Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

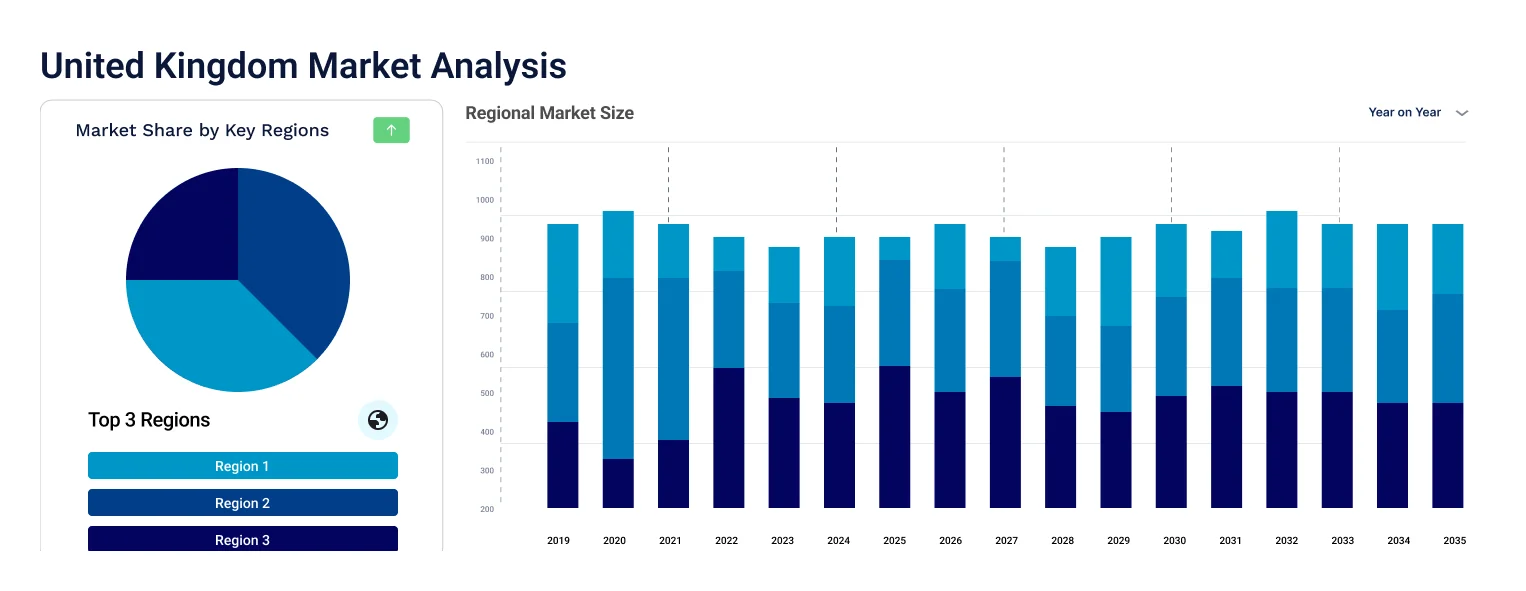

The United Kingdom bunker fuel market attained a value of USD 8.32 Billion in 2025 and is projected to expand at a CAGR of 5.80% through 2035. The market is further expected to achieve USD 14.62 Billion by 2035. Rising offshore wind installation activity is increasing demand for cleaner bunker fuels, creating funding opportunities for suppliers supporting service vessels through dedicated low-emission fuel contracts across United Kingdom coastal energy hubs.

Port electrification and stricter emissions monitoring are reshaping bunker fuel demand in the United Kingdom. Ports are embracing digital fuel reporting systems, while ship owners witness increased scrutiny from charterers. Moreover, fluctuations in the global price of fuel continue to shift the industry towards hedged fuel supply agreements. Consequently, companies are now offering fuels that are compliant with transparency, price stability, and adaptability requirements.

Companies are offering 0.10% sulphur bio MGO and 3.50% sulphur bio HSFO. Bio HSFO and bio MGO have become available to specific requirements up to B30 in South Coast ports. The United Kingdom bunker fuel market dynamics was largely shaped by ExxonMobil’s expanded portfolio of biofuels serving United Kingdom-bound vessels, announced in November 2025. This development aligns with the country’s shipping sector’s response to tightening IMO emissions rules and domestic decarbonization targets, pushing bunker suppliers to rebalance product portfolios toward low-sulfur and renewable options.

The shipping industry is focusing on fuel versatility, availability of blends, and contracts that increase compliance costs. Large-scale players are investing in upgrades and blending facilities based near major ports, such as Immingham and Southampton, which enhance rapid switching between VLSFO, MGO, and Bio blends. For example, in November 2025, Certas Energy’s Omega site started offering Hydrotreated Vegetable Oil (HVO) alongside Diesel (DERV) and AdBlue, boosting the United Kingdom bunker fuel market value. These investments support margin stability while meeting charterer requirements for emissions reporting and fuel traceability.

Compound Annual Growth Rate

5.8%

Value in USD Billion

2026-2035

FincoEnergies introduced GoodFuels B15, a blend of 15% FAME-based biofuel that aids the Dutch maritime sector in lowering emissions. Such developments signal rising demand for drop-in biofuel blends, encouraging suppliers to fund blending infrastructure and certification capabilities without requiring vessel engine modifications.

Shell and Equinor officially merged their United Kingdom offshore oil and gas operations to establish Adura, a new 50:50 joint venture to strengthen upstream stability. Following this United Kingdom bunker fuel market development suppliers can secure long-term fuel contracts linked to North Sea operations and offshore service vessel demand.

Bunker One formed a new alliance with Par Petroleum, providing nationwide road bunkering services that enhance our current barge operations. Such an alliance highlights the value of multimodal bunkering, prompting United Kingdom bunker fuel market players to invest in road-based fuel delivery to complement barge supply and improve port-side flexibility.

ABB incorporated an extensive range of technologies on Feadship Breakthrough. ABB’s technology integration reflects growing vessel efficiency standards, pushing bunker fuel suppliers to fund cleaner fuel solutions aligned with advanced onboard energy and emissions systems.

Marine biofuels are now migrating from the pilot phase to commercial fuel deliveries in the United Kingdom. Large energy companies, such as BP and Shell, are increasing the magnitude of biofuel blend support to vessels headed to the United Kingdom, driven by pressure from the IMO to decarbonize. For example, in July 2023, Standard Fuel Oils started providing biofuels to vessels in Liverpool. The government’s Clean Maritime Plan is supporting the testing of lower-emission marine fuels by directing funding toward selected ports. This development within the United Kingdom bunker fuel market is encouraging firms to readjust their commodity product lines to focus on high-quality fuel solutions aligned to satisfy requirements, as opposed to volume sales.

Firms such as TotalEnergies, Shell, and Exxon Mobil are facilitating the LNG chain networks that extend from the Southampton port to the Thames port in the United Kingdom. LNG reduces sulfur and nitrogen emissions, meeting the criteria set by the government in its emission standards. Exxon Mobil, for instance, announced that the corporation ventured into the LNG bunkering category, starting with two LNG bunker ships in October 2025. Companies in the United Kingdom bunker fuel market are also collaborating with the port authority to enable the development of safe transfer facilities for the LNG.

Suppliers are also investing in blending facilities at the port level. Ports like Immingham and Felixstowe are upgrading their fuel handling facilities for VLSFO, MGO, and biofuel switching. Such investments are also a result of stricter emission guidelines on reporting and the need for fast fuel switching. Suppliers benefit from owning or controlling storage facilities as this secures bunker fuel availability and reduces supply disruptions. In September 2025, Shell Marine completed its first LNG bunkering operation at Portland Port, reinforcing this strategy. This trend in the United Kingdom bunker fuel market favors integrated players with capital depth, while smaller traders increasingly rely on partnership or lease-based access models.

Digitalization is becoming a competitive differentiator in the United Kingdom bunker fuel market. Suppliers are deploying digital bunker delivery notes, fuel quality tracking, and emissions reporting tools aligned with United Kingdom maritime compliance frameworks. Companies like Shell are integrating fuel data with vessel performance platforms. StormGeo, on the other hand, announced the launch of its Next Generation s-Insight Bunker Management platform to digitize and optimize bunker planning and procurement for the global shipping industry, in November 2025. Bunker suppliers offering data-backed fuel traceability are gaining preference in long-term contracts.

The expansion of offshore wind projects around the United Kingdom coastline is creating a steady demand base for bunker fuels tailored to service vessels. Offshore support fleets require cleaner fuels, reliable delivery schedules, and proximity-based bunkering. Government commitments to offshore wind capacity growth are indirectly supporting bunker demand in coastal ports. Suppliers are developing dedicated fuel programs for crew transfer and maintenance vessels. Leveraging such United Kingdom bunker fuel market opportunities, JERA Nex BP commissioned a new hydrogen bunkering facility at the Port of Ostend in November 2025. These contracts offer stable volumes and lower exposure to global shipping cycles.

The EMR’s report titled “United Kingdom Bunker Fuel Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Fuel Type

Key Insight: Fuel type segmentation as considered in the United Kingdom bunker fuel market report reflects how operators balance compliance, cost exposure, and transition readiness. HSFO continues in scrubber equipped fleets prioritizing fuel price arbitrage. VLSFO anchors mainstream demand through regulatory certainty and broad availability. MGO supports auxiliary engines, port operations, and smaller vessels requiring cleaner combustion. LNG represents the clearest transition pathway for operators planning long term emissions reduction. Companies like Molgas bunkered new Calmac Ferries vessel Glen Sannox in Troon, Scotland in November 2024.

Market Breakup by Vessel Type

Key Insight: While container fleets deliver stable, predictable volumes tied to fixed schedules, tankers drive growth in the market through energy trade and stricter charterer compliance. General cargo vessels support flexible regional routes and bulk carriers contribute cyclical demand linked to commodities. Suppliers align investments with vessel behavior to balance stability, growth, and compliance exposure across the United Kingdom bunker fuel industry while maintaining operational resilience for ports, fleets, and long-term strategic positioning.

By fuel type, low sulfur fuel oil leads demand growth due to compliance reliability

Low sulphur fuel oil largely contributes to the surging demand in the United Kingdom bunker fuel market due to its compatibility with existing fleets and predictable compliance performance. Shipowners prefer VLSFO as it avoids costly engine retrofits while meeting IMO sulfur limits. Major suppliers prioritize VLSFO blending and storage at ports like Immingham and Southampton, supporting rapid switching between grades. For example, firms like Greenergy and Monjasa supply of marine fuel containing maximum 0.5% sulphur.

Liquefied natural gas is rapidly expanding its share in the United Kingdom bunker fuel market as shipping trends gradually transition toward lower carbon operations. LNG is being adopted by ferries, tankers, and coastal vessels seeking long term emissions reduction. Suppliers are investing in LNG bunkering capabilities linked to ports such as Southampton and Thames terminals. Although this category is capital intensive, LNG offers sulfur free combustion and reduced nitrogen emissions. Bunker players target multi-year contracts with dual fuel fleets to secure demand.

Container vessels dominate consumption due to routes and volume stability

Container vessels represent the dominant vessel type in the United Kingdom bunker fuel market due to fixed schedules and high fuel turnover. Liner operators prioritize reliable fuel availability across major United Kingdom ports to avoid delays. Long haul routes demand consistent VLSFO and MGO supply. Bunker contracts for container fleets often emphasize volume discounts and quality assurance. Suppliers benefit from predictable consumption patterns and centralized procurement. Containers also drive demand for digital fuel tracking and emissions reporting. In September 2023, ABB secured a complete power, propulsion, and automation systems order for Samskip Group's hydrogen-powered container vessels.

Tankers emerge to be the fastest growing vessel category for bunker fuel demand as energy trade patterns evolve. United Kingdom linked tanker traffic supports crude, refined products, and chemical movements. Compliance pressure is stronger for tankers due to charterer scrutiny. Operators increasingly demand VLSFO, MGO, and alternative fuels. Bunker suppliers pursue long term agreements tied to tanker fleets. Investments in fuel quality monitoring and port-based blending support this category, stimulating the United Kingdom bunker fuel market revenue growth.

The market is moderately consolidated, with competition centered on fuel innovation, infrastructure control, and compliance services. Major United Kingdom bunker fuel market players are shifting focus from spot fuel trading toward long-term supply contracts linked with emissions reporting and fuel traceability. Investments are flowing into port-based storage, blending capabilities, and biofuel readiness rather than volume expansion. LNG bunkering and biofuel blends are becoming strategic differentiators, especially for suppliers aligned with ferry operators, tanker fleets, and offshore wind vessels.

United Kingdom bunker fuel companies offering integrated solutions, fuel supply plus data, certification, and emissions transparency, are gaining preference from charterers. Smaller suppliers are partnering with terminals to stay competitive. Market success increasingly depends on operational reliability, regulatory alignment, and the ability to support fleet transition strategies.

Established in 1999 and headquartered in Irving, Texas, United States, Exxon Mobil Corporation serves the United Kingdom bunker fuel industry through high-quality marine fuels and global supply reliability. The company focuses on VLSFO and MGO supply supported by strong refinery integration. Exxon Mobil emphasizes fuel consistency and testing standards for international fleets operating through United Kingdom ports.

Founded in 1924 and headquartered in Paris, France, TotalEnergies SE is actively shaping the market through LNG bunkering and marine biofuel programs. The company supports dual-fuel vessels and short-sea shipping operators transitioning to cleaner fuels. TotalEnergies is investing in LNG supply chains and digital emissions tracking tools linked to European ports.

Established in 1977 and headquartered in Bury, United Kingdom, Crown Oil Limited caters to the market through flexible fuel supply and regional port servicing. The company specializes in MGO and compliant fuel delivery for coastal and inland operators. Crown Oil emphasizes responsive logistics and tailored contracts for smaller fleets. Its strength lies in serving niche operators and offshore support vessels.

Founded in 1992 and headquartered in London, United Kingdom, Greenergy International Ltd. brings strong blending and storage expertise to the market. The company focuses on fuel supply optimization and infrastructure efficiency. Greenergy supports biofuel blending and low-sulfur fuel distribution across United Kingdom terminals. Its operational model emphasizes cost control and supply resilience.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Rosneft Marine UK Ltd., Gulf Agency Company Limited, and Prax Group (Harvest Energy), among others.

Unlock the latest insights with our United Kingdom bunker fuel market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 8.32 Billion.

The market is projected to grow at a CAGR of 5.80% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of around USD 14.62 Billion by 2035.

Stakeholders are investing in blending infrastructure, forming port partnerships, expanding alternative fuel offerings, securing long-term fleet contracts, and integrating digital compliance tools while optimizing storage, logistics efficiency, and capital allocation.

The key trends in the market include the increasing concerns pertaining to the emission of greenhouse gases and the growing demand for bunker fuels with low sulphur content.

High sulphur fuel oil (HSFO), very low sulphur fuel oil (VLSFO), marine gas oil (MGO), and liquefied natural gas (LNG), among others, are the different fuel types included in the market report.

Containers, tankers, general cargo, and bulk container, among others, are the major vessel types considered in the market report.

The key players in the market include Exxon Mobil Corporation, TotalEnergies SE, Crown Oil Limited, Greenergy International Ltd., Rosneft Marine UK Ltd., Gulf Agency Company Limited, and Prax Group (Harvest Energy), among others.

Bunker fuel suppliers face regulatory uncertainty, high infrastructure costs, fuel price volatility, slow alternative fuel adoption, and pressure from charterers demanding emissions transparency while maintaining competitive pricing and consistent supply reliability.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Fuel Type |

|

| Breakup by Vessel Type |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.