Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

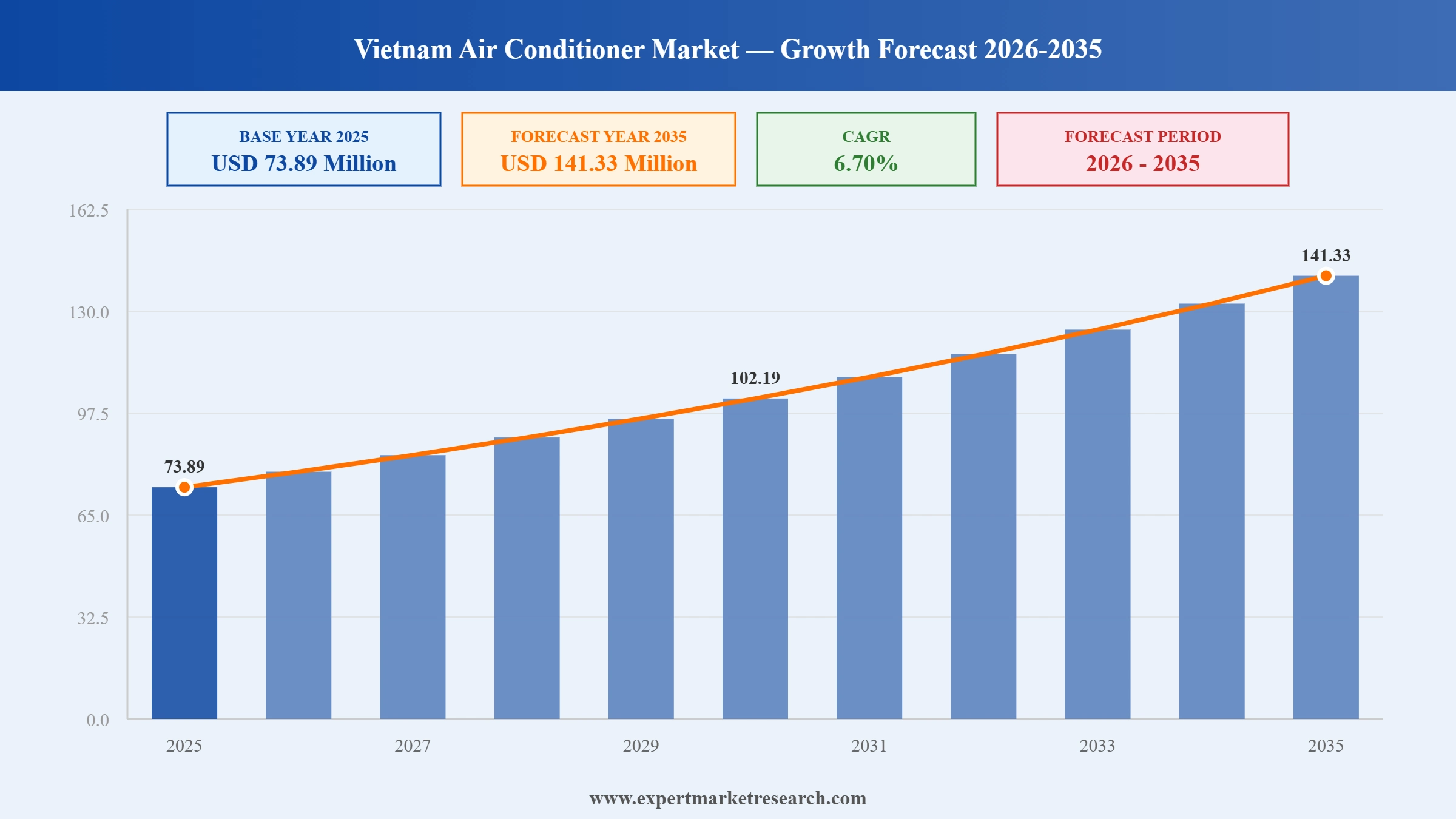

The Vietnam Air Conditioner Market reached a value of USD 73.89 Million at 2025 and is projected to expand at a CAGR of around 6.70% during the forecast period of 2026-2035. With rapid urbanisation and new residential and commercial construction activity, growing consumer demand for smart and IoT-enabled air conditioners, sustained heat intensity from Vietnam's tropical climate being exacerbated by climate change, and accelerating adoption of inverter technology driven by energy cost sensitivity, the market is expected to reach USD 141.33 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Vietnam Air Conditioner Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

73.89 |

|

Market Size 2035 |

USD Million |

141.33 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

6.70% |

|

CAGR 2026-2035 - Market by Region |

Southeast |

7.6% |

|

CAGR 2026-2035 - Market by Region |

Mekong River Delta |

6.9% |

|

CAGR 2026-2035 - Market by Type |

Central AC |

7.2% |

|

CAGR 2026-2035 - Market by Distribution Channel |

Online |

7.8% |

|

2025 Market Share by Region |

Mekong River Delta |

14.5% |

The Vietnam Air Conditioner Market is being reshaped by the convergence of climate urgency, technology-driven product innovation, and structural economic growth. Rising temperatures, expanding urban infrastructure, and a young, digitally engaged consumer base are collectively accelerating the pace of market expansion and product category evolution.

In July 2025, Samsung Vina introduced a new line of smart system air conditioners specifically designed for the Vietnamese market. The product lineup integrates Wi-Fi connectivity, energy-saving operating modes, and quieter performance benchmarks tailored to urban apartment and home environments across Vietnam's growing cities. The launch reinforces Samsung's positioning in the premium and smart AC segment in Vietnam, where consumer appetite for connected home climate solutions is accelerating in tandem with rising smartphone penetration and smart home adoption among the urban middle class.

In March 2025, AUX Air Conditioning, a major Chinese HVAC manufacturer, officially entered the Vietnamese market with its C-Series air conditioning units. The products are engineered for high performance in tropical climatic conditions, featuring low noise output, corrosion-resistant finishes suitable for coastal environments, and straightforward maintenance. AUX backed the launch with a commitment of approximately USD 4 million in annual investment toward building sales networks, warehouse infrastructure, and customer support capability, with the stated aim of achieving a 15% market share within three years of entry.

In 2025, Daikin Vietnam introduced a new range of smart air conditioners featuring integrated Wi-Fi connectivity, D-Mobile application control, and humidity optimisation technology calibrated for Vietnam's tropical climate. The product line allows users to remotely manage temperature, schedule operating times, and monitor energy usage through their smartphones. Daikin's continued investment in Vietnam-specific smart product development reflects the brand's strategy to maintain its premium market leadership as the competitive landscape intensifies with the arrival of new Chinese and Korean players targeting the mid-range segment.

In 2025, the Vietnamese government implemented mandatory energy-performance standards for non-ducted air conditioners, requiring compliance with new minimum energy efficiency benchmarks across all products sold in the domestic market. The new regulations, aligned with Vietnam's National Energy Efficiency Program (VNEEP), are designed to phase out lower-efficiency fixed-speed units and accelerate the transition to inverter technology. For manufacturers, the regulations represent both a compliance burden and a market opportunity, as the upgraded standard effectively raises the floor of consumer expectations and creates demand for a higher category of products.

In 2025, Xiaomi expanded its Mijia brand air conditioner lineup into the Vietnamese retail market, targeting the budget-to-mid-range segment with competitively priced units that combine inverter cooling technology with smart home connectivity compatible with the Xiaomi ecosystem. The launch capitalises on Xiaomi's already established consumer electronics brand presence in Vietnam and its strong digital retail channel capabilities. The move is part of a broader wave of Chinese smart appliance brands entering Vietnam's growing air conditioner category as rising incomes expand the addressable market for connected cooling products.

Vietnamese consumers, particularly in urban centres such as Ho Chi Minh City and Hanoi, are increasingly expecting air conditioners to offer smartphone app connectivity, voice assistant compatibility, and AI-driven operating modes as standard features. The shift from traditional fixed-speed units to smart inverter models is accelerating as product prices fall and digital literacy rises. In 2025, Daikin Vietnam launched smart air conditioners featuring the D-Mobile application with Wi-Fi integration and humidity optimisation, and Samsung Vina simultaneously introduced its smart system AC lineup for the domestic market, signalling that Vietnam Air Conditioner Market growth is being actively driven by technology-led product differentiation.

Vietnam's climate profile is shifting in ways that fundamentally expand the addressable air conditioner market. National meteorological data confirms that 2024 brought 19 significant heatwave events, droughts, and extreme weather episodes across the country, with temperatures in Hanoi regularly reaching 38 to 40 degrees Celsius. Official forecasts from the National Centre for Hydro-Meteorological Forecasting indicate that 2025 will bring further severe heatwaves. For both residential households and commercial facility operators, reliable air conditioning has transitioned from discretionary to essential, supporting sustained volume growth even in the face of fluctuating economic conditions.

The Vietnamese government's 2025 implementation of mandatory energy-efficiency standards for non-ducted air conditioners is fundamentally altering product development priorities and brand positioning across the market. Manufacturers that have invested in inverter compressor technology and variable refrigerant flow systems are commercially advantaged under the new regime, while producers of lower-efficiency fixed-speed units face an accelerating phase-out. The regulation aligns Vietnam with regional peers Thailand and Indonesia in deploying performance standards to drive both sustainability and modernisation of the residential cooling stock. International brands including Daikin and Mitsubishi Electric, which already lead in inverter technology, are well positioned to capture the resulting demand shift.

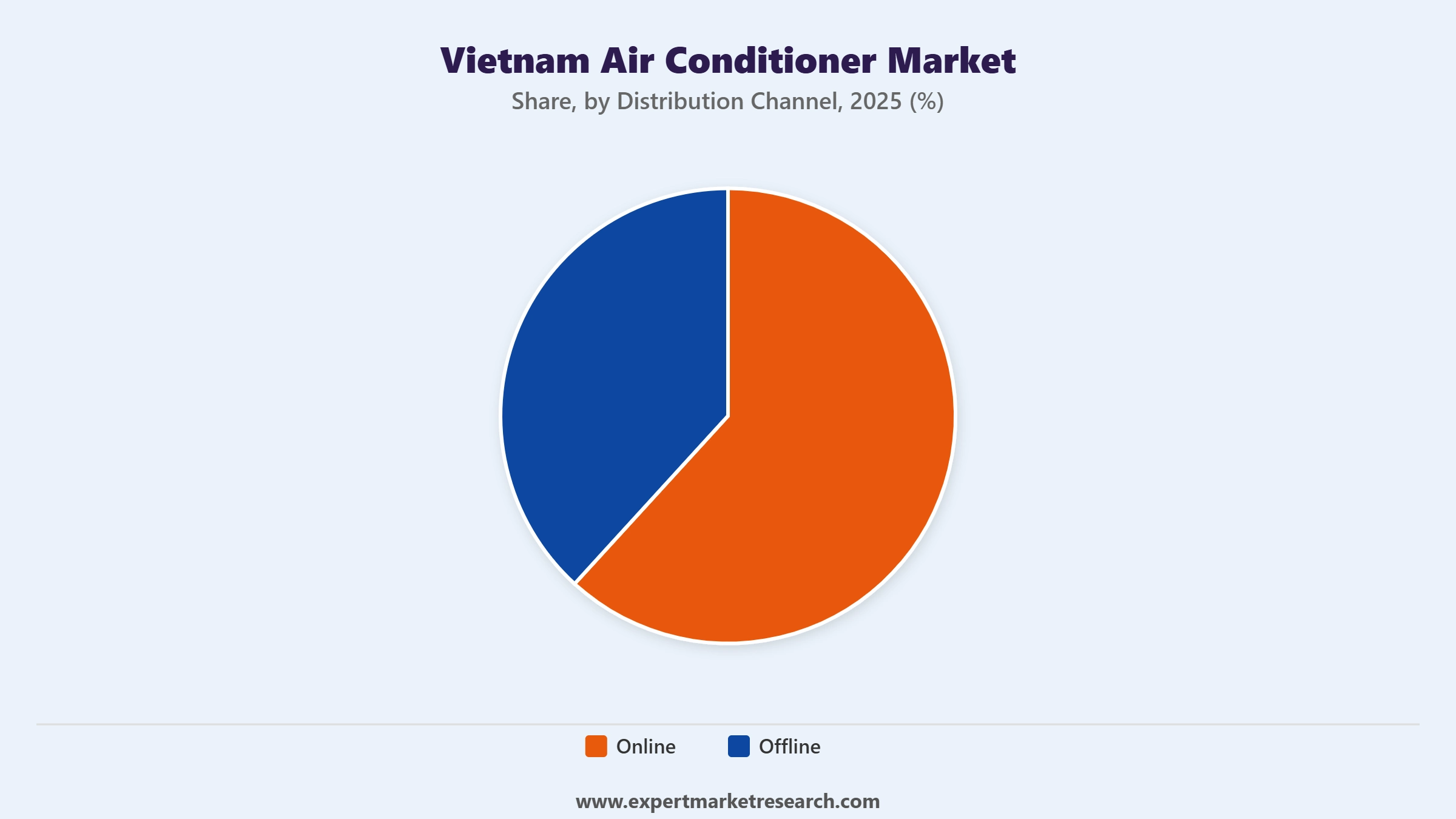

E-commerce penetration in Vietnam's consumer electronics category has been accelerating, and air conditioners are increasingly purchased through digital platforms including Shopee, Lazada, and Tiki, particularly among younger urban buyers comfortable with online transactions. Online distribution is growing at a projected 7.8% CAGR through 2035, considerably faster than overall market growth. Multi-brand stores retain their position as the dominant channel with approximately 55% market share as of 2025, but the online channel's share is expanding rapidly. Brands with strong digital marketing capabilities and fast logistics partnerships are capturing disproportionate volume growth as the online channel's reach extends beyond major urban centres to secondary cities across Vietnam.

The Expert Market Research's report titled "Vietnam Air Conditioner Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

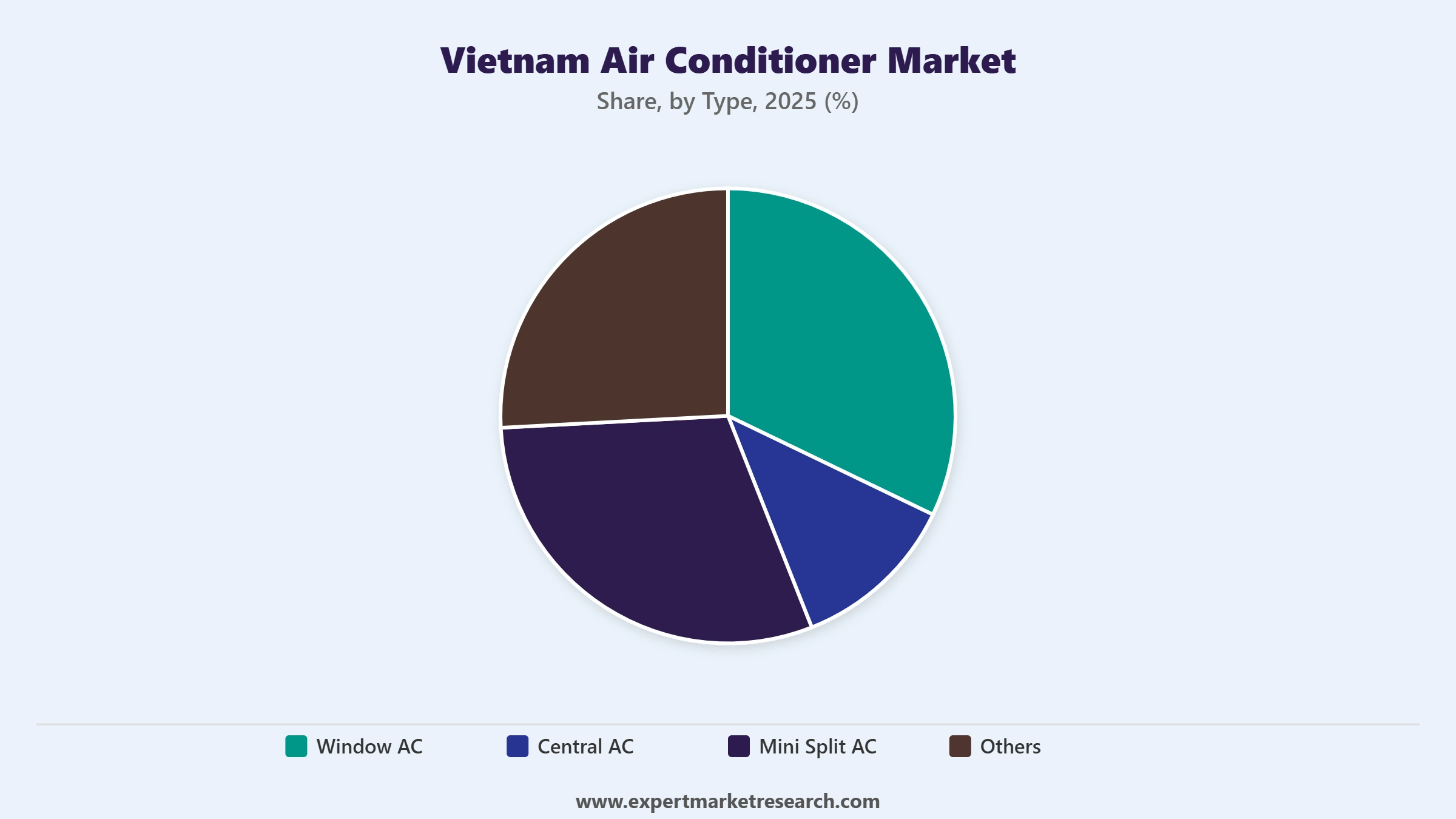

Market Breakup by Type

Key Insight: Mini split air conditioners dominate the Vietnam market by volume, ideal for urban apartments due to their energy efficiency, quiet operation, and minimal structural installation requirements. Window ACs retain relevance in smaller homes and budget-conscious households in less urbanised areas. Central AC is the fastest-growing type at a projected CAGR of 7.2% over the forecast period, driven by large commercial projects including office towers, hotels, and shopping complexes in Ho Chi Minh City and Hanoi. Key players Daikin, Panasonic, and LG have structured Vietnam-specific product ranges around mini split systems at various price tiers to capture the dominant residential demand, while Mitsubishi Electric and Toshiba compete strongly in the commercial central and VRF segments.

Market Breakup by Size

Key Insight: The 12k to 36K BTU range dominates market demand, closely matching the space-cooling requirements of Vietnam's most common residential apartment formats and small to medium commercial spaces. This segment captures the broadest category of purchasers and is the primary battleground for brands competing across the mass residential and SME commercial market. Less than 12K BTU units address compact urban studio apartments and are growing as micro-living formats expand in Ho Chi Minh City and Hanoi. The 36K to 60K BTU and 60K+ BTU categories serve hotel, healthcare, and data centre applications, growing in tandem with Vietnam's accelerating commercial real estate and digital infrastructure investment.

Market Breakup by End Use

Key Insight: The residential segment drives the majority of volume in the Vietnam air conditioner market, sustained by urbanisation, rising household incomes, and the country's tropical climate making cooling a daily necessity. The National Centre for Hydro-Meteorological Forecasting has flagged continued intensification of heatwaves, reinforcing household investment in cooling. The commercial segment, while smaller in unit volume, contributes higher average transaction values and is growing at a faster rate, driven by office construction for the technology and services sectors, hotel and resort development aligned with tourism recovery, and healthcare facility expansion. Brands targeting the commercial end use, including Mitsubishi Electric, Carrier, and Daikin, are benefiting from the government's infrastructure and foreign direct investment-driven construction pipeline.

Market Breakup by Distribution Channel

Key Insight: Offline channels, particularly multi-brand electronics stores, remain the dominant distribution route for air conditioners in Vietnam, commanding approximately 55% of market volume in 2025, according to available industry data. Consumers buying high-value cooling products continue to value in-store demonstration, installation service bundling, and credit financing options primarily available through physical retailers. However, online channels are the fastest-growing segment at a projected 7.8% CAGR through 2035. Platforms including Shopee, Lazada, and brand-owned digital storefronts are expanding brand reach into secondary cities and semi-urban areas, and offering competitive pricing that appeals to younger, digitally native consumers. Brands investing in direct-to-consumer digital infrastructure, such as Samsung and Xiaomi, are well-positioned to capitalise on this channel shift.

Market Breakup By Region

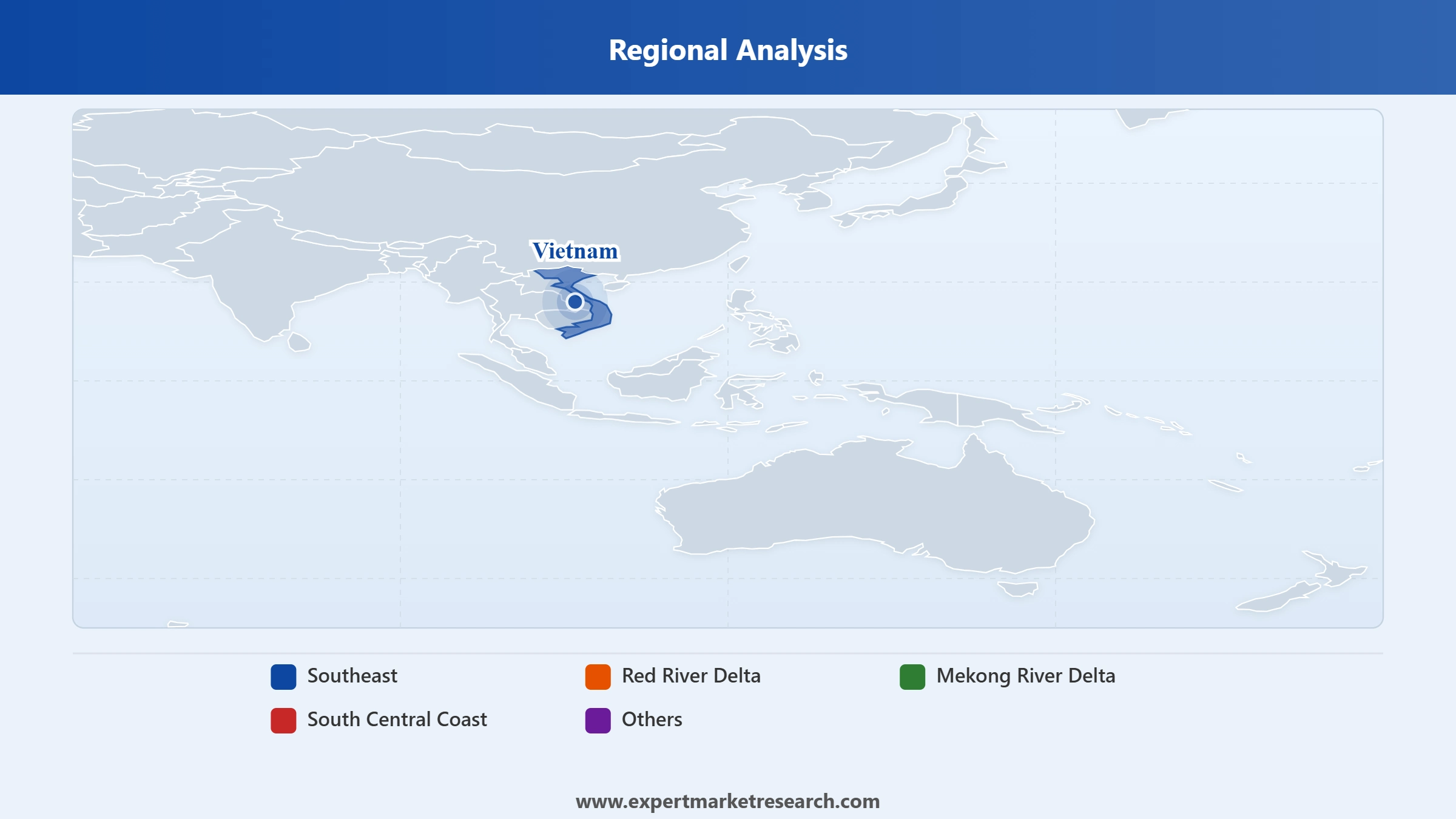

Key Insight: The Southeast region, anchored by Ho Chi Minh City, holds the largest share of Vietnam's air conditioner market, driven by its concentrated urban population, high-density residential construction, and the country's largest concentration of commercial office, retail, and hospitality infrastructure. The Red River Delta, encompassing Hanoi and surrounding provinces, is the second-largest regional market and is growing at a CAGR of 7.6% over the forecast period, supported by accelerating commercial construction and new urban residential developments attracting young professionals. The Mekong River Delta is growing at 6.9% CAGR as urbanisation and agricultural infrastructure investment drive improved living standards. The South Central Coast benefits from tourism-linked hotel and resort development generating commercial cooling demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Mini Split AC category holds the largest market share by type in Vietnam, a position reinforced by its compatibility with the country's dominant apartment and condominium housing formats and its strong energy-efficiency credentials. Urban Vietnamese consumers increasingly equate mini split systems with modern, aspirational home living, and most new residential construction projects in Ho Chi Minh City and Hanoi are designed to accommodate split AC configurations as a standard feature. Companies including Daikin, LG, and Panasonic have built the core of their Vietnam residential business on this category, with their respective inverter mini split portfolios spanning entry-level to premium price points. The 12k to 36K BTU size range captures the broadest share by unit volume, matching the typical cooling requirements of Vietnamese homes and small commercial spaces.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the distribution channel segmentation, Offline channels hold the dominant share, reflecting the importance of in-store product demonstration, post-sale installation services, and credit financing in the air conditioner purchase journey. Multi-brand retailers remain the primary point of contact for the majority of Vietnamese buyers, offering the chance to compare models across brands before committing to a purchase that represents a significant household investment. The Online segment, while a smaller current share, is the fastest-growing distribution route and is expected to gain ground steadily as e-commerce infrastructure matures and brands invest in digital after-sales service solutions. In the end-use segmentation, Residential continues to dominate by unit volume, while the Commercial segment commands higher per-unit value and is growing at a faster rate driven by Vietnam's expanding service, hospitality, and technology sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Southeast region, centred on Ho Chi Minh City and the greater Ho Chi Minh City metropolitan area, is Vietnam's dominant air conditioner market. The economic powerhouse of southern Vietnam, the region hosts the country's densest concentration of high-rise residential projects, commercial office towers, retail centres, and hospitality facilities, all generating sustained AC procurement demand. Ho Chi Minh City's hot, humid climate with temperatures consistently exceeding 30 degrees Celsius year-round makes air conditioning a non-negotiable household and workplace investment. Vietnam's ongoing infrastructure programme is delivering additional commercial real estate capacity in the broader Southeast region, creating sustained incremental demand. The region accounted for the largest share of the market in 2024, and the Southeast's CAGR of 7.6% during the forecast period underscores its continued growth leadership.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Red River Delta region, encompassing Hanoi and surrounding industrial and residential zones, is Vietnam's second most important air conditioner market and is expanding at a CAGR of 7.6%, matching the Southeast in growth momentum. Hanoi's recent severe heatwaves, with temperatures regularly reaching 38 to 40 degrees Celsius, have elevated air conditioning from a comfort product to a public health necessity for urban residents. The national government's construction of new urban districts around Hanoi, including Smart City developments such as Dong Anh Smart City, is bringing large volumes of new residential and commercial floor space into the market. The city's growing business process outsourcing, technology, and financial services sectors are also sustaining office-based commercial cooling demand. International brands including Daikin, Panasonic, and LG compete intensely in both the residential and commercial segments across the Red River Delta.

The Vietnam Air Conditioner Market is highly competitive, with Japanese brands historically holding premium leadership positions, Korean brands competing strongly on technology and brand recognition, and an expanding cohort of Chinese manufacturers aggressively targeting the mid-range and value segments. Competition is sharpening as new entrants from China bring well-engineered products at disruptive price points, compelling established players to invest more heavily in smart features, after-sales service quality, and brand differentiation.

The market also features domestic Vietnamese brands including Casper Electric and Nagakawa Group, which have built meaningful consumer loyalty through locally adapted products, competitive pricing, and nationwide service networks. Government energy-efficiency regulations taking effect in 2025 have accelerated the transition toward inverter technology across all competitive tiers, raising both the product development requirements and the minimum quality floor for all market participants.

Founded in 1924 and headquartered in Osaka, Japan, Daikin is Vietnam's leading premium air conditioner brand by brand equity and sales volume. The company's extensive Vietnam-specific product portfolio spans residential mini split, ducted, and commercial VRF systems. Daikin Vietnam's 2025 launch of smart AC units with D-Mobile app connectivity and humidity optimisation reflects the company's continued investment in maintaining its premium market position amid growing competition from Chinese brands. Daikin's well-established dealer and service network across Vietnam's major cities underpins its distribution strength.

Founded in 1918 and headquartered in Osaka, Japan, Panasonic is a long-established and widely trusted air conditioning brand in Vietnam. Its inverter-based residential and commercial AC product lines are distributed through an extensive network of branded dealers and multi-brand retailers nationwide. Panasonic's nanoe air purification technology incorporated into its AC range has been well-received by health-conscious Vietnamese consumers in post-pandemic years, and its competitive pricing across the mid-to-premium segment maintains strong volume performance in both residential and light commercial applications.

Founded in 1947 and headquartered in Seoul, South Korea, LG is among the most recognised air conditioner brands in Vietnam's residential market. The company's Dual Inverter Compressor technology and ThinQ smart home connectivity have resonated with urban Vietnamese buyers seeking energy-efficient, app-enabled cooling solutions. LG's strong presence through major electronics retail chains and its growing e-commerce channel participation make it one of the most accessible premium brands in both online and offline purchase settings across major Vietnamese cities.

Founded in 1921 and headquartered in Tokyo, Japan, Mitsubishi Electric holds a strong position in Vietnam's commercial and premium residential air conditioning segments. Its VRF and multi-split system capabilities make it a preferred brand for hotel groups, office developers, and large commercial projects where system-level performance and energy management are priorities. Mitsubishi Electric's technical reputation and specialist installer network support its positioning in higher-complexity commercial cooling applications, where price sensitivity is lower and performance requirements are more demanding.

Other key players in the market are Toshiba Corporation, Samsung Electronics Co. Ltd., Sharp Corporation, Casper Electric, Nagakawa Group, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest intelligence on the Vietnam Air Conditioner Market 2026 with our in-depth research report. Stay ahead of the competition with insights covering the fastest-growing product types, the impact of new energy-efficiency regulations, regional demand dynamics, and the competitive moves reshaping the market. Whether you are a manufacturer assessing Vietnam market entry, a distributor expanding your cooling product portfolio, or an investor evaluating the HVAC sector in Southeast Asia, this report gives you the data and insight to act with confidence. Download your free sample today and explore the key opportunities in Vietnam's thriving air conditioning industry.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Vietnam air conditioner market reached an approximate value of USD 73.89 Million.

The market is projected to grow at a CAGR of 6.70% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 141.33 Million by 2035.

The major drivers of the market are rapid urbanization and rising disposable incomes, and the growing middle-class population.

The key trends of the market include the integration of smart technology, health features, energy-efficiency with solar power, and increased sales through online platforms.

The major regions in the market are Southeast, Red River Delta, Mekong River Delta, South Central Coast, and others.

The various types considered in the market report are window AC, central AC, mini split AC, and others.

The various end uses considered in the market report are commercial and residential.

The distribution channels considered in the Vietnam air conditioner market report are online and offline.

The major players in the market are Daikin Industries Ltd., Panasonic Corporation, LG Corporation, Mitsubishi Electric Corp, Toshiba Corporation, Samsung Electronics Co., Ltd., Sharp Corporation, Casper Electric, and Nagakawa Group, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Size |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.