Explore Our Diverse Range Of Offerings

From detailed reports to experts services offered in 15+

Industry Domains

The Commodity Compass – Weeks 30-31, 2025

The Commodity Compass Newsletter Weeks 30–31, 2025 identifies the prevailing trends and market forces in the global commodity markets.

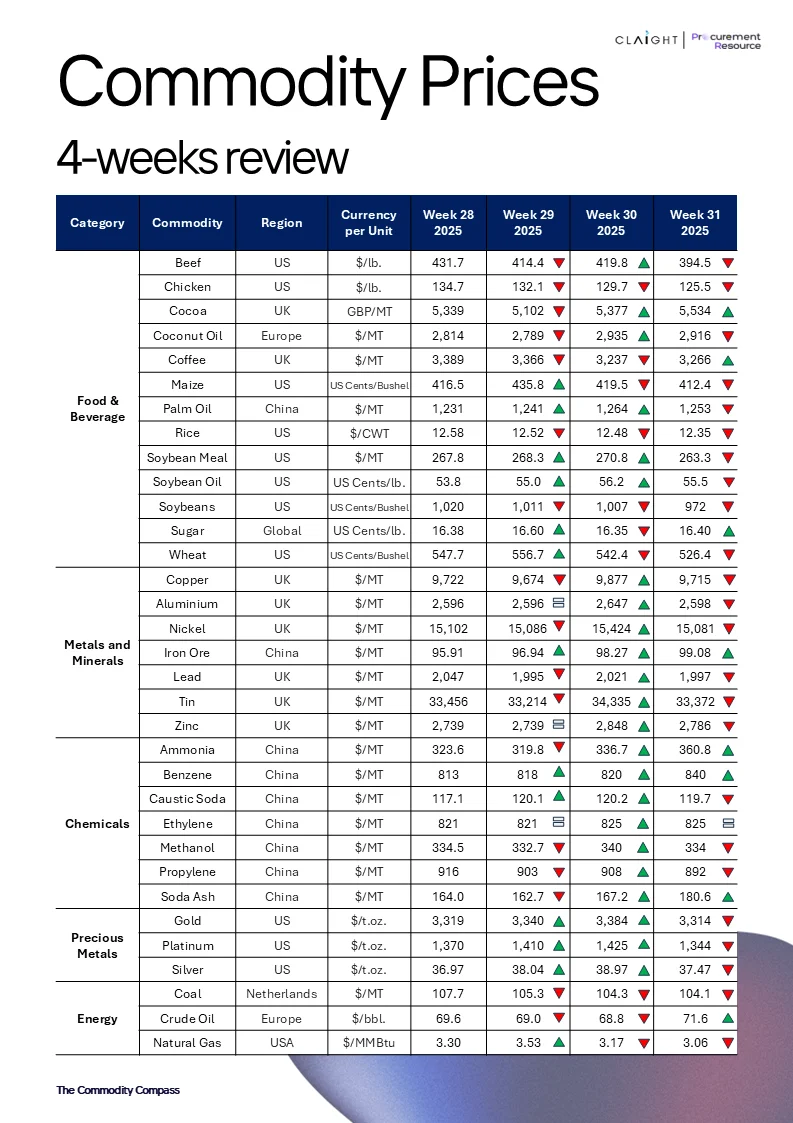

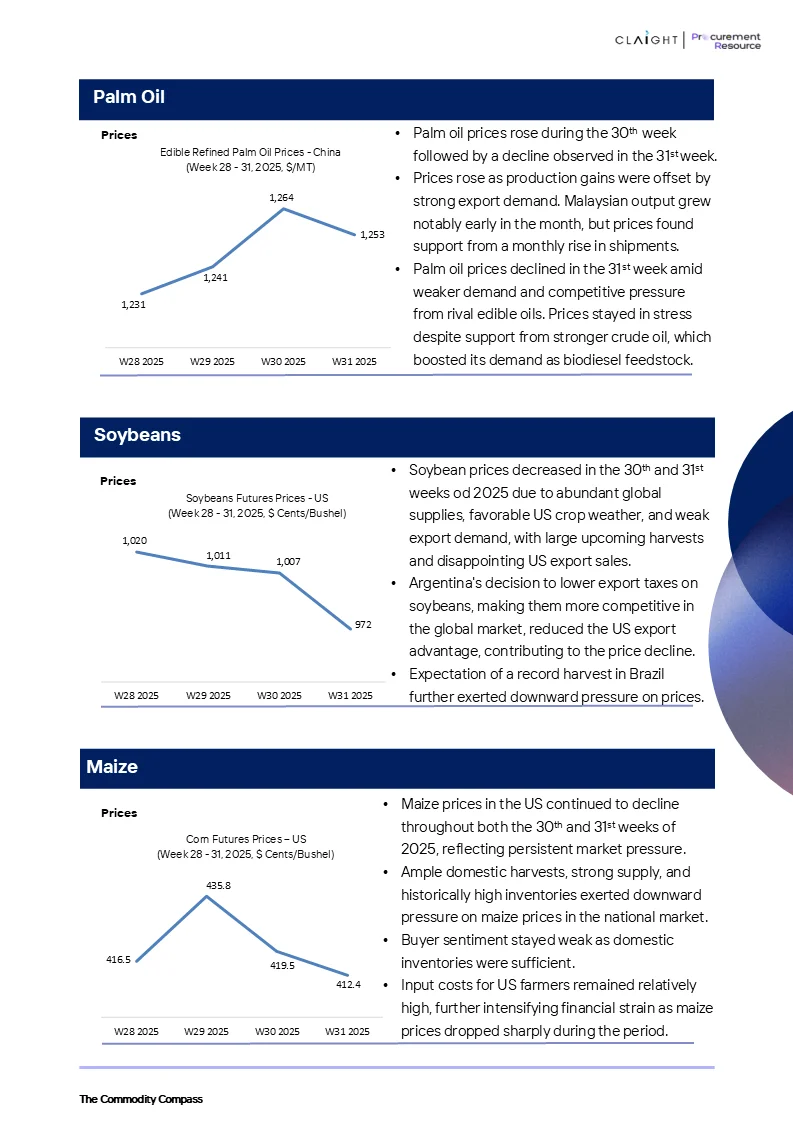

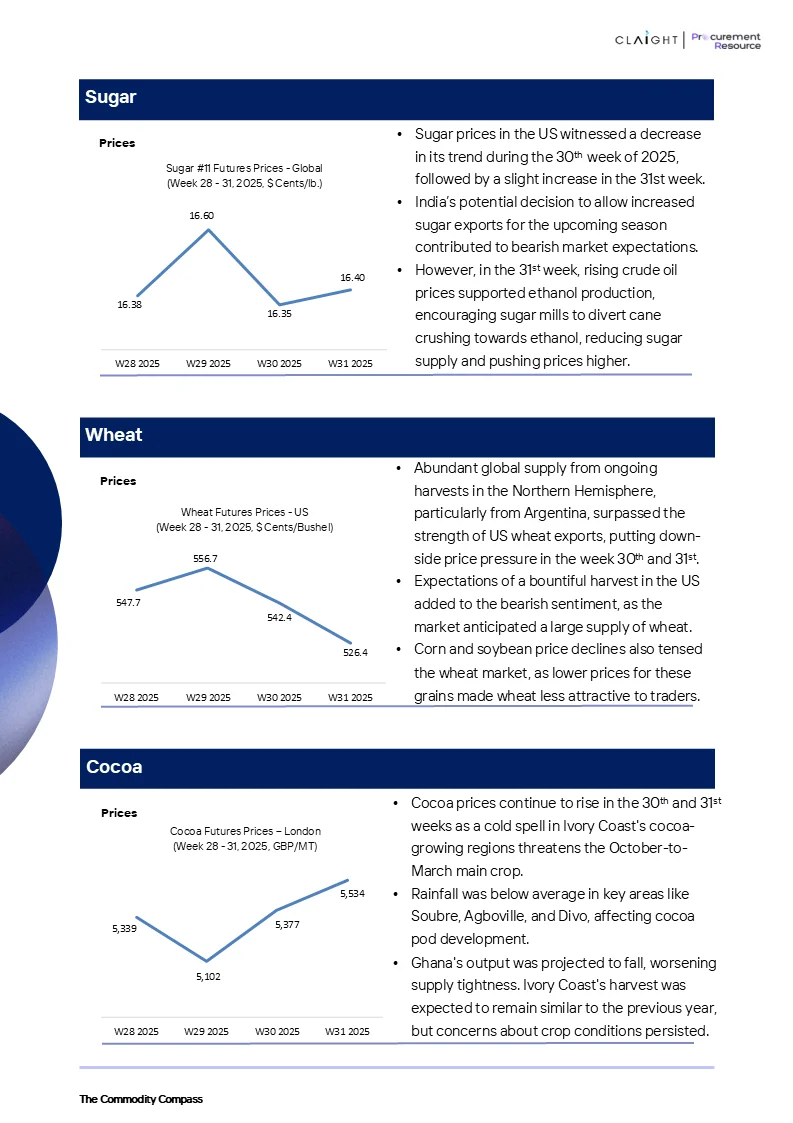

In the food and beverage industry, China edible palm oil prices leaped to $1,264/MT in Week 30 due to increasing global demand for biodiesel and a positive exchange rate. Soybean prices in the United States went on weakening, hitting 1,018 cents/bushel in Week 30 because of concerns of oversupply and ambiguity over biofuels. Corn prices revived to 435.8 cents/bushel in Week 30, supported by better export performance and favorable market sentiment. Sugar prices also saw a rise to 16.35 cents/lb in Week 31, as supported by tighter imports into the United States and lower output from Brazil.

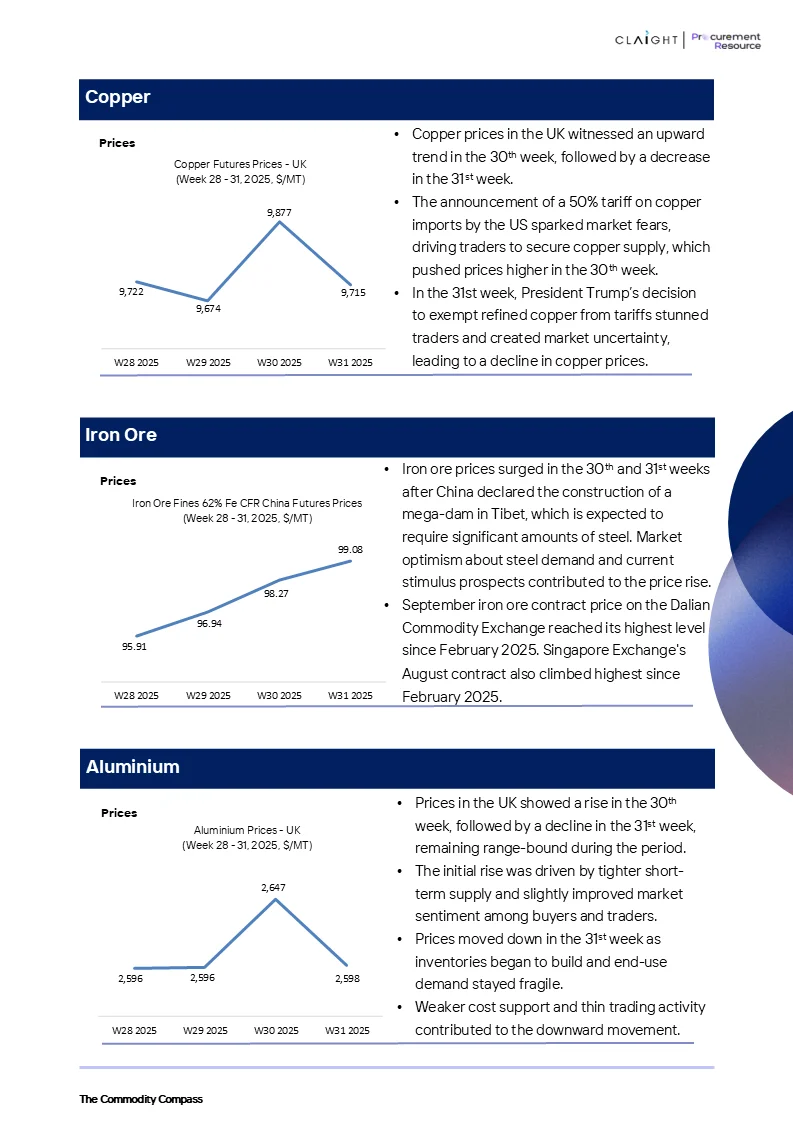

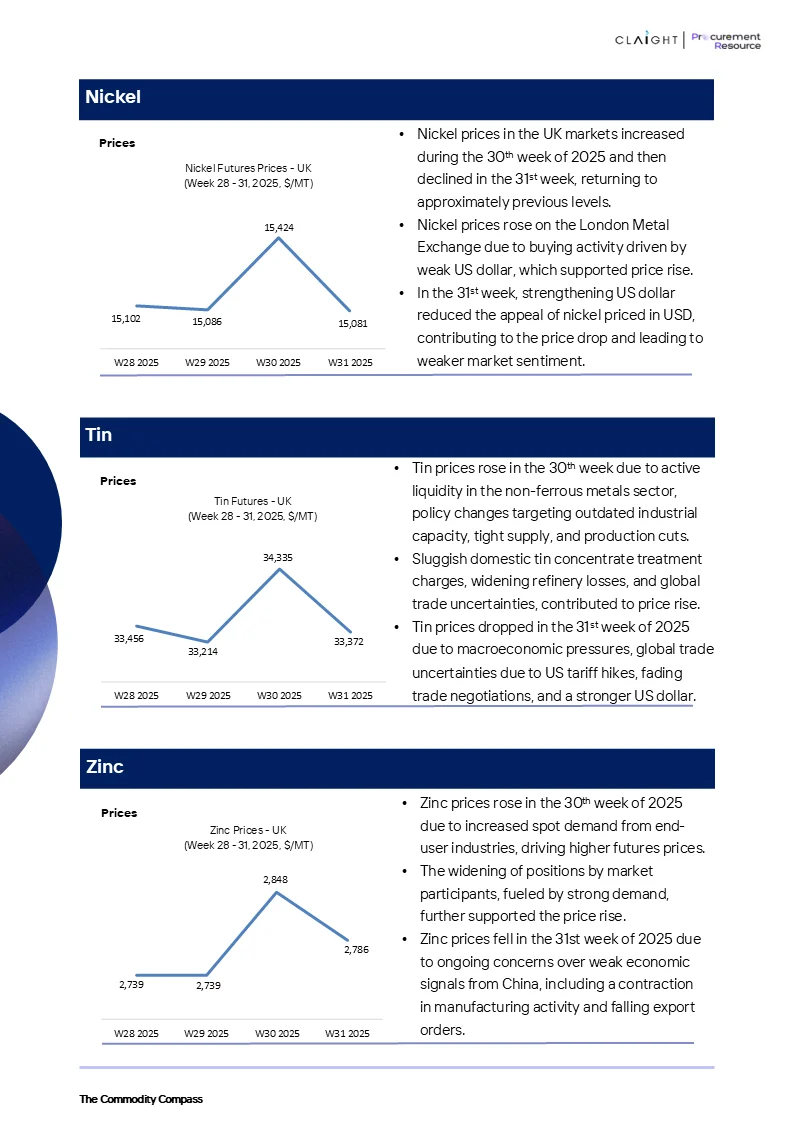

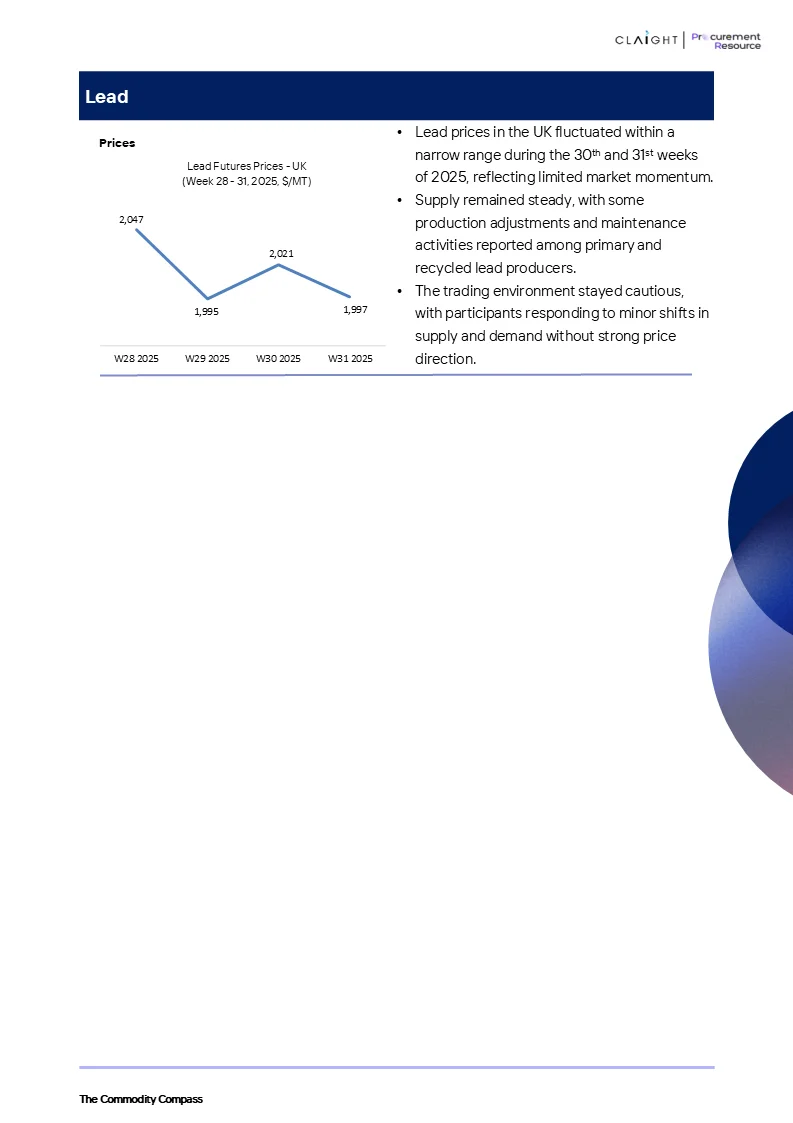

The metals and minerals market had diversified trends. Copper prices fell to $9,659/MT in Week 31 as a result of continued issues with tariffs in the United States and lower investor morale. Nickel fell to $15,013/MT in Week 31, weighed down by excess supply and poor demand for the stainless steel industry. Iron ore went up sharply to $94.1/MT in Week 31, buoyed by strong activity in Chinese steel production as well as policy incentives. Aluminium settled at $2,594/MT after the early volatility due to macroeconomic adjustments.

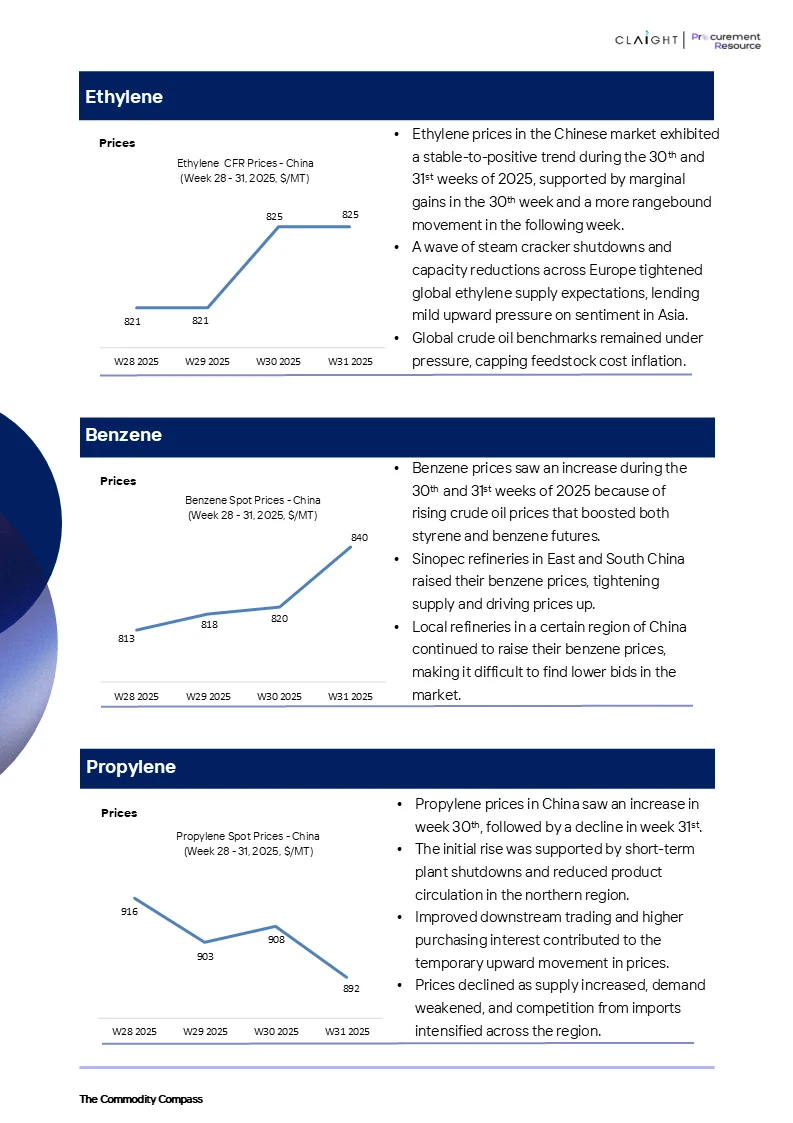

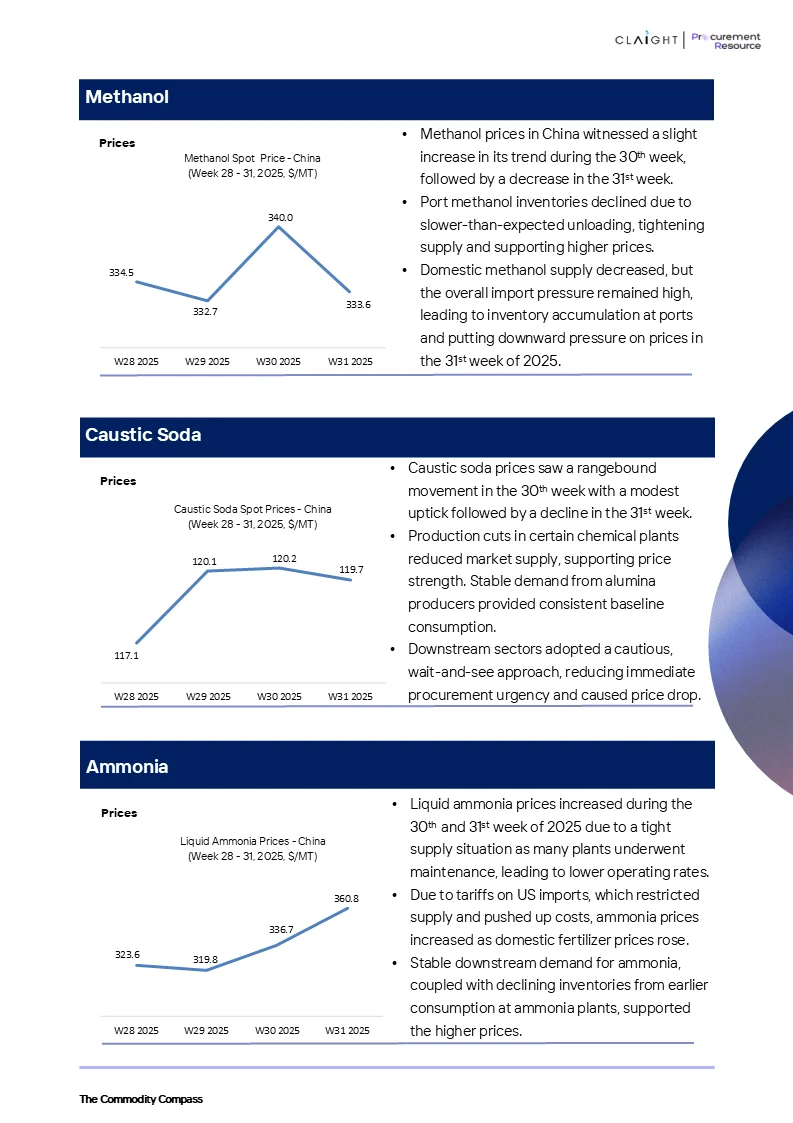

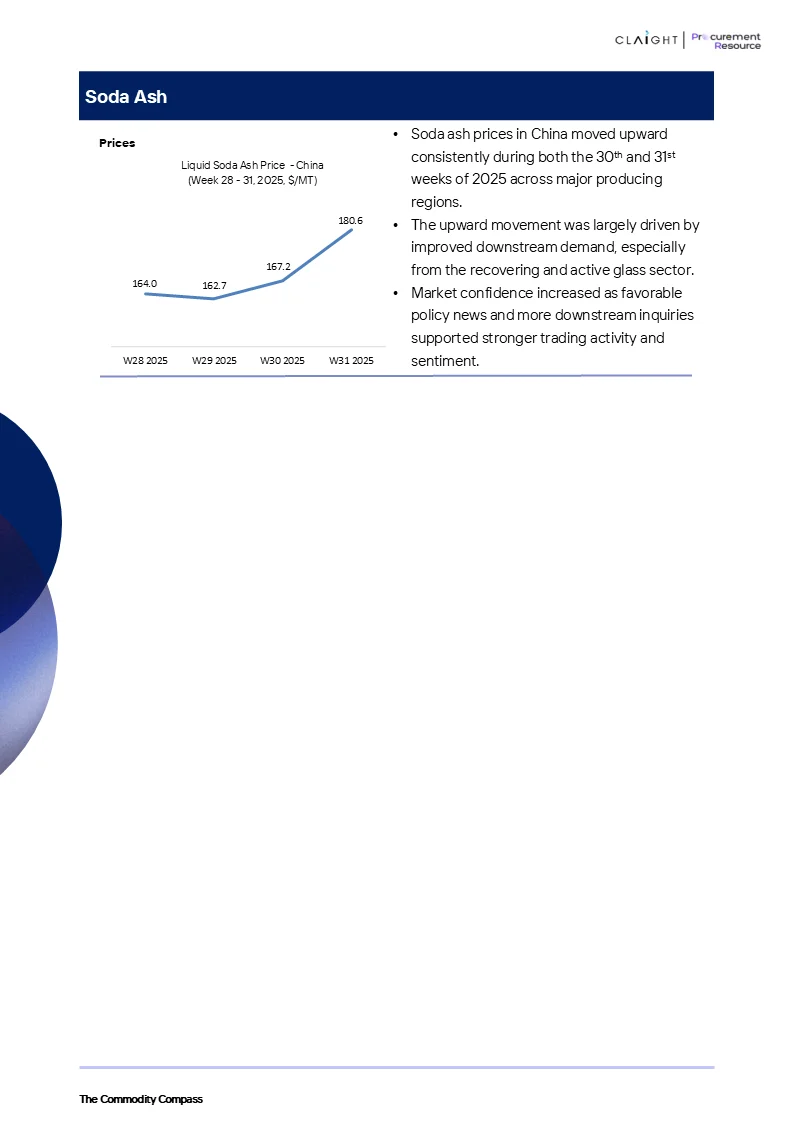

In chemicals, methanol prices settled at $332.7/MT in Week 31, after a supply surplus and increasing stocks in China. Propylene prices plunged to $892/MT in Week 31 due to softer demand and lower feedstock prices. Caustic soda, however, recorded an increase to $120.1/MT in Week 31 due to constrained supply levels and buoyant demand for alumina. Soda ash prices declined to $167.2/MT during Week 31 as increasing stocks and slow downstream consumption pressured the market.

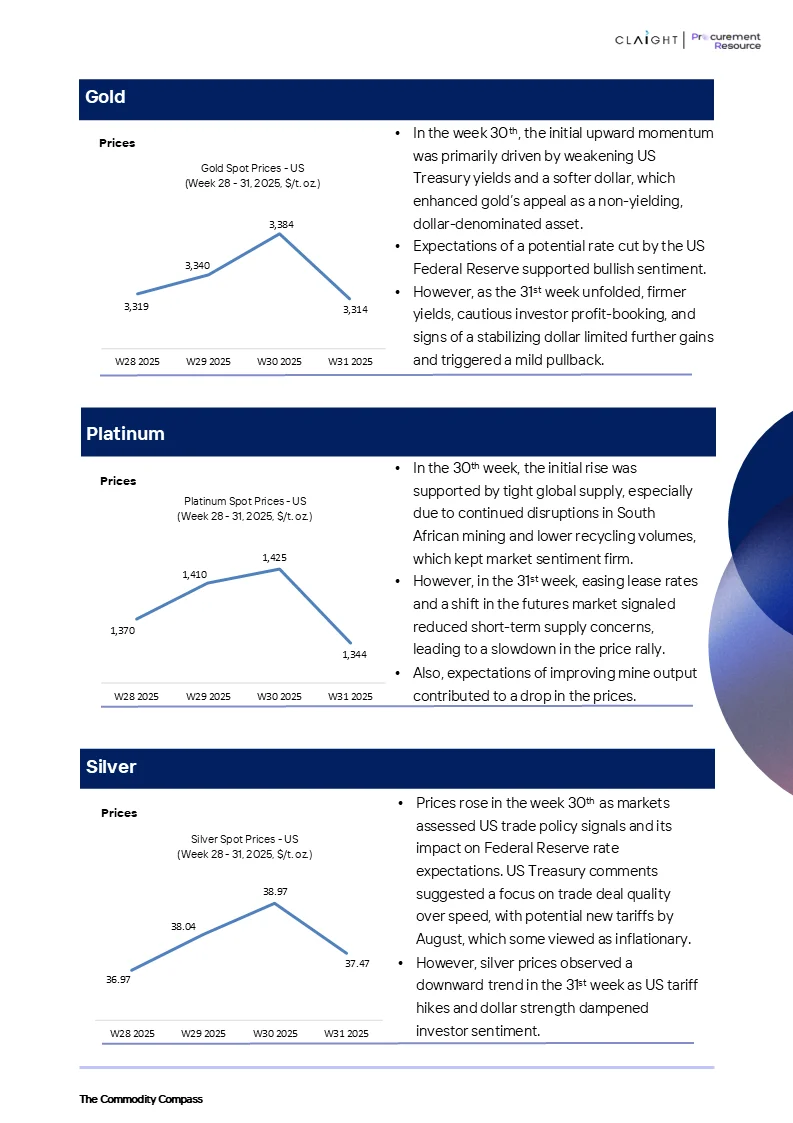

Precious metals had a mixed performance. Prices of gold recovered to $3,384/t.oz. during Week 31 due to safe-haven demand in the face of global uncertainties. Prices of silver climbed to $37.47/t.oz. during Week 31 due to robust industrial demand and mining constraints. Platinum recorded a surge to $1,425/t.oz. during Week 31 due to supply tightness and high warehouse inflows in the United States.

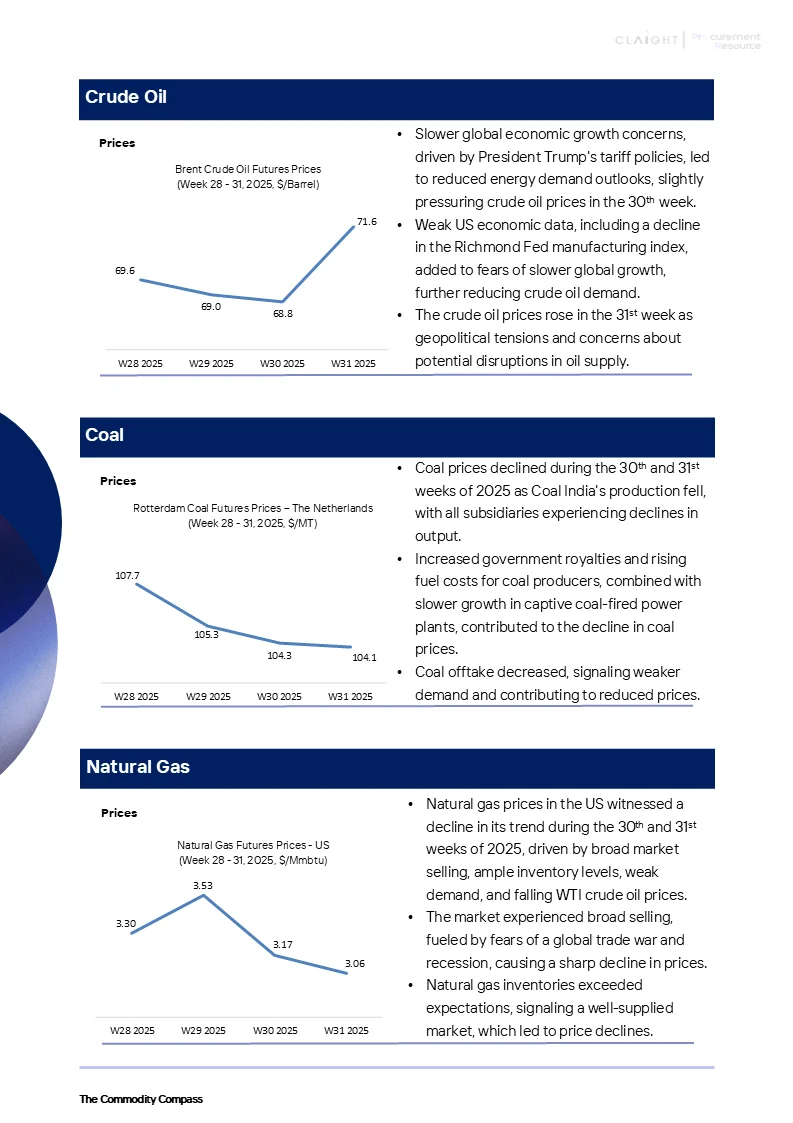

Energy markets remained volatile but mostly range-bound. Brent crude prices stabilized at $68.8/barrel during Week 31 with the help of OPEC+ production cuts and seasonal demand. Coal prices dipped minimally to $104.1/MT at ARA ports in Week 31, driven by decreasing natural gas prices. United States natural gas, in contrast, spiked to $3.06/MMBtu during Week 31 as a result of tightening storage and rising consumption fueled by a heatwave.

- Our Insights Store:

-

Industry Statistics

-

Procurement Insights

-

Consumer Insights

Our Offices

Australia

63 Fiona Drive, Tamworth, NSW

+61-448-061-727

India

C130 Sector 2 Noida, Uttar Pradesh 201301

+91-723-689-1189

Philippines

40th Floor, PBCom Tower, 6795 Ayala Avenue Cor V.A Rufino St. Makati City,1226.

+63-287-899-028, +63-967-048-3306

United Kingdom

6 Gardner Place, Becketts Close, Feltham TW14 0BX, Greater London

+44-753-713-2163

United States

30 North Gould Street, Sheridan, WY 82801

+1-415-325-5166

Vietnam

193/26/4 St.no.6, Ward Binh Hung Hoa, Binh Tan District, Ho Chi Minh City

+84-865-399-124

United States (Head Office)

30 North Gould Street, Sheridan, WY 82801

+1-415-325-5166

Australia

63 Fiona Drive, Tamworth, NSW

+61-448-061-727

India

C130 Sector 2 Noida, Uttar Pradesh 201301

+91-723-689-1189

Philippines

40th Floor, PBCom Tower, 6795 Ayala Avenue Cor V.A Rufino St. Makati City, 1226.

+63-287-899-028, +63-967-048-3306

United Kingdom

6 Gardner Place, Becketts Close, Feltham TW14 0BX, Greater London

+44-753-713-2163

Vietnam

193/26/4 St.no.6, Ward Binh Hung Hoa, Binh Tan District, Ho Chi Minh City

+84-865-399-124