Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global anti-fog additives market attained a value of USD 388.09 Million in 2025 and is projected to expand at a CAGR of 4.60% through 2035. The market is further expected to achieve USD 608.48 Million by 2035. The increasing adoption of controlled environment agriculture, as well as increased usage of high transparency food packaging, is driving the growth of the market, while increasing visibility and minimizing waste, along with offering a means to differentiate products.

There are two major factors that are contributing to growth in the anti-fog additives market. The first one involves rapid growth in greenhouse cultivation in Asia and Europe, resulting in the consistent need for anti-fog films that increase production efficiency. The second driving factor involves growing investment in premium food packaging, which encourages converters to use additives that retain clarity irrespective of temperature gradient changes.

The anti-fog additives market is now experiencing a definite shift towards specialty additives formulated specifically for their performance qualities. For instance, in May 2024, Clariant l aunched PFAS-free additives and sustainable plastic solutions, enhancing recyclability, efficiency, and reducing environmental impact at NPE 2024. Anti-fog additives from Clariant have been proven to provide fog prevention by a significant extent when compared to the previous generation. The technological shift is being driven by the growing demand for performance-enhancing products that provide longer shelf life while complying with food safety standards across different regions worldwide.

Innovation in the anti-fog additives market is continuously driven by changes occurring in both the packaging industry and controlled environment agriculture. For example, in February 2026, Cosmo Films introduced a new sealable, peelable transparent anti-fog BOPET (PET) lidding film intended for use in packaging refrigerated and fresh foods. With increasing globalization of fresh produce logistics networks, there is an increased focus on enhancing product visibility in the package, ensuring shelf attractiveness of the product, and managing internal humidity levels. Additive manufacturers are also modifying their product formulations to enable compatibility with recyclable mono material films, primarily made of polyethylene and polypropylene. Simultaneously, regulatory authorities in regions such as Europe are advocating for low migration and safer additive chemistries, which calls for innovations in the surfactant chemistry used.

Compound Annual Growth Rate

4.6%

Value in USD Million

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Recyclable mono-material food packaging was introduced by Siegwerk, Borouge, and TPN Food Packaging for packaging circularity and better barrier properties. Innovations such as these create opportunities for the development of recyclable and food-safe anti-fog additives designed for compatibility with mono-material packaging.

Avient unveiled Cesa Max flame-retardant additives that were developed considering strict industrial safety regulations as well as efficient plastic production processes. Developments like these create opportunities for anti-fog additives market players to design recyclable, food-safe formulations compatible with mono-material packaging structures.

Tosaf developed high-performance anti-fogging solutions for packaging film materials that demand prolonged transparency, moisture barrier properties, and visibility on shelves. This highlights how other players can design resilient anti-fogging technology to cater to needs associated with prolonged freshness, visibility at point-of-sale, and sustainable food packaging systems.

Kraton launched Nexar anti-fog coatings and films intended for protective eyewear products, boosting the anti-fog additives market growth. This illustrates the prospects for manufacturers to develop anti-fog technology in healthcare, industrial, and sports eyewear sectors.

One of the prevailing trends affecting the development of the market is related to the emergence of food-compatible and environment-compliant formulas. Regulatory agencies, such as the European Food Safety Authority, are introducing stricter restrictions on the permissible levels of migration of additives used in food packaging products, thus urging developers to create non-toxic substances with minimal volatility. For example, companies like Croda International are developing eco-friendly anti-fog additives, made using renewable sources. Aligning with such trends in the anti-fog additives market, in December 2025, Cosmo Films introduced high-barrier anti-fog packaging films for pet food, improving durability, freshness retention, and food-safe performance.

With the rising popularity of mono-material packaging solutions, researchers focus on ways to ensure the effectiveness of anti-fog additives on films made of polyethylene. For example, Ampacet offers a masterbatch solution compatible with films made of polymers while maintaining high optical clarity. On the other hand, in November 2023, Coveris launched recyclable MonoFlex thermoform packaging, improving barrier performance, sustainability, shelf-life, and reducing non-recyclable plastic waste, positively impacting the anti-fog additives market trends and dynamics. Legislative initiatives aimed at introducing circular economy principles, especially in the European Union, promote innovations in this regard. Thus, developers are increasingly creating additive formulas for use in specific types of recyclable films.

The proliferation of greenhouses and vertical farms is increasing demand in the anti-fogging additives market. In these applications, it is vital to avoid any condensations because they would block the sun's rays, affecting the harvest negatively. As noted by agricultural development programs in the Netherlands, greenhouse efficiency could be improved significantly by increasing its ability to transmit light. Companies, such as BASF, are developing specialized additives designed for agricultural films to ensure their continued effectiveness under any level of moisture. These additives find application in food-producing countries interested in securing their food supply and utilizing their lands effectively. In April 2026, Bird-X expanded its liquid bird deterrent portfolio with Avian Control Repellent and InvisiDye UV Marker launch.

Another emerging trend in the anti-fog additives market involves collaboration between the providers of additives and the manufacturers of films. Unlike before when firms used to market generalized products, the industry is now embracing the trend of customizing additives to fit the needs of different clients. For instance, Clariant collaborates with packaging converters to develop customized anti-fogging systems for refrigerated food transportation. Through such collaborations, manufacturers can enter into agreements lasting for several years while avoiding competition based purely on pricing. In December 2023, BASF launched Irgastab PUR 71 antioxidants, improving polyurethane foam sustainability, emissions reduction, regulatory compliance, and performance.

Development of R&D infrastructure with respect to simulation laboratories is yet another trend observed in the anti-fog additives market. In this case, companies develop simulation labs where additives can be subjected to tests under realistic conditions including temperature changes, varying humidity levels, and longer periods of storage. The development of such labs enables companies to validate the efficacy of anti-fog additives before bringing them into the market. For example, in January 2026, Avient expanded Hiformer non-PFAS process aids with liquid grades, improving polyolefin film efficiency, sustainability, and regulatory compliance.

The Expert Market Research's report titled “Global Anti-Fog Additives Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

The industry can be broadly categorised on the basis of type into:

Key Insight: The anti-fogging additives market report indicates that consumers make decisions based on cost and performance criteria. The most popular additive is glycerol ester because of its cost-effectiveness and reliable clarity. Polyglycerol ester is more durable in extreme situations, although it is not as inexpensive as glycerol ester. Sorbitan esters of fatty acids maintain their relevance in conventional applications, while ethoxylated sorbitan esters are gaining traction owing to their increased stability. Polyoxyethylene esters of oleic acid provide unique functions in special film types. The category of gelatin and titanium dioxide observe limited use in specific cases.

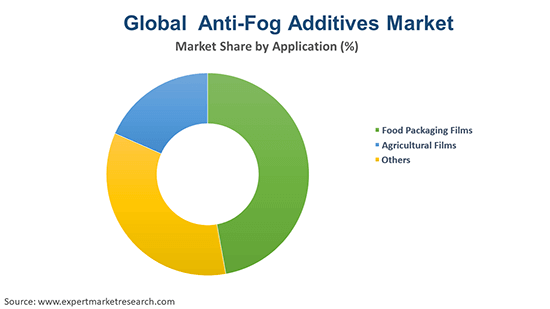

The industry can be divided on the basis of application as:

Key Insight: In terms of the end use, the anti-fog additives market is influenced by the application requirements in packaging and agriculture. Food packaging films account for the largest share of the market as a result of the need for clarity and moisture resistance in retail and logistics settings. Agricultural films are rapidly growing as greenhouse farming increases in both popularity and sophistication. In April 2026 , SPR expanded Texas agricultural film manufacturing with ExxonMobil polymers, improving durability, crop protection, efficiency, and sustainable farming solutions. Industrial and specialty films make up other applications within the market based on specific performance requirements. In each case, the key driving factors remain improved visibility, durability, and environmental adaptability.

Looks into the regional anti-fog additives markets like:

Key Insight: The current regional dynamics of the anti-fog additives market demonstrate different characteristics for various reasons. The Asia Pacific region leads market growth due to its vast industrial base and agricultural practices, with expanding manufacturing capabilities. Europe demonstrates rapid development with regard to sustainability and innovation in packaging solutions. North America remains stable with its demand because of highly developed packing and supply chain systems. Latin America offers promising prospects in agriculture, while the Middle East and Africa begin to adopt anti-fog solutions as well.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, glycerol esters accounts for the dominant share of the market due to superior clarity retention and cost efficiency

The glycerol ester-based anti-fog additives retain their dominant share in the anti-fog additives market owing to its efficiency in terms of fog dispersal along with ensuring optical clarity over the prolonged periods of storage and use cases. The growing optimization of these additives with regard to minimizing blooming effect and ensuring consistent migration through polymer films, combined with the low cost of production, makes them especially popular in the packaging sector. Moreover, their compatibility with polyethylene films further supports their popularity, considering their broad-scale use in flexible packaging. In June 2025, Palsgaard expanded plant-based anti-fog additives portfolio, enhancing food packaging transparency, sustainability, shelf-life, and regulatory compliance.

Ethoxylated sorbitan esters are anticipated to record the highest growth rate within the anti-fog additives market scope due to their improved performance when it comes to the emulsion process, along with a longer-term action at various temperatures. Due to their better dispersion capabilities, these additives are able to ensure optimal anti-fog properties in a wide range of products. Currently, there is an increasing interest in developing customized ethoxylation for certain products, including multilayer films. Additionally, due to improved characteristics, these additives are gaining popularity in premium packaging solutions.

Food packaging films dominate the application segment of the global market due to rising demand for clarity

The largest application segment in the anti-fog additives market is represented by food packaging films, owing to the increased importance given to visibility and presentation within retail settings. Additives that prevent fogging are essential for clear packaging of fresh foods such as fruits and vegetables, dairy products, and ready-to-eat meals because any appearance of condensation could affect consumer acceptance. Moreover, there is an increasing trend of manufacturers designing additives for use in packaging that is stable at low temperatures and can withstand varying conditions during storage and transport. Additives designed to ensure recyclability and mono-materiality must be capable of providing consistent results without impacting clarity. In March 2026, Innovia Films launched a recyclable P2G BOPP film, improving fresh produce shelf-life, packaging sustainability, clarity, and food waste reduction.

The farming films category is one of the fastest-growing application segments that is boosting the anti-fog additives market value. This segment’s growth is being fueled by the increase in the usage of controlled-environment agriculture. Anti-fog additives serve the purpose of preventing water drops from films used in greenhouse cultivation. These add-on features enable light to pass through the films, thus increasing productivity. Manufacturers need to design additives that can provide consistent results even after prolonged exposure to humidity and ultraviolet rays.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific clocks in the largest market share due to strong packaging manufacturing base

Asia Pacific holds the dominant share of the anti-fog additives market revenue owing to its robust packaging production capability and expanding food processing sector. Countries like China and India are witnessing an upsurge in demands for flexible packaging, especially for fresh and processed foods. The agricultural prowess of the region is also contributing to the use of anti-fog additives in greenhouse films. Producers are working towards developing affordable yet efficient anti-fog additives to serve end users in various sectors. Moreover, the increasing trend towards retail and e-commerce is stimulating demand for aesthetically pleasing packaging. In February 2025, Pellucere Technologies opened India’s first nano-coatings facility, advancing anti-fog technologies, glass performance, sustainability, and localized manufacturing capabilities.

Europe represents the fastest growing regional anti-fog additives market due to high regulatory standards and efforts aimed at ensuring sustainable packaging solutions. Europe's efforts to curb plastic waste generation are contributing to the uptake of sustainable and recyclable packaging solutions that, in turn, call for more sophisticated and eco-friendly anti-fog additives. Producers in the region are making considerable strides towards developing bio-based and low-migration anti-fogging additives to meet regulatory compliance and customer demand. The region boasts top chemical producers and advanced research and development infrastructure that foster product innovation. For example, in February 2026, hubergroup Chemicals launched ELARA additives brand, enhancing coating performance, pigment dispersion, sustainability, and regulatory-compliant formulation capabilities globally.

The market is moving towards performance-oriented innovations, with anti-fog additive companies focusing more on specialty products than on commoditized products. Top manufacturers are increasingly adopting multi-purpose additives that have anti-fog, anti-static, and slip functionalities to minimize the use of multiple components during film production.

There is an increasing interest in bio-based surfactants and low-migration chemistries due to the increased focus on recyclability and sustainability in applications like food packaging. Strategic options include co-development of customized solutions in collaboration with film convertors and agricultural film manufacturers. There is also increasing investment in pilot testing under real storage conditions, allowing anti-fog additives market players to forge long-term partnerships.

Croda International Plc, established in 1925 with its head office based in England, United Kingdom, is a producer of anti-fog additives sourced from sustainable feedstocks. The company is developing surfactant technology for use in safe food packaging. The sustainability-driven innovative model allows for the creation of products that help companies meet regulations without sacrificing performance in high-end packaging applications.

Emery Oleochemicals Sdn Bhd was founded in 1840 and based in Ohio, United States. The company uses renewable derivatives of oleochemicals as the foundation for its anti-fog additive production processes. The corporation serves the needs of the packaging industry, agriculture sector, and others. It aims at using natural ingredients as the source of additive performance in Asia Pacific markets.

Founded in 1847 and based in Essen, Germany, Evonik Industries AG places importance on high-quality specialty additives that employ state-of-the-art surfactant technology. Research and development efforts are directed toward formulating sustainable anti-fog products that can be used with intricate polymer formulations. Their product range aims to achieve consistency in fog avoidance and promote recyclable packaging projects and high-performance agriculture films around the world.

LyondellBasell Industries Holdings B.V. was formed in 2007 and is headquartered in Rotterdam, Netherlands. The company uses its anti-fog additive formulations as an integral part of its portfolio of polymer materials. It concentrates on compatibility with polyethylene and polypropylene films, accelerating growth in the anti-fog additives market. Its approach revolves around partnering with converters to formulate custom application-based formulas.

Other key players in the market include Ashland Global Specialty Chemicals Inc., Nouryon, Corbion N.V., and Clariant AG, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our anti-fog additives market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global anti-fog additives market attained a value of nearly USD 388.09 Million in 2025.

The market is projected to grow at a CAGR of 4.60% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 608.48 Million by 2035.

The major drivers of the market include rising population, growing urbanisation, and development in the food processing and packaging sectors.

Strategic innovations such as product launches and enhanced research and development operations in developing markets are the key trends propelling the growth of the market.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific, with North America accounting for the largest share in the market.

Glycerol esters, polyglycerol esters, sorbitan esters of fatty acids, ethoxylated sorbitan esters, polyoxyethylene esters of oleic acid, gelatin, and titanium dioxide, among others are the major types of anti-fog additives in the market.

Food packaging films and agricultural films, among others are the leading application sectors for anti-fog additives.

The major players in the global anti-fog additives market are Croda International Plc., Emery Oleochemicals Sdn Bhd, Evonik Industries AG, LyondellBasell Industries Holdings B.V, Ashland Global, Specialty Chemicals Inc., Nouryon, Corbion N.V., Clariant AG, Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.