Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

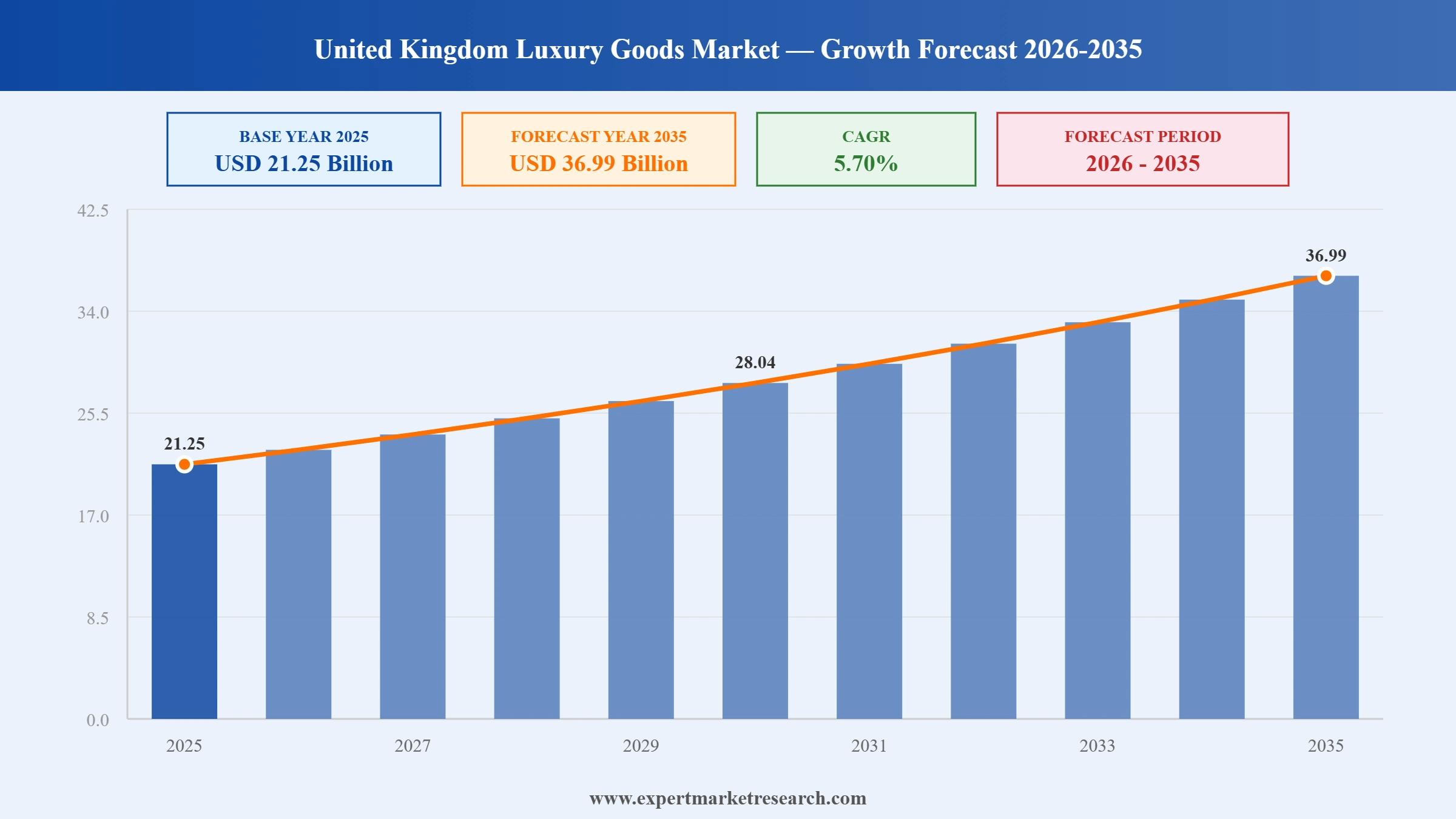

The United Kingdom luxury goods market reached a value of USD 21.25 Billion in 2025 and is projected to expand at a CAGR of around 5.70% during the forecast period of 2026-2035. Rising income levels, increasing personal customisation options, a shift to e-commerce for luxury shopping, rising direct-to-consumer sales, a focus on British heritage, and sustainability-driven demand for ethically sourced luxury goods are driving UK luxury goods market growth. The market is expected to reach USD 36.99 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United Kingdom Luxury Goods Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 21.25 |

| Market Size 2035 | USD Billion | 36.99 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.70% |

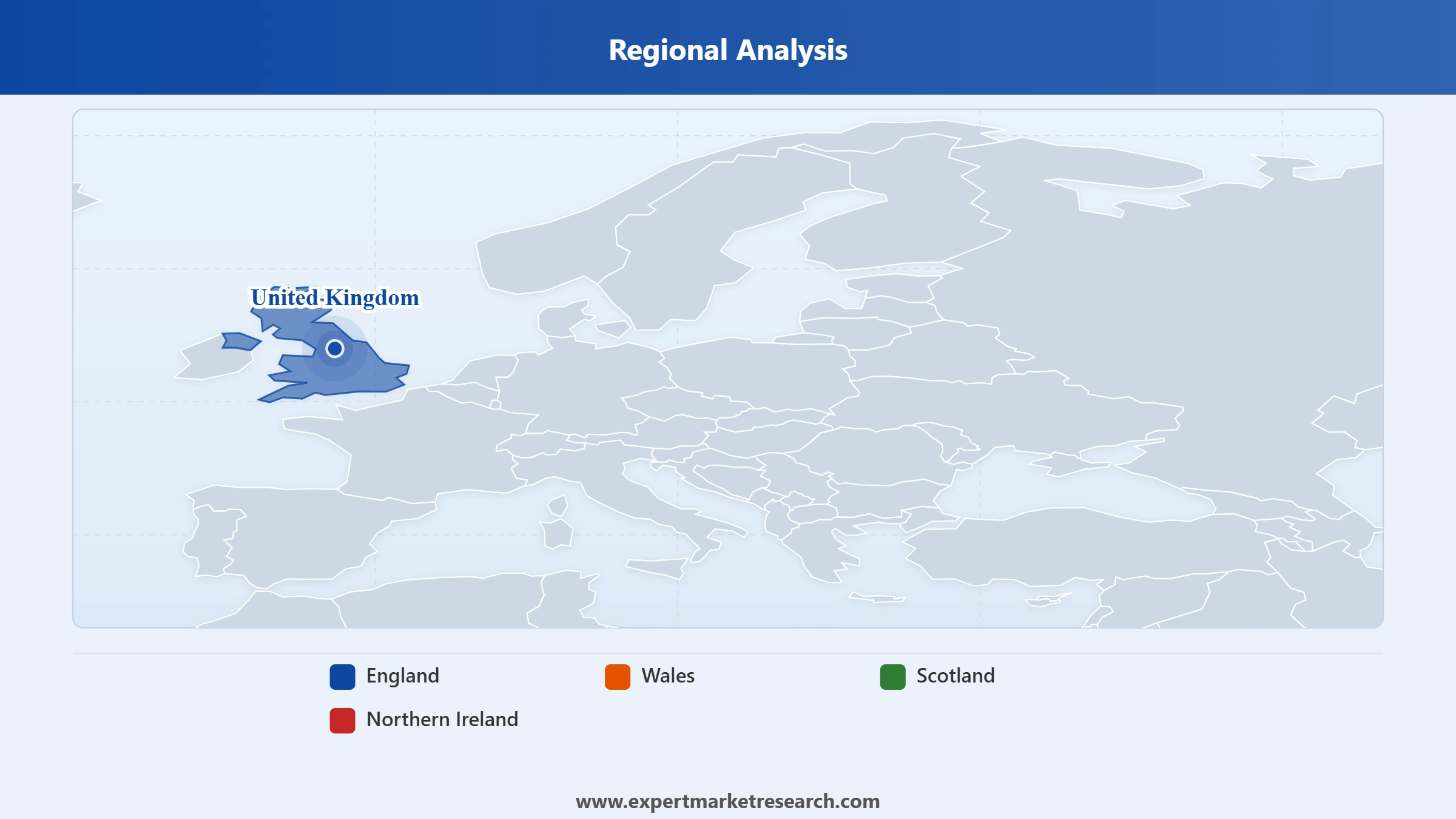

| CAGR 2026-2035 - Market by Region | England | 6.6% |

| CAGR 2026-2035 - Market by Type | Watches and Jewellery | 6.4% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 7.4% |

| Market Share by Region 2025 | Scotland | XX% |

The United Kingdom luxury goods market is driven by rising income levels, growing consumer demand for sustainable and ethically sourced luxury products, the rapid expansion of online luxury retail, the growth of second-hand and pre-owned luxury platforms, and brand innovation from global luxury conglomerates.

Burberry and London College of Fashion launched the 'Reimagining Materials' competition in May 2025, designed to promote circular design using surplus luxury fabrics. The initiative supports emerging fashion talent, promotes sustainable practices in the UK luxury goods market, and strengthens Burberry's commitment to circular fashion principles.

Vinted launched its online luxury fashion wardrobe, House of Vinted, in March 2025, featuring designer pieces from top creators and brands including Prada and Gucci. The House of Vinted launch boosted the UK's growing second-hand luxury goods segment, encouraged sustainable shopping through the circular economy, and supported charity through donations to Oxfam. The platform reflects the growing UK consumer preference for pre-owned and second-hand luxury goods.

Authentic Brands Group and Saks Global launched the Authentic Luxury Group in October 2024 to expand their portfolio of luxury brands including Barneys New York, Judith Leiber Couture, Herve Leger, and Vince. The Authentic Luxury Group launch strengthened luxury retail links and broadened global reach for these luxury brands, boosting branded lifestyle offerings in the UK luxury goods market. The launch reflects growing consolidation in the global luxury goods industry.

Marks and Spencer launched a new clothing repairs and alteration service in June 2024, aimed at boosting sustainable habits among UK consumers. The initiative reflects the UK luxury and premium apparel market's growing focus on sustainability, circularity, and product longevity. The service aligns with the UK luxury goods market trend toward sustainable consumption.

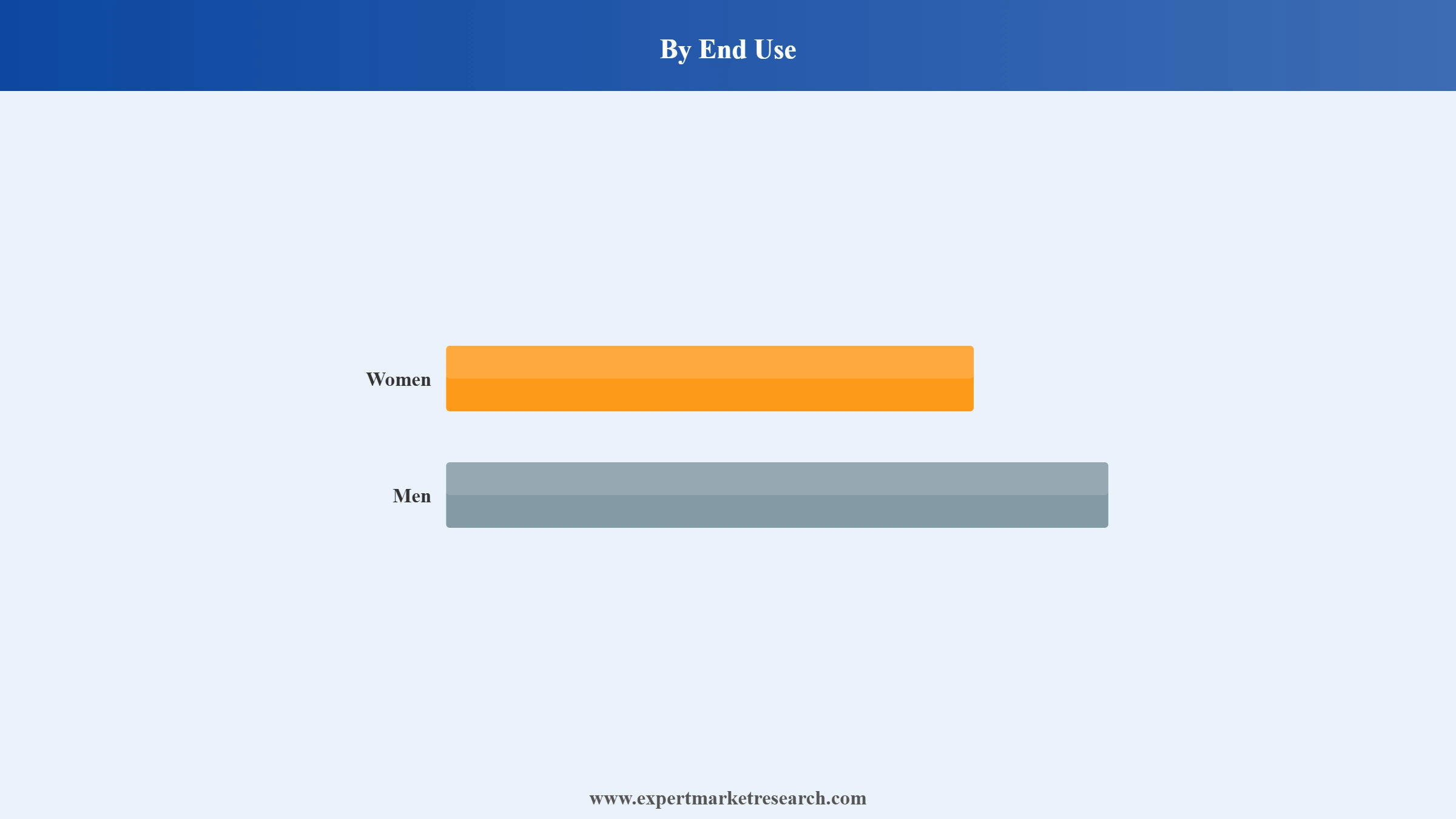

Women command the largest UK luxury goods market share by end use at approximately 54% of total revenue, driven by strong female consumer demand for luxury fashion, accessories, fine jewellery, handbags, fragrances, and cosmetics. Women's luxury goods are central to the strategies of Chanel, Kering, LVMH, and Hermes, which invest heavily in women's luxury product lines and retail experiences.

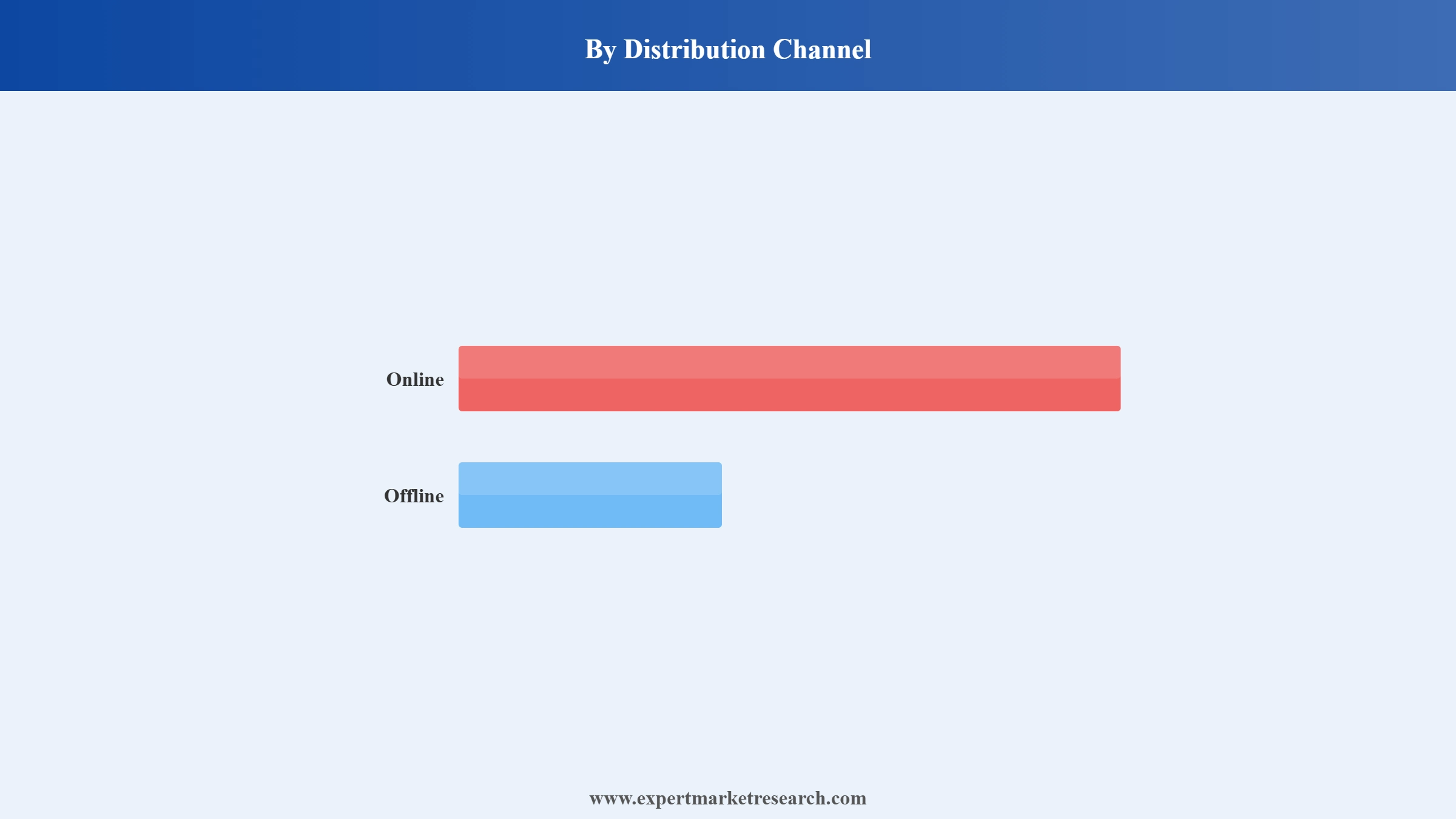

Online is the fastest-growing UK luxury goods distribution channel, reflecting the rapid shift of luxury consumers to digital and e-commerce platforms. LVMH, Kering, Richemont, and Estee Lauder collectively hold over 60% of UK luxury goods market share, and major players are investing in digital clienteling tools, augmented reality in retail, and online flagship stores.

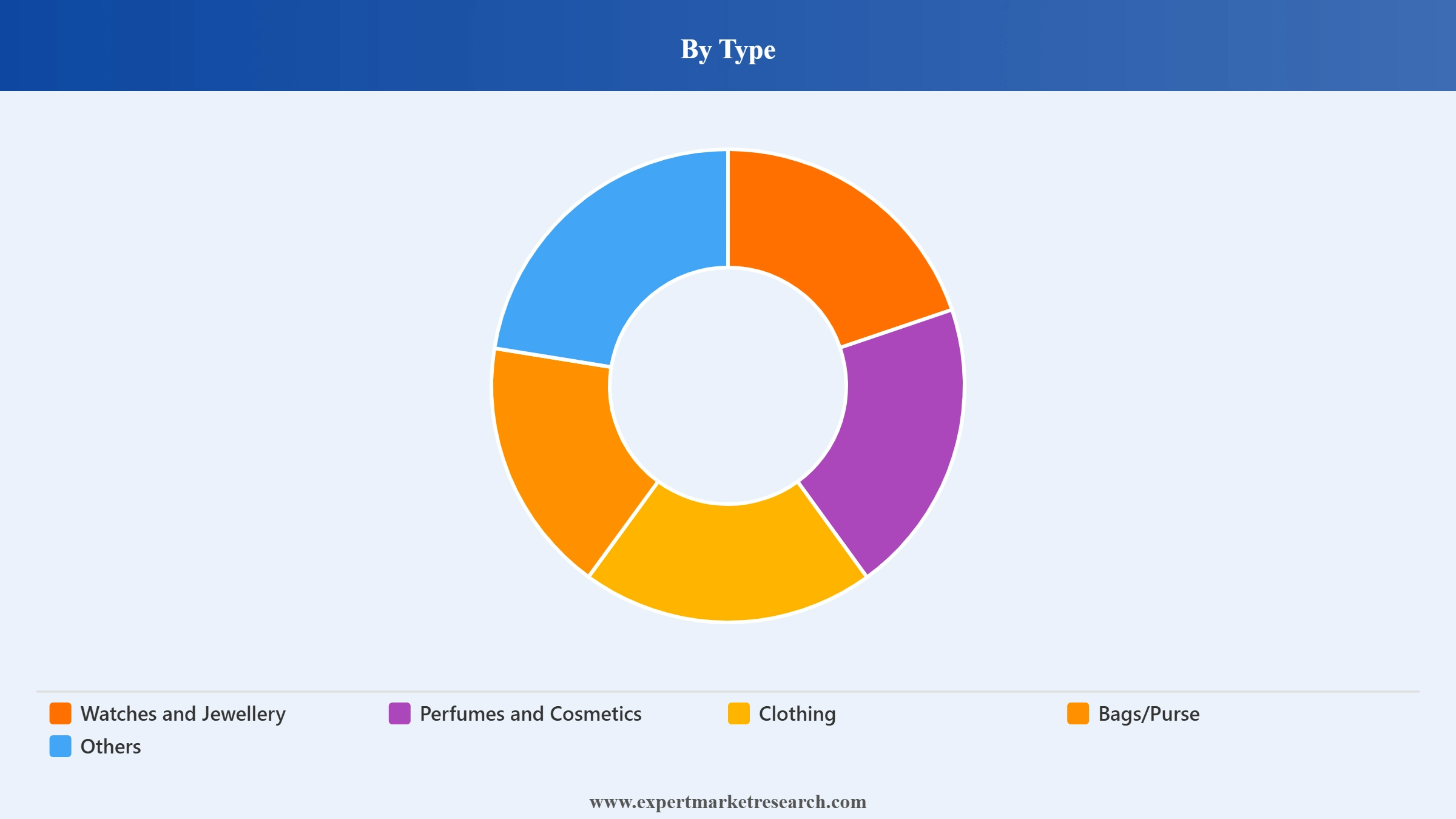

Clothing and apparel is the dominant UK luxury goods type by revenue, commanding approximately 37.43% of total UK luxury goods market value through strong demand for high-end fashion, seasonal luxury apparel collections, and branded British heritage clothing. Burberry Group PLC is a key heritage British luxury fashion brand deploying large-scale storytelling campaigns featuring British artists to boost brand identity.

Watches and Jewellery is a key UK luxury goods type through strong consumer demand for luxury investment pieces and premium Swiss watch imports. The UK imports wristwatches primarily from Switzerland, China, and Spain. Rolex SA, Richemont, and Tiffany & Co. (LVMH) are key players in the UK luxury watches and jewellery segment.

Men is a growing UK luxury goods end-use segment, driven by the premiumisation of menswear, increasing male consumer interest in luxury fashion, watches, accessories, and grooming products, and the growing influence of social media and celebrity endorsements on male luxury purchasing behaviour. Luxury houses including Hermes, Kering, Rolex, and LVMH are expanding their men’s luxury product lines and retail experiences to capture the growing male luxury consumer demographic in the United Kingdom.

The "United Kingdom Luxury Goods Market Report and Forecast 2026-2035" by Expert Market Research offers detailed analysis across the following segments:

Market Breakup by Type

Key Insight: Clothing is the dominant UK luxury goods type at approximately 37.43% of market revenue. Watches and Jewellery is a key type through luxury investment and premium watch demand.

Market Breakup by End Use

Key Insight: Women is the dominant UK luxury goods end-use segment commanding approximately 54% of market revenue. Men is a growing end-use segment through premiumisation and growing menswear luxury demand.

Market Breakup by Distribution Channel

Key Insight: Offline is the dominant UK luxury goods distribution channel through flagship stores and department stores. Online is the fastest-growing distribution channel through digital clienteling and e-commerce adoption.

Market Breakup by Region

Key Insight: England is the largest UK luxury goods region through London's global luxury retail hub and flagship store concentration. Scotland and Wales are growing regional luxury goods markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, Clothing is the dominant luxury goods type while Watches and Jewellery is a key revenue segment

Clothing and apparel commands the largest UK luxury goods market share by type at approximately 37.43% of revenue, driven by strong demand for high-end fashion, seasonal luxury apparel, and branded British heritage clothing from Burberry, Chanel, Kering-owned brands, and Ralph Lauren. Watches and Jewellery is a key type through luxury investment pieces and Swiss watch demand. Perfumes and Cosmetics is significant through luxury fragrance and beauty. Bags and Purse is a fast-growing type through designer handbag and leather goods demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, Women is the dominant end use commanding 54% of the UK luxury goods market

Women command the largest UK luxury goods market share by end use at approximately 54% of revenue, reflecting the strong female consumer demand for fashion, accessories, fine jewellery, handbags, and beauty products. Men is a growing end-use segment through premiumisation and growing male consumer interest in luxury fashion, watches, accessories, and grooming. The rising appeal of luxury goods is supported by celebrity influence and social media marketing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, Offline dominates while Online is the fastest-growing distribution channel

Offline commands the largest UK luxury goods distribution channel share, through London flagship stores (Bond Street, Knightsbridge, Mayfair), department stores (Harrods, Selfridges, Harvey Nichols), and luxury boutiques. Online is the fastest-growing distribution channel through the growing adoption of digital clienteling tools, brand e-commerce platforms, luxury fashion marketplaces, and pre-owned luxury platforms including House of Vinted.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

United Kingdom is a key Europe luxury goods market driven by rising income levels, sustainable luxury trends, digital luxury retail growth, and the strong appeal of British heritage luxury brands

The United Kingdom luxury goods market operates within the broader Europe luxury goods market. London is a global luxury retail destination attracting international luxury shoppers and hosting flagship stores for the world’s leading luxury brands on Bond Street, Knightsbridge, and Mayfair.

LVMH, Kering, Richemont, and Estee Lauder hold over 60% of UK luxury goods market share. The growing second-hand and pre-owned luxury segment, boosted by platforms such as Vinted’s House of Vinted, is creating new entry points for younger UK luxury consumers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom luxury goods market is highly competitive, with global luxury conglomerates, independent luxury houses, and heritage British brands competing through product exclusivity, British heritage positioning, digital innovation, and premium retail experiences.

Chanel Limited is a France-based global luxury house with a dominant UK luxury goods market presence through its luxury fashion, fragrance, cosmetics, jewellery, and accessories portfolio. Chanel operates flagship stores on Bond Street and in Knightsbridge in London, serving UK high-net-worth luxury consumers. Chanel integrates augmented reality into its UK retail stores to provide immersive in-store experiences for customers making purchasing decisions on luxury goods.

Kering SA is a France-based global luxury goods group with a significant UK luxury goods market presence through its portfolio of luxury fashion, leather goods, and jewellery brands including Gucci, Saint Laurent, Bottega Veneta, Alexander McQueen, Balenciaga, and Brioni. In March 2025, Kering announced an updated retail concept for luxury fashion brands including Gucci and Saint Laurent, integrating digital clienteling tools and personalised shopping experiences across flagship UK locations.

Rolex SA is a Switzerland-based luxury watch manufacturer with a strong UK luxury goods market presence through its premium mechanical watch portfolio including Submariner, Datejust, Day-Date, and GMT-Master II. Rolex serves the UK luxury watches and jewellery segment through a network of authorised dealers and select luxury retailers. Rolex maintains strict supply controls and brand exclusivity to support premium pricing.

Hermes International S.A. is a France-based ultra-luxury goods house with a prestigious UK luxury goods market presence through its leather goods, silk, ready-to-wear, watches, and fragrance portfolio. Hermes operates its flagship Bond Street store in London, serving the UK's ultra-luxury consumer segment. Hermes' handcrafted leather goods including the iconic Birkin and Kelly bags drive strong demand in the UK luxury bags and purse segment.

Other key players include Giorgio Armani S.p.A., Ralph Lauren Corporation, Compagnie Financiere Richemont SA, Prada SpA, VALENTINO S.p.A., and Tiffany & Co., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers the market data, competitive analysis, and strategic insights to capture the United Kingdom's growing luxury goods market. Reach out to our team to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is estimated to grow at a CAGR of 5.70% between 2026 and 2035.

The major drivers are rising disposable income, changing consumer preferences, and increasing role of ecommerce channels.

The key trends of the luxury goods market in the United Kingdom include the usage of augmented reality in retailing, growing focus on sustainability, and growing global demand for various kinds of luxury goods such as bags, handbags, and clothing items.

Based on region, the market is mainly divided into England, Wales, Scotland, Northern Ireland.

Based on distribution channels, the market is segmented into online and offline.

The key players in the market are Chanel Limited, Kering SA, Rolex SA, Hermès International S.A., Giorgio Armani S.p.A., Ralph Lauren Corporation, Compagnie Financière Richemont SA, Prada SpA, VALENTINO S.p.A., Tiffany & Co., among others.

In 2025, the market attained a value of nearly USD 21.25 Billion.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 36.99 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.