Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

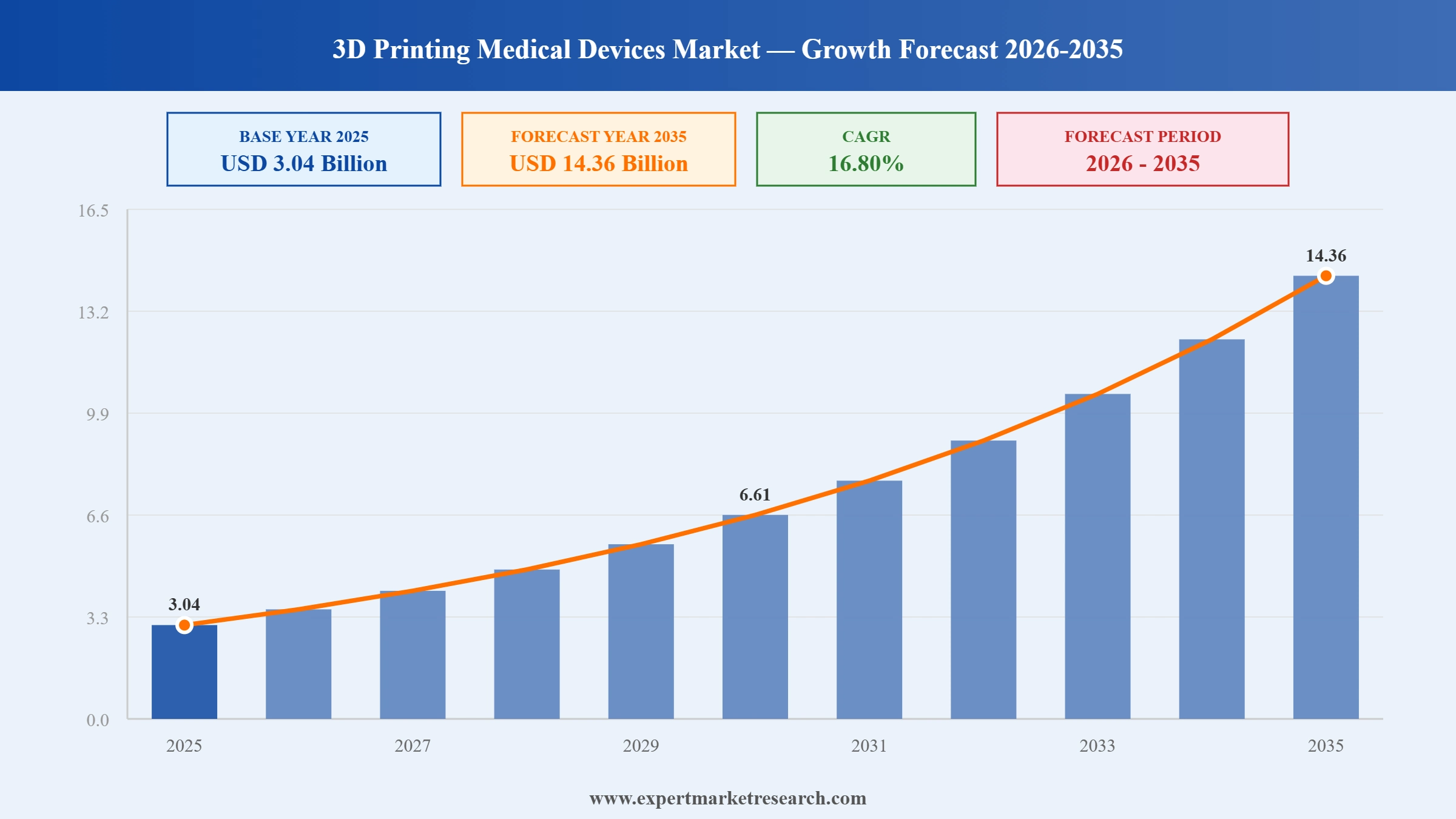

The 3D printing medical devices market was valued at USD 3.04 Billion in 2025. It is poised to grow at a CAGR of 16.80% during the forecast period of 2026-2035, and reach USD 14.36 Billion by 2035. The market growth is driven by the accelerating adoption of additive manufacturing for patient-specific implants and prosthetics, increasing demand for customized surgical instruments, and the expanding use of biocompatible materials in clinical-grade device fabrication.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

3D printing medical devices encompasses additive manufacturing-based production of medical-grade components such as implants, prosthetics, surgical guides, anatomical models, and customized instrumentation designed to improve clinical precision, patient outcomes, and procedural efficiency. The market is shaped by rapid advances in multi-material printing, high-resolution stereolithography, selective laser sintering, and electron beam melting technologies, enabling the production of complex geometries that are difficult to achieve through conventional manufacturing. The market was valued at USD 3.04 Billion in 2025, supported by increasing clinical adoption of patient-specific solutions, rising demand for minimally invasive surgical devices, and strong investment activity across medical technology and regenerative medicine domains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

3D Printing Medical Devices Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

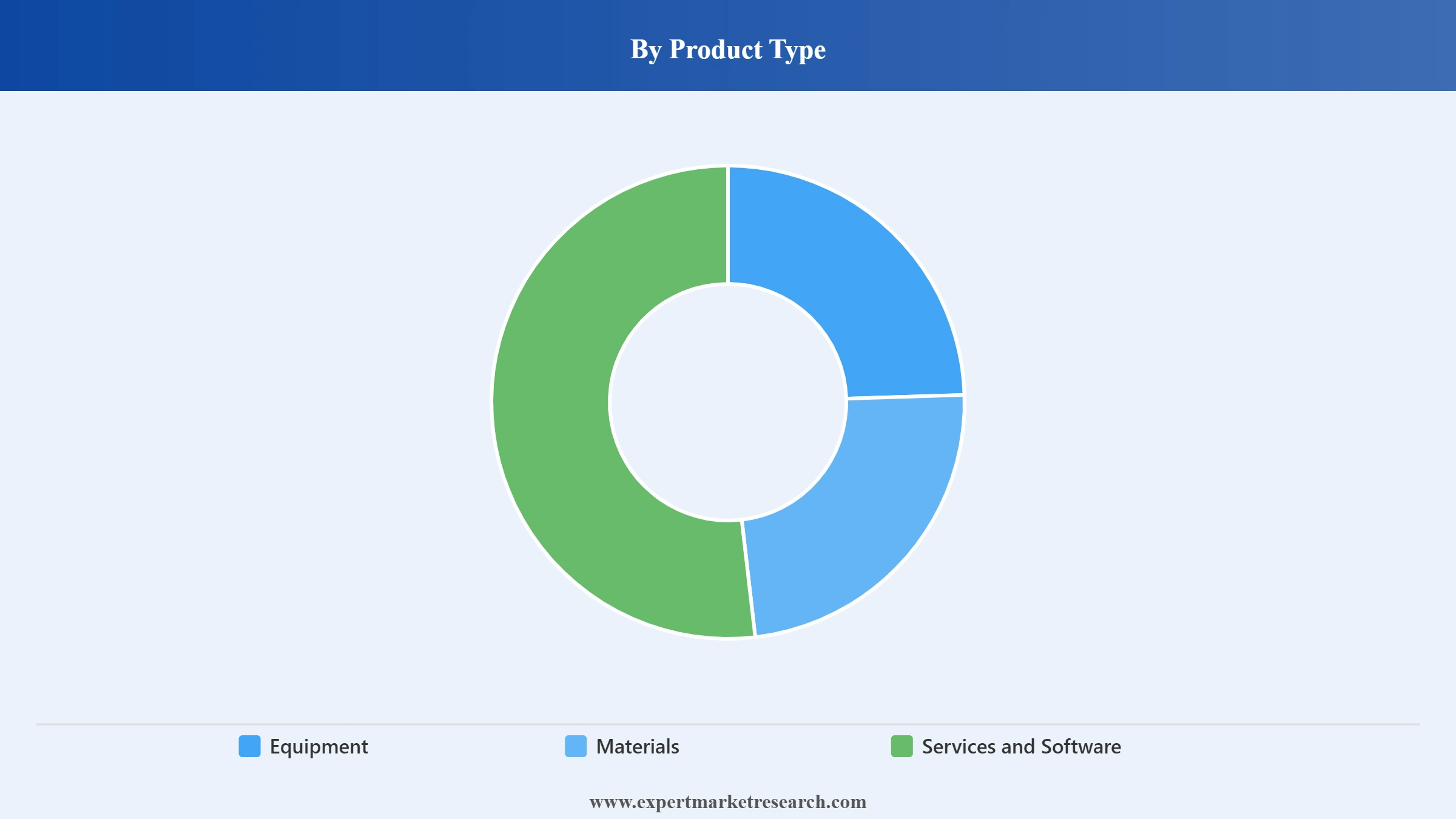

Market Breakup by Product Type

Equipment includes 3D printers, bioprinters, and supporting hardware used for the fabrication of medical-grade devices. Materials cover metal powders, polymers, ceramics, and bio-compatible formulations that directly determine mechanical and biological performance. Services and software include design tools, imaging-to-print workflows, simulation platforms, and workflow management systems that enable customization and scalable production across clinical and industrial settings.

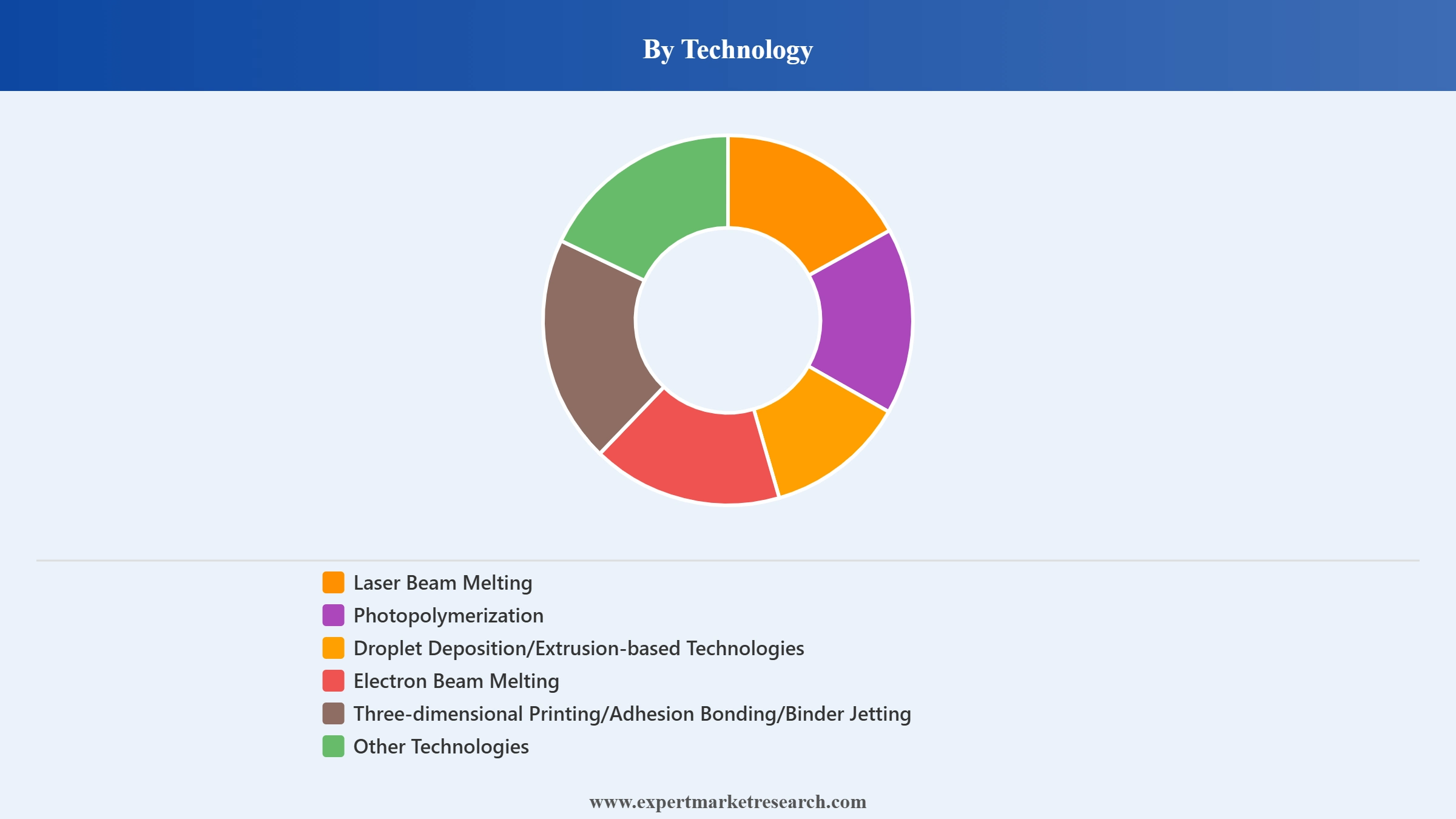

Market Breakup by Technology

Technology segmentation is defined by energy source and material processing methods. Laser beam melting and electron beam melting are primarily used for metal implants requiring high strength and structural integrity. Photopolymerization dominates high-precision applications such as dental devices and surgical guides. Extrusion and droplet-based systems are widely used in bioprinting and tissue engineering due to compatibility with bioinks. Binder jetting and related methods provide scalable, cost-efficient production for complex geometries.

Market Breakup by Applications

Applications are driven by demand for patient-specific and precision medicine solutions. Surgical guides and instruments are widely adopted due to ease of regulatory approval and integration with imaging workflows. Standard and custom implants represent a major segment, particularly in orthopedics implants and dental care. Tissue-engineered products form a high-growth area linked to regenerative medicine. Hearing aids and wearables reflect mature customization use cases enabled by additive manufacturing.

Market Breakup by End User

End-user adoption varies by function. Hospitals and surgical centers use point-of-care printing for patient-specific devices. Dental and orthopedic clinics drive high-volume demand for customized prosthetics. Academic institutions focus on research and material innovation. Pharma and medical device companies lead commercialization and scaling, while clinical research organizations support validation and regulatory compliance studies.

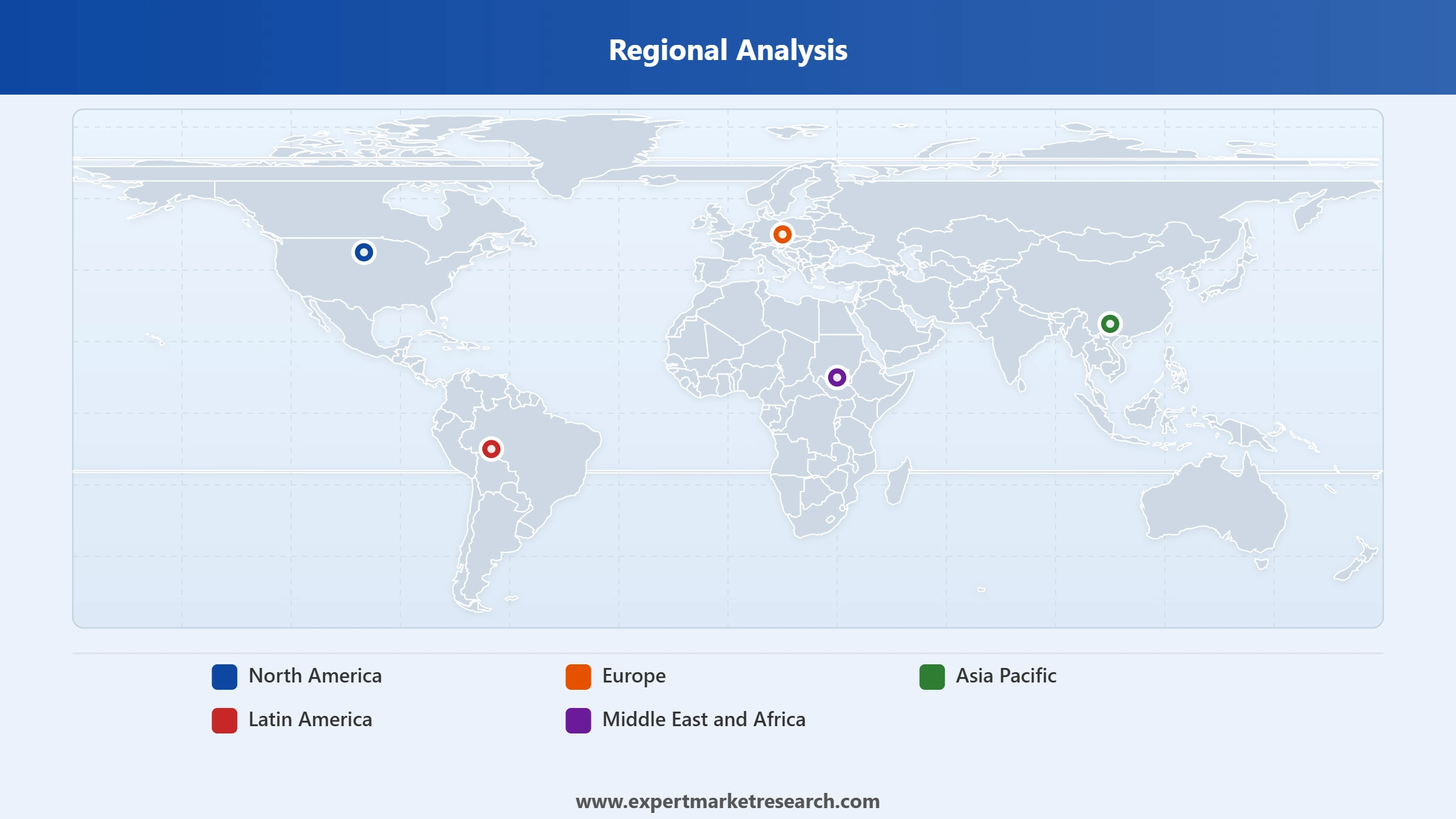

Market Breakup by Region

Regional dynamics reflect differences in infrastructure and regulatory maturity. North America leads in clinical adoption and innovation. Europe demonstrates high adoption supported by advanced healthcare infrastructure and growing use of additive manufacturing in medical device development. Asia Pacific is expanding rapidly due to healthcare investment and manufacturing capacity. Latin America, the Middle East and Africa are emerging markets with selective but growing adoption in advanced healthcare centers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Analysis Type | Factors | Example |

| Market Drivers | Adoption of patient-specific anatomicalmodellingand digital surgical planning boosts precision and surgical efficiency in healthcare. | Stratasys introduced J5 Digital Anatomy printer at RAPID + TCT 2024 improving surgical planning workflows. |

| Market Restraints | High regulatory complexity and lack of global standards increase validation time, cost, and slow commercialization of devices. | Manufacturers face lengthy process validation and quality checks, delaying approval and limiting small player market entry. |

| Market Opportunities | Point-of-care 3D printing enables on-demand production of implants and surgical tools within hospital clinical settings. | Stratasys 2025 notes OEMs adopting additive manufacturing in clinical settings to improve workflow and reduce development timelines. |

The following section outlines the key factors influencing the growth of the market, including major drivers, restraints, and emerging opportunities.

Expanding Adoption of Patient-Specific Anatomical Modeling and Digital Surgical Planning Drives Market Value

The increasing adoption of patient-specific anatomical modeling and digitally enabled surgical planning is driving strong expansion in the market. Advanced additive manufacturing systems are improving the precision and accessibility of customized medical solutions, enabling hospitals and medical device manufacturers to enhance preoperative planning and procedural efficiency. For example, in June 2024, OrthoFeed reported that Stratasys introduced its J5 Digital Anatomy 3D printer at RAPID + TCT 2024 to meet growing demand for accurate anatomical models and improved surgical planning workflows. The report highlighted that these patient-specific models can significantly improve clinical communication and reduce operative time, reinforcing wider clinical adoption of 3D printing technologies in healthcare.

High Regulatory Complexity and Lack of Standardization Challenge the Market Expansion

High regulatory complexity and lack of globally harmonized standards for additive manufacturing of medical devices significantly limit market expansion. Manufacturers must undergo extensive validation of materials, printing processes, and patient-specific device performance, increasing development time and costs. Additive manufacturing devices require rigorous process validation and quality control to ensure safety and effectiveness, which slows commercialization and creates barriers for smaller market participants.

Point-of-Care 3D Printing Integration is Accelerating Clinical Manufacturing Transformation

The integration of point-of-care 3D printing in hospitals is reshaping medical device manufacturing by enabling on-demand production of patient-specific implants, surgical tools, and anatomical models. For example, in October 2025, according to Stratasys, OEMs are increasingly adopting additive manufacturing across the product lifecycle, including clinical settings, to reduce development timelines, improve customization, and enhance workflow efficiency, supporting faster and more scalable healthcare delivery models.

Some of the notable trends in the market include rising FDA-approved patient-specific implants, expansion of biocompatible polymer printing, and growing adoption of hospital-based additive manufacturing systems in orthopedic and cranial reconstruction applications.

Rising FDA Clearance for 3D-Printed Patient-Specific Implants Boosting Clinical Adoption

The increasing regulatory approval of additively manufactured implants is reshaping surgical personalization in the market. The rising use of high-performance polymers such as PEEK is enabling safer cranial and orthopedic reconstruction with improved anatomical precision. For example, in April 2024, 3D Systems announced FDA 510(k) clearance for its VSP PEEK Cranial Implant system, enabling hospital-based production of patient-specific cranial implants. This milestone strengthens clinical confidence and accelerates adoption of additive manufacturing in neurosurgery. Consequently, such advancements are expected to significantly enhance market growth by expanding real-world surgical applications and improving procedural efficiency.

Materials Segment is Likely to Lead the Market by Product Type

The market is segmented by product type into equipment, materials, and services and software. Equipment includes 3D printers and bioprinters used for device fabrication, materials consist of metals, polymers, ceramics, and biocompatible formulations, while services and software cover design platforms, imaging-to-print workflows, and simulation tools. Among these, the materials segment is expected to lead the market due to its continuous consumption across printing processes and direct influence on the mechanical and biological performance of medical devices. The growth is primarily driven by rising demand for biocompatible and high-performance materials used in patient-specific implants, prosthetics, and surgical applications across advanced healthcare systems.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is anticipated to lead the market, supported by early clinical adoption and strong integration of additive manufacturing into healthcare systems. The region benefits from a mature regulatory environment, particularly through the U.S. Food and Drug Administration’s structured guidance on additive manufacturing, which enables clearer approval pathways for patient-specific implants, surgical guides, and dental prosthetics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The key features of the market report comprise patent analysis, funding and investment analysis, and strategic initiatives by the leading players. The major companies in the market are as follows:

Stratasys is a leading additive manufacturing company specializing in medical-grade 3D printing systems and materials. In the market, it supports surgical planning, dental applications, and patient-specific implant production through polymer-based printing platforms and integrated software ecosystems used in hospitals and device manufacturing workflows.

EnvisionTEC focuses on high-precision 3D printing systems for medical and dental applications, particularly resin-based and biocompatible material printing. It is known for enabling dental prosthetics, hearing aids, and customized surgical models through rapid, high-resolution additive manufacturing technologies used in clinical environments.

Philips operates in the 3D printing medical devices market through its imaging, diagnostic, and digital health integration capabilities. It supports patient-specific device design by combining advanced medical imaging with additive manufacturing workflows, enabling pre-surgical planning, anatomical modeling, and precision-guided interventions within hospital and clinical settings.

3D Systems is a major player in the market, offering end-to-end solutions including printers, materials, and healthcare-focused software. Its platforms are widely used for surgical guides, implants, and anatomical models, with strong adoption in orthopedic, dental, and maxillofacial applications across global healthcare institutions.

Other key players in the market are EOS, Renishaw plc., Materialise, 3T Additive Manufacturing Ltd., GENERAL ELECTRIC COMPANY, Carbon, Inc., Prodways Group, SLM Solutions, Organovo Holdings Inc., Anatomics Pty Ltd, and Groupe Gorgé.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

This report is developed through a robust mixed-methods research design combining:

Upto 15% Off

USD

$3299 $2969

$5499 $4949

$6999 $5949

$8199 $6969

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Technology |

|

| Breakup by Applications |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,299

USD 2,969

tax inclusive*

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,199

USD 6,969

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.