also benefits from its positioning as an accessible luxury, making it popular for gifting and personal indulgence.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Parfum or Extrait is emerging as a notable growth area, particularly among fragrance enthusiasts and collectors seeking richer, more concentrated compositions. In May 2025, Shinsegae Duty Free launched the Korean niche brand Borntostandout, which recently released its Extrait Extreme collection with a 60% oil concentration, indicating growing consumer appetite for higher-end fragrance formats. The shift toward ultra-premium concentrations is reshaping the South Korea fragrances and perfume market's upper tier.

By Type, Natural accounts for the dominant share of the market due to strong consumer alignment with clean beauty values

Natural fragrances dominate the South Korea fragrances and perfume market because Korean consumers have deeply internalised the principles of ingredient transparency and purity that define the broader K-beauty movement. Buyers in this market actively seek out formulations free from harmful chemicals, favouring plant-derived essential oils and sustainably harvested raw materials. This preference is reinforced by a regulatory environment that encourages clean labelling and by a retail culture that rewards brands offering detailed ingredient disclosure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Synthetic fragrances remain significant, particularly in mass-market segments where cost-effective production and creative scent replication are priorities. However, the gap between natural and synthetic is narrowing as brands adopt hybrid formulations. In late 2025, Kolmar Korea showcased proprietary fragrances using locally sourced ingredients at Cosmoprof Asia, highlighting how manufacturers are blending natural Korean botanicals with modern synthetic techniques to produce scents that are both commercially viable and culturally authentic within the South Korea fragrances and perfume industry.

By Consumer Group, Women accounts for the dominant share of the market due to established beauty routines and rising interest in premium scents

Women represent the largest consumer group in the South Korea fragrances and perfume market, underpinned by a well-established culture of multi-step beauty regimens that increasingly include fragrance as a finishing touch. Female consumers are the primary buyers across all product categories and distribution channels, with particular strength in the EDP and luxury parfum segments. The influence of K-pop idols, K-drama celebrities, and beauty content creators further drives purchasing decisions among female audiences of all age groups.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The unisex segment is gaining strong momentum, particularly among younger consumers who reject rigid gender classifications in personal care. Korean niche brands such as Nonfiction and Borntostandout have built their product lines around gender-neutral scent profiles, and this approach resonates with a generation that views fragrance as a mode of self-expression rather than conformity. In February 2025, L'Oreal's BOLD venture fund backed Borntostandout, whose collection of unisex scents continues to attract a growing international following, pointing to the expanding reach of Korean gender-neutral fragrances in the South Korea fragrances and perfume market.

By Distribution Channel, Online accounts for the fastest-growing share of the market due to Korea's advanced digital retail ecosystem and evolving consumer discovery habits

Online channels are rapidly gaining dominance in the South Korea fragrances and perfume market, powered by the country's exceptionally high internet penetration and a tech-savvy consumer base that increasingly discovers and purchases scents through digital platforms. Retailers such as Olive Young, Coupang, and Naver Shopping have expanded their fragrance categories significantly, offering curated collections, AI-driven scent matching tools, and subscription-based sampling kits. The launch of the Jo Malone London AI Scent Advisor in December 2025 by The Estee Lauder Companies exemplifies how brands are investing in digital-first experiences to bridge the sensory gap in online fragrance shopping.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Supermarkets and hypermarkets continue to hold a substantial share of fragrance distribution in South Korea, serving as accessible touchpoints for mass-market and mid-tier products. However, the Others category, which includes department store counters, duty-free shops, and branded boutiques, plays a critical role in premium and luxury fragrance sales. In January 2026, Loewe Perfumes opened its first global flagship store in Seoul's Seongsu-dong district, underscoring the strategic importance of physical experiential retail for high-end brands operating within the South Korea fragrances and perfume market.

The South Korea fragrances and perfume market features a competitive landscape that blends established international luxury houses with a rising wave of domestic niche brands. Global players such as Chanel, Dior, and Estee Lauder hold strong positions through their established retail networks, brand heritage, and extensive distribution via department stores and duty-free channels. These companies benefit from deep consumer trust and substantial marketing investments that reinforce brand desirability.

At the same time, the competitive dynamics are shifting as Korean consumers increasingly gravitate toward locally rooted, story-driven fragrance brands. Companies like ELCA Korea and Puig are adapting by tailoring their portfolios and marketing strategies to reflect Korean cultural sensibilities. Meanwhile, niche entrants are challenging traditional market hierarchies by offering distinctive scent experiences that emphasise individuality and artistic expression, creating a more fragmented but dynamic market structure.

Founded in 1990 and headquartered in South Korea, ELCA Korea Co., Ltd. manages prestige fragrance portfolios including Estee Lauder, Jo Malone London, and Le Labo across department stores, travel retail, and online channels. The company specialises in localising international brand narratives through tailored storytelling and culturally relevant collaborations. ELCA Korea focuses on sampling strategies and digital engagement to build consumer loyalty, while maintaining global brand positioning and price architecture for the Korean market.

Established in 1914 and headquartered in Barcelona, Spain, PUIG, S.L. is a global fragrance and fashion group with an expanding presence in the Korean market. Through brands such as Carolina Herrera, Rabanne, Byredo, and Penhaligon's, the company leverages high-service department store counters, travel retail, and selective boutiques. PUIG's Asia-Pacific revenue grew 21.7% on a like-for-like basis in 2025, and its fragrance and fashion division accounts for 72% of total net revenue, underscoring its strategic focus on the scent category.

CHANEL is a privately held French luxury house with a long-standing presence in the South Korea fragrances and perfume market. The brand maintains a strong foothold through iconic fragrance lines and high-visibility retail placements across Lotte, Shinsegae, and Hyundai department stores. CHANEL invests consistently in experiential retail, seasonal limited editions, and influencer partnerships to sustain brand desirability among Korean consumers who value heritage, craftsmanship, and timeless elegance in their fragrance choices.

Founded in 1946 and headquartered in New York, The Estee Lauder Companies Inc. is one of the world's leading manufacturers and marketers of prestige beauty products. The company's fragrance portfolio includes Jo Malone London, Tom Ford, Le Labo, and Kilian Paris. In October 2025, it opened a global Fragrance Atelier in Paris to accelerate innovation using AI and neuroscience. The company's fragrance division recorded 6% sales growth in Q2 of fiscal year 2026, reflecting its strategic investment in this category.

Other key players in the market are Gianni Versace S.r.l., Burberry Limited, Christian Dior SE, Tom Ford International Llc, Bulgari S.p.A., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the South Korea fragrances and perfume market 2026 with our comprehensive research report. From the latest product launches and consumer preference shifts to distribution channel dynamics and competitive developments, this report equips you with the clarity to make decisive strategic moves. Whether you are developing a new fragrance line, expanding into the Korean beauty sector, or evaluating investment opportunities, download your free sample today and unlock the opportunities shaping the future of fragrances and perfume in South Korea.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 485.19 Million.

The market is projected to grow at a CAGR of 6.30% between 2026 and 2035.

The South Korea fragrances and perfume market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 893.81 Million by 2035.

Stakeholders are expanding niche lines, localizing storytelling, investing in boutiques, scaling online sampling, and partnering with Korean influencers, boosting the South Korea fragrances and perfume market growth.

The growing demand for bespoke and premium products and the growth of social media and celebrity endorsements are the key trends in the South Korea fragrances and perfume market.

The dominant types of fragrances and perfumes in the industry are natural and synthetic.

The leading distribution channels in the market are Supermarkets and Hypermarkets, Convenience Store, and online, among others.

The key players in the market include ELCA Korea Co., Ltd., PUIG, S.L., Gianni Versace S.r.l., Burberry Limited, CHANEL, The Estée Lauder Companies Inc., Christian Dior SE, Tom Ford International LLC, Bulgari S.p.A., and Others.

Companies face crowded luxury counters, rising marketing costs, fast-changing Korean taste cycles, dependence on department stores, plus pressure to prove sustainability claims while protecting margins in a price-sensitive, promotion-heavy environment.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Type |

|

| Breakup by Consumer Group |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.