Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

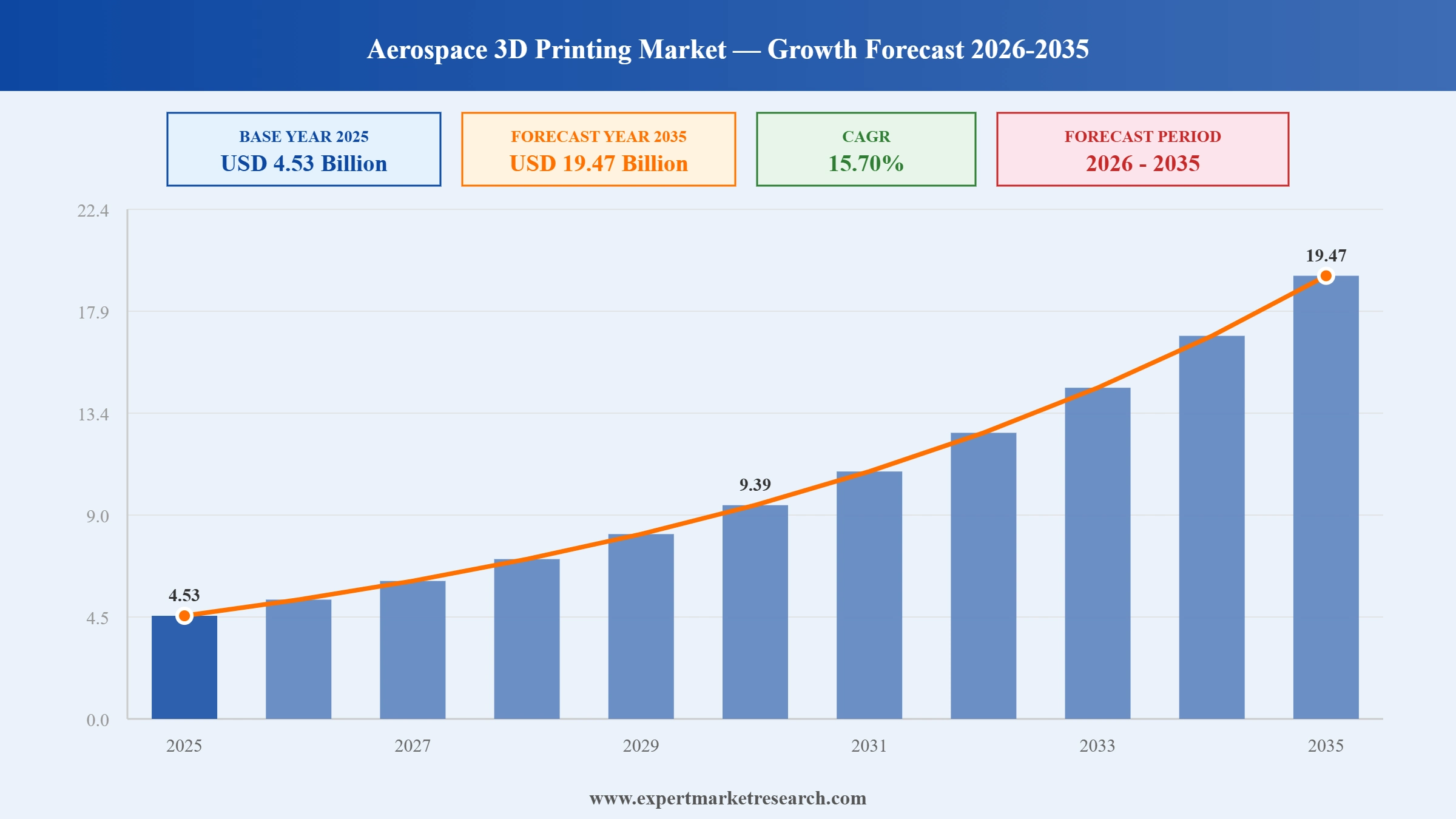

The global aerospace 3D printing market was valued at USD 4.53 Billion in 2025. The market is expected to grow at a CAGR of 15.70% during the forecast period of 2026-2035 to reach a value of USD 19.47 Billion by 2035. This robust growth trajectory is driven by a structural convergence of demand-side and supply-side forces: escalating commercial aircraft production rates, accelerating defense modernization programs across major economies, the rapid expansion of the commercial space economy, and continued advancement in additive manufacturing technologies that have progressively moved 3D printing from prototyping environments into certified serial production lines.

Aerospace 3D printing, also referred to as additive manufacturing for aerospace, encompasses the layer-by-layer fabrication of aircraft and spacecraft components using advanced materials including titanium alloys, aluminum alloys, nickel-based superalloys, and high-performance engineering polymers. This manufacturing approach enables the production of geometrically complex components that are not feasible through conventional subtractive machining or casting processes, while simultaneously delivering measurable improvements in weight reduction, material efficiency, and part consolidation. The technology is deployed across the full aerospace value chain, from original equipment manufacturers (OEMs) and Tier-1 suppliers to maintenance, repair, and overhaul (MRO) operators and defense prime contractors.

The competitive landscape of the aerospace 3D printing market is characterized by the active participation of specialized additive manufacturing technology providers, advanced material suppliers, aerospace OEMs integrating in-house printing capabilities, and a growing tier of software platforms enabling digital design-to-manufacturing workflows. North America represents the largest regional market, anchored by the United States aerospace manufacturing ecosystem, while Asia Pacific is positioned as the fastest-growing region, driven by fleet expansion programs in China and India and increasing defense investment across the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Aerospace 3D printing, or aerospace additive manufacturing, refers to the industrial-scale production of aircraft and spacecraft components using additive processes that build parts layer by layer from digital designs. Unlike traditional subtractive manufacturing methods such as CNC machining or forging, additive manufacturing deposits material only where structurally required, enabling significant reductions in buy-to-fly ratios, particularly for expensive materials such as titanium and Inconel. The output is a finished or near-net-shape component that may require minimal post-processing before integration into an aerospace assembly.

The aerospace 3D printing market encompasses all commercial activities related to the sale of additive manufacturing equipment (printers), raw materials (metal powders, polymers, composites), software platforms (design, simulation, quality management), and services (bureau printing, contract manufacturing, certification support) deployed specifically for aerospace applications. End-use verticals include civil aviation, military aviation, and spacecraft manufacturing. Applications range from rapid prototyping in the early design phase to the serial production of flight-certified functional components including engine parts, structural brackets, ducting, and interior fittings.

The regulatory environment governing aerospace 3D printing is defined by certification frameworks administered by national and supranational aviation authorities including the US Federal Aviation Administration (FAA), the European Union Aviation Safety Agency (EASA), the Civil Aviation Administration of China (CAAC), and the Directorate General of Civil Aviation (DGCA) in India, among others. Certification requirements for additive manufactured parts encompass material qualification, process qualification, non-destructive inspection, and digital traceability, forming a multi-layered compliance framework that shapes investment decisions and technology adoption timelines across the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Weight reduction is a primary engineering objective across the global aerospace industry, directly linked to fuel consumption, emissions compliance, and operating economics. Additive manufacturing enables the production of topology-optimized components that achieve identical or superior structural performance at significantly lower mass compared to conventionally manufactured counterparts. NASA has cited targets for reducing aircraft component weight by approximately 20% over the coming decade, with 3D printing identified as a critical enabling technology to achieve these targets. The adoption of lightweight titanium, aluminum, and high-performance polymer components across engine subassemblies, cabin structures, and fuselage brackets is generating sustained demand for aerospace-grade additive manufacturing capacity. Every kilogram removed from a commercial aircraft saves approximately 0.03% of total fuel burn per flight, creating compelling economics for adoption at scale across fleet sizes running into tens of thousands of aircraft globally.

The digitalization of aerospace manufacturing is accelerating the deployment of 3D printing as a production technology. Digital twin platforms allow engineers to create virtual replicas of additive manufactured components for real-time performance monitoring, predictive maintenance, and iterative design optimization without physical prototyping cycles. Integration of additive manufacturing with model-based systems engineering, cloud-based design platforms, and AI-driven quality inspection tools is compressing the product development timeline from concept to certified part. Aerospace OEMs and Tier-1 suppliers are investing in digital manufacturing infrastructure that links CAD design environments directly to certified print farms, enabling on-demand production of components without the lead times associated with traditional tooling and supplier sourcing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Defense budgets across major economies including the United States, European NATO members, China, India, and the Gulf Cooperation Council states have expanded significantly in recent years, with a substantial portion directed toward next-generation aircraft programs, missile systems, and unmanned aerial vehicle fleets that extensively leverage additive manufacturing. 3D printing enables defense manufacturers to produce low-volume, mission-specific components with reduced lead times, supporting rapid deployment requirements and battlefield maintenance scenarios. The ability to print spare parts on-demand in deployed environments, using portable or field-deployable manufacturing units, is a strategic capability that defense procurement authorities are actively developing and funding, creating durable demand for aerospace-grade additive manufacturing systems and materials.

The commercial space sector, encompassing satellite manufacturing, launch vehicle production, and space station logistics, has emerged as one of the highest-growth application areas for aerospace 3D printing. Rocket engine manufacturers use additive manufacturing to consolidate complex assemblies into single printed components, reducing assembly points, eliminating welds, and cutting production timelines significantly. Spacecraft manufacturers print structural components, fuel tanks, brackets, and thermal management parts that benefit from the design freedom and material efficiency of additive processes. The increasing launch cadence of commercial operators, combined with the growing constellation deployment strategies of satellite communication companies, is generating recurring demand for printed space-grade components manufactured to exacting performance specifications.

Artificial intelligence is transforming the design phase of aerospace additive manufacturing. Generative design algorithms use AI to explore thousands of structural configurations and identify optimized geometries that minimize mass while satisfying all structural, thermal, and aerodynamic constraints. These AI-generated designs frequently produce organic, latticed structures that cannot be manufactured using conventional methods but are ideally suited to additive processes. Machine learning-based process optimization tools are also reducing defect rates in powder bed fusion printing by dynamically adjusting laser parameters in real time based on melt pool monitoring data. The integration of AI across the design-to-manufacture workflow is compressing qualification timelines and improving first-time yield rates, making serial production of certified aerospace components increasingly viable.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The transition from prototyping to certified serial production is the most significant structural change in the aerospace 3D printing market. Historically, additive manufacturing in aerospace was limited to tooling, jigs, fixtures, and prototype components. The market is now witnessing a shift toward flight-certified, production-representative parts manufactured at scale. GE Aerospace has 3D-printed more than 100,000 fuel nozzle tips for the LEAP engine, a landmark demonstration of additive manufacturing in high-volume certified production. Stratasys-qualified Antero polymer materials, EASA-approved metallic spare parts, and FAA-certified titanium structural brackets represent a growing portfolio of certified AM parts entering service across commercial and military platforms. This production-grade maturity is the primary driver of market valuation growth through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Multi-material 3D printing systems that can deposit multiple alloys or material classes within a single build are opening new application possibilities in aerospace component design. Graded material transitions, embedded cooling channels, and integrated electrical conductor paths within structural components are among the capabilities being demonstrated in research and early production environments. Hybrid manufacturing platforms that combine additive and subtractive operations in a single machine are enabling tighter dimensional tolerances on printed surfaces that interact with mating components, addressing one of the key limitations of standalone additive processes. These hybrid systems are attracting investment from Tier-1 aerospace suppliers seeking to expand the range of components they can transition from conventional to additive processes.

The concept of the digital warehouse, in which an inventory of certified CAD files replaces physical stock, is gaining traction as a supply chain strategy for aerospace MRO operators. Rather than holding millions of individual spare parts in physical warehouses, airlines, defense operators, and spacecraft service providers can store design files and print parts on demand at certified manufacturing facilities close to the point of need. This model reduces inventory carrying costs, eliminates obsolescence risk for parts tied to out-of-production aircraft types, and shortens aircraft-on-ground (AOG) recovery times for critical spares. Lufthansa Technik and Premium AEROTEC have demonstrated this model with EASA-approved 3D-printed metallic spare parts, establishing a regulatory and commercial precedent that others in the industry are actively pursuing.

The aerospace 3D printing market faces substantial technical and institutional challenges that constrain adoption at scale. Material qualification and process certification represent the most significant barriers, requiring extensive testing, documentation, and regulatory review before printed parts can enter operational service. The qualification of a new material-process combination for a specific aerospace application can take two to five years and cost millions of dollars, creating high barriers particularly for smaller additive manufacturing providers and new entrants without established relationships with aviation authorities. Consistency of mechanical properties across print batches, sensitivity to powder quality and recoating parameters, and the management of residual stress in metal components are ongoing technical challenges that require advanced process monitoring and quality assurance systems. Cybersecurity risks associated with digital design files, including theft of proprietary component geometries and unauthorized modification of print parameters, are also drawing increasing attention from defense customers and aviation regulators.

Structural cost and supply chain restraints further moderate the pace of market expansion. High-quality metal powders for aerospace-grade printing, particularly titanium, nickel superalloys, and aluminum-lithium alloys, remain expensive relative to bulk material costs in conventional manufacturing, and supply chains for aerospace-qualified powders are concentrated among a limited number of qualified producers. Capital expenditure requirements for industrial-grade metal AM systems capable of producing flight-certified components range from USD 500,000 to over USD 5 million per unit, creating adoption barriers for smaller aerospace suppliers and emerging market manufacturers. Powder recyclability, process waste management, and the energy intensity of high-temperature sintering and melting processes are also attracting scrutiny under evolving sustainability frameworks adopted by aerospace OEMs committing to carbon neutrality targets. Regulatory divergence across national certification frameworks adds compliance complexity for globally operating aerospace suppliers seeking to qualify printed parts for multiple markets simultaneously.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The aerospace 3D printing market presents multi-dimensional growth opportunities that position well-resourced participants for sustained competitive advantage. The commercial space economy, growing at an unprecedented pace driven by satellite mega-constellations, reusable launch vehicles, and orbital service platforms, represents one of the highest-value demand segments for aerospace additive manufacturing, with essentially no legacy manufacturing constraint on adoption since many space components have no conventional manufacturing precedent. The MRO segment for aging commercial aircraft fleets provides a recurring, economically compelling use case for on-demand printed spare parts, estimated to represent a multi-billion dollar addressable opportunity as airworthiness authorities refine approval pathways. Advanced material innovations including high-entropy alloys, ceramic matrix composites, and multi-material gradient structures are creating next-generation component possibilities. Strategic collaborations between additive manufacturing technology providers, material scientists, aerospace OEMs, and national research institutions continue to expand the certified application envelope. Stakeholders seeking granular intelligence on technology adoption timelines, segment-level revenue forecasts, and competitive positioning are encouraged to access the complete Expert Market Research Aerospace 3D Printing Market Report 2026-2035.

The Expert Market Research Aerospace 3D Printing Market report provides comprehensive segmentation across printing technology, offering type, platform, application, and end use, enabling precise identification of the highest-growth investment and entry points.

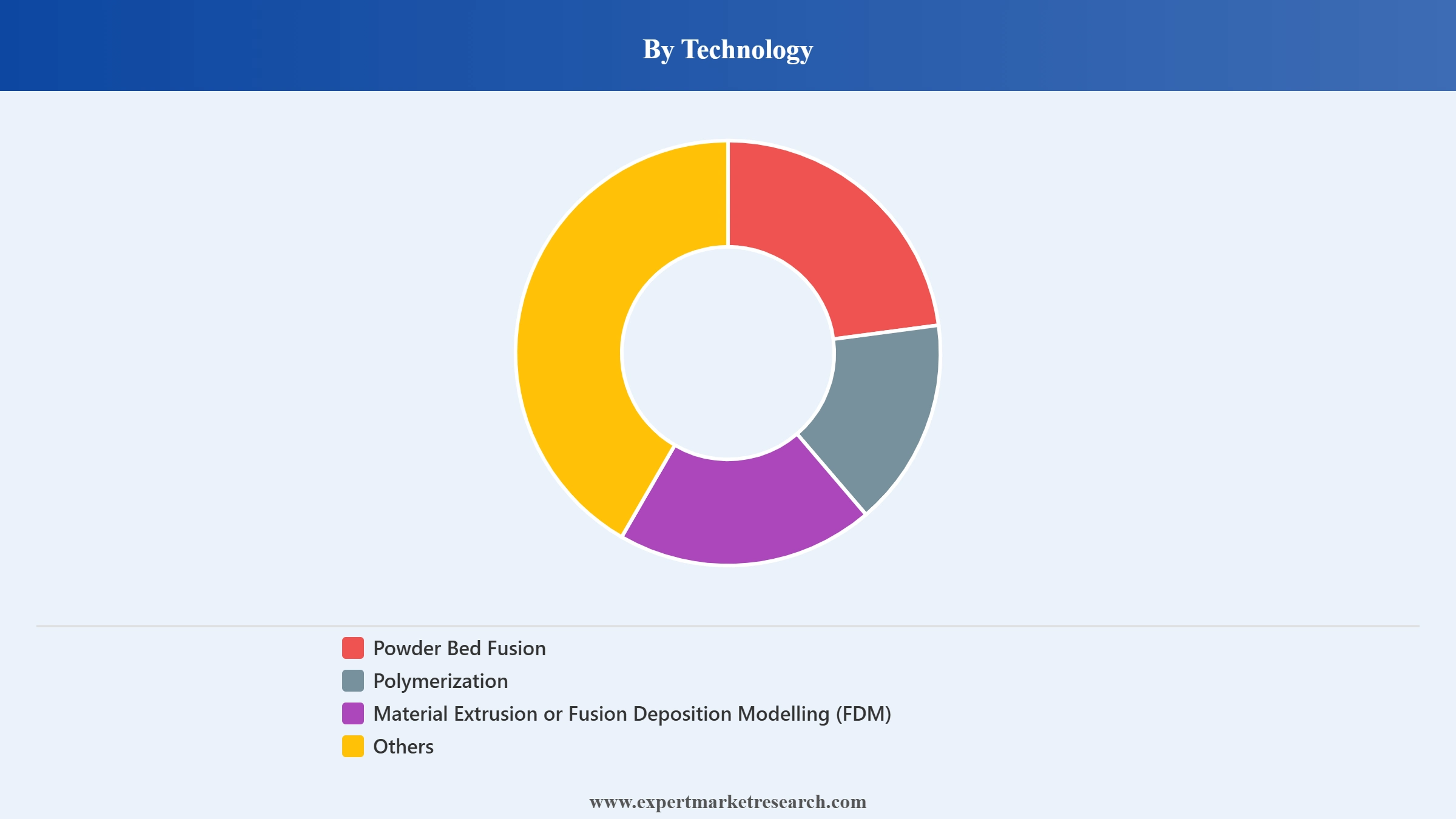

By technology, the market is segmented into:

Key Insights: The aerospace 3D printing market spans four core technologies driving additive manufacturing adoption. Powder bed fusion leads the market, producing high-density certified metal components including turbine blades and fuel nozzles. Polymerization delivers superior surface resolution for detailed prototypes and aerodynamic models. Fused deposition modelling commands the largest installed base, widely used for tooling, cabin fittings, and ducting using qualified thermoplastics. Directed energy deposition, binder jetting, and wire arc additive manufacturing address large-format structural fabrication and component repair requirements.

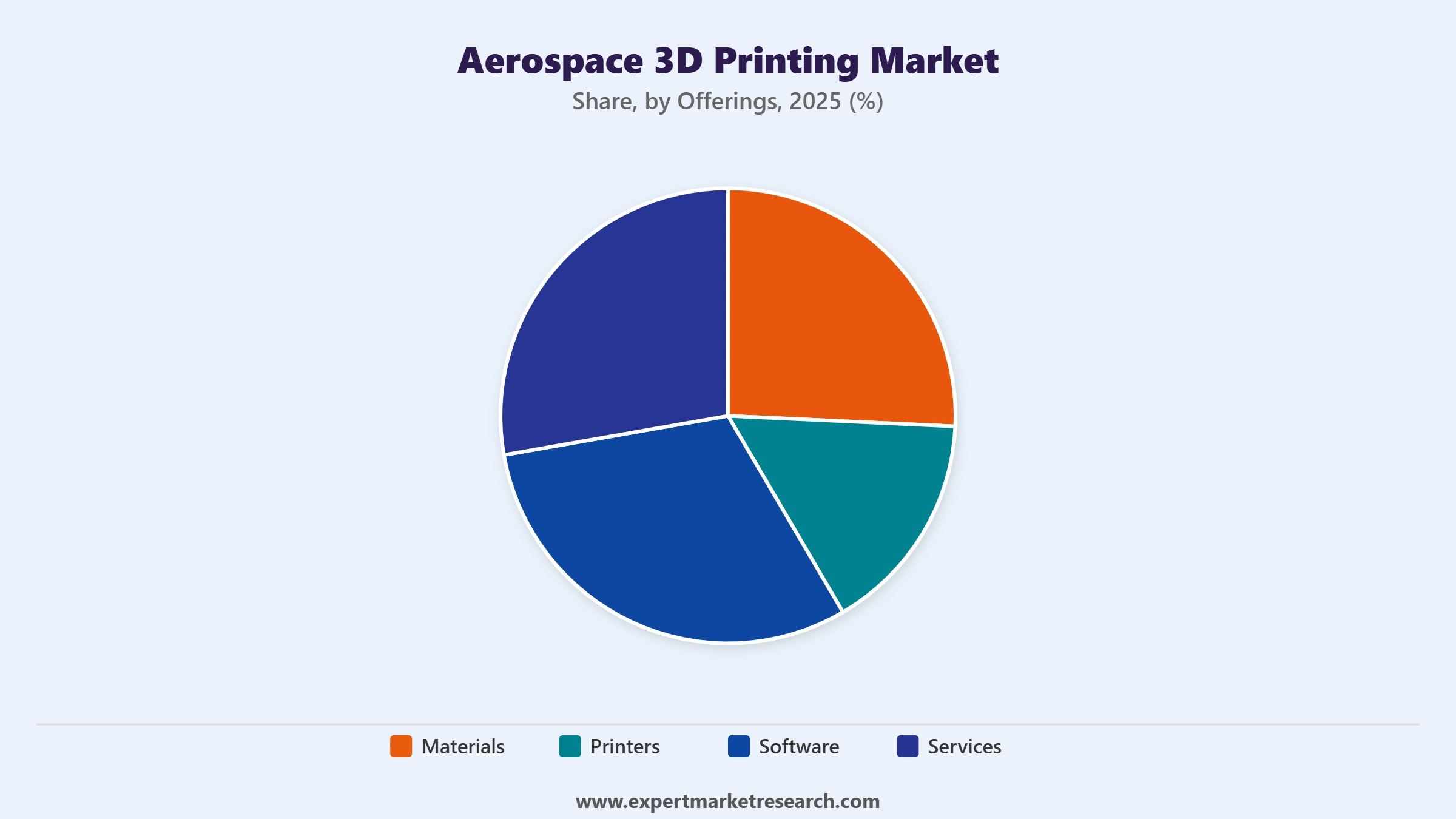

By offerings, the market is classified into:

Key Insights: Across offerings, printers represent the largest revenue segment, supported by sustained OEM capital investment in industrial AM systems. Materials is the fastest-growing category, driven by demand for aerospace-qualified titanium, nickel superalloys, and high-performance polymers. Software platforms covering topology optimization, simulation, and digital twin integration are expanding rapidly. Services, including bureau manufacturing, certification support, and post-processing, enable aerospace companies without in-house capability to access qualified additive manufacturing production.

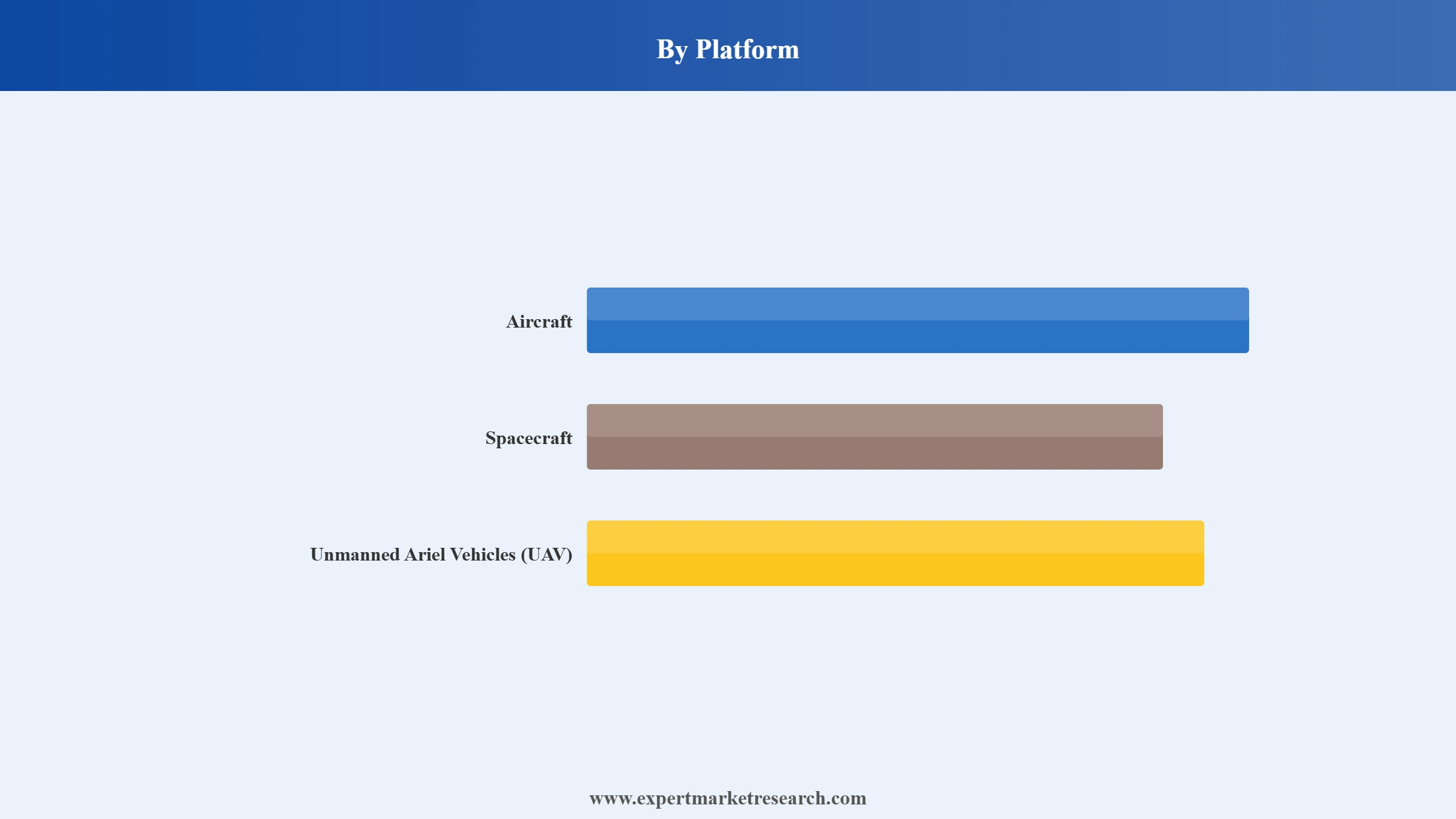

By platform, the market is divided into:

Key Insights: Aircraft constitutes the largest platform segment, with commercial and military programmes deploying AM extensively across engine components, structural parts, and cabin systems. Spacecraft is the fastest-growing platform, driven by reusable launch vehicles, satellite constellations, and deep-space missions requiring complex printed propulsion and structural components. Unmanned aerial vehicles are projected to register the highest platform-level CAGR, as military and commercial UAV programmes benefit directly from AM's design flexibility and low-volume production economics.

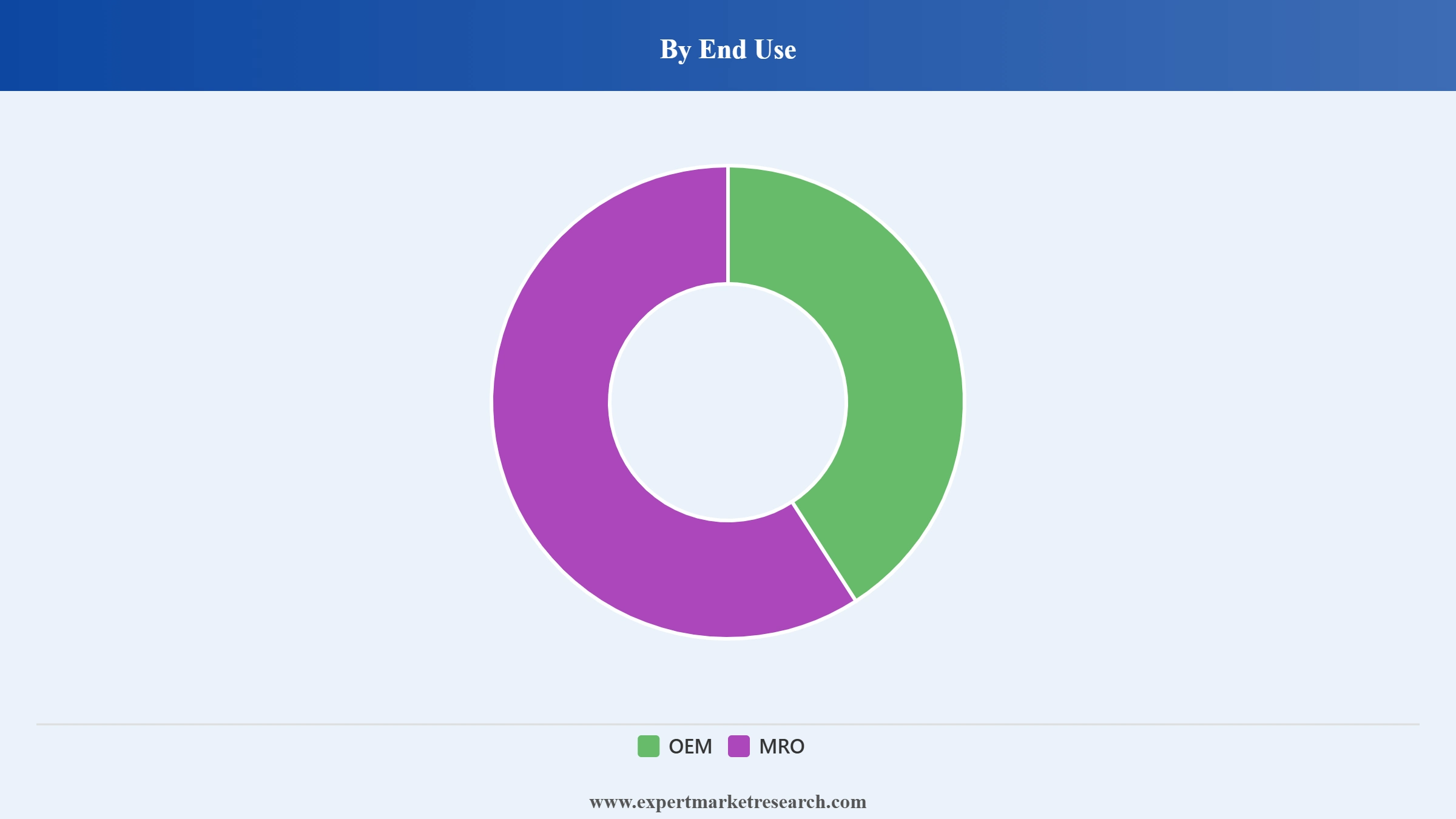

By end use, the market is segmented into:

Key Insights: OEMs represent the dominant end-use segment, with Boeing, Airbus, GE Aerospace, and Lockheed Martin deploying certified AM across engine, structural, and interior programmes. The MRO segment is growing rapidly as airlines and military operators adopt additive manufacturing to produce on-demand spare parts, address obsolescence challenges, and reduce aircraft-on-ground recovery times. The digital warehouse model, replacing physical stock with certified CAD file libraries, is accelerating MRO adoption globally.

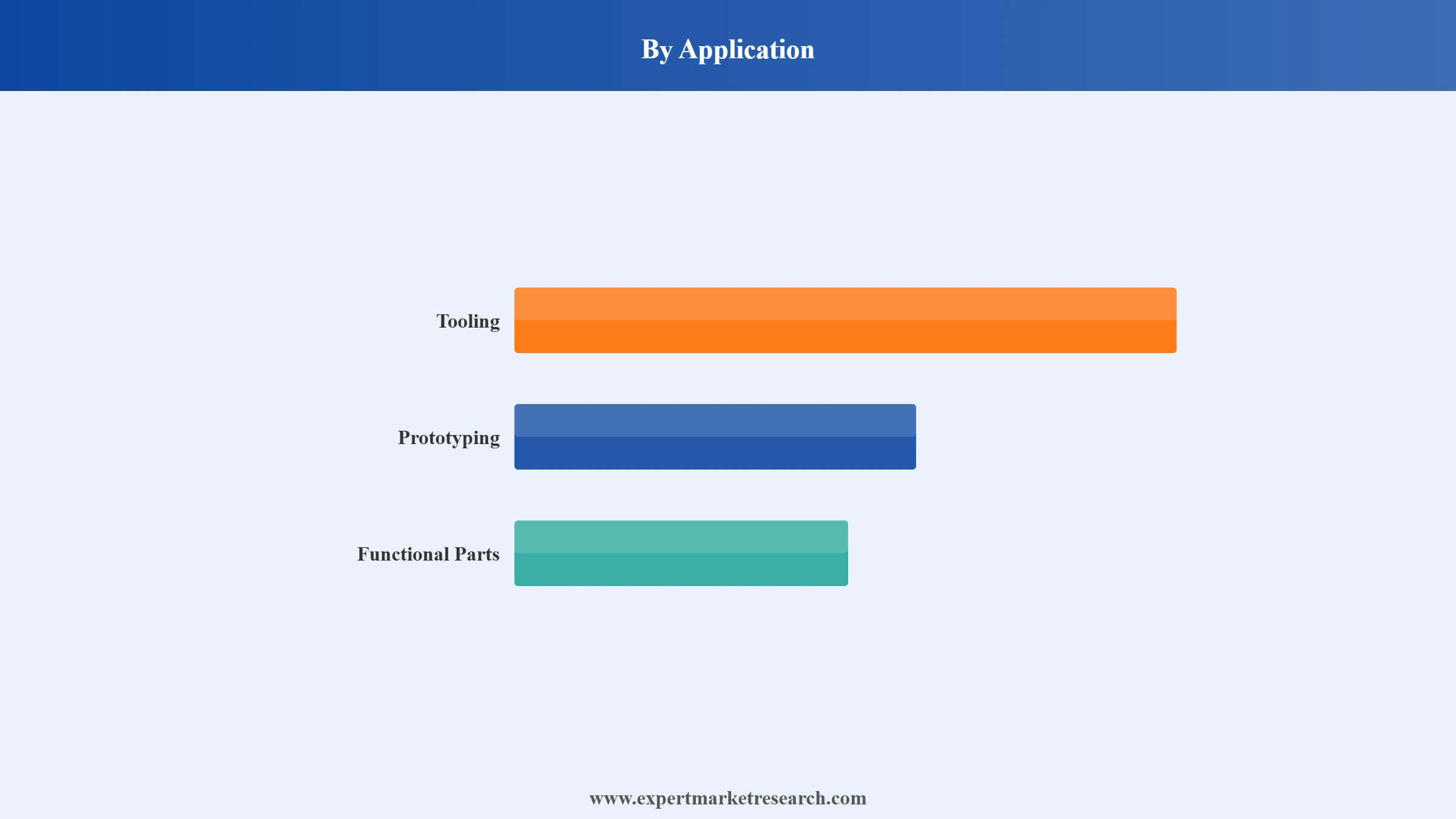

By application, the market is divided into:

Key Insights: Tooling was the earliest commercially viable aerospace AM application, with printed jigs, fixtures, and assembly aids significantly reducing procurement costs and lead times. Prototyping enables rapid design iteration across UAV, eVTOL, and next-generation aircraft programmes at lower cost than conventional methods. Functional parts represent the highest-growth segment, with flight-certified engine components, structural brackets, and cabin fittings now entering certified serial production as regulatory qualification frameworks and material certification databases progressively expand.

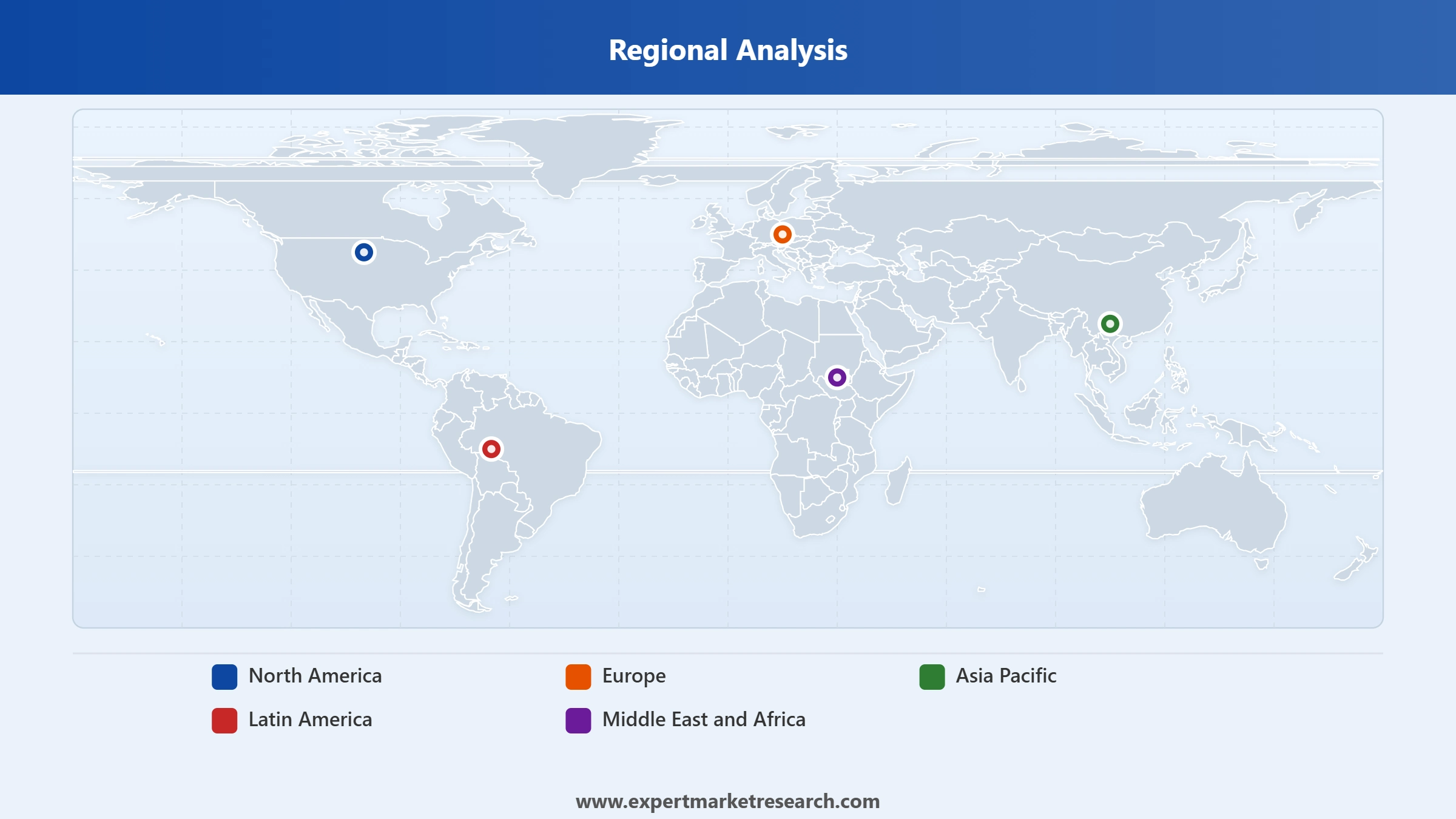

By region, the market is classified into:

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the largest and most advanced regional market for aerospace 3D printing, anchored by the comprehensive aerospace manufacturing ecosystem of the United States. The US market benefits from the concentrated presence of major aerospace OEMs including Boeing, Lockheed Martin, Northrop Grumman, and Raytheon Technologies, all of which have integrated additive manufacturing into their production processes. GE Aerospace operates one of the world largest certified aerospace AM production programs, having printed over 100,000 fuel nozzle tips for its LEAP engine family. The presence of specialized AM technology companies including Velo3D, Desktop Metal, Markforged, and leading material providers creates a deep and competitive supply chain. NASA and the US Department of Defense have directed significant research and procurement funding toward additive manufacturing capability development, reinforcing technology maturity and certification progress. Canada contributes through aerospace maintenance and regional aircraft manufacturing, with growing adoption of AM in MRO operations. The region is projected to maintain leadership through the forecast period, supported by fleet renewal programs and ongoing defense modernization.

Europe is the second-largest regional market, driven by a mature aerospace manufacturing base anchored by Airbus, Rolls-Royce, Safran, MTU Aero Engines, and Leonardo. Germany represents the largest national market within Europe, with EOS GmbH one of the world foremost powder bed fusion technology providers headquartered in Munich. The UK and France are significant markets, supported by Rolls-Royce engine manufacturing investments in additive manufacturing and Safran's adoption of 3D-printed titanium components. EASA has established progressive certification frameworks for additive manufactured parts, including the 2022 approval of the first load-bearing metallic AM spare part jointly developed by Lufthansa Technik and Premium AEROTEC. Airbus uses additive manufacturing for cabin brackets, tool production, and is advancing toward structural component applications. The EU's Clean Aviation programme and national industrial policy frameworks supporting advanced manufacturing are reinforcing investment in aerospace AM across member states.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR significantly above the global average, driven by fleet expansion, indigenous aircraft programs, and increasing defense investment across China, India, Japan, and South Korea. China holds the largest national market share within the region, supported by COMAC's C919 and CR929 commercial aircraft programs, state investment in aerospace AM research, and the rapid growth of domestic space launch programs. India is the fastest-growing national market, driven by the government's aerospace manufacturing incentive schemes, the emergence of domestic launch vehicle companies such as Agnikul Cosmos, and investment by DRDO in additive manufactured defense components. South Korea's KARI has demonstrated world-first space-grade titanium additive manufacturing. Japan's established aerospace suppliers including Kawasaki Heavy Industries and Mitsubishi Heavy Industries are advancing AM adoption in aircraft component production. Australia is contributing through collaborative research programs between Boeing and domestic material suppliers.

Latin America represents a nascent but developing market for aerospace 3D printing, led by Brazil and Mexico. Brazil's aerospace sector, anchored by Embraer, is the primary driver, with additive manufacturing adoption focused on prototyping and tooling applications and gradually expanding into certified component production. Mexico's growing role as an aerospace manufacturing hub within North American supply chains, particularly for wire harness, aerostructures, and MRO, is creating demand for AM capabilities to support lean manufacturing and supply chain agility. Limited local AM material supply chains and nascent regulatory frameworks for additive manufactured part certification constrain adoption but represent addressable opportunities as local aerospace manufacturing capacity grows.

The Middle East and Africa region is at an early stage of aerospace 3D printing market development but presents significant long-term potential driven by infrastructure investment and aviation fleet expansion. The UAE is the leading national market within the region, supported by the government's commitment to building a diversified aerospace manufacturing sector and the presence of major carriers Emirates and Etihad creating demand for MRO services. The UAE government invested over USD 22 billion in airport expansion projects, establishing a foundation for aviation services growth. South Africa represents the most developed aerospace manufacturing market within Sub-Saharan Africa. The region faces challenges including limited local expertise in advanced additive manufacturing and an evolving regulatory framework for AM component certification, but national aerospace strategies in Saudi Arabia, UAE, and Turkey are channeling investment into advanced manufacturing capabilities.

The report presents a detailed analysis of the following key players in the global aerospace 3D printing market, looking into their capacity, and latest developments like capacity expansions, plant turnarounds, and mergers and acquisitions:

Stratasys Ltd., headquartered in Eden Prairie, Minnesota, United States, is a global leader in polymer additive manufacturing solutions. Founded in 1989, the company develops and manufactures a broad range of 3D printing systems, materials, and services serving aerospace, defence, automotive, and healthcare industries. Its key product lines include the F900, Fortus, J850, and Origin platforms. Stratasys-qualified materials including Antero 800NA and Antero 840CN03 are certified for aerospace production in collaboration with Boeing, Northrop Grumman, Raytheon, and the US Air Force.

3D Systems, Inc., headquartered in Rock Hill, South Carolina, United States, is one of the pioneers of additive manufacturing, founded in 1986 by Chuck Hull, the inventor of stereolithography. The company offers a comprehensive portfolio of 3D printing technologies including SLA, SLS, DMP metal printing, and multi-jet printing, serving aerospace, defence, healthcare, and industrial sectors. Its Aerospace and Defence division is projected to become its largest and fastest-growing business in 2026, with revenue from production systems and custom metal parts forecast to surpass USD 35 million, supported by active US Air Force development programmes.

EOS GmbH Electro Optical Systems, headquartered in Krailling, Germany, is a world-leading provider of industrial powder bed fusion systems for both metal and polymer additive manufacturing. Founded in 1989, the company specialises in laser sintering and direct metal laser sintering (DMLS) technologies that are widely adopted across aerospace, defence, and space programmes globally. Its platforms including the EOS M 290 and EOS M 400-4 are extensively used by aerospace OEMs and Tier-1 suppliers for producing certified, flight-ready engine components, structural brackets, and turbine hardware from titanium, Inconel, and aluminium alloys.

Norsk Titanium US Inc., headquartered in Plattsburgh, New York, United States, is a specialist additive manufacturing company focused on the production of structural titanium components for the aerospace industry using its proprietary Rapid Plasma Deposition (RPD) wire arc additive manufacturing technology. Founded in 2007 and originally established in Norway, the company became the world's first FAA-approved manufacturer of 3D-printed structural titanium aircraft components. Its RPD process deposits titanium wire in a controlled argon atmosphere, producing near-net-shaped structural parts with significantly reduced material waste and lower buy-to-fly ratios compared to conventional machining from titanium billet.

The Expert Market Research report gives an in-depth insight into the industry by providing a SWOT analysis as well as an analysis of Porter's Five Forces model. The report covers the key players in the aerospace 3D printing market, including Ultimaker BV, Materialise NV, Aerojet Rocketdyne Holdings Inc., Velo3D Inc., Desktop Metal Inc. (ExOne), MTU Aero Engines AG, Lockheed Martin Corporation, and Safran Group, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 15.70% between 2026 and 2035.

The major drivers of the market include the need to reduce the production time of components, requirement for cost-efficient and sustainable products, advancements in 3D printing technology, increasing adoption of 3D printers into manufacturing processes across industries, and growing adoption by leading companies.

The low volume production of aircraft components in the aerospace industry and rising demand for lightweight components are the key industry trends propelling the market's growth.

Air ducts, wall panels, metal structural components, gasoline tanks, intricate gear cases and covers, transmission housings, structural hinges, lightweight engine parts, and other elements are among the lighter and more durable items that 3D printing can produce. It helps in creating sophisticated, complicated design geometries that maximise design performance in a aircraft.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The various technologies involved in the market are powder bed fusion, polymerisation, and material extrusion or fusion deposition modelling (FDM), among others.

Based on offering, the market is classified into materials, printers, software, and services.

The several platforms in the market are aircraft, spacecraft, and unmanned ariel vehicles (UAV).

The end-uses of the market are OEM and MRO.

The major applications of the market are tooling, prototyping, and functional parts.

Metal brackets that have a structural purpose inside of aircraft are made using aerospace 3D printing. As more prototypes are 3D printed, designers may improve the shape and fit of completed items.

The major players in the industry are Stratasys Ltd, 3D Systems, Inc., EOS GmbH Electro Optical Systems, Norsk Titanium US Inc., Ultimaker BV, Materialise NV, Aerojet Rocketdyne Holdings Inc., Velo3D Inc., Desktop Metal Inc. (ExOne), MTU Aero Engines AG, Lockheed Martin Corporation, and Safran Group, among others.

In 2025, the global aerospace 3D printing market reached an approximate value of USD 4.53 Billion.

The market is expected to witness robust expansion and reach approximately USD 19.47 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by Offerings |

|

| Breakup by Platform |

|

| Breakup by End Use |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.