Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The Global Textile Dyes Market reached a value of USD 10.75 Billion at 2025 and is projected to expand at a CAGR of around 6.10% during the forecast period of 2026-2035. With surging demand for coloured textiles, polyester-led synthetic-fibre growth, sustainable and low-water dye chemistry investment, and tighter brand-led environmental compliance, the market is expected to reach USD 19.43 Billion by 2035.

Compound Annual Growth Rate

6.1%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Textile Dyes market growth is being driven by accelerating sustainability investment in low-water reactive chemistries, surging polyester and synthetic-fibre demand, large-scale capex from Indian suppliers like Atul and Kiri, and rising brand-led compliance with OEKO-TEX, GOTS, and ZDHC standards across global apparel value chains.

Sustained brand-side and venture-capital investment in plant-based and bio-based textile dye chemistries continued through 2025, including bio-derived indigo, fermentation-based reactive dyes, and microbial colorants. Several startups partnered with global apparel brands and incumbent suppliers including LANXESS AG and Atul Ltd. to scale pilot manufacturing. The trend is reshaping innovation pipelines in the textile dyes industry and complementing low-water reactive chemistry advances such as Huntsman/Archroma's AVITERA SE, supporting the broader push toward circular and lower-impact apparel value chains.

Atul Ltd. expanded its sulphur black dye manufacturing capacity to 26,000 MTA, with the new plant equipped with a zero-liquid-discharge (ZLD) facility that aligns with the company's sustainability commitments. Sulphur black is a heavily used dye in cotton denim and indigo-style fabric production, and Atul's GOTS-approved and OEKO-TEX Standard 100 compliant grades target export-oriented apparel manufacturing in India, Bangladesh, and Vietnam. The expansion reinforces Atul's leadership in cellulosic dye chemistries and supports brand-led demand for traceable, low-impact colorants.

Huntsman Textile Effects, now operating as part of Archroma following the 2023 acquisition, continued to scale its third-generation AVITERA ROSE SE poly-reactive dyes range. The chemistry reduces water and energy consumption by up to 50% and increases mill output by approximately 25%, lowering per-kilogram water use from 30-40 litres to roughly 15-20 litres. Adoption is being driven by global apparel brands seeking ZDHC- and OEKO-TEX-aligned dyeing partners, and by mills in Bangladesh, Vietnam, India, and Turkey upgrading to lower-impact reactive chemistries.

Atul Ltd. completed an expansion of its liquid epoxy resin capacity to 50,000 tpa from 30,000 tpa effective 25 October 2024, with an approved investment of INR 200 crore. While the project sits adjacent to Atul's dyes and dyestuffs business, it reflects the company's broader capex programme aligned with the integrated chemicals platform that supports its specialty dyes manufacturing footprint in Gujarat. Atul's specialty dyes facility, valued at INR 600 crore, supports an annual production increase of 15,000 metric tons of dyes for textile and industrial customers.

Kiri Industries Ltd. continued to expand its reactive and disperse dye manufacturing capacity in Gujarat through 2024, supporting the company's leadership across export markets in Europe, Bangladesh, Vietnam, and Turkey. Kiri's product portfolio spans reactive, vat, acid, direct, disperse, and basic dyes, alongside dye intermediates, and the company has invested in effluent-treatment, ZLD, and product-stewardship programmes. The expansion is positioned to capture share from less compliant suppliers as international brands tighten supplier-onboarding requirements around environmental standards.

Sustainable dye chemistry has shifted from differentiator to default. Huntsman Textile Effects (now part of Archroma) is scaling its third-generation AVITERA ROSE SE poly-reactive dyes, which cut water use by up to 50% and lift mill output by 25%, while Atul Ltd.'s expanded sulphur black plant operates with zero-liquid-discharge facilities. The trend is driven by global apparel brands enforcing ZDHC and OEKO-TEX requirements on their supplier base, by water-stress regulation in dyeing hubs across India, Bangladesh, and China, and by retailer-led traceability commitments. Sustainability now sits at the centre of dye-supplier selection across reactive, disperse, and vat categories.

Polyester is the largest and fastest-growing fibre globally, and disperse dyes are the chemistry of choice for polyester colouration. Athleisure, fast-fashion, automotive interiors, and home-textile applications are driving polyester volumes, and disperse-dye suppliers including Huntsman/Archroma's TERESIL W/WW range — bluesign-approved and OEKO-TEX Standard 100 certified — are gaining share. The trend matters because disperse dyes carry stricter sublimation-fastness, washing, and chlorine resistance requirements, supporting higher ASPs versus commoditised reactive grades. Indian and Chinese suppliers are investing aggressively in disperse capacity to capture share in Vietnam, Bangladesh, and Turkey-served export markets.

Indian textile dye suppliers are entering a structural capex up-cycle. Atul Ltd. completed a 26,000 MTA sulphur black expansion with ZLD facilities and continues to invest in its INR 600 crore specialty dyes facility (15,000 MTA capacity). Kiri Industries is expanding reactive and disperse capacity in Gujarat, and Colorant Limited is scaling intermediates production. The trend matters because India's tightening environmental enforcement, combined with brand-led pull, is consolidating supply around compliant operators with ZLD, traceable upstream sourcing, and OEKO-TEX/GOTS approvals — accelerating the displacement of sub-scale, non-compliant capacity domestically and globally.

Bio-based and plant-based dye chemistry pipelines are maturing into commercial-pilot scale. Bio-derived indigo, fermentation-based reactive dyes, microbial-pigment platforms, and natural-extract dyes from companies including Living Ink, Colorifix, and PILI are advancing through brand-led pilots with apparel groups. Incumbents are responding through M&A, joint development, and licensing arrangements. The trend matters because bio-based dyes offer dramatically improved environmental profiles, support higher-margin brand storytelling, and are aligned with regulatory trajectories in the EU and the United States — making early-stage participation a strategic hedge for established suppliers including LANXESS AG, Atul, and Archroma.

The Expert Market Research’s report titled “Global Textile Dyes Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Dye Type

Key Insight: Reactive dyes hold the largest share of the global textile dyes market because cotton, viscose, and other cellulosic fibres remain the largest fibre cohort dyed industrially, and reactive chemistries deliver the most reliable wash- and light-fastness on cellulose. Disperse dyes are the second-largest category and the fastest growing, anchored by polyester's dominance in synthetic-fibre output. Vat dyes lead in indigo and denim applications, while acid and basic dyes serve specialty wool, silk, nylon, and acrylic applications. Atul Ltd.'s sulphur-black expansion, Kiri Industries' reactive/disperse capex, and Huntsman/Archroma's AVITERA ROSE SE rollout reflect the segment's innovation intensity.

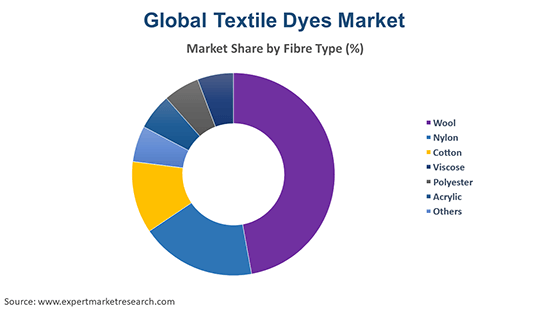

Market Breakup by Fibre Type

Key Insight: Polyester holds the largest fibre-type share of the global textile dyes market, anchored by polyester's dominant share of global fibre output and its widespread use in apparel, athleisure, home textiles, and technical applications. Disperse dyes are the colourant of choice for polyester. Wool, while smaller in volume, is a higher-margin segment and absorbs acid and chrome dyes for premium apparel and carpets. Acrylic - used in sweaters, knitwear, and outdoor textiles - relies on basic and cationic dyes. Cellulosic fibres (cotton, viscose) sit in the Others category in this segmentation but represent the largest single industrial dyeing volume globally for reactive chemistries.

Market Breakup by Region

Key Insight: Asia Pacific commands the dominant share of the global textile dyes market, supported by China's leadership in synthetic-fibre output, India's strong dye-manufacturing base (Gujarat clusters anchored by Atul, Kiri, Colorant), and Bangladesh and Vietnam's rapidly expanding apparel-export industries. Europe holds the second-largest share by value, with strong premium and technical-textile demand and a sophisticated specialty-dye supplier base anchored by LANXESS AG (Germany) and Archroma. North America anchors disperse and reactive dye demand for athleisure, home textiles, and technical applications, while Latin America and the Middle East and Africa offer structural long-term growth tied to apparel exports and rising domestic textile manufacturing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Dye Type: Reactive dyes hold the dominant share of the global textile dyes market, anchored by cotton's continued role as the world's largest natural fibre and reactive chemistry's superior wash- and light-fastness on cellulose. Atul Ltd.'s 2024 sulphur-black expansion to 26,000 MTA - equipped with zero-liquid-discharge facilities - supports the broader cellulosic-dye category. Disperse dyes are the second-largest and fastest-growing category, anchored by polyester's leadership in global fibre output. Huntsman/Archroma's TERESIL W/WW disperse dyes range, bluesign approved and OEKO-TEX Standard 100 certified, exemplifies the premium segment, while reactive innovation is anchored by AVITERA ROSE SE poly-reactive dyes that deliver up to 50% water-use reduction.

By Fibre Type: Polyester holds the dominant fibre-type share of the global textile dyes market, supported by polyester's leadership in global fibre output and its dominance in athleisure, fast-fashion, automotive interiors, and home textiles. Disperse dyes are the colorant of choice for polyester, with Huntsman/Archroma, LANXESS, Atul, and Kiri Industries supplying global mills. Wool absorbs the second-largest share of premium dye chemistries (acid and chrome dyes) and supports premium apparel and carpet applications. Acrylic, used in sweaters and outdoor textiles, relies on basic and cationic dye chemistries. Polyester's dominance is reinforced by the global shift to performance and athleisure apparel, which drives sustained disperse-dye volumes.

By Region: Asia Pacific commands the dominant share of the global textile dyes market by both volume and value, anchored by China's textile manufacturing scale, India's leadership in dye and dye-intermediate production, and Bangladesh's USD 45-billion-plus apparel-export industry. Europe holds the second-largest share, supported by premium-textile and technical-textile demand and the specialty-dye supplier base led by LANXESS AG (Germany) and Archroma. North America's share is anchored by athleisure, home textiles, and technical applications. Indian capex programmes - Atul Ltd.'s sulphur-black expansion and Kiri Industries' Gujarat capacity additions - are reinforcing Asia Pacific's structural lead and absorbing share from less compliant capacity worldwide.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific: Asia Pacific is the dominant regional market for textile dyes by both volume and value. China hosts the world's largest textile and synthetic-fibre manufacturing base and is a major dye producer. India is the largest exporter of dyes and dye intermediates, anchored by Gujarat clusters where Atul Ltd. operates a INR 600 crore specialty dyes facility (15,000 MTA capacity) and an expanded 26,000 MTA sulphur-black plant with zero-liquid-discharge facilities. Kiri Industries Ltd. supplies reactive, disperse, vat, acid, direct, and basic dyes to apparel exporters in Bangladesh, Vietnam, and Turkey. State environmental enforcement, rising effluent-treatment standards, and brand-led ZDHC/OEKO-TEX requirements are consolidating supply around the largest compliant operators across the region.

Europe: Europe is the second-largest regional textile dyes market and is led by LANXESS AG (Germany) and Archroma (formerly including Huntsman Textile Effects), with deep capability across reactive, disperse, vat, and acid chemistries. The region anchors premium, technical, and automotive textile demand, supported by sophisticated apparel and home-textile customers in Italy, France, Germany, the UK, and Switzerland. The EU's REACH regulation, the Textile Strategy under the EU Green Deal, and forthcoming Digital Product Passport requirements are driving brand-led traceability investments and accelerating supplier consolidation. Sustainable chemistries - Huntsman/Archroma's third-generation AVITERA ROSE SE rollout exemplifies the leading edge - are increasingly central to European supplier strategies.

The global textile dyes market is moderately fragmented, with a small group of multinational specialty-chemical leaders - LANXESS AG, Archroma (which absorbed Huntsman Textile Effects), and Clariant - competing alongside large Indian dye exporters including Atul Ltd., Kiri Industries Ltd., and Colorant Limited, Chinese suppliers, and a long tail of regional manufacturers. Competitive priorities have shifted toward sustainable dye chemistry, OEKO-TEX/GOTS/ZDHC alignment, zero-liquid-discharge effluent management, and traceability-grade documentation that meets brand-supplier-onboarding requirements.

Innovation pipelines are increasingly focused on low-water reactive chemistry (AVITERA ROSE SE third-generation), bio-based and fermentation-derived dyes, and circular dyeing technologies. Indian suppliers are scaling capacity at Gujarat clusters with ZLD facilities, while European leaders are investing in lifecycle-assessment tooling and digital traceability. Strategic priorities include vertical integration into dye intermediates, partnerships with apparel brands and bio-based-dye startups, and selective M&A to expand specialty-grade capability.

Founded in 1970 and headquartered in The Woodlands, Texas, USA, Huntsman Corporation is a global manufacturer of differentiated organic chemicals. Huntsman's Textile Effects business - a leading supplier of dyes, chemicals, and effects to the global textile industry - was acquired by Archroma in 2023, and the AVITERA SE poly-reactive dye platform continues to be commercialised under the combined entity, with the third-generation AVITERA ROSE SE rollout reducing water and energy consumption by up to 50% in mill operations.

Founded in 1998 and headquartered in Vadodara, Gujarat, India, Kiri Industries Ltd. is one of the largest manufacturers of dyes, dye intermediates, and basic chemicals in India. The company offers reactive, vat, acid, direct, disperse, basic, and other dye chemistries, and exports to apparel and textile customers in Europe, Bangladesh, Vietnam, Turkey, and the United States. Kiri continues to invest in capacity expansion, effluent treatment, and zero-liquid-discharge facilities, supporting brand-led environmental compliance requirements across global supply chains.

Founded in 1947 and headquartered in Atul (Valsad district), Gujarat, India, Atul Ltd. is a diversified specialty chemicals company with a long heritage in dyes, dye intermediates, and dyestuffs. The company operates a INR 600 crore specialty dyes facility supporting 15,000 MTA of additional production and expanded sulphur-black capacity to 26,000 MTA with zero-liquid-discharge in 2024-25. Atul's GOTS-approved and OEKO-TEX Standard 100 compliant grades target export-oriented apparel customers in India, Bangladesh, Vietnam, and the EU.

Founded in 2004 (as a spin-off of Bayer AG) and headquartered in Cologne, Germany, LANXESS AG is a global specialty chemicals company with a strong textile dyes business covering reactive, vat, acid, and disperse chemistries. LANXESS supplies premium European apparel, technical, and home-textile customers and operates a global manufacturing footprint across Europe, North America, and Asia. The company's portfolio is aligned with EU REACH and ZDHC requirements, supporting a growing customer base prioritising lifecycle traceability and sustainable colorant performance.

Other key players in the market are Colorant Limited, Archroma, Clariant AG, DyStar Group, BASF SE (specialty colorants division), Anand International, Bodal Chemicals Ltd., Aarti Industries Ltd., Sumitomo Chemical Company Limited, Zhejiang Runtu Co., Ltd., Zhejiang Jihua Group Co., Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Textile Dyes Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on dye-chemistry innovations, capacity expansions, and top-growth regions. Whether you are launching a new sustainable dye platform or expanding capacity in Asia Pacific, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Textile Dyes industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 10.75 Billion.

The market is projected to grow at a CAGR of 6.10% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035 to reach USD 19.43 Billion by 2035.

Growth is driven by sustained demand for coloured textiles and synthetic fibres, accelerating sustainability investment in low-water reactive chemistries (AVITERA ROSE SE), large-scale capex from Indian suppliers (Atul's sulphur black expansion to 26,000 MTA, INR 600 crore specialty dyes facility, Kiri Industries' Gujarat capacity additions), brand-led ZDHC/OEKO-TEX/GOTS compliance, and rising bio-based and plant-based dye R&D investment.

Reactive dyes hold the largest share of the market, anchored by cellulosic fibre dyeing, with disperse dyes the fastest-growing category supported by polyester's leadership in synthetic-fibre output. Vat dyes lead in denim and indigo applications, while acid and basic dyes serve specialty wool, silk, nylon, and acrylic applications. Innovation in low-water poly-reactive chemistry (AVITERA ROSE SE) is reshaping the reactive segment.

Key trends include sustainable dye chemistry becoming a default supplier criterion (Huntsman/Archroma AVITERA ROSE SE third-generation, Atul ZLD facilities), polyester and disperse-dye demand outpacing average market growth, the Indian capex up-cycle anchored by Atul and Kiri's Gujarat expansions, and the maturing pipeline of bio-based and plant-based dye chemistries.

The key players in the market include Huntsman Corporation, Kiri Industries Ltd., Atul Ltd., LANXESS AG, Colorant Limited and Others.

North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa are the major regions covered in the market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Dye Type |

|

| Breakup by Fibre Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.