Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

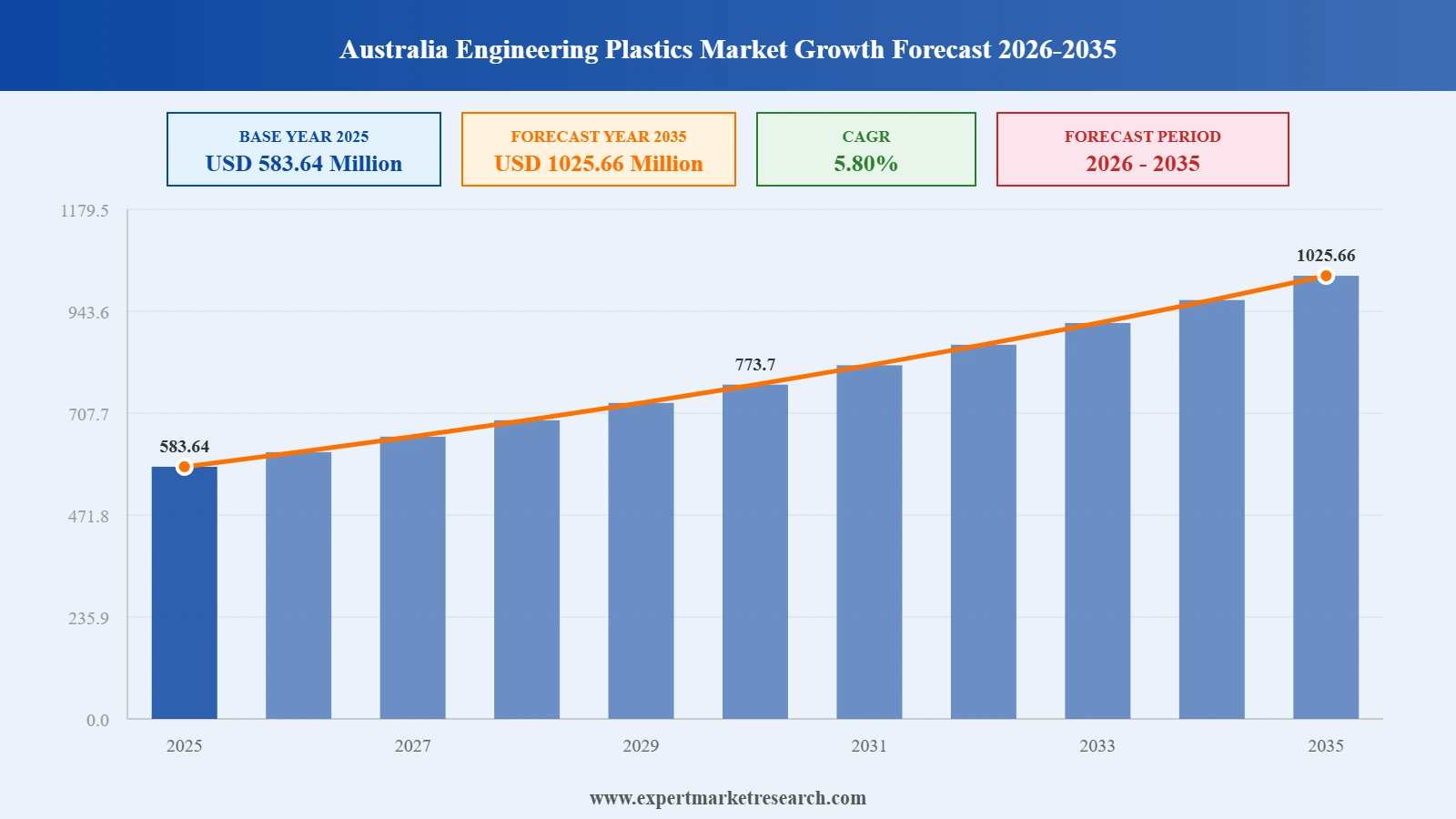

The Australia engineering plastics market size reached USD 583.64 Million in 2025. The market is expected to grow at a CAGR of 5.80% between 2026 and 2035, reaching almost USD 1025.66 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Engineering plastics, a class of synthetic resins with superior performance characteristics compared to conventional plastics, are witnessing increasing demand in Australia. These plastics offer stability across a wide temperature range and withstand mechanical stress, climate variations, and chemical exposure effectively. Australia’s push for manufacturing growth, particularly in electrical and electronic equipment production, is bolstering demand, driven by the surge in smart devices and domestic consumption.

The Australia engineering plastics market growth is further fuelled by the rising adoption of advanced technologies like digitalisation, robotics, IoT, and 5G connectivity. Local demand, coupled with fleet upgrades, is expected to boost aerospace component production. However, Australia currently relies heavily on imports to meet its engineering plastics demand.

Australia has initiated the National Plastics Plan, emphasising product stewardship through recycling and waste reduction. Engineering plastics find applications in various industries, including mechanical components, packaging, and containers, owing to their lightweight nature and performance advantages over metals and ceramics. These materials are increasingly replacing metals in construction and automotive sectors due to their durability, design flexibility, and high strength-to-weight ratios, contributing to improved fuel efficiency. The injection moulding process drives the Australian engineering plastics market development and demand by converting engineering plastics into essential end products.

Market expansion is primarily driven by the growing automobile industry amid urbanisation trends. In the electronics sector, the demand for engineering plastics is rising alongside the expansion of electronic and electrical industries, driven by increased consumer demand for electronic products.

The construction sector's boom, fuelled by rapid urbanisation, also contributes to market growth, as engineering plastics find applications in various construction materials. Additionally, the packaging industry's growth, driven by increased consumer goods demand, supports the engineering plastics market, given their role in packaging materials.

In the food and beverage sector, engineering plastics are witnessing high demand due to the rising need for packaging materials amid increasing demand for packaged food products. Overall, advancements in technology and changing consumer preferences are driving the expansion of the engineering plastics market across diverse industries in Australia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

"Australia Engineering Plastics Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Market Breakup by Performance Parameter

Market Breakup by Application

Market Breakup by Region

Key players in the engineering plastics in Australia research, develop and manufacture products while forming partnerships and mergers to support end users in the market.

Australia's engineering plastics market faces significant operational challenges driven by evolving regulatory expectations and sustainability obligations. The Australian Government's accelerating focus on plastic packaging reform, including proposals for mandatory Extended Producer Responsibility and national recyclability grading frameworks, is compelling manufacturers and downstream users to review material specifications, increase recycled content, and redesign formulations for end-of-life compliance. These obligations add technical and cost complexity to product development cycles, particularly for manufacturers operating across multiple packaging and industrial applications simultaneously.

Heavy import dependence represents a persistent structural restraint. Australia lacks domestic polymerisation capacity for most engineering polymer grades, making the market reliant on overseas production, primarily from Asian manufacturers. This exposes buyers to exchange rate volatility, freight cost fluctuations, and supply chain disruptions. Competition from low-cost imported engineering plastics continues to constrain pricing power for locally based processors and converters, while high domestic energy costs further reduce competitive parity against major producing economies.

Several structural growth opportunities are nonetheless emerging. Australia's AUKUS nuclear-powered submarine programme is creating sustained industrial demand for high-performance composites and glass-reinforced plastics within defence supply chains. The ongoing transition toward electric vehicles is generating demand for lightweight, heat-resistant engineering thermoplastics in battery enclosures and structural components. Additionally, the renewable energy and 5G infrastructure buildout are expanding consumption of specialised engineering polymer grades across construction, electronics, and industrial machinery applications.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is estimated to be valued at USD 583.64 Million in 2025.

The market is projected to grow at a CAGR of 5.80% between 2026 and 2035.

The engineering plastics market is expected to reach USD 1025.66 Million in 2035.

The market is categorised according to its performance parameter, which includes low performance, and high performance.

The key market players are Covestro AG, McNeall Plastics Pty Ltd., AJ Plastics Engineering Pty Ltd., Metal Manufactures Pty Limited., Solutions In Plastic & Engineering, Plasticut, Adarsh Australia, Intelsol Pty Ltd. T/A Australian Plastic Fabricators, Engineering Plastics on Line Pty Ltd., and others.

The market is driven by factors that include growing automobile industry amid urbanisation trends, increasing manufacturing growth, rising adoption of advanced technologies, among others.

The market is categorised according to its application, which includes electricals and electronics, automotive and transportation, industrial and machinery, consumer appliances, packaging and others.

Nylon stands out for its exceptional wear resistance and load-bearing capabilities, making it one of the most prevalent engineering plastics in use today. Components crafted from nylon weigh up to 80% less than their metal counterparts, offering a compelling advantage in various applications.

Polyethylene ranks among the most extensively utilised engineering plastics, prised for its adaptability and economical nature. Available in diverse forms including low-density polyethylene (LDPE) and high-density polyethylene (HDPE), it serves a multitude of purposes across industries.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Performance Parameter |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.