Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

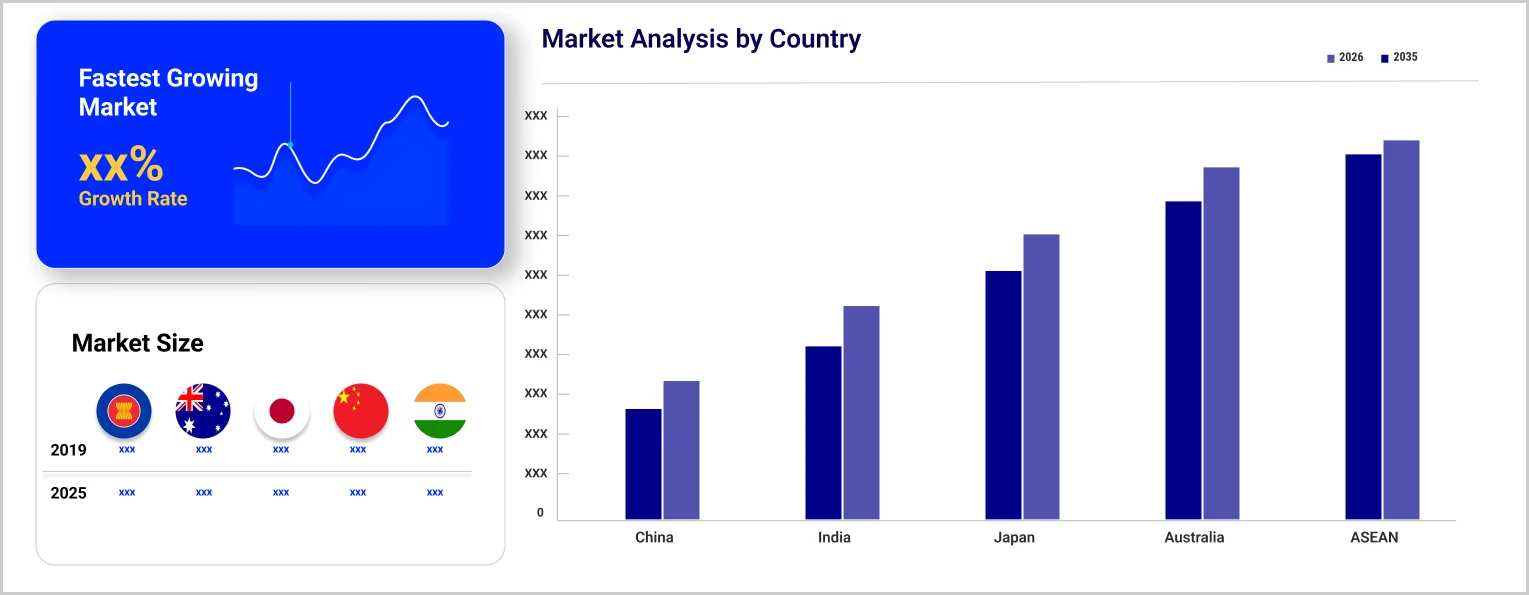

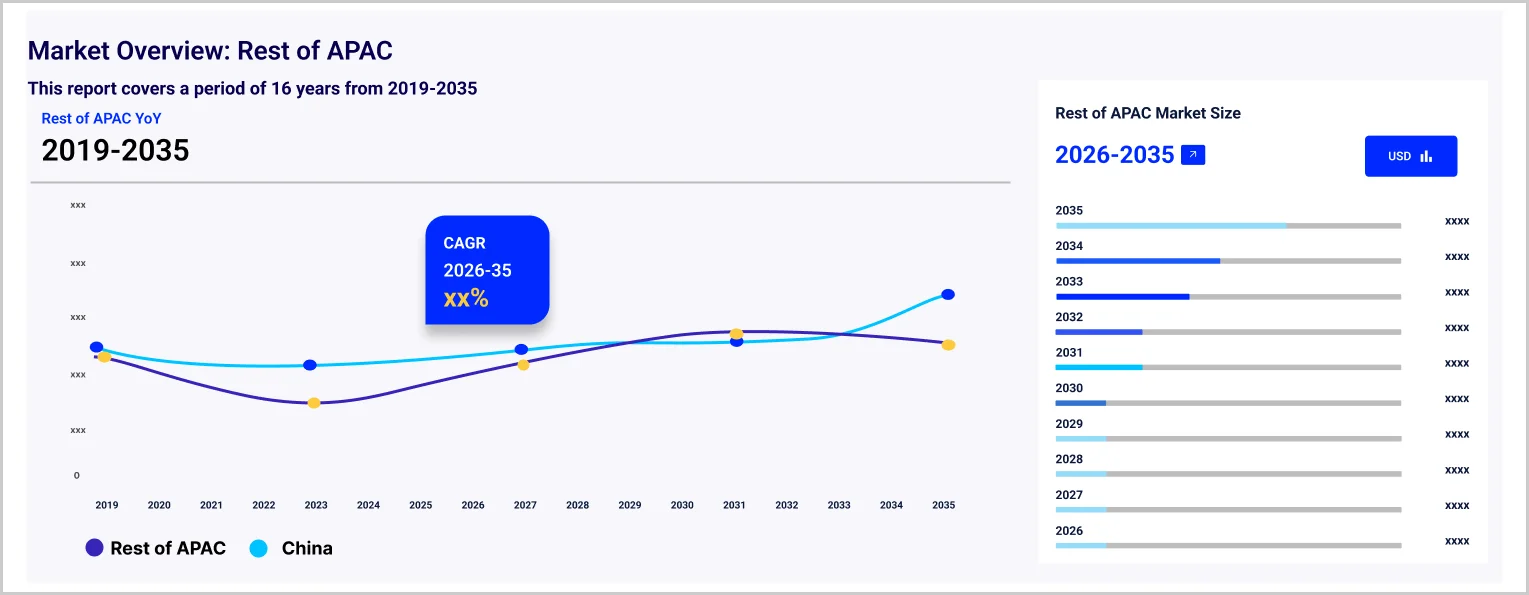

The anti-obesity drugs market size was valued at USD 2.77 Billion in 2025, with Asia Pacific holding a significant market share. The market is driven by the rising prevalence of obesity. It is expected to grow at a CAGR of 10.70% during the forecast period of 2026-2035, with the values likely to attain USD 7.66 Billion by 2035.

It is reported that the obesity prevalence rate in the Asia Pacific region is increasing rapidly. This surge in obesity rates is expected to augment the need for effective weight management solutions including anti-obesity drugs.

In January 2024, it was reported that Chinese biotechnology company Innovent Biologics Inc. and Eli Lilly and Company’s anti-obesity drug mazdutide achieved positive Phase III results, with data showing a significant reduction in body weight by week 32 and a majority of patients undergoing weight loss of 5% or more. The development of such innovative anti-obesity medications with higher efficacy and fewer side effects is expected to elevate the Asia Pacific anti-obesity drugs market value.

One of the major market trends is the rising development of biosimilar drugs to provide cost-effective alternatives for weight management. For instance, in April 2024, Hangzhou Jiuyuan Gene Engineering Co., Ltd. revealed that it is seeking marketing approval for Jiyoutai, the first biosimilar drug expected to provide strong competition to Novo Nordisk’s weight-loss and diabetes drugs portfolio in China.

Compound Annual Growth Rate

10.7%

Value in USD Billion

2026-2035

Anti-obesity drugs comprise medications that aid in reducing or controlling the weight of an individual such as appetite suppressants, fat absorption inhibitors, and metabolic enhancers. The rising public awareness regarding the risks associated with obesity like cardiovascular diseases, hypertension, and diabetes, is prompting obese patients to seek appropriate treatments including weight loss drugs. Further, increased initiatives from the government to combat obesity are expected to drive the Asia Pacific anti-obesity drugs market growth.

The high prevalence of obesity directly influences the market demand for anti-obesity drugs. It is reported that the obesity prevalence rate in the Asia Pacific region is growing rapidly. In China, over 50% of adults and nearly 20% of school-age children are experiencing overweight conditions . This surge in obesity rates can be attributed to changing dietary habits and increased sedentary lifestyles, which is expected to augment the need for effective weight management solutions, thereby boosting the market share of anti-obesity drugs.

One of the major Asia Pacific anti-obesity drugs market trends is the rising development of biosimilar drugs to provide cost-effective alternatives for weight management. For instance, in April 2024, a Chinese biopharmaceutical company Hangzhou Jiuyuan Gene Engineering Co., Ltd. revealed that it is seeking marketing approval for Jiyoutai (a biosimilar to semaglutide), the first biosimilar drug expected to provide strong competition to Novo Nordisk’s weight-loss and diabetes drugs portfolio in China. The increased access to a wide range of anti-obesity drugs in the region is anticipated to propel the market growth.

The Asia Pacific anti-obesity drugs market share is positively influenced by the ongoing research in obesity treatment solutions which is leading to the introduction of novel anti-obesity drugs. In January 2024, it was reported that Innovent Biologics Inc. (a Chinese biotechnology company) and Eli Lilly and Company’s anti-obesity drug mazdutide (a dual glucagon-like peptide-1 (GLP-1) glucagon receptor agonist) achieved positive Phase III results. In the GLORY-1 trial, the drug met both of its primary endpoints, with data showing a significant reduction in body weight by week 32 and a majority of patients undergoing weight loss of 5% or more. The development of such innovative anti-obesity medications with higher efficacy and fewer side effects is expected to elevate the market value.

The report offers a detailed analysis of the market based on the following segments:

Breakup by Drugs

Breakup by Drug Class

Breakup by Mechanism of Action

Breakup by Route of Administration

Breakup by Prescription Type

Breakup by Distribution Channel

Breakup by Region

The key features of the market report include patent analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players. The major companies in the market are as follows:

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Upto 15% Off

USD

$2699 $2429

$4299 $3869

$5799 $4949

$6999 $5949

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The Asia Pacific anti-obesity drugs market is expected to be driven by the rising demand for the global market, which is anticipated to grow at a CAGR of 10.70% during the forecast period of 2026-2035 and is likely to reach a market value of USD 7.66 Billion by 2035.

The rising obesity rates and increased initiatives from the government are fuelling the demand for the market.

One of the significant trends is the rising development of biosimilar drugs to provide cost-effective alternatives for weight management. For instance, in April 2024, Hangzhou Jiuyuan Gene Engineering Co., Ltd. revealed that it is seeking marketing approval for Jiyoutai, the first biosimilar drug expected to provide competition to Novo Nordisk’s weight-loss and diabetes drugs portfolio in China.

Based on the drugs, the market is segmented into semaglutide, phentermine/topiramate, naltrexone/bupropion, liraglutide, gelesis 100, orlistat, phentermine, methamphetamine, and tirzepatide.

Drug classes available in the market include amphetamine, GLP-1 receptor agonist, and lipase inhibitors.

By mechanism of action, the market is divided into centrally acting drugs and peripherally acting drugs.

The market breakup by route of administration includes oral and subcutaneous.

The market breakup by prescription type includes prescription drugs and over the counter drugs.

Distribution channels of the market are hospital pharmacies, drug stores, retail pharmacies, and online pharmacies.

The market segmentation by countries includes China, Japan, India, ASEAN, and Australia, among others.

The key players in the market are VIVUS Inc., Pfizer Inc., Novo Nordisk, Bayer AG, F. Hoffmann-La Roche, Glaxosmithkline, Arena Pharmaceuticals, Eisai Co. Ltd, Takeda Pharmaceutical Company, and Nalpropion Pharmaceuticals Inc.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Drugs |

|

| Breakup by Drug Class |

|

| Breakup by Mechanism of Action |

|

| Breakup by Route of Administration |

|

| Breakup by Prescription Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,699

USD 2,429

tax inclusive*

Single User License

One User

USD 4,299

USD 3,869

tax inclusive*

Five User License

Five User

USD 5,799

USD 4,949

tax inclusive*

Corporate License

Unlimited Users

USD 6,999

USD 5,949

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.