Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

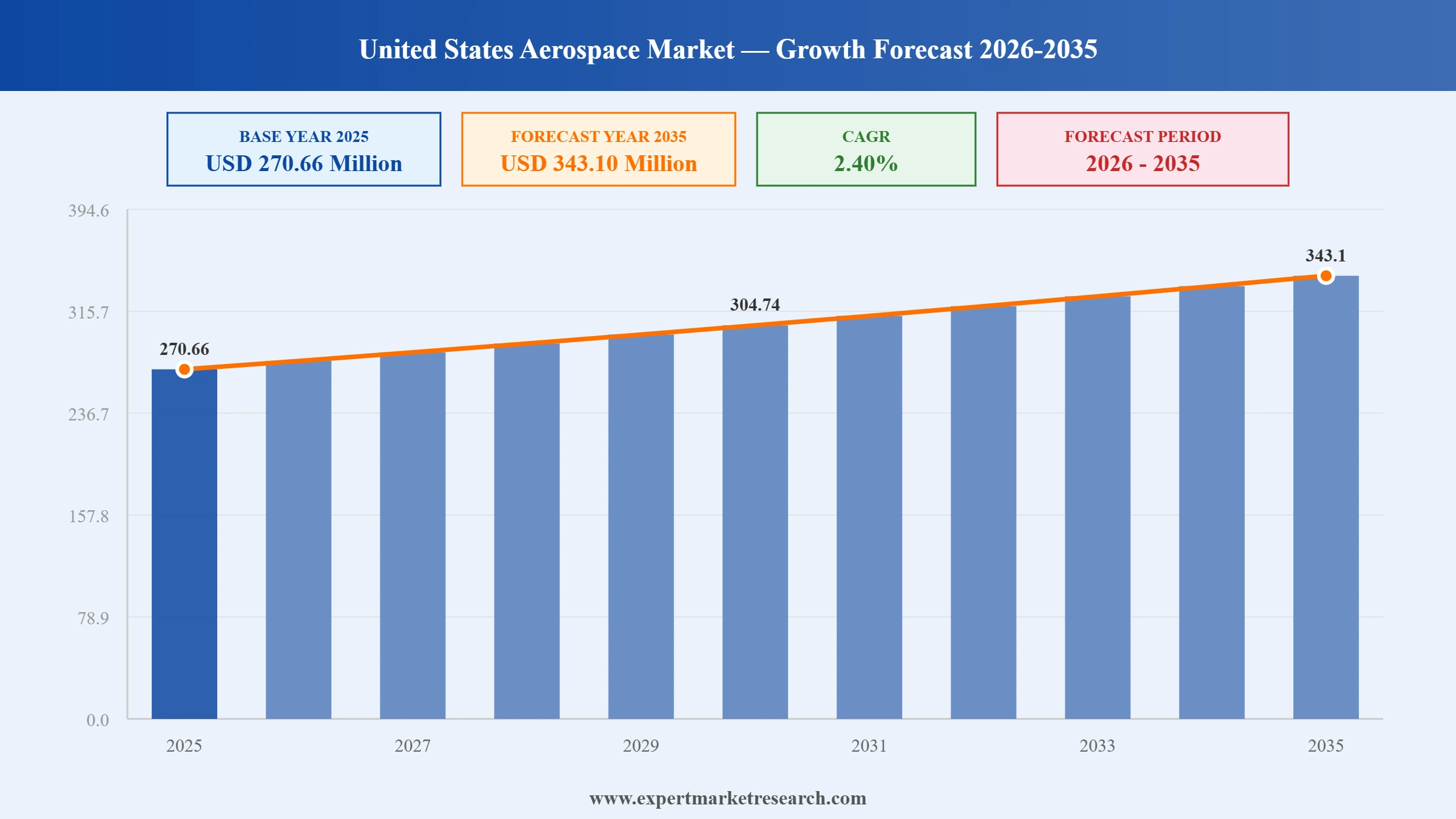

The United States aerospace market was valued at USD 270.66 Million in 2025. The market is expected to grow at a CAGR of 2.40% during the forecast period of 2026-2035 to reach a value of USD 343.10 Million by 2035. Increasing investments in defense, commercial aviation, and aerospace innovation are collectively supporting the overall market growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Lockheed Martin, Boeing, Raytheon, Northrop Grumman, BAE, and L3Harris agreed in April 2026 to quadruple production of Exquisite Class precision weaponry including the Precision Strike Missile. Lockheed also opened its Rapid Fielding Center in Dallas, directly expanding production throughput for advanced aerospace defence systems in the United States.

Raytheon signed five landmark framework agreements with the US Department of War in February 2026 to significantly increase Tomahawk, AMRAAM, SM-3, and SM-6 production. Annual Tomahawk production is to exceed 1,000 units and AMRAAMs at least 1,900, representing a major expansion of United States aerospace precision strike capability.

US companies led by Boeing secured foreign procurement contracts worth USD 244 billion in 2025 with US Commerce Department assistance, nearly tripling 2024 levels. Boeing's 1,075 net jetliner orders in 2025, its sixth-best year ever and first time it outpaced Airbus in seven years, represent a landmark commercial aviation recovery.

Lockheed Martin signed a framework agreement with the US Department of War in January 2026 to quadruple THAAD interceptor production capacity and broke ground on a new Munitions Acceleration Center in Camden, Arkansas. The agreement supports sustained long-term production commitments worth significantly above USD 1 billion annually.

Boeing's commercial aviation recovery is generating strong United States aerospace market growth momentum. The company booked 336 net commercial orders in Q4 2025 alone, ending 2025 with a record USD 682 billion total backlog including 6,100 commercial airplanes. Boeing delivered its sixth-best year for orders in 2025.

Investment in autonomous aircraft systems is expanding the addressable scope of the United States aerospace market beyond traditional manned platforms. Sikorsky and Robinson Helicopter Company unveiled the R66 TURBINETRUCK autonomous cargo helicopter in March 2026, signalling growing commercial viability of unmanned logistics platforms for US aerospace market growth.

Boeing Global Services secured record annual orders of USD 28 billion in 2025, including US Air Force C-17 flight deck replacement awards, ending the year with a record USD 30 billion backlog. This MRO demand surge in the United States aerospace market reflects the scale of maintenance requirements for an aging US military and commercial aircraft fleet.

Lockheed Martin reported USD 18 billion in Q1 2026 revenue, maintaining steady year-over-year performance driven by next-generation defence platform demand. Lockheed's total company backlog reached a record USD 176 billion as of 2025, reflecting the long-term durability of US defence procurement funding for the United States aerospace market.

US aerospace manufacturers are increasing investment in sustainable aviation fuel compatibility and fuel-efficient platform development. Boeing's 787 Dreamliner and forthcoming next-generation aircraft programmes and GE Aerospace's next-generation engine platforms are positioning US companies at the forefront of aerospace decarbonisation in the United States aerospace market.

United States Aerospace Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

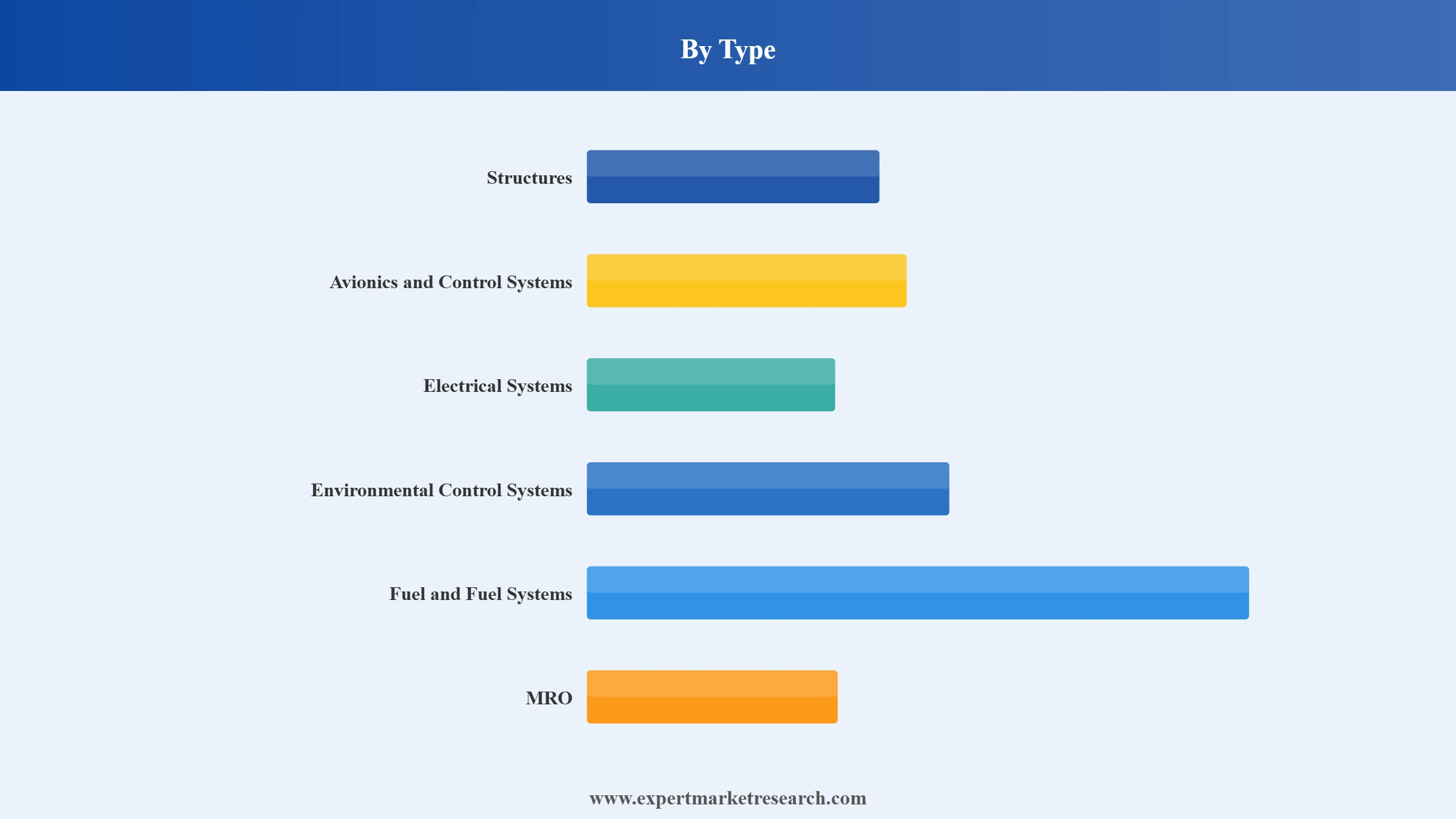

Market Breakup by Type

Key Insight: Structures represents the largest component segment in the United States aerospace market, encompassing airframes, engine systems, cabin interiors, and landing gear across commercial and military platforms. Engine and engine systems are the highest-value structural sub-category, with GE Aerospace and Pratt and Whitney producing the majority of US commercial jet engines under long-term exclusive supply relationships with Boeing and Lockheed Martin. MRO is the fastest-growing type segment, with Boeing Global Services recording a record USD 30 billion backlog in 2025 as aging fleets and expanded aircraft operations drive maintenance requirements.

Market Breakup by Operation

Key Insight: Manual operation aircraft represent the dominant share of the United States aerospace market by fleet size and current revenue, encompassing virtually all commercial aviation, the majority of military aircraft, and general aviation platforms. Autonomous aircraft is the fastest-growing operation type, driven by significant defence investment in unmanned aerial systems for combat, surveillance, and logistics, and growing commercial investment in autonomous air cargo platforms. Sikorsky's March 2026 unveiling of the R66 TURBINETRUCK with Robinson Helicopter signals expanding autonomous helicopter commercial applications in the US market.

Market Breakup by Body Type

Key Insight: Narrow body aircraft represent the dominant body type in the United States aerospace market by volume, driven by the overwhelming commercial success of the Boeing 737 MAX family, which anchors the largest portion of Boeing's record 6,100-plane backlog. Narrow body platforms serve the most commercially active short-to-medium haul air travel routes, sustaining very high utilisation rates and correspondingly high MRO demand. Wide body aircraft is the faster-growing body type segment, driven by long-haul international travel demand recovery, Emirates' landmark USD 96 billion widebody order in 2025, and Korean Air Lines' USD 50 billion Boeing widebody deal.

Market Breakup by Aircraft Type

Key Insight: Narrow body aircraft represent the dominant body type in the United States aerospace market by volume, driven by the overwhelming commercial success of the Boeing 737 MAX family, which anchors the largest portion of Boeing's record 6,100-plane backlog. Narrow body platforms serve the most commercially active short-to-medium haul air travel routes, sustaining very high utilisation rates and correspondingly high MRO demand. Wide body aircraft is the faster-growing body type segment, driven by long-haul international travel demand recovery, Emirates' landmark USD 96 billion widebody order in 2025, and Korean Air Lines' USD 50 billion Boeing widebody deal.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, structures dominate the market due to their foundational role in all aircraft platforms across commercial and defence sectors

Structures command the dominant share of the United States aerospace market by type, encompassing the airframe, engine systems, cabin interiors, and landing gear that form the fundamental physical architecture of every commercial and military aircraft platform. The sheer scale of Boeing's commercial delivery backlog and Lockheed Martin's defence programme portfolio creates persistent, long-cycle demand for structural components. Spirit AeroSystems, acquired by Boeing in December 2025, is a key structural components supplier that Boeing has reintegrated to improve production stability and quality control across its aircraft assembly operations.

MRO is the fastest-growing type segment within the United States aerospace market, driven by the increasing age of US commercial and military aircraft fleets and the scaling of operations as Boeing ramps commercial deliveries. Boeing Global Services secured record annual orders of USD 28 billion in 2025, while Lockheed Martin's MRO and sustainment services are a growing contributor to defence programme revenue. Avionics and control systems are also growing strongly, driven by both military modernisation demand for advanced flight management and health monitoring systems and commercial aviation's investment in digitally connected cockpit and cabin technologies.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Operation, manual aircraft account for the dominant share due to regulatory certainty and commercial aviation's current infrastructure

Manual operation aircraft account for the overwhelming majority of total United States aerospace market revenue, spanning the entire commercial aviation sector, the majority of military platforms, and general aviation. The regulatory framework for manned aviation is well established, enabling efficient certifications, financing, insurance, and operational deployment at scale. Boeing's commercial aircraft backlog of over 6,100 planes and Lockheed Martin's F-35 and C-130J production programmes collectively define the demand profile for manual aircraft structures, avionics, systems, and MRO services through the end of the forecast period.

Autonomous aircraft is the fastest-growing operation type segment, with US defence spending on unmanned aerial vehicles, autonomous logistics rotorcraft, and unmanned combat platforms accelerating through the forecast period. Northrop Grumman's RQ-4 Global Hawk and emerging next-generation unmanned combat platforms represent significant long-term defence procurement commitments. The commercial autonomous aircraft market is at an earlier commercial stage, with Sikorsky and Archer Aviation among the companies advancing autonomous and electric vertical takeoff and landing platforms toward FAA certification and commercial deployment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Aircraft Type, commercial aviation accounts for the dominant share due to Boeing's record backlog and global fleet expansion

Commercial aviation commands the largest aircraft type share of the United States aerospace market, reflecting Boeing's central role as one of only two global widebody and narrowbody commercial aircraft manufacturers. Boeing's 2025 commercial aviation recovery, delivering 600 commercial aircraft for its best year since 2018 and securing 1,075 net orders, has rebuilt the production throughput that had contracted during safety crisis years. The Qatar Airways widebody deal valued at USD 96 billion and Korean Air Lines' USD 50 billion Boeing order from 2025 are among the largest aviation contracts in history, anchoring commercial aviation market momentum through the forecast period.

Military aviation is the most commercially stable and contract-certain aircraft type segment in the United States aerospace market, with major programmes including the F-35 Lightning II, KC-46A Tanker, T-7A Red Hawk, and CH-53K helicopter providing predictable long-term revenue streams for Lockheed Martin, Boeing, and Sikorsky. The April 2026 agreement to quadruple Precision Strike Missile production and Raytheon's February 2026 framework agreements to increase Tomahawk, AMRAAM, and SM-6 production reflect the sustained intensity of US military aircraft and weapons system procurement that underpins the overall market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United States aerospace market is dominated by a small group of prime contractors that combine aircraft manufacturing, systems integration, and MRO capabilities across both commercial and military segments. Lockheed Martin, Boeing, Raytheon Technologies (RTX), Northrop Grumman, and General Dynamics each hold multi-decade franchise positions secured through exclusive or preferred supplier relationships with the Department of Defense and commercial airlines. Competition in the defence segment is characterised by long-cycle programme competitions, followed by monopolistic production once a platform is selected.

The commercial aviation segment is a duopoly between Boeing and Airbus, with Boeing's 2025 order recovery reinforcing its competitive relevance. GE Aerospace and L3Harris compete effectively in engine systems and avionics respectively. New entrants including autonomous aircraft startups and sustainable aviation fuel producers are emerging as structural market contributors but remain peripheral to the dominant prime contractor ecosystem through most of the forecast period.

Lockheed Martin Corporation was founded in 1995 through the merger of Lockheed and Martin Marietta and is headquartered in Bethesda, Maryland. The company is the largest defence contractor in the United States and the world, with 2025 revenue exceeding USD 70 billion. Lockheed produces the F-35 Lightning II, the most sophisticated fighter aircraft in service globally, along with THAAD missile defence, PAC-3 MSE interceptors, and C-130J transport aircraft. In Q1 2026, Lockheed reported USD 18 billion in revenue and maintained a record backlog exceeding USD 176 billion, reflecting the long-term durability of its defence programme portfolio.

Raytheon Technologies Corporation (RTX) was formed in 2020 through the merger of Raytheon Company and United Technologies, and is headquartered in Arlington, Virginia. The company operates through Pratt and Whitney (jet engines), Collins Aerospace (avionics, interiors, and systems), and Raytheon (missiles and defence electronics). In February 2026, Raytheon signed five landmark framework agreements with the US Department of War to substantially increase production of Tomahawk, AMRAAM, SM-3, and SM-6 precision munitions, cementing RTX's central role in US precision strike capability expansion.

The Boeing Company was founded in 1916 and is headquartered in Arlington, Virginia. Boeing is the world's largest aerospace company and the most significant commercial aircraft manufacturer in the United States, competing with Airbus for global commercial aviation supremacy. Boeing's full year 2025 revenue reached USD 89.5 billion with 600 commercial deliveries, its strongest performance since 2018, and the company ended the year with a record backlog of USD 682 billion including 6,100 commercial aircraft. Boeing's Defence, Space and Security segment secured several major US military programme awards including Apache helicopter and KC-46A Tanker contracts in Q4 2025.

Northrop Grumman Corporation was founded in 1939 and is headquartered in Falls Church, Virginia. The company is a leading producer of advanced aerospace and defence systems, with primary capabilities in stealth aircraft, missile systems, space sensors, and unmanned aerial vehicles. Northrop Grumman's B-21 Raider next-generation stealth bomber, the F-35's electronic warfare systems, and the RQ-4 Global Hawk unmanned surveillance platform represent its most strategically significant aerospace contributions. The company was among the signatories of the April 2026 agreement to quadruple precision weapons production for the US Department of War.

Other key players in the market are General Dynamics Corporation, GE Aviation, L3Harris Technologies, Leidos, Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the United States aerospace market 2026 with our comprehensive report. Stay ahead with valuable data on defence procurement trends, commercial aviation order dynamics, and autonomous aircraft investment. Whether you're an aerospace manufacturer, defence investor, or MRO provider, this report gives you the clarity you need. Download your free sample now and discover key opportunities in the United States thriving aerospace industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 2.40% between 2026 and 2035.

The major market drivers are improving standards of living, affordable prices of tickets, and increased frequency of flights and route availability.

The key trends in the market include rise in the number of passengers, demand for repair and maintenance, and rapid advancements in technology.

The market is categorised according to the body type, which includes wide body and narrow body.

The key market players are Lockheed Martin Corporation, Raytheon Technologies Corporation, Boeing Company, General Dynamics Corporation, Northrop Grumman Corporation, GE Aviation, L3Harris Technologies, and Leidos, Inc., among others.

Based on the operation, the market is divided into autonomous aircraft and manual.

Based on the aircraft type, the market is divided into commercial aviation, general aviation, military aviation, and others.

In 2025, the United States aerospace market reached an approximate value of USD 270.66 Million.

The market is expected to witness steady growth during the forecast period of 2026-2035 to reach a value of USD 343.10 Million by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Operation |

|

| Breakup by Body Type |

|

| Breakup by Aircraft Type |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.