Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

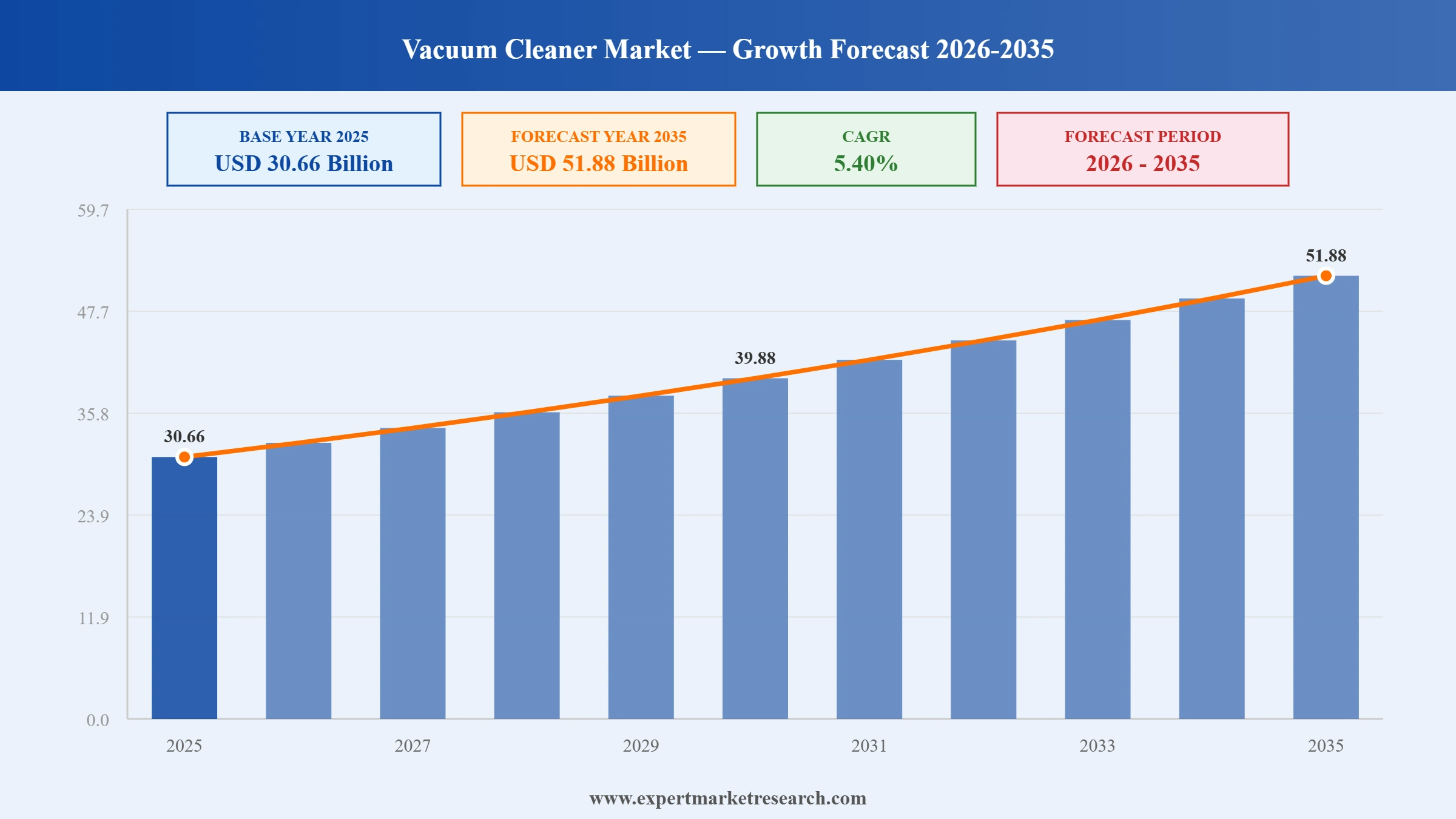

The global vacuum cleaner market reached a value of USD 30.66 Billion at 2025 and is projected to expand at a CAGR of around 5.40% during the forecast period of 2026-2035. With growing demand for smart and robotic cleaning solutions, rising awareness of indoor air hygiene, accelerating adoption of AI-powered vacuum systems, and expanding residential and commercial cleaning requirements, the market is expected to reach USD 51.88 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Vacuum Cleaner Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 30.66 |

| Market Size 2035 | USD Billion | 51.88 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.40% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 6.2% |

| CAGR 2026-2035 - Market by Country | India | 7.1% |

| CAGR 2026-2035 - Market by Country | China | 6.0% |

| CAGR 2026-2035 - Market by Product | Robotic | 7.6% |

| CAGR 2026-2035 - Market by Distribution Channel | Offline Stores | 8.6% |

| Market Share by Country 2025 | UK | 3.3% |

The global vacuum cleaner market is undergoing a notable structural transformation, driven by the rapid integration of artificial intelligence, robotics, and smart connectivity into product design. Consumer demand is shifting visibly toward automated, multi-functional cleaning solutions that deliver both convenience and hygiene performance, particularly within residential applications in fast-growing urban centres. These shifts are creating competitive pressure on traditional vacuum manufacturers while simultaneously opening fresh opportunities for innovation-led companies to capture meaningful market share.

Samsung and LG showcased new robot vacuum models at CES 2026 featuring high-temperature steam cleaning, advanced AI navigation, and embedded security capabilities. Samsung's Bespoke AI Steam model incorporates 100-watt suction power and auto-extending brushes that target corners, while LG introduced a built-in docking station with fully hands-free functionality including automatic water supply, mop washing, and dust disposal.

LG Electronics showcased four vacuum cleaning products tailored specifically for the European market at IFA 2025 in Berlin. The new lineup includes a robot vacuum with steam mopping capability, a built-in docking station, a cordless stick vacuum, and a wet-dry stick vacuum. Powered by on-device AI for improved navigation and automatic carpet detection, LG's IFA range reinforces the brand's strategy of combining performance with smart home integration for European consumers.

Roborock unveiled the Saros Z70 at CES 2025, the first mass-produced robot vacuum equipped with a foldable five-axis mechanical arm branded OmniGrip. Combining 22,000 Pa suction power with StarSight Autonomous System 2.0 navigation and AI-powered obstacle detection, the Saros Z70 can identify, lift, and relocate small household objects while delivering simultaneous vacuuming and mopping, setting a new benchmark for robotic cleaning automation.

SharkNinja launched the Shark PowerDetect NeverTouch Pro 2-in-1 Robot Vacuum and Mop in September 2024, targeting the premium residential cleaning segment. The device features NeverStuck technology for autonomous obstacle navigation and threshold crossing, combined with PowerDetect sensors that identify dirt levels, floor types, and edge patterns to deliver adaptive, precision cleaning performance throughout the home.

AI-powered navigation is redefining performance benchmarks in the global vacuum cleaner market. Manufacturers are embedding LiDAR, 3D Time-of-Flight sensors, and machine learning algorithms to enable real-time mapping and adaptive cleaning. Roborock's Saros Z70, launched in January 2025, exemplifies this shift by integrating a foldable robotic arm and 22,000 Pa suction into a single autonomous device.

Heightened awareness of indoor air quality is accelerating adoption of HEPA-equipped vacuums across the global vacuum cleaner market. Approximately 78% of households consider clean indoor air a priority, per American Cleaning Institute data, boosting demand for HEPA-integrated models that effectively capture allergens, dust mites, pollen, and fine particulate matter within residential environments.

E-commerce platforms are reshaping the vacuum cleaner market growth landscape as consumers prioritise convenience and price transparency. Leading brands including Samsung, LG, and Ecovacs have strengthened direct-to-consumer digital channels, while platforms such as Amazon have become central to product discovery, review-driven decision-making, and repeat purchase activity across major markets.

Rapid urbanisation and the rise of dual-income households are sustaining robust residential demand within the global vacuum cleaner market. Rising disposable incomes and growing hygiene consciousness are encouraging consumers to upgrade from conventional to smart, cordless, or robotic vacuum models, with vacuum cleaner market growth particularly pronounced across urban centres in Asia Pacific, Europe, and North America.

The vacuum cleaner market is witnessing broadening demand across commercial and industrial environments as hygiene and workplace safety regulations tighten globally. Facilities management in healthcare, hospitality, and manufacturing sectors are deploying HEPA-filtered and high-suction drum vacuum solutions for compliance and operational efficiency. In June 2025, Tennant recorded its 10,000th robotic scrubber sale, reflecting growing adoption of intelligent commercial cleaning systems.

The report of Expert Market Research's titled "Vacuum Cleaner Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

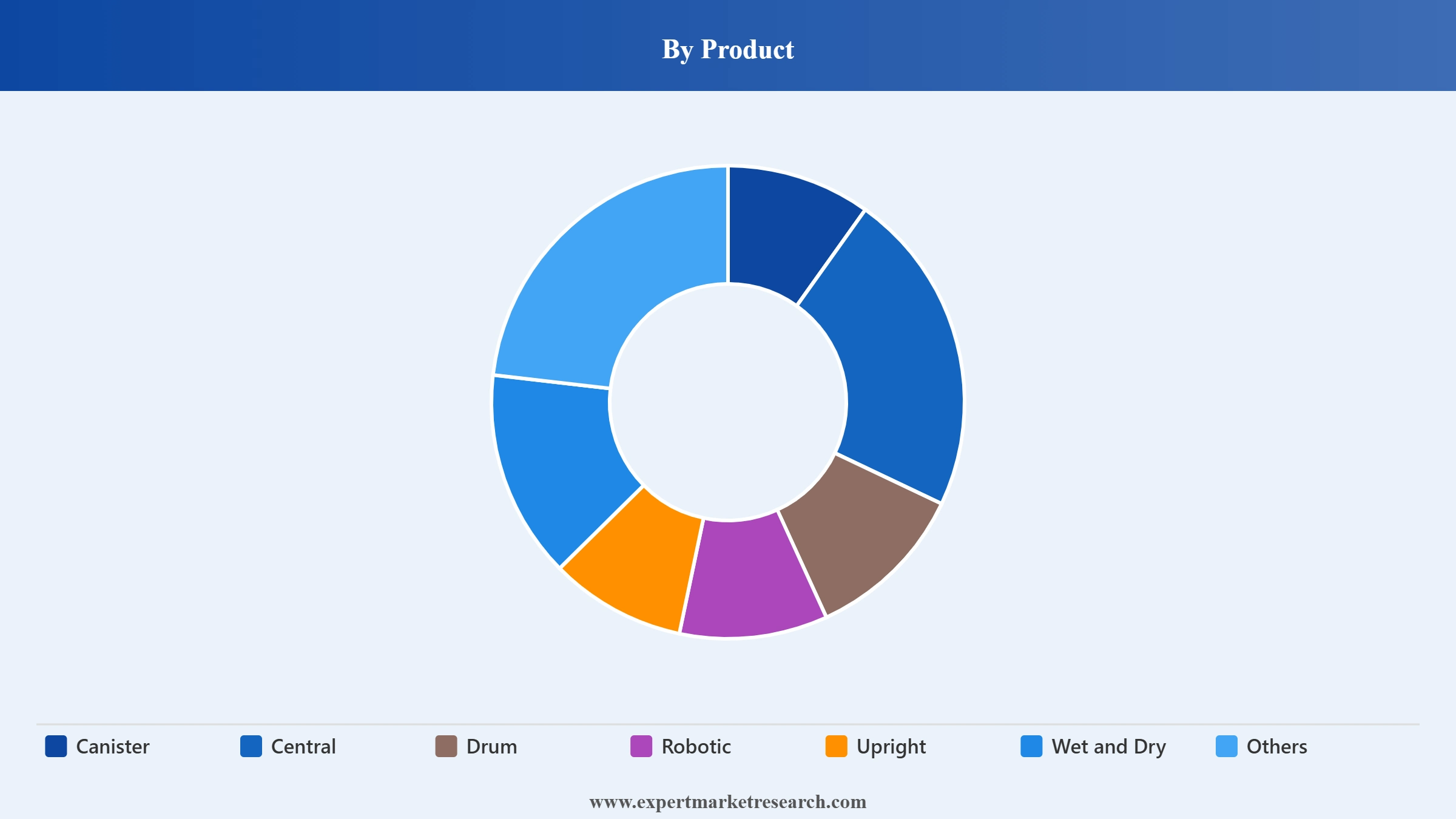

Market Breakup by Product

Key Insight: The canister vacuum cleaner segment holds the largest share of the global vacuum cleaner market, driven by its distinctive design that separates the motor from the cleaning head via a flexible hose. This configuration provides users with superior manoeuvrability, making it highly effective for cleaning stairs, furniture undersides, and narrow spaces that upright vacuums cannot easily access. Growing availability of HEPA-filter-enabled canister models has further reinforced consumer preference, particularly among allergy-sensitive households. Among the fastest-growing sub-segments, robotic vacuum cleaners are gaining strong momentum on the back of AI navigation improvements and rising smart home adoption. Brands including Roborock, Ecovacs, and SharkNinja are continuously expanding their robotic portfolios with self-emptying bases, LiDAR mapping, and hybrid mopping capabilities, making automation accessible to a broader global audience.

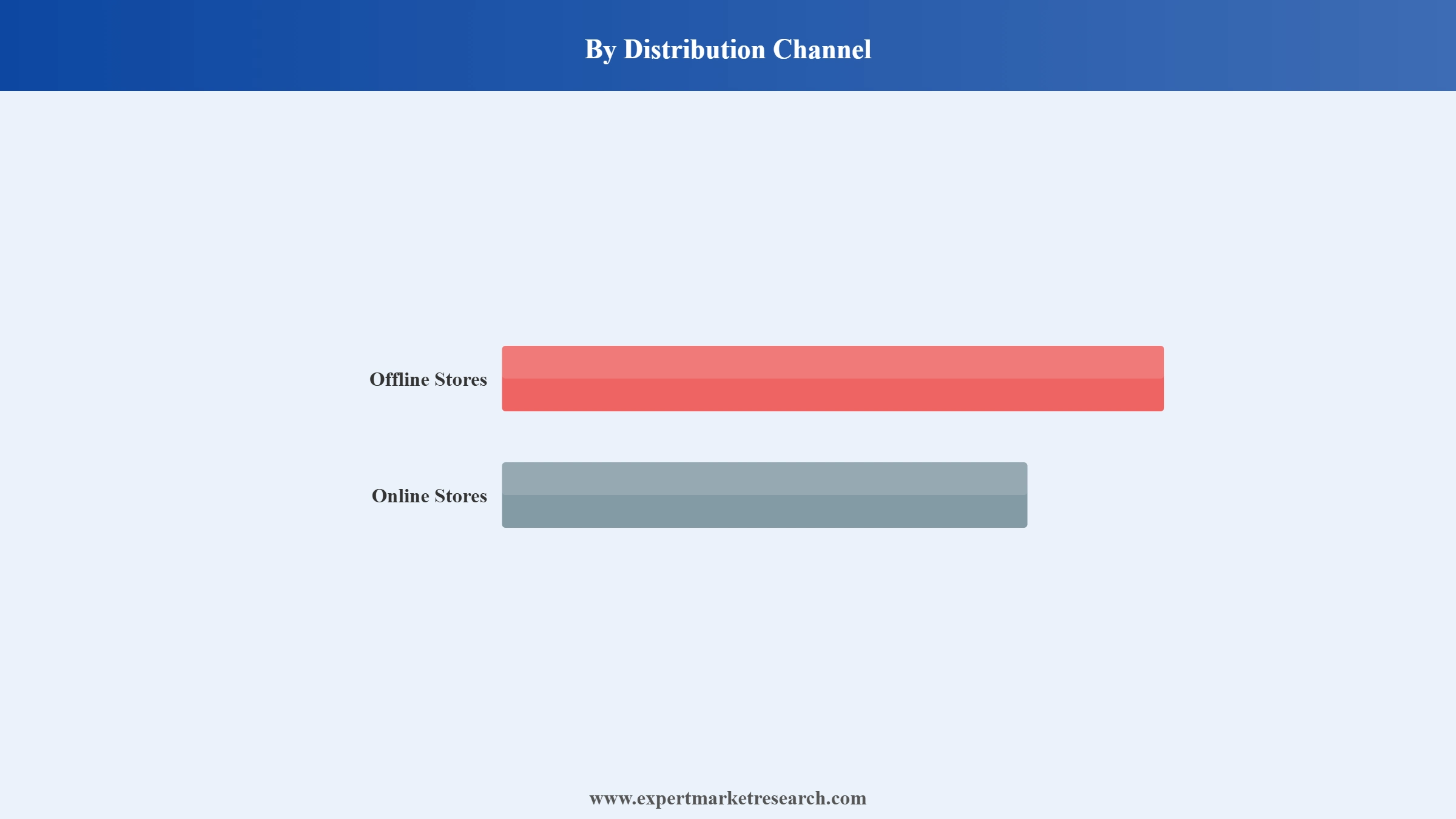

Market Breakup by Distribution Channel

Key Insight: The online stores segment dominates distribution in the global vacuum cleaner market, reflecting broader shifts in consumer purchasing behaviour across electronics and home appliances. Digital platforms offer buyers convenient access to comprehensive product catalogues, comparison tools, and competitive discounts that physical stores struggle to replicate. Leading manufacturers including Samsung, LG, and Ecovacs have strengthened direct-to-consumer online channels to widen market reach and improve margins. The growing same-day and next-day delivery infrastructure across North America and Asia Pacific has further reduced buyer hesitation around online appliance purchases. The offline channel retains relevance, particularly for premium purchases where consumers prefer a hands-on product evaluation experience, in-store demonstrations, and access to after-sales servicing commitments from established retail chains.

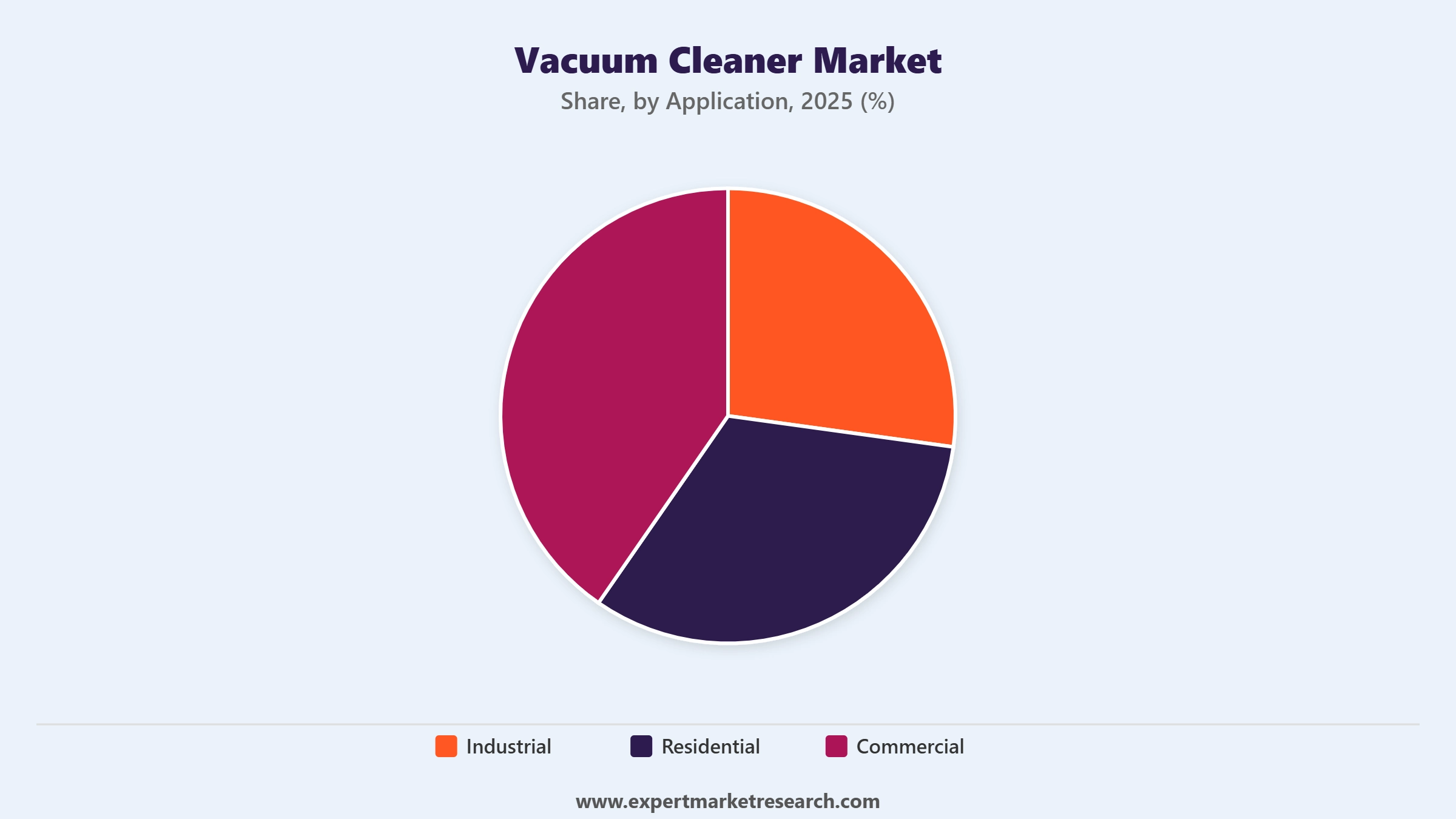

Market Breakup by Application

Key Insight: The residential segment accounts for the dominant share of the global vacuum cleaner market, propelled by rising household incomes, increasing health and hygiene consciousness, and the growing popularity of smart home automation. Urbanisation trends and the proliferation of dual-income households have expanded demand for time-efficient cleaning appliances, especially cordless and robotic models that minimise manual effort. Commercial applications, including offices, hotels, and healthcare facilities, represent the second-largest segment, driven by heightened hygiene standards and facility management requirements. The industrial segment is on a steady growth path, supported by tightening workplace safety regulations in sectors such as pharmaceuticals, metalworking, construction, and food processing, where high-suction drum and portable vacuum systems are essential for controlling dust and maintaining safe working environments.

Market Breakup by Region

Key Insight: Asia Pacific leads the global vacuum cleaner market in terms of growth potential, underpinned by rapid urbanisation, an expanding middle-class consumer base, and growing adoption of smart home technologies across China, Japan, India, and Southeast Asia. North America remains a highly significant market driven by strong consumer purchasing power, established brand loyalty, and consistent product replacement cycles. Europe follows closely, with demand shaped by EU energy efficiency regulations, consumer preference for compact and eco-designed appliances, and the influence of well-established German and British brands. Latin America and the Middle East and Africa represent emerging markets where rising incomes, improving retail infrastructure, and growing awareness of home hygiene are gradually broadening access to vacuum cleaning products across residential and commercial segments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product, canister vacuum cleaners dominate the market due to high versatility, ergonomic design, and broad multi-surface consumer adoption

Canister vacuum cleaners lead the global vacuum cleaner market by holding the largest product segment share, underpinned by their unique structural design that separates the motor and dust collection unit from the cleaning head via a flexible hose. This configuration delivers superior manoeuvrability that makes these units highly effective across stairs, under furniture, behind appliances, and along narrow corridors where upright models lose efficiency. Canister vacuums support a wide range of detachable cleaning tools, enabling consistent performance across carpeted, tiled, and hardwood surfaces in both residential and commercial settings. Growing availability of HEPA-filter-integrated canister models has further strengthened consumer preference, particularly within households managing allergies, asthma, or respiratory sensitivities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The robotic vacuum segment represents the most compelling growth engine within the vacuum cleaner industry, expanding rapidly on the back of AI navigation advances and the accelerating smart home technology wave. Brands such as Roborock, Ecovacs, and SharkNinja are continuously raising the performance bar through features including self-emptying dustbins, hybrid mopping capabilities, and advanced room-mapping algorithms. In January 2025, Roborock unveiled the Saros Z70 at CES 2025, the world's first mass-produced robot vacuum with a five-axis mechanical arm, illustrating how the robotic sub-segment is transitioning from basic floor automation toward full intelligent home assistance.

By Distribution Channel, online stores account for the dominant share of the market due to growing e-commerce adoption and competitive pricing advantages

Online stores have become the leading distribution channel in the global vacuum cleaner market, reflecting a broader shift in consumer purchasing behaviour across home appliances and electronics. E-commerce platforms give buyers convenient access to wide product catalogues, detailed comparison tools, and competitive discounts that physical stores find difficult to replicate. Manufacturers including Samsung, LG, Ecovacs, and Roborock have actively strengthened direct-to-consumer digital channels to broaden market reach and improve pricing control. The expansion of same-day and next-day delivery infrastructure in key regions, particularly across North America and Asia Pacific, has meaningfully reduced buyer hesitation around online appliance purchases and accelerated digital conversion rates.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The offline channel retains a meaningful position within the global vacuum cleaner market growth picture, especially for premium and high-value purchases where consumers prefer hands-on product evaluation. Physical retail chains, home appliance superstores, and electronics outlets offer in-store product demonstrations, after-sales service packages, and flexible financing options that remain attractive to a significant consumer base. Hybrid retail strategies, combining online discovery and research with in-store purchasing decisions, are gaining traction among leading brands that are keen to serve multi-channel shopping preferences.

By Application, residential use accounts for the dominant share of the market due to rising household incomes, growing hygiene awareness, and increased demand for automated home cleaning solutions

Residential applications dominate the global vacuum cleaner market, driven by fundamental changes in consumer lifestyle and growing awareness of the health implications of poor indoor air quality. The rise of dual-income households across Asia, North America, and Europe has intensified the premium placed on time-saving, automated cleaning solutions. Cordless and robotic vacuum cleaners have become particularly sought-after in urban residences, where compact living spaces and busy schedules create persistent demand for efficient, low-effort maintenance technologies. Consumer interest in HEPA-filter-equipped residential models has surged as the incidence of dust allergies, asthma, and other respiratory conditions continues to rise globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Commercial and industrial applications are forming an increasingly important secondary demand pillar within the vacuum cleaner industry. The commercial segment encompasses hotels, hospitals, corporate offices, and retail environments, where high-performance and durable vacuum solutions are required for daily maintenance routines. Industrial demand is advancing steadily, underpinned by stricter regulatory enforcement of workplace dust exposure limits in pharmaceutical, metalworking, construction, and food manufacturing sectors. In June 2025, Tennant highlighted the sale of its 10,000th robotic scrubber, reflecting the growing procurement interest in intelligent cleaning systems across industrial and facilities management operations.

Asia Pacific dominates the market due to rapid urbanisation, rising disposable incomes, and strong smart home adoption across China, India, and Japan

Asia Pacific holds the largest and fastest-growing share of the global vacuum cleaner market, underpinned by an expanding urban population, a rapidly growing middle class, and deepening penetration of smart home technologies across the region's most populous economies. China functions as both the world's leading vacuum cleaner production hub and one of its most significant consumer markets, with annual output of approximately 200 million units supported by an extensive manufacturing infrastructure and competitive export network. India is emerging as a high-growth market as rising consumer spending on home appliances coincides with accelerating urbanisation and improving household income levels. Japan and South Korea continue to drive premiumisation trends, with consumers embracing advanced robotic and cordless models at notably high adoption rates.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America represents the second most significant regional market in the global vacuum cleaner landscape, characterised by high consumer spending power, strong brand loyalty to established players, and consistent product replacement cycles. The United States accounts for the bulk of regional demand, supported by broad retail distribution, active e-commerce adoption, and a mature smart home ecosystem. Cordless vacuum adoption has exceeded 62% penetration in urban US households, while robotic vacuum ownership approaches 29%, reflecting a well-developed consumer appetite for premium and automated cleaning solutions. Major manufacturers including SharkNinja and iRobot are headquartered in the region, driving continuous product innovation and sustaining consumer engagement through active seasonal promotions and retail partnerships.

The global vacuum cleaner market features a moderately competitive structure combining large multinational electronics corporations with specialist cleaning appliance brands. Market participants are intensifying investment in AI-driven robotics, advanced filtration technology, and smart home integration to differentiate their offerings in an increasingly crowded product landscape. Chinese manufacturers, including Roborock and Ecovacs, have significantly eroded the market share of legacy Western and Korean brands through aggressive pricing, rapid product iteration, and feature-rich flagship models that appeal to both premium and value-seeking consumers.

Strategic consolidation, product diversification, and geographic expansion remain the dominant competitive priorities. Leading brands are investing heavily in premium and mid-premium AI-powered vacuum models while also exploring adjacent product categories, including washing machines and air purifiers, to build broader connected home care ecosystems. E-commerce capabilities, direct-to-consumer digital channels, and data-driven personalisation are emerging as key differentiators within the mature North American and European markets.

LG Electronics, founded in 1958 and headquartered in Seoul, South Korea, is a global leader in consumer electronics and home appliances with operations in over 100 countries. Its vacuum product line includes the CordZero cordless and robotic cleaning series, featuring AI chip-based navigation, on-device obstacle recognition, and auto-emptying docking towers. LG has a well-established global distribution network and strong brand equity in residential appliances, with a growing strategic focus on smart home ecosystem integration and premium cleaning technology.

Ecovacs Robotics, founded in 1998 and headquartered in Suzhou, China, is a specialist in smart home cleaning solutions with a commercial presence across more than 60 countries. The company's Deebot series is among the most recognised robotic vacuum product families globally, consistently updated with AI navigation, self-emptying base systems, and hybrid vacuum-mopping capabilities. Ecovacs has positioned itself as a formidable challenger to legacy brands in the premium robotic vacuum segment through disciplined R&D investment and competitive pricing strategies.

SharkNinja, founded in 1994 and headquartered in Needham, Massachusetts, United States, operates across both the Shark vacuum and Ninja kitchen appliance segments. The Shark PowerDetect product range is well-regarded for high suction performance, innovative dirt-detection sensors, and consumer-friendly pricing that bridges the mid-premium and premium segments. The company commands a substantial share of the North American vacuum cleaner market and has been actively expanding its footprint across Europe through partnerships with major retail chains and digital distribution platforms.

Roborock, founded in 2014 and headquartered in Beijing, China, has established itself as one of the fastest-growing brands in the global robotic vacuum cleaner segment. Its Saros series, including the Saros Z70 with the proprietary OmniGrip mechanical arm technology, represents the cutting edge of autonomous cleaning innovation. Roborock holds approximately 16% global robot vacuum market share and maintains strategic subsidiaries across the United States, Japan, Germany, Netherlands, Poland, and South Korea, supporting its international expansion ambitions.

Other key players in the market are Haier Inc., Miele and Cie. KG, Samsung Electronics Co. Ltd, BISSELL Homecare Inc., Panasonic Corporation, iRobot Corporation, Koninklijke Philips N.V., Eureka Forbes Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest intelligence on the global vacuum cleaner market 2026 with our comprehensive research report. From AI-powered robotic cleaning platforms and HEPA filtration advancements to the fastest-growing regional markets and competitive dynamics, this study delivers the data you need to stay ahead. Whether you are expanding a product line, evaluating a new geography, or benchmarking against key competitors, this report gives you the clarity to act decisively. Download your free sample today and uncover the most promising opportunities in the growing vacuum cleaner space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 30.66 Billion.

The market is projected to grow at a CAGR of 5.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of USD 51.88 Billion by 2035.

The increasing burden of infections and contamination-induced diseases across residential and commercial areas, rising demand for vacuum cleaners from hospitals, and rising hygienic consciousness are the major drivers of the market.

The key trends in the market include the technological innovations by the major market players to reduce the weight and increase the efficiency of vacuum cleaners and increasing incorporation of vacuum cleaners in smart homes.

Canister, central, drum, robotic, upright, and wet and dry, among others are the different products in the market.

Offline stores and online stores are the various distribution channels of the market.

A vacuum cleaner is used for cleaning dust and contaminants easily across large areas and in hard-to-reach places.

Depending upon exposure to dust and dirt, vacuum cleaner can be used twice a week or more frequently as needed.

The key players in the market include LG Electronics Inc., Haier Inc., Miele & Cie. KG, Samsung Electronics Co., Ltd, BISSELL Homecare, Inc., Panasonic Corporation, iRobot Corporation, Koninklijke Philips N.V., Eureka Forbes Ltd., SharkNinja Operating LLC, Ecovacs Robotics, Inc., Beijing Roborock Technology Co., Ltd, and Others.

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa are the major regions covered in the market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Distribution Channel |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.