Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

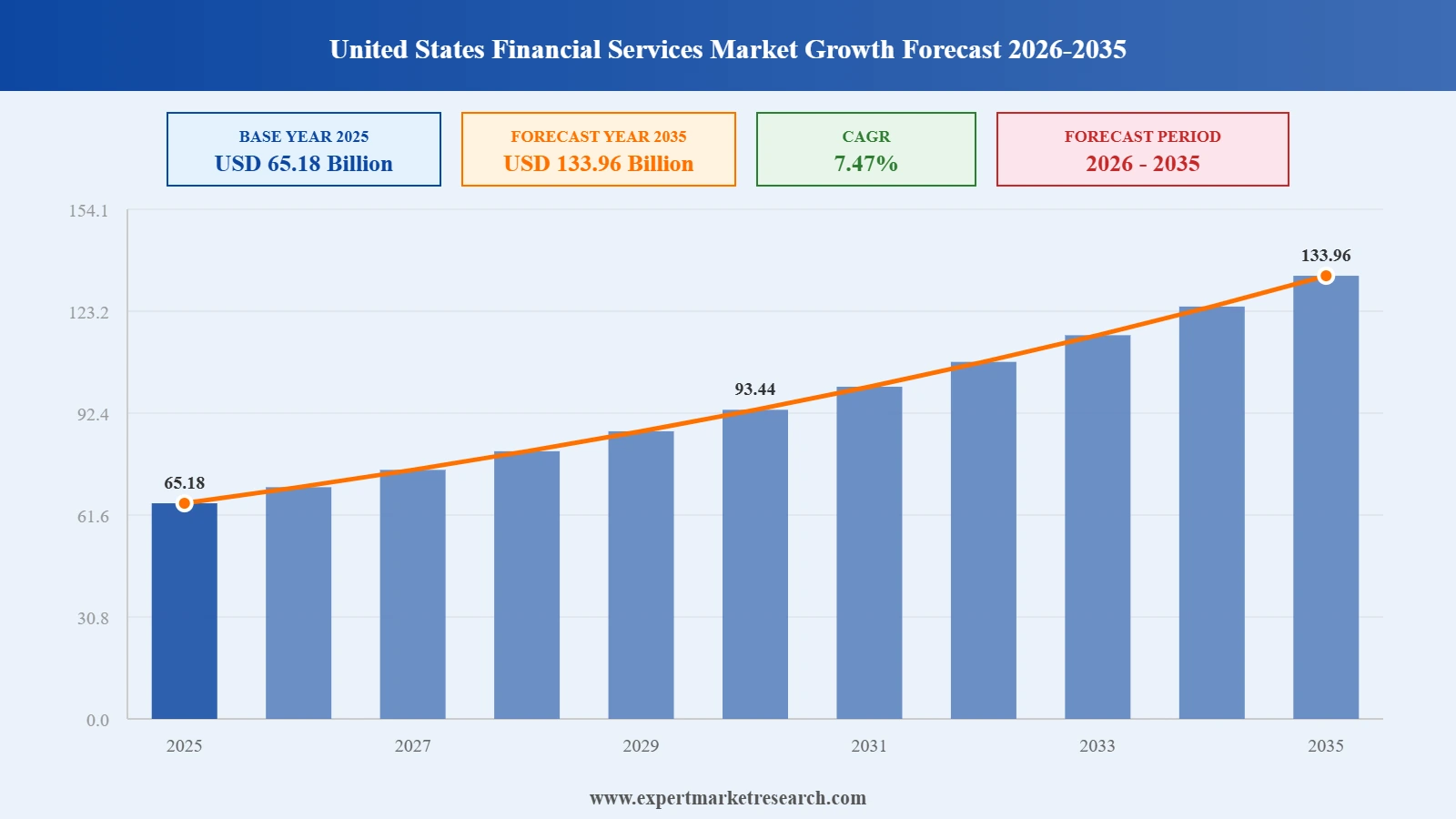

The united states financial services market reached a value of USD 65.18 Billion at 2025 and is projected to expand at a CAGR of around 7.47% during the forecast period of 2026-2035. With accelerating fintech adoption reshaping banking and payments, AI-powered wealth management and advisory tools expanding investment access, record-high capital market activity driven by robust institutional demand, and growing SME financial services demand from entrepreneurial growth, the market is expected to reach USD 133.96 Billion by 2035.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

The United States financial services market is experiencing profound transformation driven by AI integration across banking, wealth management, and insurance operations. Record-high capital market activity at major institutions, accelerating digital adoption among consumers and businesses, and deregulatory momentum are collectively reshaping competitive dynamics. Physical branch expansion is coexisting with digital-first services as leading banks pursue omnichannel strategies to capture diverse customer segments.

JPMorgan Chase reported fourth-quarter and full-year 2025 financial results, confirming the firm had reached USD 4.4 trillion in assets and USD 362 billion in stockholders' equity at year-end. The results underlined JPMorgan's position as the world's largest bank by market capitalisation and demonstrated record-level performance across investment banking, commercial banking, and consumer financial services, reinforcing its industry leadership in the United States financial services market.

JPMorgan Chase announced plans to open more than 500 new branches by 2027, including 14 new J.P. Morgan Financial Centers, as part of a multi-billion dollar investment in its physical distribution network. With 1,700 existing locations being renovated and expanded capabilities for affluent banking, commercial lending, and auto loans, the initiative demonstrates the continued strategic value of branch infrastructure alongside digital channels in the United States financial services market.

America's major financial institutions closed 2025 at record-high stock valuations, with Bank of America, JPMorgan Chase, Wells Fargo, and Citigroup all achieving peak share prices or surpassing historical book value metrics for the first time in years. Record investment banking and trading fee revenues, combined with improved credit performance and expanding market share, were cited as the primary drivers of the exceptional performance across the United States financial services market in 2025.

JPMorgan Chase reported strong second-quarter 2025 results, confirming USD 4.6 trillion in total assets, driven by continued net interest income growth, record equities trading revenues, and expansion across consumer and small business banking. The performance highlighted JPMorgan's structural advantages in scale and diversification, reinforcing the firm's dominant competitive position across multiple service categories within the United States financial services market through the mid-2025 reporting period.

Artificial intelligence is being embedded across the United States financial services market, from JPMorgan Chase's large language model deployment for document analysis to Bank of America's Erica virtual financial assistant serving over 40 million users. AI-powered underwriting is accelerating loan approval, reducing default rates, and enabling granular risk segmentation. Capital One's AI-driven fraud detection and personalised product recommendation systems exemplify the competitive differentiation being created through machine learning investment.

More than 50% of US consumers now conduct primary banking through digital channels, including mobile apps, according to 2025 Federal Reserve consumer finance data. This structural shift is driving incumbent banks to accelerate mobile feature development and digital onboarding capabilities while maintaining physical branch networks for complex advisory needs. The United States financial services market is adapting to an omnichannel imperative that requires investment in both digital infrastructure and strategic physical presence.

US household wealth reached approximately USD 156 trillion as of 2025, according to Federal Reserve Board data, creating an exceptionally large addressable market for wealth management services. Edward Jones Investments, Goldman Sachs, and Morgan Stanley are expanding advisor networks and digital wealth platforms to capture growing demand from both mass-affluent and high-net-worth individuals. Fee-based advisory model adoption continues to accelerate across the United States financial services market.

The United States financial services market entered 2025 with the highest level of regulatory freedom experienced by major institutions in approximately 15 years, according to industry observers. Easing capital rules and reduced merger scrutiny are enabling banks to accelerate expansion, pursue strategic acquisitions, and increase capital returns to shareholders. This deregulatory environment is widely expected to catalyse consolidation activity and accelerate balance sheet growth among the largest US financial institutions through the forecast period.

Growing awareness of climate-related property risks and accelerating cyber threat sophistication are driving robust insurance premium growth across the United States financial services market. Nationwide Mutual Insurance Company and Farmers Insurance Group are investing in advanced risk modelling and digital claims processing to serve a rapidly evolving risk landscape. The commercial cyber insurance segment is experiencing double-digit annual premium growth as enterprise clients seek comprehensive coverage for ransomware and data breach exposures.

The report of the Expert Market Research's titled "United States Financial Services Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

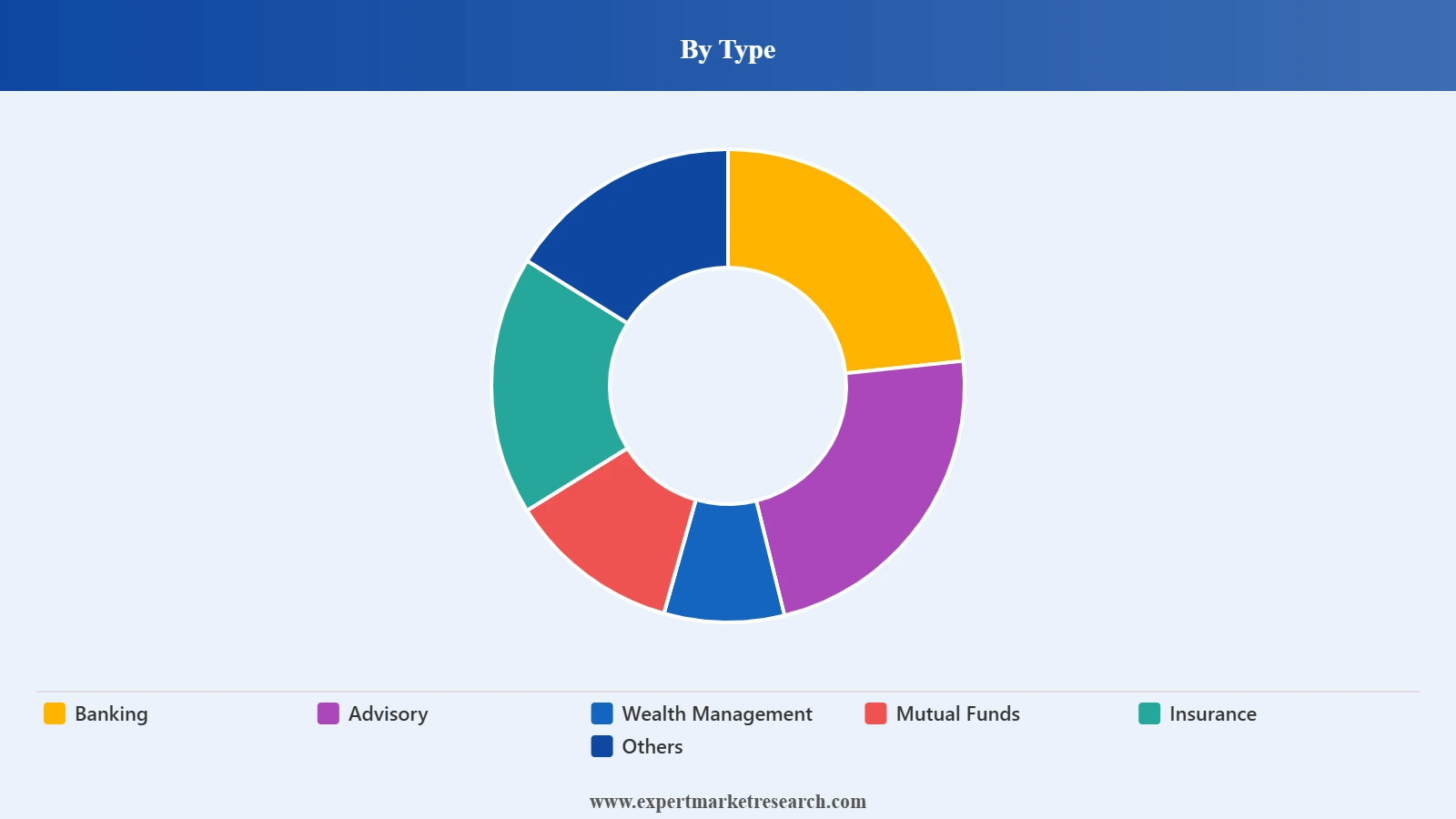

Market Breakup by Type

Key Insight: Banking dominates the United States financial services market by type, anchored by the world's largest and most liquid banking system. The FDIC counted 4,614 institutions in the US as of 2023, with JPMorgan Chase, Bank of America, and Wells Fargo collectively holding a dominant share of total assets. Wealth management is the fastest-growing segment, driven by record household wealth levels and increasing adoption of fee-based advisory services across mass-affluent and high-net-worth individual demographics.

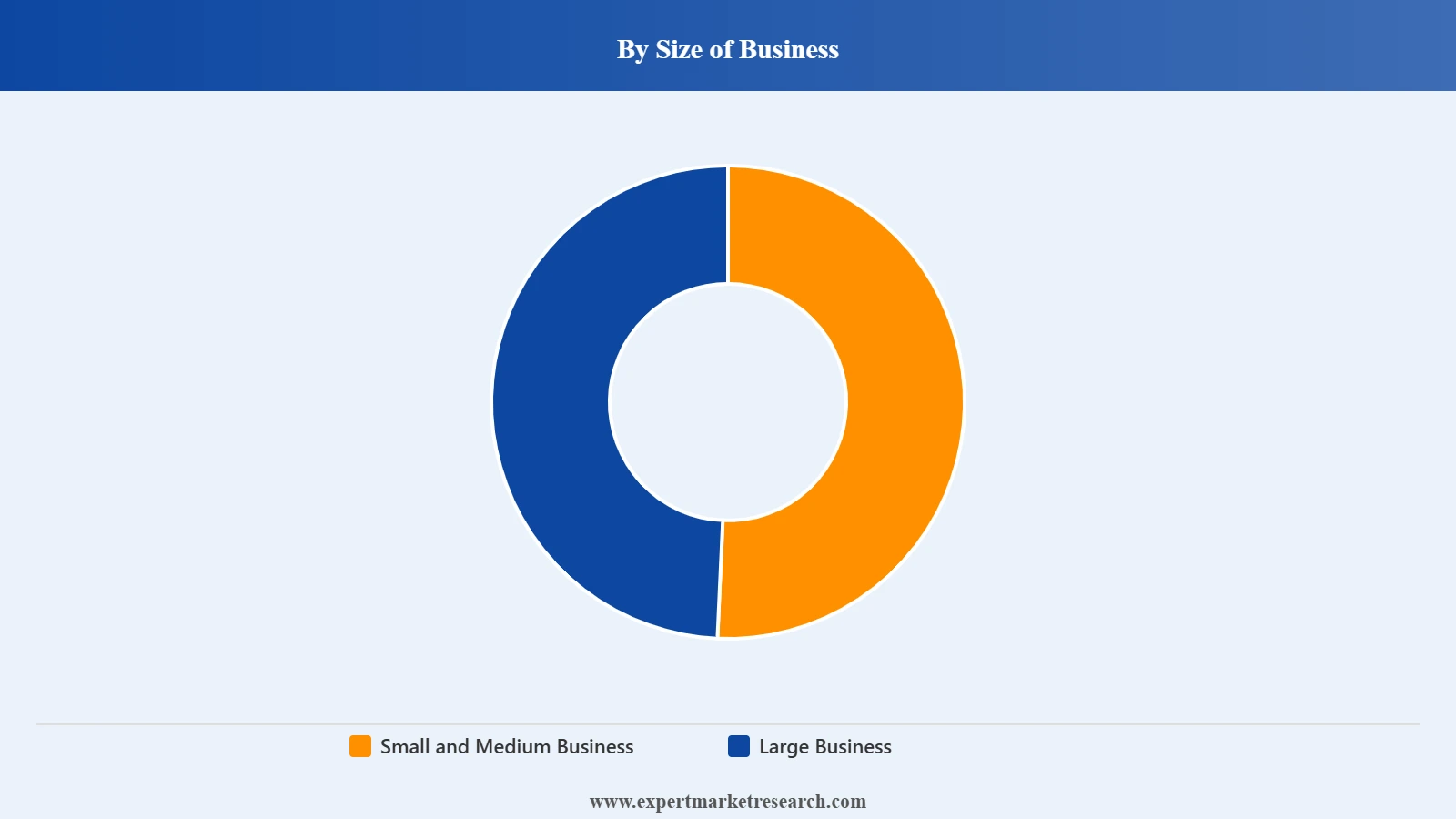

Market Breakup by Size of Business

Key Insight: Large business commands the dominant share of the United States financial services market by size of business through investment banking, commercial lending, treasury management, and institutional asset management services. However, the small and medium business segment is the faster-growing category, driven by fintech lender expansion, bank branch initiatives targeting SMEs, and embedded finance solutions enabling efficient digital access to working capital, payments, and insurance for smaller enterprises.

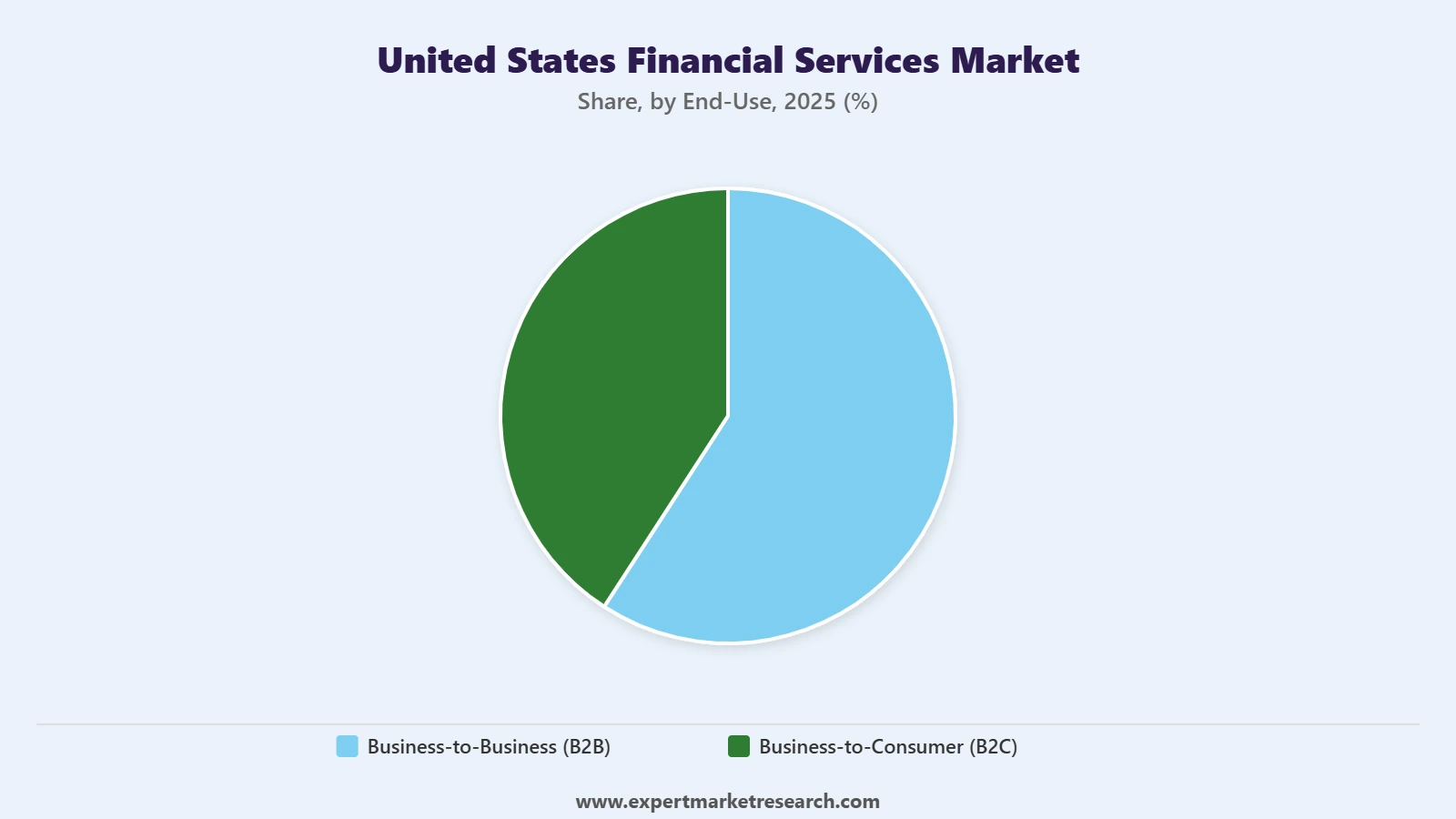

Market Breakup by End-Use

Key Insight: B2B end-use commands the largest share of the United States financial services market by value, reflecting the scale of institutional banking, corporate treasury management, investment banking fees, and commercial insurance premiums transacted between financial institutions and business clients. B2C represents the largest segment by customer volume, driven by consumer banking, retail insurance, and personal investment products serving over 215 million digital banking users across the country.

Market Breakup by Region

Key Insight: MIDEAST dominates the United States financial services market by region, anchored by New York City as the global capital of investment banking, equity markets, hedge funds, and institutional asset management. Wall Street headquarters of JPMorgan Chase, Citigroup, and Goldman Sachs generate the highest concentration of fee income nationally. FAR WEST, anchored by California, Silicon Valley, and San Francisco, is a major fintech hub and the leading region for venture capital-backed financial services innovation and digital-first banking adoption.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

By Type, banking accounts for the dominant share of the market due to the scale of the US commercial and retail banking system and the breadth of financial products offered.

Banking holds the largest share of the United States financial services market, reflecting the scale, reach, and product breadth of major commercial banks. The US banking system's total assets exceed USD 20 trillion, with JPMorgan Chase alone holding USD 4.4 trillion as of year-end 2025. Consumer banking, commercial lending, trade finance, and treasury services collectively represent enormous fee and net interest income streams. JPMorgan's plan to open over 500 new branches by 2027 reinforces the continued strategic value of physical banking distribution in the US.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Wealth management is the fastest-growing segment within the United States financial services market by type, driven by record US household wealth of approximately USD 156 trillion per Federal Reserve data. Fee-based advisory models are displacing commission-based structures as clients increasingly prioritise fiduciary accountability and holistic financial planning. Edward Jones Investments serves over 8 million clients through its nationwide financial advisor network, while Goldman Sachs expands its Marcus consumer wealth platform to capture the growing mass-affluent segment.

By Size of Business, large business accounts for the dominant share of the market due to the scale of institutional banking, corporate finance, and commercial insurance services.

Large business accounts for the majority of United States financial services market revenue by size category, driven by the massive transaction volumes and fee income generated through investment banking advisory, corporate loan syndication, institutional asset management, and large commercial insurance underwriting. JPMorgan Chase, Citigroup, and Goldman Sachs serve the largest US and global corporations through integrated financial services platforms that generate disproportionate revenues relative to their client counts.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

The small and medium business segment of the United States financial services market is the higher-growth category, as fintech-driven innovation lowers the cost of SME financial services delivery. Digital lending platforms, automated bookkeeping integrations, and embedded payroll-linked financial products are enabling banks and non-bank providers to serve smaller businesses profitably at scale. Capital One's small business card and lending expansion and U.S. Bancorp's digital SME banking platform are representative of the competitive investment being directed at this segment.

By End-Use, B2B accounts for the dominant share of the market due to the scale of institutional and corporate financial services transactions in the United States.

B2B end-use accounts for the largest value share of the United States financial services market, driven by investment banking fees, corporate lending, institutional fund management, commercial insurance, and inter-bank financial transactions. The scale of US corporate capital markets activity, including M&A advisory, equity and debt underwriting, and derivatives markets, generates enormous annual fee income that is captured predominantly within the B2B segment. Goldman Sachs reported record equities trading revenues in Q1 2026, demonstrating sustained strength in institutional B2B financial services demand.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

B2C represents the largest segment by customer volume in the United States financial services market, encompassing consumer banking, retail insurance, personal investment accounts, and individual retirement planning products serving over 215 million digital banking users as of 2025. Bank of America's Erica AI assistant, serving tens of millions of consumers, and Nationwide Mutual's expansion of personal lines insurance products represent the continued investment in B2C digital experiences that drive customer acquisition and retention across major institutions.

Strategic Growth Opportunities in the US Financial Services Sector

The US financial services market presents a rich array of strategic growth opportunities for incumbents and new entrants alike. These opportunities are emerging at the intersection of technology, demographic change, evolving consumer preferences, and shifting regulatory frameworks.

Open Banking and API-Driven Ecosystem Development

The gradual adoption of open banking principles in the United States accelerated by the Consumer Financial Protection Bureau's proposed data access rules under Section 1033 of the Dodd-Frank Act is creating conditions for an API-driven financial ecosystem similar to those established in the EU under PSD2. Financial institutions that invest early in secure, developer-friendly API infrastructure will be positioned to monetize data sharing, attract fintech partners, and participate in multi-product financial ecosystems that extend their addressable market beyond traditional account relationships.

Wealth Management and Robo-Advisory for Retail Investors

The democratization of wealth management through robo-advisory platforms led by Betterment, Wealthfront, and Schwab Intelligent Portfolios has opened the investment advisory market to retail participants with as little as USD 1 in investable assets. As the Gen Z and Millennial wealth transfer accelerates over the next decade, robo-advisory platforms that combine automated portfolio management with human advisor access (hybrid advisory) are expected to capture disproportionate market share. Total assets under management in the US robo-advisory segment are forecast to grow substantially through 2035.

ESG Investing and Sustainable Finance Demand

Environmental, social, and governance (ESG) investing has evolved from a niche institutional preference into a mainstream retail investment theme. US asset managers overseeing ESG-aligned funds collectively manage trillions in assets, and demand from institutional investors including public pension funds, endowments, and sovereign wealth funds continues to expand the investable universe for sustainable finance products. Regulatory pressure toward climate risk disclosure, combined with growing retail demand for impact-aligned portfolios, is creating durable growth conditions for ESG-focused asset managers, green bond issuers, and sustainability-linked lending platforms.

MIDEAST dominates the market due to New York City's unparalleled concentration of investment banks, asset managers, and capital markets infrastructure.

MIDEAST holds the dominant position in the United States financial services market, led by New York City's status as the global capital of investment banking, institutional asset management, hedge funds, and equity markets. JPMorgan Chase, Citigroup, Goldman Sachs, MetLife, and numerous other tier-one institutions are headquartered in New York, collectively generating the highest concentration of financial services fee income, employment, and capital deployment in the country. The region's deep talent pool and regulatory proximity make it structurally irreplaceable as the US financial centre.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

SOUTHEAST is the fastest-growing region within the United States financial services market, driven by rapid population inflows from northern states, strong business formation rates, and the emergence of financial services hubs in Miami, Atlanta, Dallas, and Charlotte. Bank of America, headquartered in Charlotte, is a cornerstone of the Southeast's financial infrastructure. JPMorgan's plans to open over 500 branches nationally include significant Southeast expansion to capture the region's growing consumer and SME market. Miami's emergence as a Latin American-connected financial hub is attracting international banking and wealth management investment.

The United States financial services market is characterised by a high degree of concentration at the top, with JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, and Goldman Sachs commanding a dominant share of total banking assets, investment banking fees, and institutional services revenues. These institutions benefit from scale advantages in capital, technology investment, regulatory compliance infrastructure, and multi-product cross-selling capabilities that are difficult for smaller players to replicate.

Competition is intensifying from multiple directions: fintech companies attacking high-margin lending and payments segments, digital neobanks reducing acquisition costs for consumer banking, and non-bank financial institutions expanding into credit and insurance. The deregulatory environment of 2025 is widely expected to accelerate consolidation as larger institutions seek acquisition targets to expand geographic reach or add specialised capabilities. Record profitability is providing the capital base for both organic investment and strategic acquisitions across the United States financial services market.

Founded in 1799 and headquartered in New York City, JPMorgan Chase and Co. is the largest bank in the United States and one of the largest financial institutions in the world, with USD 4.4 trillion in assets at year-end 2025. The firm operates across consumer and community banking, commercial banking, investment banking, asset and wealth management, and financial transaction processing. JPMorgan announced plans to open over 500 new branches by 2027, reinforcing its physical and digital growth strategy across the United States financial services market.

Founded in 1904 and headquartered in Charlotte, North Carolina, Bank of America Corporation is the second-largest US bank with approximately USD 3.3 trillion in assets. The company serves approximately 67 million consumer and small business clients through its nationwide banking network and digital platform, including the Erica AI-powered virtual financial assistant serving tens of millions. Bank of America's stock reached a record high in December 2025, surpassing its pre-financial crisis peak, reflecting the strength of its diversified financial services business model.

Founded in 1812 and headquartered in New York City, Citigroup, Inc. is a global financial services company and one of the largest US banks, operating in over 160 countries. Citigroup provides consumer banking, institutional banking, credit cards, and investment banking services. In 2025, Citigroup's stock surpassed its book value per share for the first time in seven years, reflecting the significant progress of its multi-year organisational transformation and strategic refocusing on core institutional and consumer financial services in the United States financial services market.

Founded in 1852 and headquartered in San Francisco, California, Wells Fargo and Company is one of the United States' largest diversified financial services companies, offering banking, investment, mortgage, and consumer and commercial finance products. Wells Fargo's stock reached record highs in 2025 as analysts projected continued outperformance driven by operational efficiency improvements, net interest income recovery, and the resolution of legacy regulatory constraints that had capped its balance sheet growth since 2018.

Other key players in the market are U.S. Bancorp, The Goldman Sachs Group Inc., TD Bank, N.A., MetLife, Inc., Edward Jones Investments, Nationwide Mutual Insurance Company, Farmers Insurance Group, Capital One Financial Corporation, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead of the transformation in United States financial services industry from 2026 with our comprehensive market report. Gain intelligence on banking expansion strategies, wealth management growth, AI-driven service delivery, and regional market dynamics shaping competitive positioning. Whether you are a financial institution, fintech company, or institutional investor, this report delivers the clarity you need. Download your free sample today and discover the key opportunities in the thriving United States financial services industry through 2035.

United Kingdom Financial Services Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The United States financial services market reached a value of nearly USD 65.18 Billion in 2025.

The United States financial services market is projected to grow at a CAGR of 7.47% between 2026 and 2035.

The major drivers of the market include the growing demand for insurance and loans, global economic growth and increasing number of start-up businesses.

The increasing interest of service companies to locate their service headquarters in the nation and the adoption of advanced technologies are the key industry trends propelling the growth of the market.

Banking is the dominant type of financial service in the United States financial services market.

The major end-uses of the financial services market in the United States include the Business-to-Business (B2B) and Business-to-Consumer (B2C).

The major players in the industry are JPMorgan Chase & Co., Bank of America Corporation, Citigroup, Inc., Wells Fargo & Company, U.S. Bancorp, The Goldman Sachs Group Inc., TD Bank, N.A., MetLife, Inc, Edward Jones Investments, Nationwide Mutual Insurance Company, Farmers Insurance Group, and Capital One Financial Corporation, among others.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of USD 133.96 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Size of Business |

|

| Breakup by End-Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.